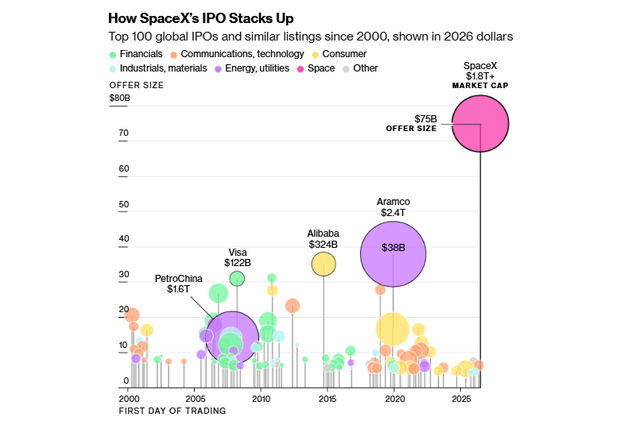

Here is a graphic that compares the size of the initial public offering (vertical axis) and the total company market cap (size of circle) of SpaceX to everything that has come before:

Elon Musk’s space launch/AI conglomerate spin-off SpaceX went public on Friday. Retail investors were all over it like a pack of starving dogs, driving up prices of SPCX from its opening $162 to $192 as of the close Monday. This has been grand theater, with Musk serving up signature visions of gargantuan total addressable markets, while investors are in fact getting crumbs of a money-loser. In the restaurant biz, this is known as selling the sizzle instead of the steak.

Let us pause for a reverent moment to savor the grand vision used to sell SpaceX: making humanity multiplanetary by dramatically lowering the cost of access to space. It extends beyond launch services into global communications (via Starlink), space infrastructure, in-space manufacturing, resource extraction, transportation, and ultimately a potential Mars economy—expanding from billions to trillions of dollars in theoretically addressable markets. Ooh, ahh, who would not want a piece of that?

Well, there are some problems here. It is hard not to splutter when trying to explain it, it is so bad for investors. I will just call out three issues I see:

( 1 ) Governance: You Own It But Can’t Influence It

The IPO float represents roughly 4-5% of total shares, so we the people only get a sliver of the company. But it gets worse. Public shareholders receive Class A shares with one vote each, while Musk holds Class B shares carrying ten votes each, giving him approximately 85% voting control. More unusually, the company bylaws explicitly prohibit shareholder proposals — meaning investors cannot even put advisory resolutions to a vote. This is governance subordination beyond what even Zuckerberg imposed on his investors.

( 2 ) Valuation: Priced for Perfection Without Profits

There is no price/earnings ratio because there are no earnings. At $2 trillion, SpaceX trades at approximately 20 times REVENUE. That price/sales is not unheard of for a small, fast-growing software company with almost no capital requirements (think: early-stage Amazon, Google, Palantir, etc.). But it makes no sense to apply it to a capital-intensive hardware and infrastructure business with negative GAAP earnings. Starlink is growing rapidly but requires continuous heavy capital expenditure to maintain and expand its satellite constellation. And SpaceX faces meaningful competition for orbital launches from Blue Origin, ULA (for military missions), maybe Rocket Labs, and the Chinese (for non-West payloads). And, if you dig into it, over 90% of their proposed addressable market is not space at all, but enterprise AI (!!). SpaceX pitches a total addressable market of $28.5 trillion, with AI opportunities alone accounting for $26.5 trillion. This is essentially the entire global GDP of the planet for a single year, and I guess they assume their pitiful Grok will claw back lots of market share from Claude, ChatGPT, and Gemini. As we said, priced for perfection.

( 3 ) Unbuilt Revenue Streams

SpaceX has announced contracts to provide AI compute services to other companies — potentially a significant revenue source — but the data centers required don’t yet exist. Investors are therefore paying partially for infrastructure that is neither built nor generating revenue, on a timeline that remains speculative.

OK, but we have seen shares of Musk’s other baby, Tesla (TSLA), remain at uniquely high price/sales and price/earnings, seemingly indefinitely. So, investing in SpaceX is much like investing in that shiny yellow metal called gold: there will never be conventional earnings payback, but there might well be some greater fool out there who will pay more for my shares than I did. This really comes down to a psychological head game, not fundamentals. Gold has in fact done very well over the years, and the pros learned the hard way not to short TSLA, not matter how unsupportable its price is.

Final comments on index fund buying to drive up the share price – one of the bull drivers for SpaceX has been the prospect that the huge company market cap (around $2 Trillion) would force index funds like NASDAQ and S&P500 to buy boatloads of SPCX stock, driving up the price. But it turns out this will not be such a big factor. These indices only take into account the publicly traded shares, not locked-up, non-traded founder shares. So, we are looking at around $100 billion in traded SPCX shares, not the full $2 billion, which is mainly shares controlled by Musk and venture capital. $100 billion is only about 0.15% of the total S&P500 market cap of about $70 trillion. This means fund purchases of SPCX should not by itself drive down prices of other companies.

It is true that inclusion in Nasdaq-100 and Russell indexes will force automatic buying of around $25 billion in SPCX shares from funds tracking those indices. That seems like a significant driver, but (a) everyone knows this, so it is already factored into today’s prices, and (b) index fund purchases will be offset by billions in sales from VC’s as they sell shares when their lock-up periods expire in a few months.

Side comment: Historically, the major indices have had a little gravitas about what companies to include. The Nasdaq-100 typically requires at least a 3 month “seasoning” period for an IPO to trade, and then waiting till the next regularly-scheduled reconstitution. Thus, it might take around six months for an IPO to make it into the Nasdaq-100 index. For SpaceX (and presumably for Anthropic and OpenAI IPOs), NASDAQ changed the rules to allow REALLY big IPOs to be included within 15 days. (This means that some other company will get booted from the Nasdaq-100). Russell caved even further than NASDAQ, with almost immediate inclusion in the Russell 3000.

Staid Standard and Poor’s alone has maintained its dignity here, refusing to compromise on its principles. For inclusion in the S&P 500, a company must be publicly listed for at least one full year, must show positive GAAP earnings in the most recent quarter and positive cumulative earnings across the trailing four quarters (this is going to be tough for a cash-burner like SpaceX), and at least 10% (not 5%) of its shares must be publicly traded. So, no S&P listing for SpaceX in the near future.