Last week we noted how a hive of millions of small, mainly young investors in the Reddit user group, r/wallstreetbets (“WSB”) targeted GME, the small, heavily shorted stock of troubled video game retailer GameStop. In a classic short squeeze, the stock price was driven up from a more or less rational price of $20 per share, to over $400.

Continue readingAuthor: Scott Buchanan

The GameStop Short Squeeze: Swarm of Small Investors Stings Wall Street Hedge Funds

If you think the price of a stock is going to go up, you can buy shares and wait for the price to go up, then sell the shares to someone else. This is called being “long” a stock. If it turns out that the stock price goes down and stays down, the most money you can lose is the amount you put in, since the stock price cannot go below zero.

But what if you think the stock price is going to go down instead of up? You may believe the price has run up irrationally high, or your analysis uncovers poor earnings prospects. A favorite tactic of Wall Street pros, including hedge funds, in this case is to “short” a stock.

How Whales Got To Be Whales

Although they live in the ocean like fish, whales are clearly mammals. A reasonably complete series of intermediate fossils have been found for the evolution of whales from terrestrial mammals. A sampling of these transitional species is shown below:

Continue readingThe Kalecki Profit Equation: Why Government Deficit Spending (Typically) MUST Boost Corporate Earnings

Some equations or relations in economics are inspired guesswork, which may or may not precisely describe the real world. There are other equations which always hold, since they are simple accounting identities. The Kalecki Profit Equation is of the latter type. It describes precisely the factors which determine corporate profits. Knowing this relation can give investors a leg up in predicting earnings.

Continue readingQE, Stock Prices, and TINA

The U.S. economy as quantified by GDP has been sputtering along in slow growth mode for a number of years. It took a huge hit in 2020 due to covid shutdowns and has not nearly recovered. But stock prices have been rocketing upwards, and this past year is no exception. Markets took a cliff-dive in March, but have since way overshot to the upside.

Here is a plot of the past five decades of U.S. GDP and of the Wilshire 5000 index, which approximates the total stock market capitalization in the U.S.:

Chart Source: St. Louis Fed, as plotted by Lyn Alden Schwartzer

These two curves have crisscrossed each other over the past five decades, but in recent years the stock market has roared to the upside. One of Warren Buffet’s favorite metrics as to whether stock are overvalued is to consider the ratio of these two quantities, i.e. the market-capitalization-to-GDP (Cap/GDP) ratio:

Source: Lyn Alden Schwartzer

The ratio is much higher than it has even been. The last time it got this high was in 2000, and that did not end well.

Continue readingThe Feel of Money

The Federal Reserve System has the ability create virtual dollars with the stroke of a key. They also issue the physical bills of U.S. currency ($1, $1, $2, $5, $10, $20, $50, and $100). The actual manufacturing of the bills for the Fed is done by the federal Bureau of Engraving and Printing.

Wouldn’t it be nice if you could just print up a bunch of $100 notes yourself? Well, the feds have already thought of that, and include an ever-growing array of features to make it hard to duplicate these bills.

Counterfeiting of dollar bills has a long history. Following a distasteful experience of runaway inflation with paper money during the Revolutionary War, the U.S. remained primarily on a gold standard for most of its existence. The first major issuance of paper money was in 1862, to help finance the Civil War. Counterfeiting of these bills soon became a major problem, with up to half the dollars in circulation being phony. A primary mission of the U.S. Secret Service when it was founded in 1865 was to combat counterfeiting.

During World War II, the Nazis in “Operation Bernhard” succeeded in producing enough counterfeit British money that the U.K. had to switch production of banknotes to a different format. The work was carried out by prisoners at concentration camps. Later in the war, the prisoners were tasked with counterfeiting U.S. currency as well. Due to the security features in the dollars, this was a more complex task. Also, the prisoners realized that their chance of being killed was higher after they succeeded in devising a process for making counterfeit dollars, so they slowed the work down as much as they could. The $100 bill has been a frequent target of more recent counterfeiters, including the British Anatasios Arnaouti gang and (allegedly) North Korea.

Modern U.S. currency includes numerous feature which make it difficult to duplicate. Only about 1 note in 10,000 in circulation is fake. You can click this link

The Seven Denominations | U.S. Currency Education Program

to zoom in on each of the seven denominations of U.S. currency and see the current security features for each one. The more valuable bills get more sophisticated. The $100 bill has color-shifted numerals and bell image, a 3-D security ribbon with shifting images of bells and 100s, a security thread which glows under ultraviolet light, and subtle watermarks. Magnetic features are also included.

But it turns out that one of the most reliable and hard-to-duplicate features of dollars is the feel in your fingers, a result of the material they are made from and the printing process which gives a 3-D texture:

Perhaps the most difficult-to-duplicate counterfeit deterrence feature of U.S. banknotes is its unique yellow-green paper, manufactured under close security by a single U.S. firm from a mixture of 75 percent cotton and 25 percent flax. When combined with intaglio-printed images and numerals, this gives the notes a unique “feel,” which surveys have reported is the most common method of counterfeit detection by the public and bank employees.

So, if you want your own $100 bills, it looks like you will have to earn them, or wait for the next stimulus check to arrive.

The Many Faces of Molasses

It started as a simple question: can you substitute blackstrap molasses for regular molasses in a gingerbread recipe?

In order to reduce our potential exposure to Covid, we are ordering groceries online and having them delivered. Whole Foods (owned by Amazon), delivers free to Amazon Prime customers like us. In our order the other day we included molasses. We are almost out, and I wanted to make a gingerbread recipe this holiday week. The bottle that arrived yesterday along with the rest of our order says “Blackstrap Molasses”. Hmm, I wondered, what is different about blackstrap molasses and can you use it in place of the usual Grandma’s molasses that we have always had in our cupboards?

Once I get reading on a topic, it is hard to stop. It turns out there is much to know about molasses (treacle, in the U.K.). We all know it to be a sweet, flavorful ingredient in baked goods, and in savory dishes like pulled pork and baked beans. Diluted molasses is touted as a hair de-frizzer and hair mask, and there are even claims it can help combat gray hair.

However, there is a decidedly unsavory side to its past. It played a key role in fueling the triangular Atlantic slave trade in the 1700’s and early 1800s. Plantations worked by slaves in the Caribbean would ship molasses to the American colonies, where it would be converted into rum. The rum was shipped to West Africa, to pay for more people to be captured and then shipped to the Caribbean plantations to grow more sugar and make more molasses.

Not to mention the deadly “Great Molasses Flood” in Boston. On January 15, 1919, a 50-ft high storage tank of molasses ruptured, and sent a 15-ft high wall of syrup racing through the street at 35 miles an hour. It crushed and drowned anything and anyone in its path. Buildings were collapsed, and 19 people died. It has a place in the history of litigation as the birthing the modern class action lawsuit.

But I digress. Back to the difference since between types of molasses. Sugarcane is squeezed to extract cane juice. Sugar, the main desired product, starts off dissolved in the juice. The cane juice is boiled to remove water, to precipitate the solid sugar crystals. The liquid that remains after the first boiling (and the removal of the sugar from that stage) is called first or light molasses. That is what has usually been sold in U.S. grocery stores.

That first molasses is subjected to a second boiling, to extract even more sugar. The remaining liquid is called second molasses, or dark or robust molasses. From all accounts, this is pretty similar in properties to the initial light molasses, just somewhat less sweet and more flavorful. Folks say that you can substitute dark molasses for light molasses in most recipes without making a big difference.

To extract the last little bit of sugar, the second molasses is boiled even longer and hotter. After the sugar from that stage has been removed, what is left is the so-called blackstrap molasses. Obviously, this product will have less sugar and less liquid, then the light molasses, with a higher concentration of the other flavoring components. The operational question for me is: Can I take some of that blackstrap molasses and simply re-dilute it with some sugar and some water to get the equivalent of light molasses?

Internet opinion on this matter is mixed. On the one hand, there are those who answer this question in the affirmative. They say that a half cup of blackstrap molasses plus half cup of light corn syrup (or half a cup of a water plus sugar mixture) can readily be substituted for a cup of light molasses.

On the other hand I read counsel such as this:

Blackstrap molasses is what results when regular molasses is boiled down and super-concentrated, This results in bitter, salty sludge that only has a 45 percent sugar content, as opposed to the 70 percent sugar level found in both light and dark varieties of baking molasses. Spoon University warns against using blackstrap molasses as substitute for true molasses in any recipe calling for the latter due to the fact that its bitter flavor will overpower the taste of whatever you’re making.

And this :

Do not use blackstrap molasses as a substitute for light or dark molasses. It has a strong, bitter taste and isn’t very sweet. It’s more likely to wreck your recipe than help it.

But still I (being a chemical engineer by trade) wondered if this “strong, bitter” taste is merely the lack of sugar, which could be cured by replacing the missing sugar. After all, unsweetened chocolate is unpalatably bitter, but we fix that by adding sugar.

I don’t claim the final word on this, but it seems that the severe third boiling that yields the blackstrap molasses does some chemical alterations. It is not merely a matter of removing sugar. It is all well when sugar is lightly heated to form light brown caramel, but when it gets pushed too far, some bitter, dark brown compounds can form. It is not clear that merely adding sugar can undo these flavors, considering that blackstrap still contains a lot (45%) of sugar.

Conclusion: Blackstrap molasses may be fine for your BBQ sauce and as a trendy, mineral-packed low-sugar sweetener for your yoghurt and tea. But that bottle of thick black goo on my counter is going back to Whole Foods, not into my gingerbread.

Where Does Money Come From?

Money can be simplistically defined as “A medium that can be exchanged for goods and services and is used as a measure of their values on the market, and/or a liquifiable asset which can readily be converted to the medium of exchange”. Earlier we described the amounts of various classes of “money” in the U.S. Here is a chart showing the amount of currency in circulation (coins and bills; lowest line on the chart) for 2005-2020, and also M1 (green), M2 (upper curve, purple) and “monetary base” (currency plus reserves at the Fed; red line).

To recap what M1 and M2 are:

M1: Physical currency circulating outside of the Fed and private banking system, plus the amount of demand deposits, travelers’ checks and other checkable deposits. This is highly “liquid” money, i.e. accepted and used for transactions in the private economy.

M2: M1 + most savings accounts, money market accounts, retail money market mutual funds, and small denomination time deposits (certificates of deposit of under $100,000).

The funds in these additional savings and money market accounts can in general be easily transferred to checkable accounts, and thus could go towards making purchases if desired.

Physical currency is made and put into circulation by the government or quasi-governmental agencies (the Treasury mints coins, and the Federal Reserve prints bills). But what about all the other money (M1, M2, etc.), which dwarfs the physical currency? How does it grow?

Without getting into all the weeds, it turns out that the major driver of money creation in modern economies is the process of bank loans. The vast majority of money in countries like the U.S. is not created directly by government or central bank operations, but is created in the private sector when commercial banks make loans. When individuals or companies decide to take out more loans (including loans for cars, houses, or business investment), the effective money supply in the nation increases. This is true for other modern economies. For instance, the Bank of England states:

There are three types of money in the UK economy:

3% Notes and coins

18% Reserves

79% Bank deposits

A typical scenario of how bank lending increases money might go something like this: Fred would like to add an enclosed back porch to his house, but doesn’t have the money in hand to pay a carpenter to build it for him. So the base case is no payment to the carpenter and no porch for Fred. However, Fred realizes he can go the bank and get a loan to pay for the porch. So he obtains a $20,000 loan from the bank, which first shows up as a $20,000 credit to Fred’s checking account. The bank credits Fred’s account, and in exchange obtains a contract from Fred promising that Fred will pay it back, with interest.

Fred writes a check for $20,000 to the carpenter, who in turn pays $10,000 to a lumberyard for materials and keeps the other $10,000 as his fee. The lumberyard is able to pay its workers for that day, and order replacement lumber from a mill. The workers spent their pay on various items. The carpenter puts $5000 of his $10,000 fee in a savings account, and pays the rest to a car dealer for a used car.

The initial loan to Fred set off a chain of spending and economic activity, which would not have otherwise occurred. Fred has his porch, the lumberyard workers continue to be employed and supporting their local merchants, the carpenter gets a second car, and this money keeps ricocheting around until it gets drained away into stagnant savings, or is used to pay down prior debt. Although they are not aware of it, part of the lumberyard workers’ pay for that day came out of the debt incurred by Fred.

The granting of that loan created $20,000 of spending capability, i.e. money. As far as the economy is concerned, that $20,000 did not exist as effective money prior to the loan. Thus, the money came into existence simultaneously with the debt associated with the loan. Fred received the capacity to spend $20,000 today, but in turn accepted the obligation to pay back this money, with interest. It is assumed that Fred had a stable income, such that he would in fact be able to pay back the loan in the future.

In general, increasing debt increases the money supply, and paying down debt extinguishes money. For simplicity, suppose Fred repays the $20,000 loan (with $2000 interest added) in one big lump, two years later. In that year, he will presumably spend into the economy something like $22,000 less than he would have otherwise. Thus, his paying down of his debt will act as a decrease in the circulating money.

In normal times, as one person is paying down his loan (and thereby shrinking the money supply), someone else is taking out a new and even larger loan, so total debt and the amount of money in circulation stays about the same, or grows somewhat. A feature of the 2008-2009 recession, however, was a big drop in consumer demand for credit; folks decided to pay down debts and not borrow so much money to buy stuff. The effect was a big drop in spending and thus in overall economic activity (GDP) and in employment.

Where was that $20,000 before Fred borrowed it? We might think that it was sitting unused in the bank vaults, just waiting to be borrowed. That turns out to be an incorrect picture of the lending process.

Bank loans differ in key ways from, say, an interpersonal loan. If I lend you money, I might draw down my checking deposit and give you a check which you would deposit in your bank account. No new money is created. You may hand me an I.O.U. slip stating when you will pay me back and with what interest, but that would still be just the same funds being traded back and forth between the two of us. I would have to have the money in my account to start with before I could loan it to you.

Bank lending is different. A bank can lend money and hence create a new deposit, which amounts to brand-new money, even if the bank does not have that money to start with. This is counterintuitive. In a later post we may flesh out this seemingly magical aspect of bank lending. See Overview of the U. S. Monetary System for a more complete discussion.

“Rapid Uncontrolled Disassembly”: Musk’s Positive Take on Rocket Explosion

If you haven’t been living under a rock, you probably saw at least one image of Elon Musk’s “Starship” rocket blowing up last week. This is a really big rocket, some 165 ft high, which Musk intends to use to ferry humans to Mars, as early as 2026. And before that, paying passengers like you and I are to climb aboard for brief tourist excursions to outer space.

The rocket is designed to land back on its launchpad, to be ready for its next flight. That part is what went wrong last Wednesday. I snagged three screenshots from the live-streamed SpaceX video on YouTube to show what happened. The first image shows the vessel descending on its rocket jets, obviously dropping way too fast as it neared the ground.

This is what happened upon impact:

Ouch. It turns out that not enough fuel was getting to the rocket engines to slow the vessel’s descent.

Here are the smoking ruins:

Another man may have been chagrined over this outcome, but not the indomitable Musk. He had given this flight only one in three odds of landing intact, and he was ecstatic over the vast majority of things that went right, and the useful data collected. After all, the rocket did successfully take off, ascend to 40,000 ft (12 km), and mainly descend in the desired horizontal orientation to minimize overheating. Right after the blast he tweeted:

“Fuel header tank pressure was low during landing burn, causing touchdown velocity to be high & RUD, but we got all the data we needed! Congrats SpaceX team hell yeah!!”

When you are Elon Musk, a little RUD (Rapid Uncontrolled Disassembly) is all in a day’s work. Which may be partly why he accomplishes so much more than most of us.

Thanks for the Patent System

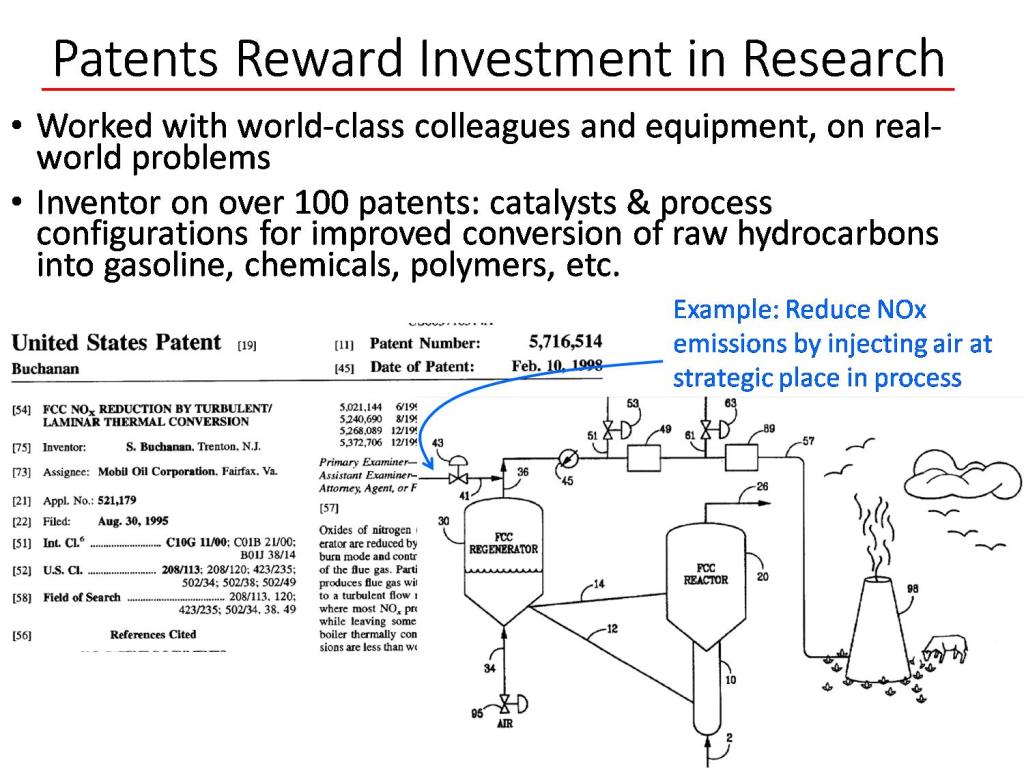

Although I write on a variety of subjects, my main professional training (through the PhD level) is as a chemical engineer. Chemical engineering is one of the broader technical disciplines. It bridges between chemistry, which is mainly associated with academic-type laboratory work, and huge chemical plant equipment. One year I was making and testing catalysts in the lab, then next I was calculating fluid flows and designing internals for a 100 ft high distillation tower (and climbing around inside that tower to insure the parts were being properly welded in place):

In my work in industrial research, I have been paid to develop technical improvements which could have economic value. A key incentive my company had for investing in this research was the expectation that if we came up with a novel improvement, that we could have exclusive rights to practice that improvement. There would have been little point in paying for research if our competitors could immediately make use of our hard-won insights. A snip of one of my patents is shown below.

For the world, and for most large groupings such as nations, the average income per capital is roughly equal to the average production per capita. The way to get more “stuff” (goods and services, and all their benefits) is to make more stuff. The way to make more stuff (per capita, and for fixed a workweek) is to make workers more productive. A key factor in productivity is technology. Two hundred years ago, nearly everyone in the U.S. had to be out in the sun and cold, working the soil, sowing by hand and plowing with the aid of animals, to grow enough food to feed everyone. Now I believe we are fed by only 2% of the workforce, using artificial fertilizers, improved seeds, huge tractors and combines, and satellite-aided computer scheduling. Most of the rest of us get to work in air-conditioned offices (or homes, in a pandemic year) and eat as much food as we want.

The patent system of the U.S. and other nations is designed to promote progress in productive technology. Early on, the newborn U.S. Congress passed the Patent Act of 1790, titled “An Act to promote the progress of useful Arts”. Without getting into all the legal details, a valid U.S. patent allows the inventor to exclude any other party from practicing their invention, for a period of twenty years. However, one of the requirement for a patent application is to clearly explain to the public how the invention works. When the twenty years is over, anyone can take advantage of the technology which the inventor has disclosed, which hopefully leads to widespread practice of technical improvements. While we can always ponder improvements to our system of patents, readers can thank it in part for many medical advances, and for delivering them from trudging behind a plow.