That is the title of a 2020 book by Dierdre McCloskey and Art Carden. It attempts to sum up McCloskey’s trilogy of huge books on the “Bourgeois Virtues” in one short, relatively easy to read book. I haven’t read the full trilogy, so I can’t say how good the new book is as a distillation, but I found that it was easy to read and at least makes me think I understand McCloskey’s basic thesis for why the world got rich. I share some highlights here.

Part 1 of the book aims to establish that the world did in fact get richer over recent centuries, plus give a basic explanation of liberal political thought. If you already know this you could skip this part and cut down an easy 189 page read to a very easy 106 page read (part 1 is for some reason written in a way that assumes you disagree with the authors, which grates when you don’t, or perhaps also if you do).

Part 2 gets to what I at least came for- digging into the history to solve the puzzle of why the Industrial Revolution / Great Enrichment took off when and where it did. Which means first, explaining why many things people think made 18th century England special were actually common elsewhere, like markets:

We ask whether coordination failures are a source of nominal rigidities. This was suggested in a recent speech by ECB President Christine Lagarde. She said, “In the recent decades of low inflation, firms that faced relative price increases often feared to raise prices and lose market share. But this changed during the pandemic as firms faced large, common shocks, which acted as an implicit coordination mechanism vis-à-vis their competitors.”

Coordination failure was suggested as a possible cause of price rigidity in a theory paper by Ball and Romer (1991). They demonstrated the possibility for multiple equilibria, and we perform the first laboratory test to observe equilibrium selection in this environment.

We theoretically solve a monopolistically competitive pricing game and show that a range of multiple equilibria emerges when there are price adjustment costs (menu costs). We explore equilibrium selection in laboratory price setting games with two treatments: one without menu costs where price adjustment is always an equilibrium, and one with menu costs where both rigidity and flexibility are possible equilibria.

In plain language, for our general audience, the idea is that the prices you set might depend on what other people are doing. If other people are responding to a shock (for example, Covid driving up labor costs all over town might cause retail prices to rise) then you will, too. If every other store in town is afraid to raise prices, then there is a certain situation where you might resist adjusting your prices, too (price rigidity).

Results: First, when there is only one theoretical equilibrium, subjects usually conform to it. When cost shocks are large, price adjustment is a unique equilibrium regardless of the presence of menu costs, and we see that subjects almost always adjust prices. When cost shocks are small and there are menu costs rigidity is a unique equilibrium and subjects almost never adjust. Conversely, with small cost shocks subjects almost always adjust when there are no menu costs.

The more interesting cases are when the parameters allow for either rigidity or flexibility to be selected. We find that groups do not settle at the rigidity equilibrium. Rather, depending on the specific nature of the shock, between half and 80% of subjects adjust in response to a shock. The intermediate levels of adjustment are represented here in this figure as the red circles that fall between the red and green bands where multiple equilibria are possible.

In the figure above, the red circles are higher when the production cost shock gets further from zero in absolute value. We see that the proportion of subjects adjusting prices is proportional to the size of the cost shocks. This is consistent with the interpretation that the large post-COVID cost shocks acted as an implicit coordination mechanism for firms raising prices. Our results provide a number of interesting insights on nominal rigidities. We document more nuance in the paper regarding heterogeneity and asymmetry. Comments and feedback are appreciated! If it’s not clear from the EWED blog how to email me (Joy), find my professional contact info here.

Despite its many flaws*, I always like to checkinon what the Taylor Rule suggests for the Fed. Its virtues are that it gives a definite precise answer, and that it has been agreed upon ahead of time by a variety of economists as giving a decent answer for what the Fed should do. Without something like the Taylor Rule, everyone tends to grasp for reasons that This Time Is Different. Academics seek novelty, so would rather come up with some new complex new theory of what to do instead of something undergrads have been taught for years. Finance types tend to push whatever would benefit them in the short term, which is typically rate cuts. Political types push whatever benefits their party; typically rate cuts if they are in power and hikes if not, though often those in power simply want to emphasize good economic news while those out of power emphasize the bad news.

The Taylor Rule can cut through all this by considering the same factors every time, regardless of whether it makes you look clever, helps your party, or helps your returns this quarter. So what is it saying now? It recommends a 6.05% Fed funds rate:

Fed Funds Rate Suggested by the Bernanke Version of the Taylor Rule Source: My calculation using FRED data, continually updated here

I continue to use the Bernanke version of the Taylor Rule, which says that the Fed Funds rate should be equal to:

Core PCE + Output Gap + 0.5*(Core PCE – 2) +2

*What are the flaws of the Taylor Rule? It sees interest rates as the main instrument of monetary policy; it relies on the Output Gap, which can only really be guessed at; and it incorporates no measures of expectations. If I were coming up with my own rule I would probably replace the Output Gap with a labor market measure like unemployment, and add measures of money supply shifts and inflation expectations. Perhaps someday I will, but like everyone else I would naturally be tempted to overfit it to the concerns of the moment; I like that the Taylor Rule was developed at a time when Taylor had no idea what it might mean for, say, the 2024 election or the Q3 2024 returns of any particular hedge fund.

That said, people have now created enough different versions of the Taylor Rule that they can produce quite a range of answers, undermining one of its main virtues. The Atlanta Fed maintains a site that calculates 3 alternative versions of the rule, and makes it easy for you to create even more alternatives:

Two of their rules suggest that Fed Funds should currently be about 4%, implying a major cut at a time that the Bernanke version of the rule suggests a rate hike. On the other other hand, perhaps this variety is a virtue in that it accurately indicates that the current best path is not obvious; and the true signal comes in times like late 2021 when essentially every version of the rule is screaming that the Fed is way off target.

I’ve often heard that before modern water treatment, it was safer to drink beer; but I’ve also heard people call this a historical myth. A new paper in the Journal of Development Economics by Francisca Antman and James Flynn comes down strongly on the side of “beer really was safer”:

This paper provides the first quantitative estimates into another well-known water alternative during the Industrial Revolution in England.

Although beer in the present day is regarded as being worse for health than water, several features of both beer and water available during this historical period suggest the opposite was likely to be true. First, brewing beer requires boiling the water, which kills many dangerous pathogens often found in drinking water. As Bamforth (2004) puts it, “the boiling and the hopping were inadvertently water purification techniques”. Second, alcohol itself has antiseptic qualities. Homan (2004) notes that “because the alcohol killed many detrimental microorganisms, it was safer to drink than water” in the ancient near-east.

They use several identification strategies to establish this, for instance when a tax on malt was increased and mortality went up:

But did this mean people were drunk all the time? Probably not:

beer in this period was generally much weaker than it is today, and thus would have been closer to purified water. Accum (1820) found that common beers in late 18th and early 19th century England averaged just 0.75% alcohol by volume, a fraction of the content of the beers of today. Beer in this period was therefore far less harmful to the liver. Taken together, these facts suggest that beer had many of the benefits of purified water with fewer of the health risks associated with beer consumption today.

In fact, people at the time didn’t necessarily know that beer was healthier:

Thus, even though people did not recognize beer as a safer choice, drinking beer would have been an unintentional improvement over water, and thus may have contributed to improvements in human health and economic development over the period we investigate

Though as usual, Adam Smith was ahead of his time. Here’s what he had to say in his 1776 Wealth of Nations, in a chapter on malt taxes:

Spirituous liquors might remain as dear as ever, while at the same time the wholesome and invigorating liquors of beer and ale might be considerably reduced in their price.

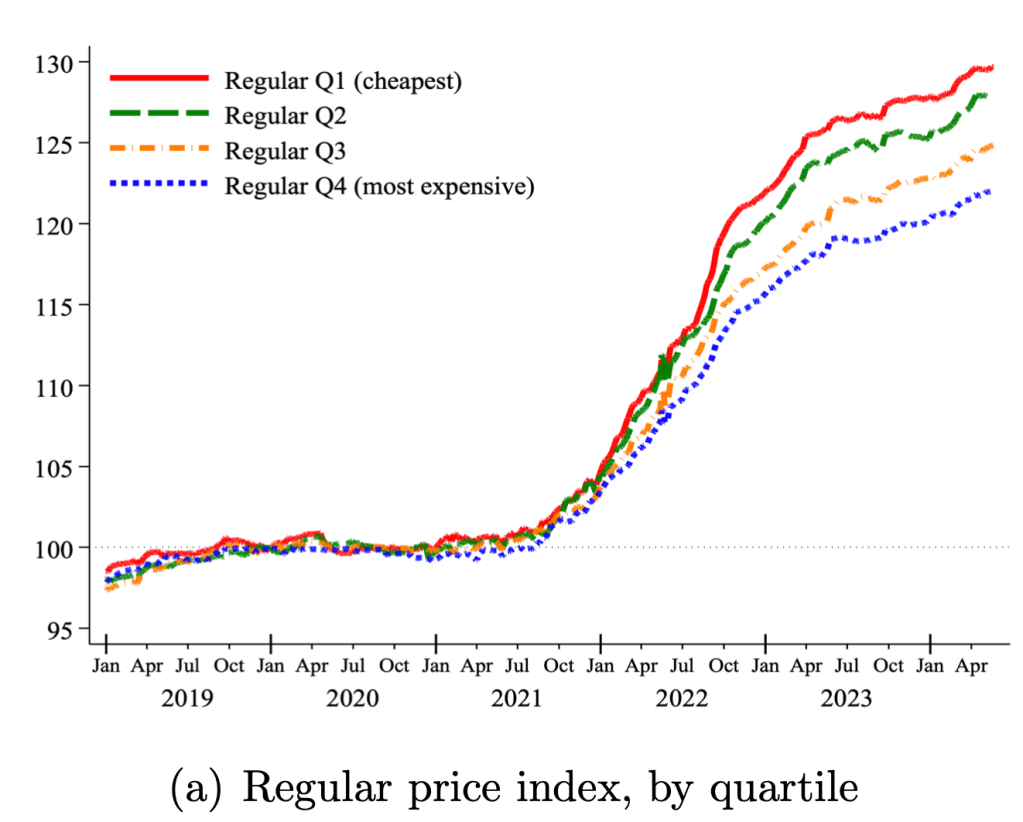

During the peak of the Covid inflation in 2022 I speculated that food inflation was worst for the cheapest products:

a typical McDouble now costs well over $2 in most of the US, while a typical Big Mac is still well under $6. You used to be able to get 4-5 McDoubles for the price of a Big Mac; now you typically get less than 3 and sometimes, as in Keene, less than 2.

What’s going on here? First, the McDouble was always absurdly cheap. Second, prices rise most quickly where demand is inelastic, and demand is less elastic for goods that are cheaper and goods that are more like “necessities” than “luxuries”.

We use micro price data for food products sold by 91 large multi-channel retailers in ten countries between 2018 and 2024. Measuring unit prices within narrowly defined product categories, we analyze two key sources of variation in prices within a store: temporary price discounts and differences across similar products. Price changes associated with discounts grew at a much lower average rate than regular prices, helping to mitigate the inflation burden. By contrast, cheapflation—a faster rise in prices of cheaper goods relative to prices of more expensive varieties of the same good—exacerbated it. Using Canadian Homescan Panel Data, we estimate that spending on discounts reduced the change in the average unit price by 4.1 percentage points, but expenditure switching to cheaper brands raised it by 2.8 percentage points….

The prices of cheaper brands grew between 1.3 to 1.9 times faster than the prices of more expensive brands—and only when inflation surged, not before or after.

I’m exploring whether the meme generator by Glif could be a way to introduce an econ paper. What if you identify a main character in your research project for GLIF to drag? (BTW, I have learned that the Wojack Meme Generator will re-write the name of the person you put in if your phrase is too long but that does not mean that the phrase is not used for content. So, you can put a longer phrase into the meme generator.)

I’m going to re-print here the prompt I actually used to get the Glif meme. As a warning, this approach is obviously not appropriate for more professional audiences. But sometimes you have a chance to quickly show your paper to a more informal audience either in a presentation or online. Having a way to wake up the audience in that situation could be helpful.

I’m not sharing all of these because I like them. I’m trying to give readers a chance to decide if they’d want to try it themselves. I think some of these prompts don’t work well and the cartoons either aren’t funny or are not true to life. However, I do find them interesting if the assignment is to scrape the internet for the maximally negative sentiment about a certain thing.

The prompt I used: “Pay Transparency Advocate” / “Effort Transparency and Fairness,” with Elif Demiral and Umit Saglam (under review)

Prompt: “Person Who Trusts ChatGPT” / “Do People Trust Humans More Than ChatGPT?” (2024) with William Hickman. Journal of Behavioral and Experimental Economics, 112: 102239.

This week, I’m doing some review for a macro-related project. In economics, the concepts of real and nominal rigidities help explain why prices and wages do not always adjust quickly in response to shocks. These rigidities create frictions that affect how markets function. A well-known rigidity is downward nominal wage rigidity (I have an experimental paper on that).

“Nominal rigidities” refer to the stickiness of prices and wages in their nominal (monetary) terms. These rigidities prevent immediate adjustment of prices and wages to changes in the overall economic environment.

Examples of Nominal Rigidities

Menu Costs: The costs associated with changing prices, such as reprinting menus or reprogramming point-of-sale systems. For instance, a restaurant might avoid changing its menu prices frequently because of the costs involved in printing new menus and the risk of confusing or losing customers.

Nominal Wage Contracts: Many workers are employed under contracts that fix their wages for a certain period, such as a year. This means that even if the demand for labor changes, wages cannot adjust immediately. For example, a factory might have a one-year wage contract with its workers, preventing it from lowering wages even during a downturn.

Price Stickiness Due to Psychological Factors: Prices may remain rigid because businesses fear that frequent changes might upset customers or erode their trust. A classic example is a retail store keeping prices stable to maintain a reputation for reliability, even when costs fluctuate.

Side note: Lars Christensen predicts less nominal rigidity in our future. Menu costs are getting smaller and customers could become accustomed to, for example, watching the price of milk fluctuate in real time in response to statements by the Fed. Click here for related Twitter joke.

I was writing up something for my graduating seniors about how to keep learning economics after school, and realized I might as well share it with everyone. This may not be the best way to do things, it is simply what I do, and I think it works reasonably well.

Blogs by Economists: There are many good ones, but besides ours Marginal Revolution is the only one where I aim to read every post

Podcasts on the Economy: NPR’s The Indicator (short, makes abstract concepts concrete), Bloomberg’s Odd Lots (deeper dives on subjects that move financial markets)

Podcasts by Economists: Conversations with Tyler and Econtalk (note that both often cover topics well outside of economics). Macro Musings goes the other way and stays super focused on monetary policy.

Twitter/X: This is a double-edged sword, or perhaps even a ring of power that grants the wearer great abilities even as it corrupts them. The fastest way to get informed or misinformed and angry, depending on who you follow and how you process information. Following the people I do gives you a fighting chance, but even this no guarantee; even assuming you totally trust my judgement, sometimes I follow people because they are a great source on one issue, even though I think they are wrong on lots of other things. Still, by revealed preference, I spend more time reading here than other single source.

Finance/Investing: Making this its own category because it isn’t exactly economics. Matt Levine has a column that somehow makes finance consistently interesting and often funny; unlike the rest of Bloomberg, you can subscribe for free. He also now has a podcast. If you’d like to run money yourself some day, try Meb Faber’s podcast. If you’d like things that touch on finance and economics but with more of a grounding in real-world business, try the Invest Like the Best podcast or The Diff newsletter.

Economics Papers: You can get a weekly e-mail of the new papers in each field you like from NBER. But most econ papers these days are tough to read even for someone with an undergrad econ degree (often even for PhDs). The big exception is the Journal of Economic Perspectives, which puts in a big effort to make its papers actually readable.

Books: This would have to be its own post, as there are too many specific ones to recommend, and I don’t know that I have any general principle of how to choose.

This is a lot and it would be crazy to just read all the same things I do, but I hope you will look into the things you haven’t heard of, and perhaps find one or two you think are worth sticking with. Also happy to hear your suggestions of what I’m missing.

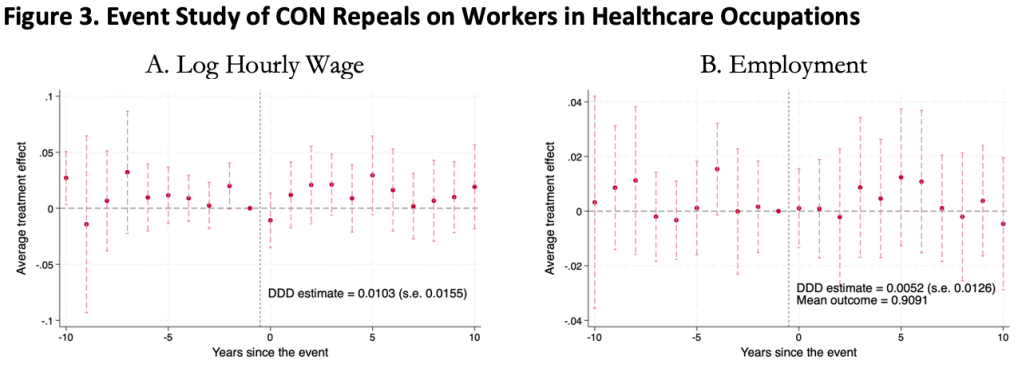

This was surprising to me, as I kind of expected CON laws to harm workers. Certificate of Need laws require many types of health care providers to obtain the permission of a state board before they are allowed to open or expand. This could lead to fewer health care facilities, and so less demand for health care workers, lowering wages and employment. It could also lead to less competition among health care employers, to similar effect.

On the other hand, less competition in the market for health services could raise profits, with room to share them in the form of higher wages. Or, CON being primarily targeted at capital expenditures like facilities and equipment could increase the demand for labor (to the extent that labor and capital are substitutes in health care). All these competing theories seem to cancel out to one big null when we look at the data.

We use 1979-2019 data from the Current Population Survey and a generalized triple-difference approach comparing CON-repealing to CON-maintaining states, and find a bunch of fairly precise zeroes. This holds for many different definitions of “health care worker”: those who work in the health industry, in health occupations, in hospitals, in health care outside hospitals, nurses, physicians, and more.

This is the first word on the topic, not the last; I wouldn’t be too surprised if someone down the road finds that CON does significantly affect health care workers. In this paper we pushed hard on the definition of “health care workers”, but not on “Certificate of Need” or “wages”. We simply classify states as “CON” or “non-CON” because that is what we have data for, but some states have much stricter programs than others, and some day someone will compile the data on this back to the 1970’s. The easier thread to pull on is “wages”. We use one good measure (the natural log of inflation-adjusted hourly real wages), but don’t do any robustness checks around it; considering “business income” could be especially important here. It is also possible that CON affects workers in other ways; we only checked wages and employment.

The full paper is here (ungated here) if you want to read more.

I got to be a guest of Vignesh Swaminathan who is based in Mumbai. It’s fun to have a deep conversation with someone on the other side of the world and share it with the whole internet (and the AI’s).

The first 10 minutes are about Tyler’s GOAT book. Vignesh asked me to name some influential economists who did not make Tyler’s list.

Around minute 12 we talk about the experimental economics methodology.

The middle (minute 15-42) is a discussion of the pipeline into tech and my Willingness to be Paid paper. He adds his perspective on tech jobs in India.

Around minute 42, Vignesh makes a switch over to the Barbie movie and then Oppenheimer. He observes that Oppenheimer is a “brand.” I speculate on careers in Barbieland. We recorded this before Christmas of ’23, right after everyone had seen these summer movies. Both movies ended up in the 2024 Oscars awards ceremony.

I predicted that people will eventually be able to create a custom movie from a verbal prompt, because of the AI content revolution. Here in Spring of ’24 that has already come true. Sora is shocking everyone and even caused Tyler Perry to halt a physical film studio expansion.

Around minute 55, we pivot to Hayek and competition, which leads to a postmortem on Google Plus (RIP).

Skimming back through this conversation has me thinking about tech work. The market for IT workers and programmers has evolved since I first started the project that became “Willingness to be Paid: Who Trains for Tech Jobs?”

I like pointing people all the way back to this report on jobs from 1958. Learn to Code has been good advice for a long time, for the people who can tolerate the work. That does not mean it will be true forever, but I would argue that it is still true today.

Silicon Valley as a career might have peaked around 2021. It’s not going away, but it might not be growing anymore in terms of the number of talented people who can be absorbed there. (Might I suggest Huntsville instead?)

The rise of artificial intelligence is affecting job seekers in tech who, accustomed to high paychecks and robust demand for their skills, are facing a new reality: Learn AI and don’t expect the same pay packages you were getting a few years ago.

Jobs in areas like telecommunications, corporate systems management and entry-level IT have declined in recent months, while roles in cybersecurity, AI and data science continue to rise, according to Janco’s data. The average total compensation for IT workers is about $100,000, making the position a target for continued cost-cutting.

One reason tech jobs are less attractive than some other professional paths is that the skillset changes. We mentioned this as a drawback in our policy paper. Computers are constantly changing. Vignesh and I discuss the issue of risk. I suggested that companies could pay less for talent if they were willing to offer packages that carry less risk of getting fired.

Nevertheless, tech still has decent job prospects. An unemployment rate of about 5% is about normal for work, even though tech had seen lower rates at the peak of demand. I do not know what programming as a career will look like in 10 years, but I’d say the same about screenwriting and live sports commentary. The LLMs are coming for everything or nothing or something in between.

I’ve been on tour (regionally) with our ChatGPT paper and getting opportunities to query different audiences about their LLM use. Last week I talked to a young man in our business school who is using ChatGPT to write SQL code at his job. I said in the podcast that I would still advise young people in Alabama to learn to code, even if they are not going to move to Silicon Valley. I think coding is more fun in the LLM-age or at least less miserable.