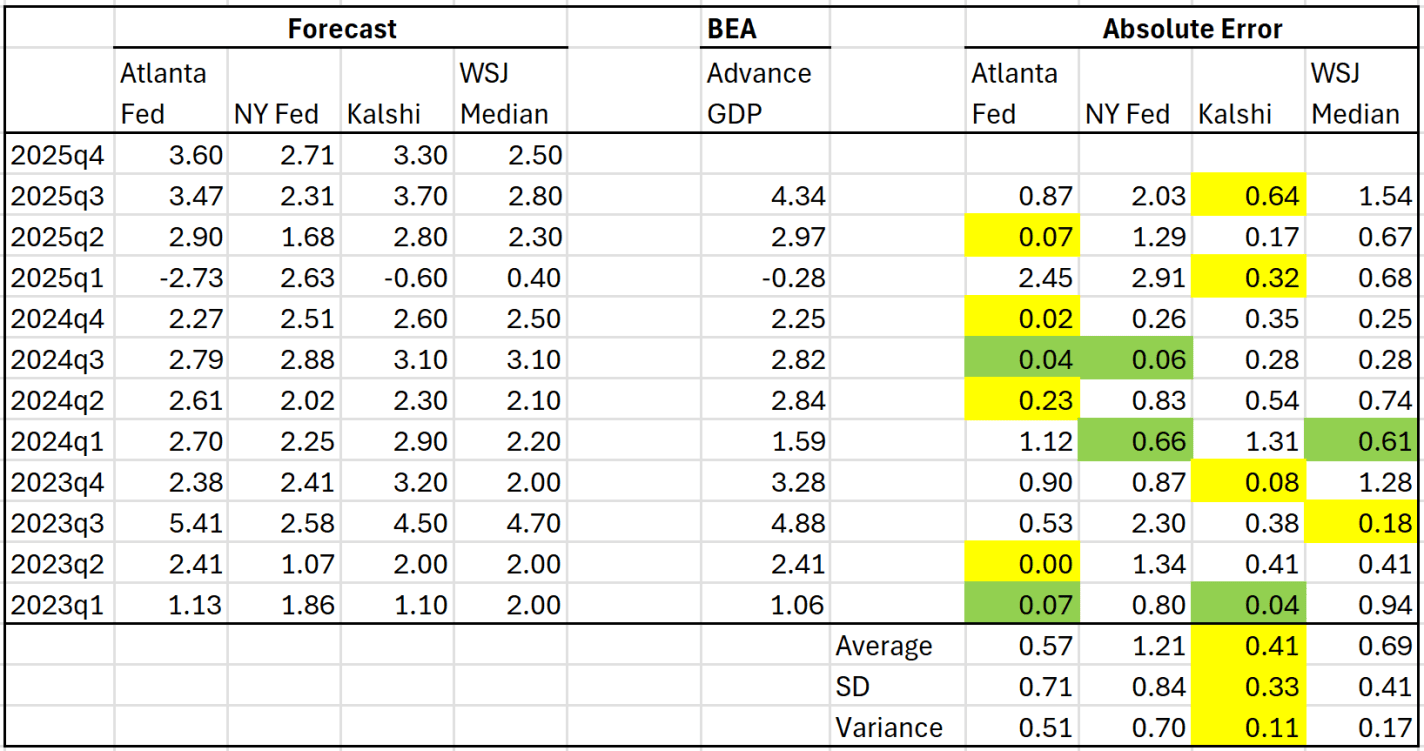

UPDATE 2/19/2026: the last GDPNow estimate from the Atlanta Fed is 3.0% and the Kalshi markets are now predicting 2.8%. I would expect this is a slightly better range than the 3.3-3.6% from my post written on 2/18/2026.

In April 2025 I wrote about several different forecasts for GDP growth. At the time the latest GDP quarter available was 2025Q1. We’ve had two more quarters of data since then, plus a highly anticipated report for Q4 coming out this Friday. How have these different predictions done recently? Here is the updated table from that prior post:

When I wrote the post in April 2025, I said that a simple average of the Atlanta Fed and Kalshi forecasts was the best simple predictor of the actual BEA advance figure. Based on the middle quarters of 2025, I think that continued to be true: each of them was the best estimate in one quarter, and perhaps just as importantly the NY Fed and WSJ survey of economists understated GDP growth pretty significantly.

There is still one more Atlanta Fed GDPNow update coming tomorrow before we get the actual BEA data on Friday, but based on where the numbers are now, we should expect Q4 to be around 3.4-3.5% (annualized) growth rate. This would put the total 2025 calendar year growth at around 2.3% — decent, but still below 2024’s 2.8% growth.

There was a seismic shift in the AI world recently. In case you didn’t know, a Claude Code update was released just before the Christmas break. It could code awesomely and had a bigger context window, which is sort of like memory and attention span. Scott Cunningham wrote a series of posts demonstrating the power of Claude Code in ways that made economists take notice. Then, ChatGPT Codex was updated and released in January as if to say ‘we are still on the frontier’. The battle between Claude Code and Codex is active as we speak.

The differentiation is becoming clearer, depending on who you talk to. Claude Code feels architectural. It designs a project or system and thrives when you hand it the blueprint and say “Design this properly.” It’s your amazingly productive partner. Codex feels like it’s for the specialist. You tell it exactly what you want. No fluff. No ornamental abstraction unless you request it.

Codex flourishes with prompts like “Refactor this function to eliminate recursion”, or “Take this response data and apply the Bayesian Dawid-Skene method”. It does exactly that. It assumes competence on your part and does not attempt to decorate the output. It assumes that you know what you’re doing. It’s like your RA that can do amazing things if you tell it what task you want completed. Having said all of this, I’ve heard the inverse evaluations too. It probably matters a lot what the programmer brings to the table.

Both Claude Code and Codex are remarkably adept at catching code and syntax errors. That is not mysterious. Code is valid or invalid. The AI writes something, and the environment immediately reveals whether it conforms to the rules. Truth is embedded in the logical structure. When a single error appears, correction is often trivial.

When multiple errors appear, the problem becomes combinatorial. Fix A? Fix B? Change the type? Modify the loop? There are potentially infinite branching possibilities. Even then, the space is constrained. The code must run, or time out. That constraint disciplines the search. The reason these models code so well is that the code itself is the truth. So long as the logic isn’t violated, the axioms lead to the result. The AI anchors on the code to be internally consistent. The model can triangulate because the target is stable and verifiable.

May you live in interesting times – apocryphal Chinese curse

In early 2025 I shared forecasts about the economy that turned out to be pretty good. This year, economic forecasts center around a boringly decent year (2.6% GDP growth, inflation below 3%, unemployment stays below 5%, no recession), though with high variance. But forecasts about politics and war foretell a turbulent year.

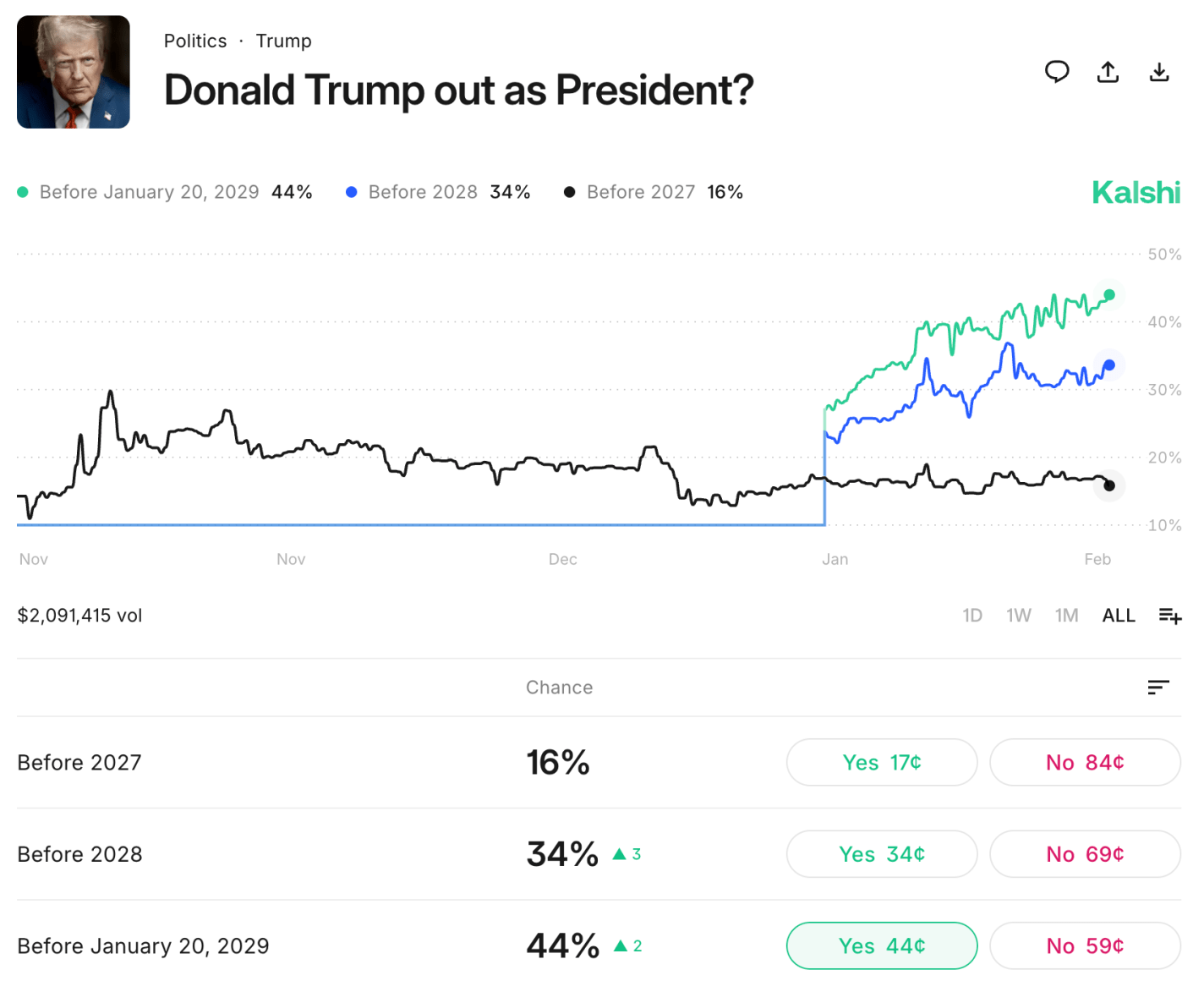

In the US, midterm elections have a 78% chance to flip control of the House and 35% chance to flip the Senate despite a tough map for Democrats. A midterm wave for the out-of-power party is typical in the US, given that the party in power always seems to over-play their hand and voters quickly get sick them. More surprising is that forecasters give a 44% chance that Donald Trump leaves office before his term is up, and a 16% chance that he leaves office this year. Markets give a 20% chance that he will be removed from office through the impeachment process, so the rest of the 44% would be from health issues or voluntary resignation.

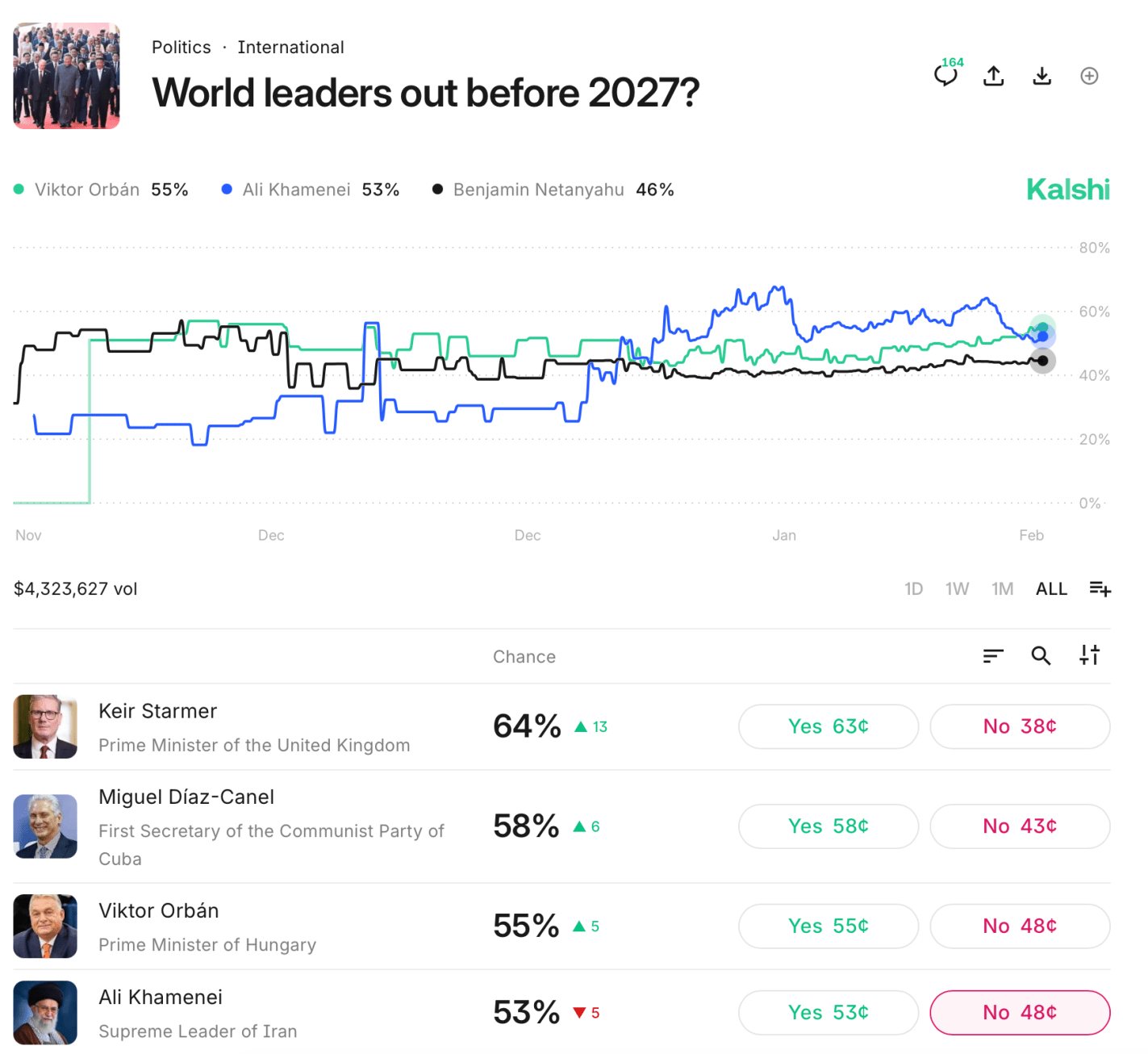

Forecasters at Kalshi predict a greater than even chance that 4 notable world leaders leave office this year:

I find this especially notable because Viktor Orban is the only one who would be removed through regularly scheduled elections. In the UK, Keir Starmer was just elected Prime Minister in 2024 and doesn’t have to face reelection until 2029; but he is so unpopular that his own Labor Party is likely to kick him out of office if local elections in May go as badly as polls indicate. If so, he would join Boris Johnson and Liz Truss as the third British PM in four years to leave office without directly losing an election. The leaders of Cuba and Iran don’t face real elections and would presumably be pushed out by a popular uprising orUS military action.

Some other important world leaders will probably stay in office this year, but forecasters still think there is a significant chance they leave: Israel’s Netanyahu (49%), Ukraine’s Zelenskyy (32%), and Russia’s Putin (14%). For the latter two, this belief could be tied to the surprisingly high odds given to a ceasefire in the Russia-Ukraine war this year (45%). Orban leaving office could be tied into this, as Hungary has often vetoed EU support for Ukraine.

Myself, I find most of these market odds to be high, and I’m tempted to make the “nothing ever happens” trade and bet that everyone stays in office. But even if all these markets are 10pp high, it still implies quite an eventful year ahead. Prepare accordingly.

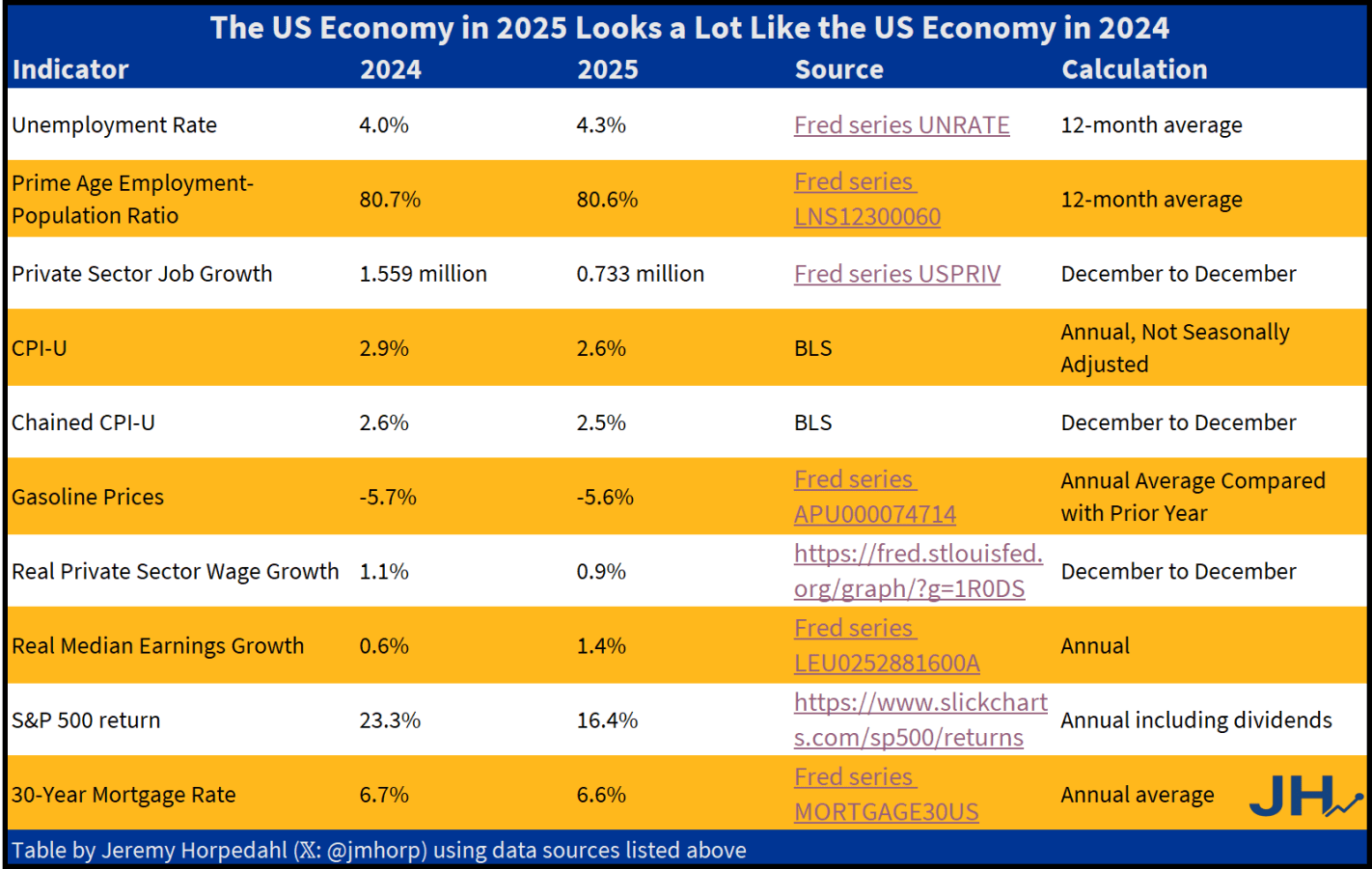

So what is the truth? I have put together what I think are the best economic indicators to judge how the economy is doing. And what does it tell us? I think the fairest read is that 2025 was a pretty good year, but based on most economic data it was almost identical to 2024.

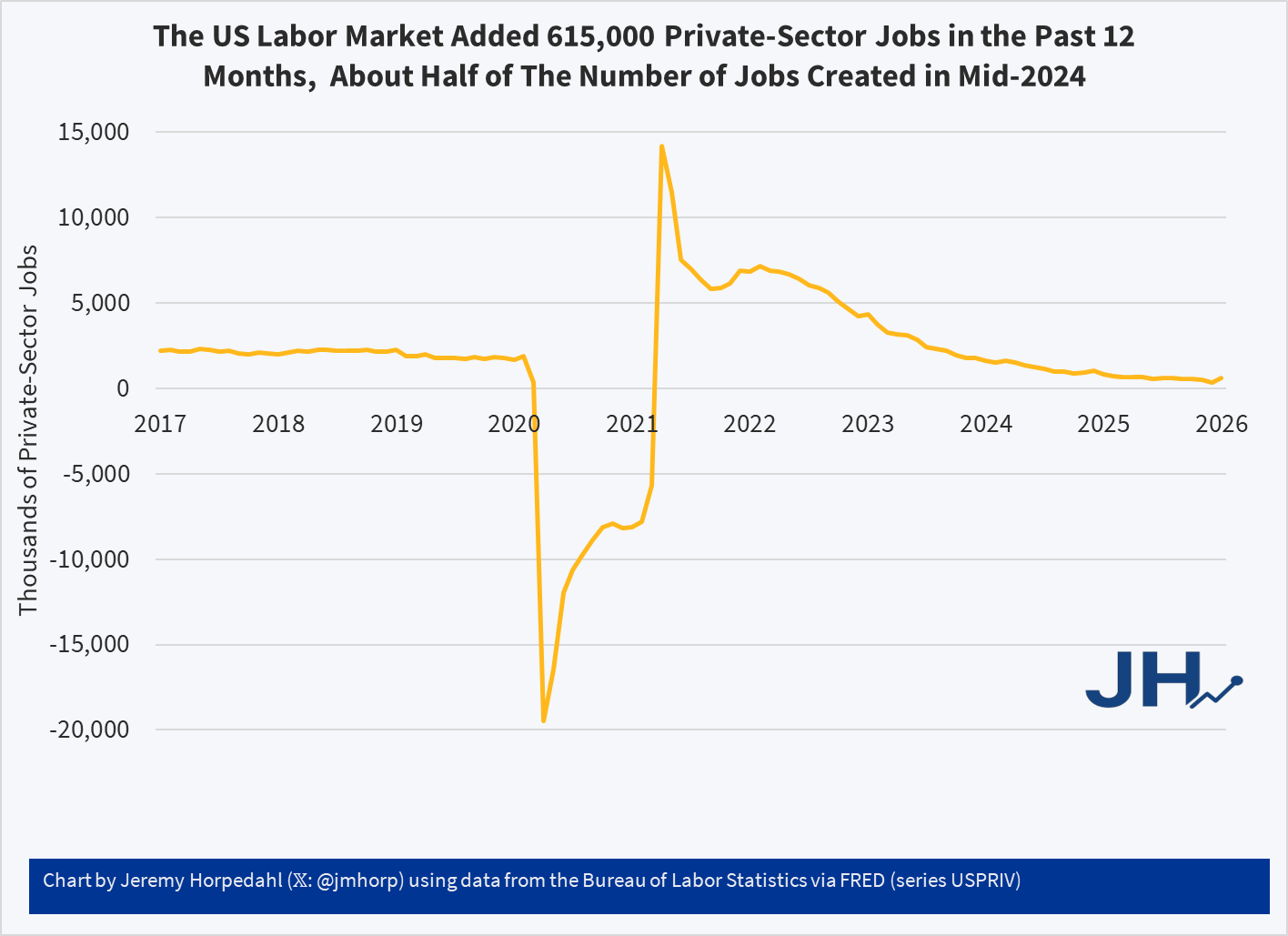

The only indicator that is clearly better is private-sector job growth in 2024. We might add S&P 500 in 2024 growth too, although some other assets such as gold have performed better in 2025. Inflation in 2025 is a tad lower, but not the massive improvement Trump suggests. This is especially the case for one of his favorite prices, gasoline. Yes, 2025 is a little lower than 2024… just like 2024 was a little lower than 2023.

And what of that greatest of all macroeconomic indicators, GDP? We don’t yet have Q4 data for GDP, which means we don’t have full-year 2025 data yet. But the growth rate of real GDP in 2024 was 2.8%, and betting markets are currently predicting 2.3% for 2025. Betting markets could be wrong! But it seems unlikely it would be much above 2.8% (those same betting markets only think there is a 4% chance it will be over 3.0%).

None of this is to say that the 2024 and 2025 economies are exactly the same. Certainly there is more uncertainty due to the shifting tariff policy, but on the other hand even with that uncertainty the economy is still performing fairly well. And my table above only includes economic outcomes, not any changes to government budgets, nor important social indicators such as crime. These are important too, but my focus in this post is only on the economic data.

It seems that in those surveys about whether the economy is better now or under Biden, it would be useful to offer an “about the same” option. Of course, in 2021-2022 inflation was much worse under Biden — but job growth was much better. A lot of this was baked in from the pandemic, 2020 monetary and fiscal stimulus, etc. Once we were back to a semi-normal economy in 2024, it was a decent year. Not blockbuster, but decent. So was 2025.

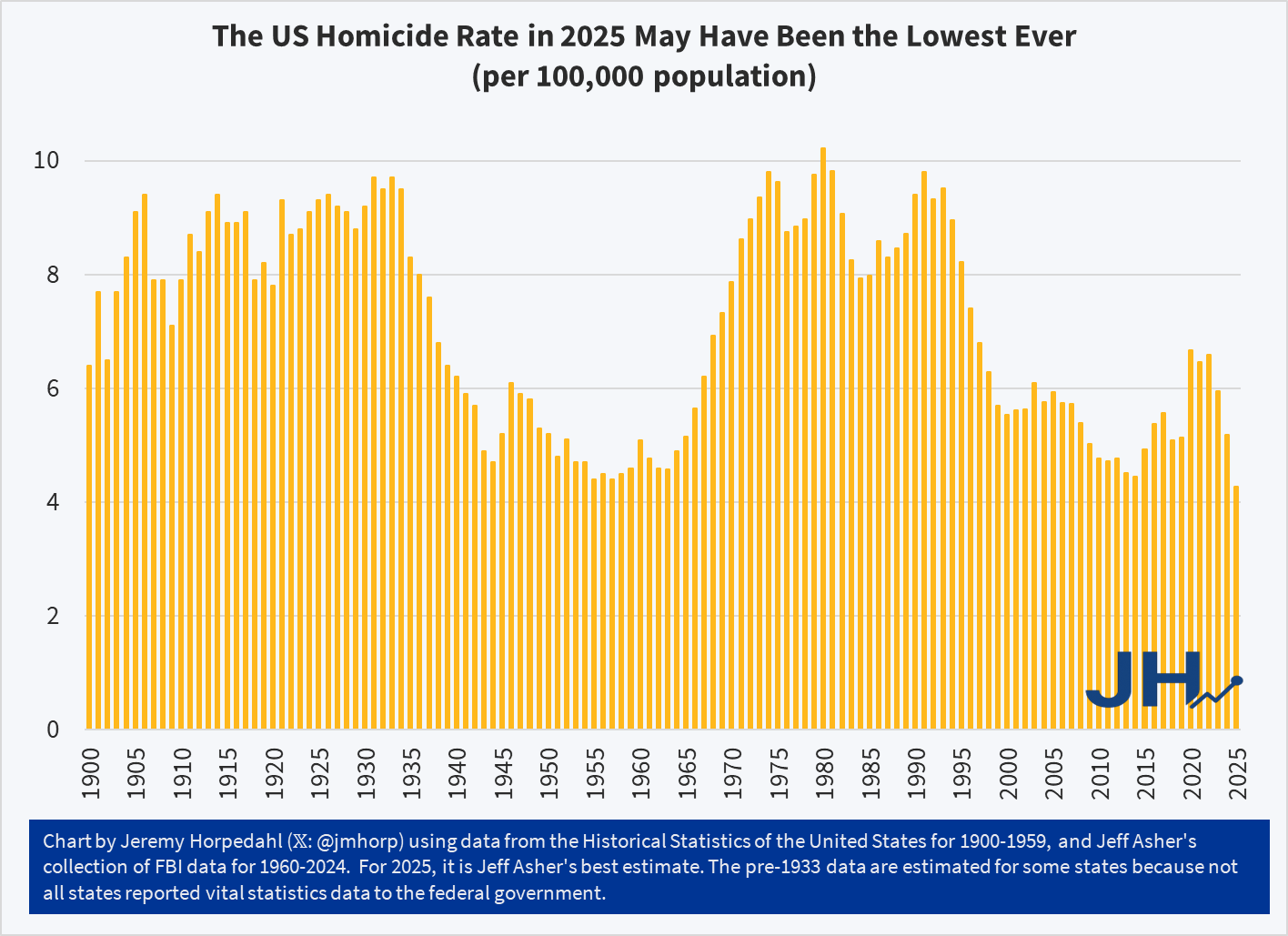

The following chart merges two data sources to create a long-run series on homicides in the US. Based on early estimates for 2025 from Jeff Asher, the homicide rate may be as low as 4.3 murders per 100,000 population. That would be the lowest since at least 1900, and possibly the lowest US homicide rate ever since the best evidence suggests it was even higher pre-1900. The current record low was 4.4 murders per 100,000, which the US saw in 1955, 1957, and 2014.

Declining fertility rates have been in the news a lot lately, and with good reason. Some countries, such as South Korea, have seen massive declines in fertility rates, and they face huge social problems and population decline resulting from these declining rates. But does the United States face the same problem?

To be clear, fertility rates are down in the US. Using the most common measure, the total fertility rate, births per woman in the US fell from a peak of over 3.5 births at the peak of the Baby Boom in the late 1950s and early 1960s, to around 2 births per woman in the 1990s and 2000s, and fell further to 1.6 births in 2023 (note: it had been around 2 births in the 1930s as well — the Baby Boom was a very real).

But the total fertility rate, or the number of births per woman of child-bearing age (usually 15-49) in a particular year is not a perfect measure. As Saloni Dattani clearly explains, if the timing of births is changing, this can make the TFR temporarily fluctuate. If women on average are delaying births to a later age, the TFR will fall initially even if women end up having the exact same number of children.

An alternative measure suggested by Dattani is the completed cohort fertility rate. This measure looks at the total number of children that women from a particular birth year in a country have throughout their child-bearing years. This rate also shows a decline for the US, but it is much more gradual: for women born in the 1930s (who would eventually become mothers during the Baby Boom), they peaked at about 3.25 births per woman, which declined to right at about 2.0 births in the 1950s (the Baby Boomers themselves), and has gradually risen since then to about 2.20 for women born in the early 1970s.

How does the US completed cohort fertility rate compare with other countries?

Even before Elon Musk gutted X’s content moderation, James Bailey was tired of the shouting. “It’s like a cursed artifact that gives you great power to keep up with what’s going on, but at the cost of subtly corrupting your soul,” said the 38-year-old Providence College economics professor.

He retreated. This year, he realized he was spending five to 10 minutes a day on a site he used to ignore.

The WSJ reporter contacted me after seeing my previous post about LinkedIn here, explaining how I think LinkedIn has improved as a way to share and read articles, and was always good as a way to keep up with former students. Just in the short time since the WSJ article came out, I finally used LinkedIn for one of its official purposes, hiring, where it worked wonders helping to fill a last-minute vacancy.

If you don’t trust me or the WSJ to identify the hot social network, lets see what the actual cool kids are up to

One of the major goals of the new Trump administration, particularly the DOGE unit, was to shrink the size of the federal government’s budget. Did they achieve this goal?

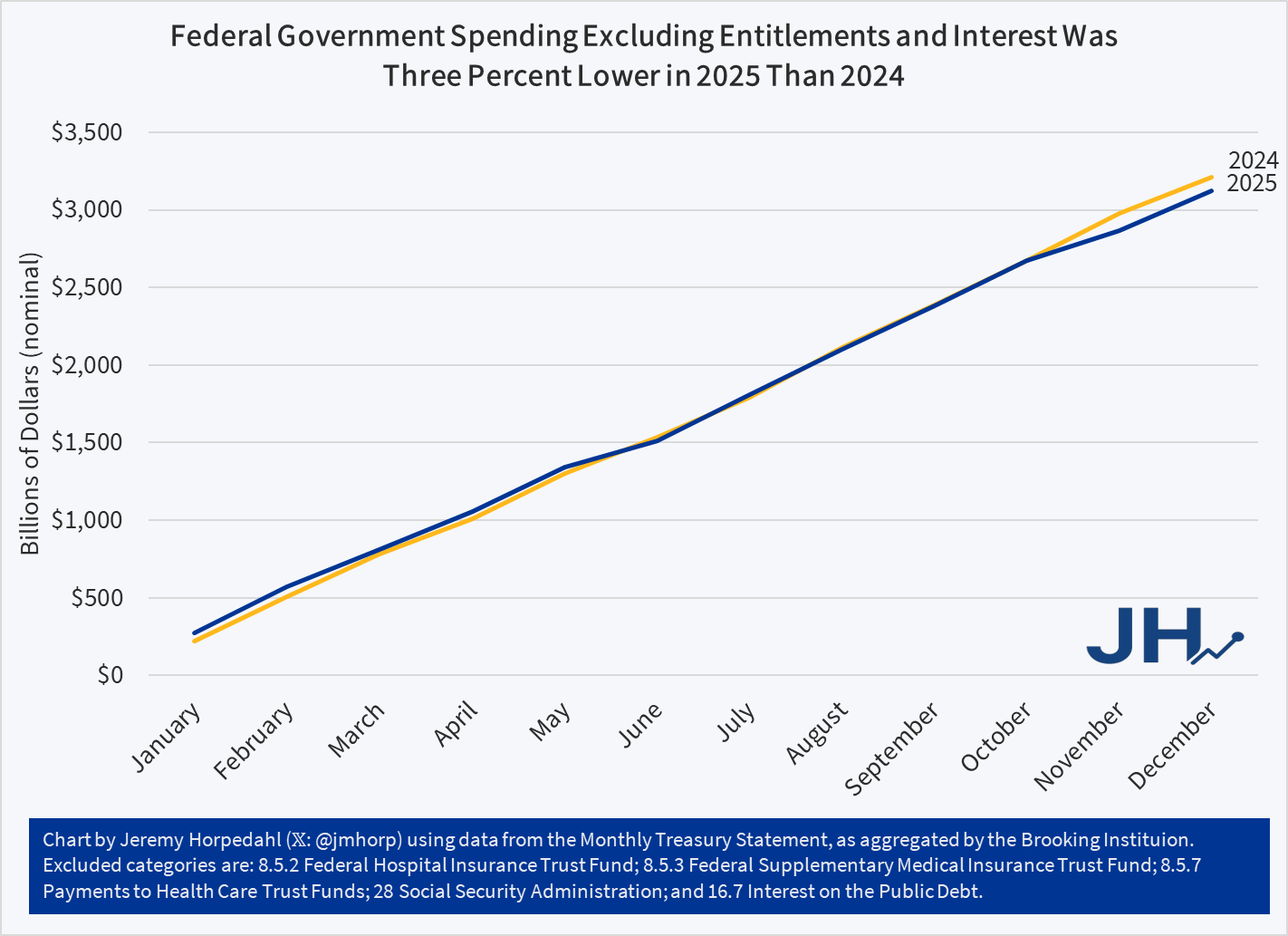

Last spring both my co-blogger Zachary and I pointed to a tool from the Brookings Institution to track federal spending, pulling in data directly from the US Treasury in a convenient format. Back in March I said “this will be a useful tool to follow going forward.” Now we have a full year of spending data for 2025.

When we look at total spending for Calendar Year 2025, it was about $318 billion higher than 2024, or about 4 percent higher. So, it seems that by that measure, the cuts that the Trump administration made were too small to overcome the other areas that grew.

But…

It may be more useful to remove some spending from the equation. In particular, entitlement programs and interest spending are very large spending categories that aren’t subject to the annual budgeting process. Of course, any program is ultimately under the control of Congress, so it’s a little bit of a cheat to remove Social Security and Medicare, but those programs are on autopilot with respect to the annual federal budget process. They are worth talking about, but they are probably worth talking about separately (especially because they have their own funding mechanisms). And interest on the debt isn’t something a President can control directly: it can only be reduced in future years by closing the budget gap today.

Removing those programs — which constitute about $4.8 trillion of the $7.9 trillion in 2025 spending (so a lot!) — gives you this chart (note: figures have been slightly updated with more complete data since I originally posted this chart):

Federal spending by this measure was about $85 Billion lower in 2025 than the prior year, or about 5 percent. And that’s in nominal terms: it is an even bigger cut if we adjust for inflation. Notice too that the pattern fits what we might expect: spending was slightly higher in the first half of the year (before any Trump changes could have had much of an effect), almost exactly equal for most of the second half, and then slightly below once we get to November and December (after the Deferred Resignation Program layoffs in October). If we ignore the first two months of the year (when it would have been really hard for Trump to have an effect), the drop in spending is about 8 percent.

What were the biggest cuts that led to the $85 billion drop? Keep in mind that some programs increased spending, such as military spending, so there are more than $85 billion in cuts. Using the Daily Treasury Statement categories, here are the big ones:

Federal Financing Bank (Treasury): $59 billion

Department of Education: $46.8 billion

USAID: $30.2 billion

EPA: $17 billion (though EPA seems to have gone on a spending binge at the end of 2024. Compared with 2023, the first Trump year was 50% higher!)

Federal Employee Insurance Payment (OPM): $16.3 billion

Those are all the programs I could find that declined by at least $1 billion, totaling a little over $200 billion. There were some other highly salient cuts that were under a billion dollars (such as the Corporation for Public Broadcasting, which was completely eliminated). Looking at that list I don’t think there is an easy way to sum up a “theme,” but I think the real theme is that if the Trump administration wants 2026 discretionary spending to be even lower than 2025, they will really need some major action from Congress. These cuts are mostly low-hanging fruit, and some are long-running goals of the GOP (such as Dept. of Education, foreign aid, and public television).

Of course, to really get federal spending under control, Congress will have to tackle entitlement reform and shrink the budget deficit to lower interest costs. Social Security, Medicare, and interest payments — the bulk of federal spending, over 60% of the total — increase by 9% in 2025. Again, it was probably unreasonable to expect Trump and Congress to have done anything major with them in a single year, but something must be done soon: the Social Security Old Age trust fund will be depleted in about 8 years, and the Medicare Part A trust fund will be depleted in about 10 years.

Have you ever looked up and wondered where the time went? One moment you’re living your life, and the next moment you realize that you’ve just lost time that you’ll never get back? That’s what happened to Japan’s economy at the turn of the century in an episode that’s known as ‘the lost decades’. It was a period of slow or null economic growth. Economists differ with their explanations. One cause was the prevalence of ‘zombie firms’.

Japan’s Economy

Japan had a current account surplus from 1980-2020, which means that they had more savings than they effectively utilized domestically. Metaphorically, they were so full of savings that they exhausted productive domestic investment opportunities and their savings spilled out into other counties in the form of foreign investments. This was driven by high household savings and slow growth in domestic investment demand. The result was the Japanese firms had easy access to credit. Maybe a little too easy…

Private corporate debt ballooned throughout the 1980s. That’s not intrinsically a problem. In the 1990s, households began saving somewhat less, and most firms began to drastically deleverage… But not all firms. The net effect of the mass deleveraging was that interest rates fell. The firms that remained in debt were the ones that risked insolvency. Less productive firms had slim profits and their Earnings Before Interest, Taxes, Depreciation, and amortization (EBITDA) was slim. So slim, that they couldn’t pay their debts. Faced with the prospect of insolvency, firms did what was sensible. They refinanced at the lower interest rates. Firms went to their banks and to bond markets and rolled over their debt, which they couldn’t afford, and replaced it with debt that had a lower interest rate. This occurred across industries, but especially in non-tradable goods and services that were insulated from international competition. Crisis averted.

Except this process of refinancing, while avoiding acute defaults and a potential financial crises, ensured that the less productive firms would survive. Not exactly failing and not exactly thriving, they could sort of just hold on to something that looks like life. Well, high debt and low profits aren’t much of a life for a firm. It’s more like being undead – like a zombie. Between 1991 and 1996, the share of non-finance firm assets held by zombie firms ballooned from 3% to 16%. The run-up differed by industry: Manufacturing zombie assets rose from 2% to 12%, from 5% to 33% in real estate, and from 11% to 39% in services. These zombie firms linger on, tying up valuable resources with low-productivity activities and drag on the economy.

China’s Economy

I’m not prone to China hysteria generally. However, I do have uncertainty about the plans and actions of the Chinese government because I don’t know that domestic economic welfare is its priority. That makes forecasting more political and less economic and outside my expertise. Regardless, the Chinese economy is a constraint on the government, whether they like it or not. And there are some echoes of the Japanese economy’s lost decades.