Has it gotten easier or harder for Americans to afford the basic necessities of life? Part of the answer to this question depends on how you define “basic necessities,” but using the common triad of food, clothing, and housing seems like a reasonable definition since these composed over 80% of household spending in 1901 in the United States.

If we use that definition of necessities, here is what the progress has looked like in the US since 1901:

The data comes from various surveys that the Bureau Labor Statistics has collected over the years, collectively known as the Consumer Expenditure Surveys. The surveys were conducted about once every 1-2 decades from 1901 up until the 1980s, and then annually starting in 1984. Some of these are multi-year averages, but to simplify the chart I’ll just state one year (e.g., “1919” is for 1918 and 1919). The categories are fairly comprehensive: “food” includes both groceries and spending at restaurants; “housing” includes either mortgage or rent, plus things like utilities and maintenance; and “clothing” includes not only the cost of the clothes themselves, but services associated with them such as repairs or alterations (much more important in the past).

We can see in the chart that over time the share spent on these three areas of spending has declined dramatically, taken as a group. Housing is different, but it has been fairly stable over time, mostly staying between 22% and 29% of income (the Great Depression being an exception). There are two time periods when these costs rose: the Great Depression and the late 1970s/early 1980s. Both are widely recognized as bad economic times, but they are aberrations. The jump from 1973 to 1985 in spending on necessities was fully offset by 2003, and today spending on necessities is well below 1973 — even though for housing, it is a few percentage points greater.

A chart like this shows great progress over time, but it will inevitably raise many questions. Let me try to answer a few of them in advance.

Many regular Americans and policymakers say they want the US to manufacture more things domestically. But when they ask economists how to accomplish this, I find that our most common response is to question their premise- to say the US already manufactures plenty, or that there is nothing special about manufacturing. It’s easy for people to round off this answer to ‘your question is dumb and you are dumb’, then go ask someone else who will give them a real answer, even if that real answer is wrong.

Economists tell our students in intro classes that we focus on positive economics, not normative- that we won’t tell you what your goals should be, just how best to accomplish them. But then we seem to forget all that when it comes to manufacturing. Normally we would take even unreasonable questions seriously; but I think wondering how to increase manufacturing output is reasonable given the national defense externalities.

So if you had to increase the value of total US manufacturing output- if you were going to be paid based on a fraction of real US manufacturing output 10 years from now- how would you do it?

I haven’t made a deep study of this, but here are my thoughts. Better ideas at the top, ‘costly but would increase manufacturing output’ ideas at the bottom:

Claims that the middle class or working class has been “hollowed out” in the US have been made for years, or decades really. The latest claim is an essay in the Free Press by Joe Nocera. But these claims are usually lacking in data, while strong in anecdotes. Let’s look at the data.

Notice that the latest data point is for 2024, which is the highest they have ever been in this data series, and likely higher than any point in the past. While many point to about the year 2000 as when troubles for the working class started (this is when manufacturing employment really fell off a cliff, and China joined the WTO in 2001), inflation-adjusted earnings have risen 11% for this group of workers since then. You might say that’s not a lot of growth — and you would be correct! But this group is better off economically than in the year 2000, which is a point that gets lost in so many discussions about this issue.

But that’s just a national number. Might some states that were especially hit by manufacturing job losses be worse off? Nocera mentions North Carolina and the Midwest. To answer this, we can use BLS OEWS data, which has not only median wages by state, but also the 10th percentile wage — the lowest of the working class. Here’s what median real wage growth (again inflation-adjusted with the PCEPI) since 2001 (the earliest year in this series with comparable data):

There was a recent Planet Money Podcast episode that includes a fun exercise. An NPR employee produces a dozen chicken eggs and wants to sell them at cost to another employee for $5. That’s the setup. How does the employee decide who should receive the eggs? Clearly, the price mechanism won’t work since the price is fixed. A lottery is also not allowed. The egg recipient could engage in arbitrage, reselling the eggs for a higher price. But that’s not very likely and would be socially awkward. The egg producer wants to make someone happy. Who would he make the happiest?

That’s the challenge that the Planet Money team tries to solve.

First, they started with a survey. Rather than asking coworkers to rank a long list of things that includes eggs, the survey adopts a more robust method of pairwise comparisons. Do you prefer toast vs eggs? Eggs vs oatmeal? Toast vs oatmeal? and so on. One problem that they encounter, however, is that there is a lot of diversity among preparations methods. My oatmeal is better than my eggs. But my brother’s oatmeal is not. As it turns out, there is not a standard quality of prepared oatmeal and prepared eggs. So the survey is a flop.

Then they consult an economist. They decide to try to measure “willingness to pay”, which is an economic concept that identifies the maximum that a person could pay for something without becoming worse off. They couldn’t really ask the coworkers what their WTP is. People are social creatures and have many reasons to lie, mislead, signal, and to simply not know. Since someone’s WTP reflects preferences and values, we need a way to solicit the true preference while avoiding lies and most mistakes. Here’s how the economist suggested that they reveal the coworker preferences.

Step 1: Tell the coworker these rules.

Step 2: Coworker reports their WTP for a single egg in dollars

Step 3: A random price will be chosen by a machine. If the price is above the self-reported WTP, the coworker is not allowed to buy the egg. If the price is below the WTP, then the coworker must buy the egg at the random price.

I like to take existing datasets, clean them up, and share them in easier to use formats. When I started doing this back in 2022, my strategy was to host the datasets with the Open Science Foundation and share the links here and on my personal website.

OSF is great for allowing large uploads and complex projects, but not great for discovery. I saw several of my students struggle to navigate their pages to find the appropriate data files, and they seem to have poor SEO. Their analytics show that my data files there get few views, and most of the ones they get come from people who were already on the OSF site.

This year I decided to upload my new projects like County Demographics data to Kaggle.com in addition to OSF, and so far Kaggle is the clear winner. My datasets are getting more downloads on Kaggle than views on OSF. I’ve noticed that Kaggle pages tend to rank highly on Google and especially on Google Dataset Search. I think Kaggle also gets more internal referrals, since they host popular machine learning competitions.

Kaggle has its own problems of course, like one of its prominent download buttons only downloading the first 10 columns for CSV or XLSX files by default. But it is the best tool I have found so far for getting datasets in the hands of people who will find them useful. Let me know if you’ve found a better one.

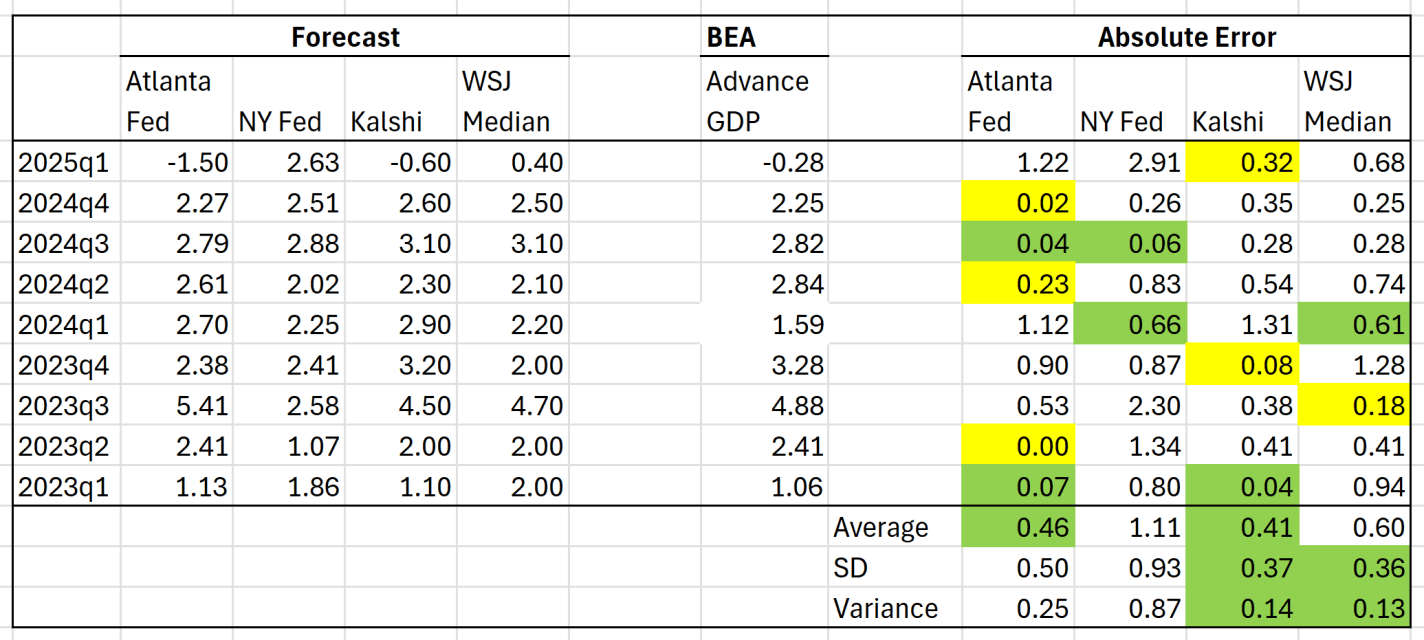

The 2025 first quarter GDP data came in slightly bad: negative 0.3%. I think the number is a bit hard to interpret right now, but it’s hard to spin away a negative number. A big factor pulling down the accounting identify that we call GDP was a massive increase in imports, specifically imports of goods. It’s likely this is businesses trying to front-run the potential tariffs (and keep in mind this was pre-“Liberation Day,” so probably even more front running in April), so the long-run effect is harder to judge.

But aside from the interpretation of the GDP estimate, we can ask a related question: did anyone predict it correctly? I have written previously about two GDP forecasts from two different regional Federal Reserve banks. They were showing very different estimates for GDP!

Both the Fed estimates ending up being pretty wrong: -1.5% and +2.6%. But there are two other kinds of forecasts we can look at.

The first is from a survey of economists done by the Wall Street Journal. The median forecast in that survey was positive 0.4%. This survey got the direction wrong, but it was much closer than the Fed models.

Finally, we can look at prediction markets. There are many such markets, but I’ll use Kalshi, because it’s now legal to use in the US, and it’s pretty easy to access their historical data. The average Kalshi forecast for Q1 (a weighted average of sorts across several different predictions) was -0.6%. Pretty close! They got the direction right, and the absolute error was smaller than WSJ survey. And obviously, much better this quarter than the Fed models.

But this was just one quarter, and perhaps a particularly weird quarter to predict (Atlanta Fed even had to update their model mid-quarter, because large gold inflows were throwing of the model). You may say that weird quarters are exactly when we want these models to perform well! But it’s also useful to look at past predictions. The table below summarizes predictions for the past 9 quarters (as far back as the current NY Fed model goes):

Chickens were apparently domesticated from the red jungle fowl (Gallus gallus), a native of southeast Asia, thousands of years ago. Humans have been selectively breeding them ever since. Traditionally, chickens were valued mainly for their eggs. Surplus roosters would get eaten, of course, and tough overage laying hens would end up in the stewpot. But your typical chicken was a stringy, hardy bird whose job was to stay alive and to lay eggs.

Raising chickens en masse just for eating started in 1923 with Celia Steele of southern Delaware, somewhat by accident. She wanted to set up a small flock of egg-laying chickens to supplement her husband Wilmer’s Coast Guard salary. She placed an order for 50 chicks, but it was mistakenly heard as 500. When she got this huge shipment, she thought fast and decided to raise them to eating size (“broilers”) and then immediately sell them. She built a coop designed for grow-out, rather than for egg-laying. This enterprise was profitable, so she expanded operations. She doubled production the next year, and by 1926 she had 10,000 chickens. Her neighbors saw her success, and also went into the broiler biz. Thus was spawned the modern broiler industry. All this was aided by the general prosperity in the 1920s, together with technical progress in refrigeration and transportation. Her first broiler house is now on the U.S. Registry of Historic Places.

However, chickens themselves were still scrawny by today’s standards. As of 1948, chicken meat was still an expensive luxury. With the broiler (meat chicken) market established, breeders naturally tried to develop strains that would grow big and fast. That not only allows more meat to be grown in a given flock, but fast growth means less feed is consumed to get to market weight.

For several years around 1950, A&P Supermarkets sponsored a “Chicken of Tomorrow” program, overseen by the USDA, to promote improved broiler breeding. As examples of chickendom as of 1948, here are plucked carcasses of contestants for the Chicken of Tomorrow contest of that year. Note how stringy they are, compared to the plump, meaty bird you buy at the grocery store today:

Without going into much detail, the ultimate product was a cross (hybrid) between the Cornish chicken and other breeds. Cornish cross chickens were initially bred for size and growth rate. By say the 1990s, that led to birds that were so heavy that they sometimes could not support their own weight. More recent breeding programs promote leg strength and other health factors, as well as sheer growth.

To produce today’s optimized broiler is a complex process. Breeders must maintain something like four purebred strains, and then carefully cross-breed them, and then cross-breed some more, to get the final hybrid chick to send out for farmers to raise. Only these hybrids have the optimized characteristics; you can’t just take a bunch of these crossed chickens and breed a good flock from them:

Only a few large outfits can afford to do this, so most hatcheries are supplied by a handful of big breeders. However, there seems to be enough competition to keep the prices down for the consumer. Some folks will always find something to complain about (reduced genetic diversity or hardiness, etc.), but they are welcome to breed and grow less efficient chickens, if it pleases them.

In terms of dollars: “The inflation-adjusted cost of producing a pound of live chicken dropped from US$2.32 in 1934 to US$1.08 in 1960. In 2004, the per-pound cost had dropped to 45 cents, according to the USDA Poultry Yearbook (2006).”

According to the National Chicken Council, in 1925 it took a broiler chicken an average of 112 days to reach a market weight of 2.5 pounds. As of 2024, the market weight has soared to 6.5 pounds, and chickens reach that weight much faster, in 47 days (about the time it takes leafy green vegetables). The net result is that now it only takes about 1.7 pounds of feed to grow one pound of chicken, compared to 4.7 lb/lb in 1925. This nearly three-fold reduction in resource consumption translates into lower consumer costs, lower load on the environment and agricultural resources, and even lower CO2 generation. The largest jump feed conversion efficiency (from 4 to 2.5 lb/lb) occurred between 1945 and 1960, thanks to the development of the Cornish cross.

In economics, commitment devices are often seen as clever solutions to self-control problems—ways people can tie their future hands to avoid giving in to temptation. A smoker throws away their cigarettes, a dieter pays in advance for healthy meals, a student announces a deadline publicly so they can’t back out. The idea is that by limiting future choices, a person can force themselves to stick with a preferred long-term strategy. But commitment devices also show up in places far removed from personal productivity—and in some cases, they carry bad unintended consequences when the strategic landscape shifts.

Consider the case of gang tattoos, especially those associated with MS-13. For years, highly visible tattoos served as a powerful way to demonstrate loyalty to the group. These tattoos—sometimes covering the face, neck, or arms—weren’t just aesthetic. They signaled that the individual was fully committed to the gang. In economic terms, they functioned as a high-cost, hard-to-fake commitment device. By making oneself easily identifiable as a gang member, a person burned bridges to legitimate employment or life outside the gang. That might seem irrational at first glance, but it was often a rational decision in context. Within certain neighborhoods or prisons, that signal provided protection, status, and trust among peers. The visible commitment reduced the gang’s uncertainty about who was loyal and who might defect.

But the rules of the game changed. In March 2022, El Salvador launched an aggressive crackdown on gangs following a sharp spike in homicides. Under a sweeping “state of exception,” authorities suspended constitutional rights, arrested tens of thousands of people, and expanded prison capacity dramatically. Tattoos quickly became one of the easiest ways for police to identify and detain suspected gang members. News reports describe men being pulled from buses or homes not for current criminal activity, but simply because of the ink on their skin. In many cases, the tattoos were from years earlier—when the wearer had been young and immersed in a world where signaling loyalty felt necessary for survival. Now, those same signals serve as evidence in court or grounds for indefinite detention.

Generally, decisions to spend federal funds come is the authority of congress. But the Trump administration has very publicly made clear that it will try to cut the things that are within its authority (or that it thinks should be within that authority). Truly, the fiscal year with the new Republican unified government won’t begin until October of 2025. So, the last quarter is when we’ll see what the Republicans actually want – for better or for worse. In the meantime, we can look past the hyperbole and see what the accounting records say. The most recent data includes 95 days after inauguration. First, for context, total spending is up $134 billion or 5.8% from this time last year to $2.45 trillion.

The Trump administration has been making news about their desire and success in cutting. Which programs have been cut the most? As a proportion of their budgets, below is a graph of were the five biggest cuts have happened by percent. The Cuts to the FCC and CPB reflect long partisan stances by Republicans. The cuts to the Federal Financing Bank reflect fewer loans administered by the US government and reflect the current bouts to cut spending. Cuts in the RRB- Misc refer to some types of railroad payments to employees. In the spirit of whiplash, the cuts to the US International Development Finance Corporation reverse the course set by the first Trump administration. This government corporation exists to facilitate US investment in strategically important foreign countries.

But some programs have *increased* spending since 2024. The five largest increases include the USDA, the US contributions to multilateral assistance, claims and judgments against the US, the federal railroad administration, and the international monetary fund. Funding for farmers and railroads reflect the old agricultural and new union Republican constituencies. The multilateral assistance and IMF spending reflects greater international involvement of the administration, despite its autarkic lip service.

The Smoot-Hawley Tariff of 1930 was opposed by a thousand economists, but passed anyway, exacerbating the Great Depression. Now that the biggest tariff increase since 1930 is on the table, the economists are trying again. I hope we will find a more receptive audience this time.

The Independent Institute organized an “Anti-Tariff Declaration” last week that now has more signatures than the anti-Smoot-Hawley declaration, including many from top economists. One core argument is the sort you’d get in an intro econ class:

Overwhelming economic evidence shows that freedom to trade is associated with higher per-capita incomes, faster rates of economic growth, and enhanced economic efficiency.

But I thought the Declaration made several other good points. Intro econ textbooks say that tariffs at least benefit domestic producers (at the expense of consumers and efficiency), but in practice these tariffs have been mainly hurting domestic producers, because:

The American economy is a global economy that uses nearly two thirds of its imports as inputs for domestic production.

I get asked to sign a petition of economists like this every year or so, but this is the first one I have ever agreed to sign onto. Most petitions are on issues where there are good arguments on each side, like whether to extend a particular tax cut, or which Presidential candidate is better for the economy. But the argument against these tariffs is as solid as any real-world economic argument gets.

The full Declaration is quite short, you can read the whole thing and consider signing yourself here.