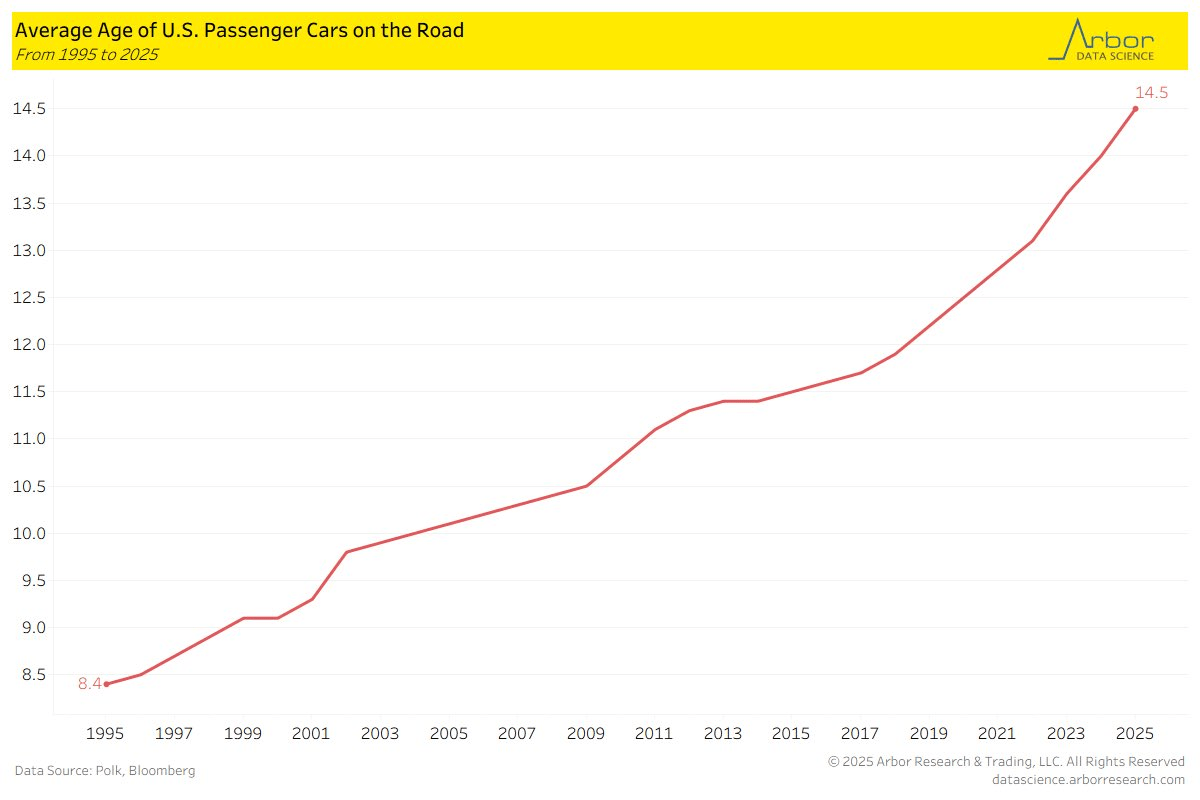

The following chart from Arbor Research shows that the average age of cars on the road in the US is 14.5 years. If we go back to 1995, it was almost half that, and the increase has been steady since over the past 30 years. Similar data from the Bureau of Transportation Statistics confirms these numbers.

Why would this be? I see two primary explanations that are possible. One is that cars are becoming more reliable (better quality), so consumers are happy to drive them longer. The other is that cars today are less affordable, so people are only hanging onto old cars because they are forced to. One of these is a happy explanation, one is consistent with a narrative of stagnation. Which is true?

On the affordability question, we do have some good data, but it points in the opposite direction: cars are much more affordable today than in 1995, or even before that.

Hey look, I just found a way to get infinite free electric power:

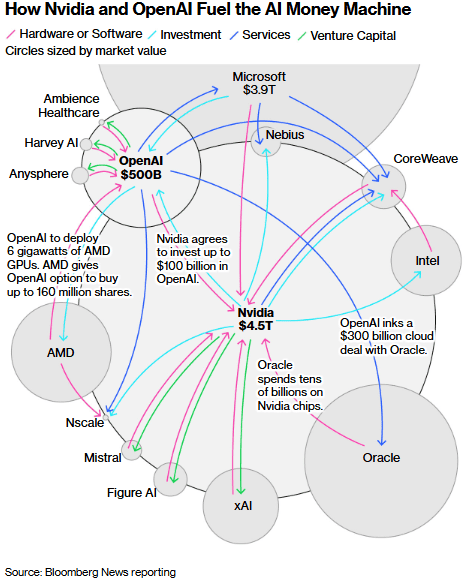

This sort of extension-cord-plugged-into-itself meme has shown up recently on the web to characterize a spate of circular financing deals in the AI space, largely involving OpenAI (parent of ChatGPT). Here is a graphic from Bloomberg which summarizes some of these activities:

Nvidia, which makes LOTS of money selling near-monopoly, in-demand GPU chips, has made investing commitments in customers or customers of their customers. Notably, Nvidia will invest up to $100 billion in Open AI, in order to help OpenAI increase their compute power. OpenAI in turn inked a $300 billion deal with Oracle, for building more data centers filled with Nvidia chips. Such deals will certainly boost the sales of their chips (and make Nvidia even more money), but they also raise a number of concerns.

First, they make it seem like there is more demand for AI than there actually is. Short seller Jim Chanos recently asked, “[Don’t] you think it’s a bit odd that when the narrative is ‘demand for compute is infinite’, the sellers keep subsidizing the buyers?” To some extent, all this churn is just Nvidia recycling its own money, as opposed to new value being created.

Second, analysts point to the destabilizing effect of these sorts of “vendor financing” arrangements. Towards the end of the great dot.com boom in the late 1990’s, hardware vendors like Cisco were making gobs of money selling server capacity to internet service providers (ISPs). In order to help the ISPs build out even faster (and purchase even more Cisco hardware), Cisco loaned money to the ISPs. But when that boom busted, and the huge overbuild in internet capacity became (to everyone’s horror) apparent, the ISPs could not pay back those loans. QQQ lost 70% of its value. Twenty-five years later, Cisco stock price has never recovered its 2000 high.

Beside taking in cash investments, OpenAI is borrowing heavily to buy its compute capacity. Since OpenAI makes no money now (and in fact loses billions a year), and (like other AI ventures) will likely not make any money for several more years, and it is locked in competition with other deep-pocketed AI ventures, there is the possibility that it could pull down the whole house of cards, as happened in 2000. Bernstein analyst Stacy Rasgon recently wrote, “[OpenAI CEO Sam Altman] has the power to crash the global economy for a decade or take us all to the promised land, and right now we don’t know which is in the cards.”

For the moment, nothing seems set to stop the tidal wave of spending on AI capabilities. Big tech is flush with cash, and is plowing it into data centers and program development. Everyone is starry-eyed with the enormous potential of AI to change, well, EVERYTHING (shades of 1999).

The financial incentives are gigantic. Big tech got big by establishing quasi-monopolies on services that consumers and businesses consider must-haves. (It is the quasi-monopoly aspect that enables the high profit margins). And it is essential to establish dominance early on. Anyone can develop a word processor or spreadsheet that does what Word or Excel do, or a search engine that does what Google does, but Microsoft and Google got there first, and preferences are sticky. So, the big guys are spending wildly, as they salivate at the prospect of having the One AI to Rule Them All.

Even apart from achieving some new monopoly, the trillions of dollars spent on data center buildout are hoped to pay out one way or the other: “The data-center boom would become the foundation of the next tech cycle, letting Amazon, Microsoft, Google, and others rent out intelligence the way they rent cloud storage now. AI agents and custom models could form the basis of steady, high-margin subscription products.”

However, if in 2-3 years it turns out that actual monetization of AI continues to be elusive, as seems quite possible, there could be a Wile E. Coyote moment in the markets:

Economist Craig Paulsson has made a simple game free to all.

When you go to MapGDP.com you will find a real picture from Google Maps and a simple question. Guess the GDP/capita in the country where this picture was taken.

Many economics teachers will at some point visit the topic of “what is GDP” or “economic growth.” This web game is great for both topics. I put the website on my classroom projector and called on students to take the guess. We then could do the reveal together. I rate this high value for low effort from a teacher’s perspective. No login or account creation required.

If you are an EWED reader and not an econ teacher, you might have fun playing the game yourself. Almost as satisfying as Wordle…

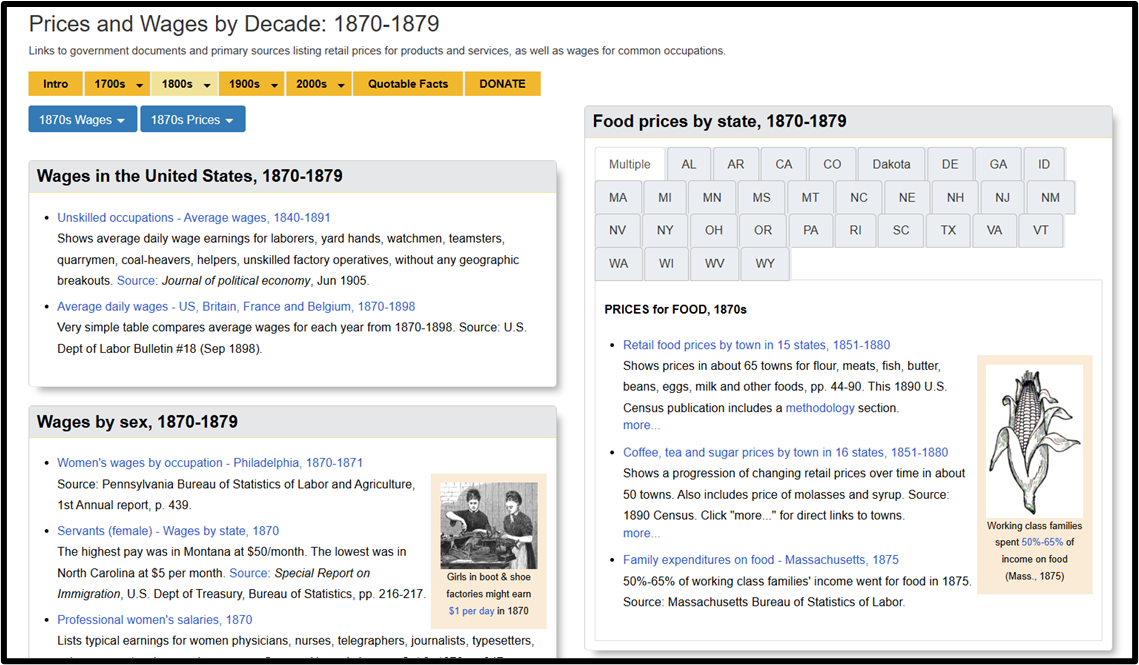

Today I’m just sharing a truly awe-inspiring resource. The University of Missouri has what is essentially a central clearinghouse for prices and wages. If you want the price of anything, then they should be your first stop.

See the screenshot at the bottom. The website links to the original sources for household consumption prices, occupation wages, etc. They make it easy to cut the data by date, industry, location, etc. Because they cite their sources, you can see some data series that are not even available on FRED – without having to perform the painful sleuthing on a government website.

I especially like this site for its historical data. One of the challenges of historical US data is that individual cities may not have prices that are representative of the national levels or trends. Lower levels of market integration make representative samples even more important than in modern data. But really, that was more of a concern for 20th century researchers. Now, we love our panel data. So, the historically less integrated markets of the US provide ‘toy economies’ that include greater regionalism and local shocks.

Although David Jacks has loads of tabulated data, he doesn’t have it all. The Missouri library site links to PDFs of original statistical publications which, while digitized, have never been tabulated into useable data fit for modern researchers.

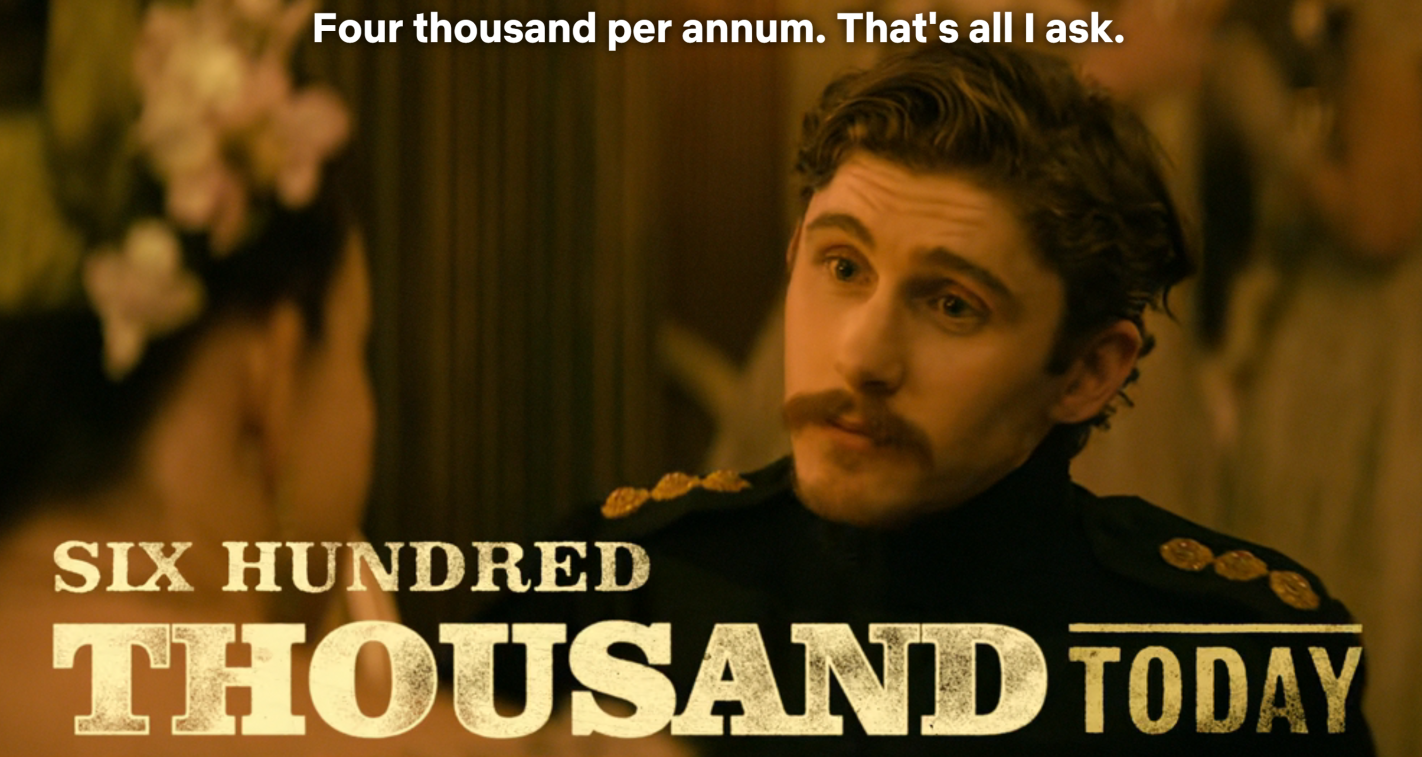

When reading an old novel or watching a period drama movie or TV show, it is almost inevitable that some historical currency amounts will be mentioned. This is especially true when the work is dealing with money and wealth, for example the series “The Gilded Age” is about rich people in late 19th century America. So money comes up a lot. I wrote a post a few weeks ago trying to contextualize a figure of $300,000 from 1883 for that show.

A new Netflix series “The House of Guinness” is another period piece that spends a lot of time focusing on rich people (the family that produces the famous beer), as well as their interactions with poorer folks. So of course, there are plenty of historical currency values mentioned, this time denominated in British pounds (the series is primarily set in Ireland, where the pound was in use). On this series, though, they have taken the interesting approach of giving the viewers some idea of what historical currency values are worth today, by overlaying text on the screen (the same way they translate the Gaelic language into English).

For example, in Episode 4 of the first season, one of the Guinness brothers is attempting to negotiate his annual payment from the family fortune. He asks for 4,000 pounds per year. On the screen the text flashes “Six Hundred Thousand Today.”

The creators of the show are to be commended for giving viewers some context, rather than leaving them baffled or pausing the show to Google it. But is 600,000 pounds today a good estimate? Where did they get this number? As with the “Gilded Age” estimate, it’s complicated, but it is probably more than you think.

Here is a chart of the Core Personal Consumer Index for inflation (Core PCE), which is the Fed’s favorite measure on inflation, from 1970 through early 2024:

This chart is from an article by the Richmond Fed, The Origins of the 2 Percent Inflation Target. That article has a long discussion of how and why the Fed decided to name an explicit inflation target of 2% in 2012. Although controlling inflation has been formally part of the Fed’s “dual mandate” since the Federal Reserve Reform Act of 1977, it had traditionally not set a single numerical target. After years of discussions within the Fed, it was decided that the benefits of a clear single target outweighed the potential downsides. 2% was though to be about the lowest you could run, while still giving the Fed some room to cut short term rates in a recession without running up against the dreaded zero lower bound. It was understood that 2% was a loose target, with some years a little over or under to be allowed to balance each other out.

That Richmond Fed article was published in early 2024. At that point, inflation was falling quickly and steadily from its post-Covid high, as consumers finished spending down their gigantic stimulus package windfalls.

Unsurprisingly, this article concludes that “Even during this period, long-run inflation expectations have remained anchored, rising no higher than 2.5 percent, according to the Cleveland Fed.”

That was about 18 months ago. The actual path of inflation since then has not be a descent to 2-2.5%. Between gigantic peacetime deficits by two administrations, and the results of tariffs, inflation seems to have leveled out at around 3%:

The sub-2% inflation that was normal for twenty years (2000-2020) may now be a lost world. This puts the Fed in an awkward spot. Even ignoring the irresponsible squawking from some quarters of the government, it will not be an easy decision to keep cutting rates (to address soft employment) if inflation stays this high. The Fed’s mantra this time around is that the current inflation is just a transient response to tariffs and so can be largely discounted. But I recall similar verbiage in 2021, as the Fed dismissed the ramping inflation back then as merely a transitory effect of pandemic supply chain restrictions. They were wrong then, and I suspect it would be wrong now to be too complacent. The 1970s-80’s showed that once the inflation genie gets out of the bottle, it can be very costly to subdue it. Whether 2.0 % is still the right target, however, may be open to debate.

My new article, “Prohibition and Percolation: The Roaring Success of Coffee During US Alcohol Prohibition”, is now published in Southern Economic Journal. It’s the first statistical analysis of coffee imports and salience during prohibition. Other authors had speculated that coffee substituted alcohol after the 18th amendment, but I did the work of running the stats, creating indices, and checking for robustness.

My contributions include:

National and state indices for coffee and coffee shops from major and local newspapers.

A textual index of the same from book mentions.

I uncover that prohibition is when modern coffee shops became popular.

The surge in coffee imports was likely not related to trade policy or the end of World War I

Both demand for coffee and supply increased as part of an intentional industry effort to replace alcohol and saloons.

An easy to follow application of time series structural break tests.

An easy to follow application of a modern differences in differences method for state dry laws and coffee newspaper mentions.

Evidence from a variety of sources including patents, newspapers, trade data, Ngrams, naval conflicts, & Wholesale prices.

Generally, the empirical evidence and the main theory is straightforward. I learned several new empirical methods for this paper and the economic logic in the robustness section was a blast to puzzle-out. Finally, it was an easy article to be excited about since people are generally passionate about their coffee.

Bartsch, Zachary. 2025. “Prohibition and Percolation: The Roaring Success of Coffee During US Alcohol Prohibition.” Southern Economic Journal, ahead of print, September 22. https://doi.org/10.1002/soej.12794.

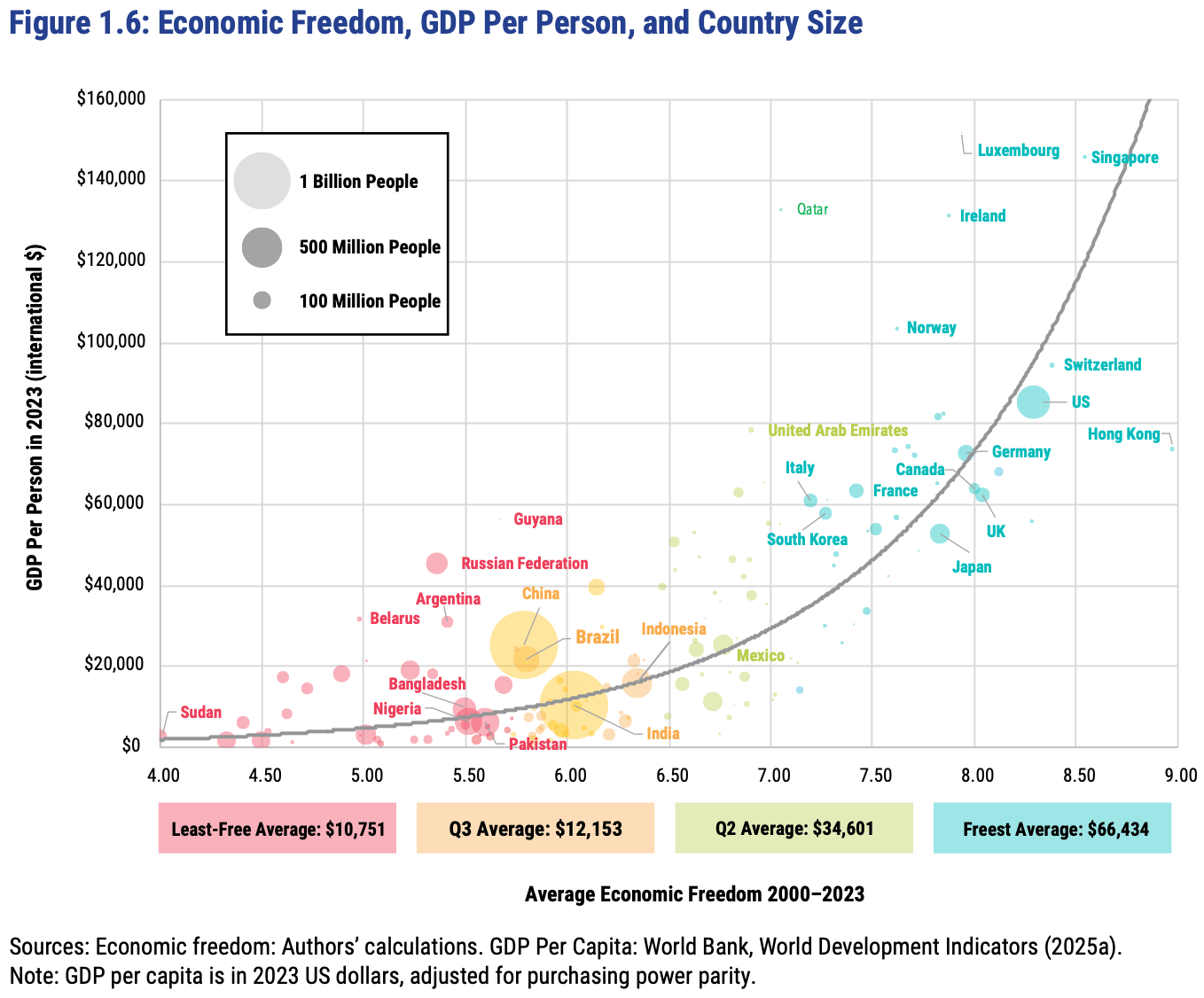

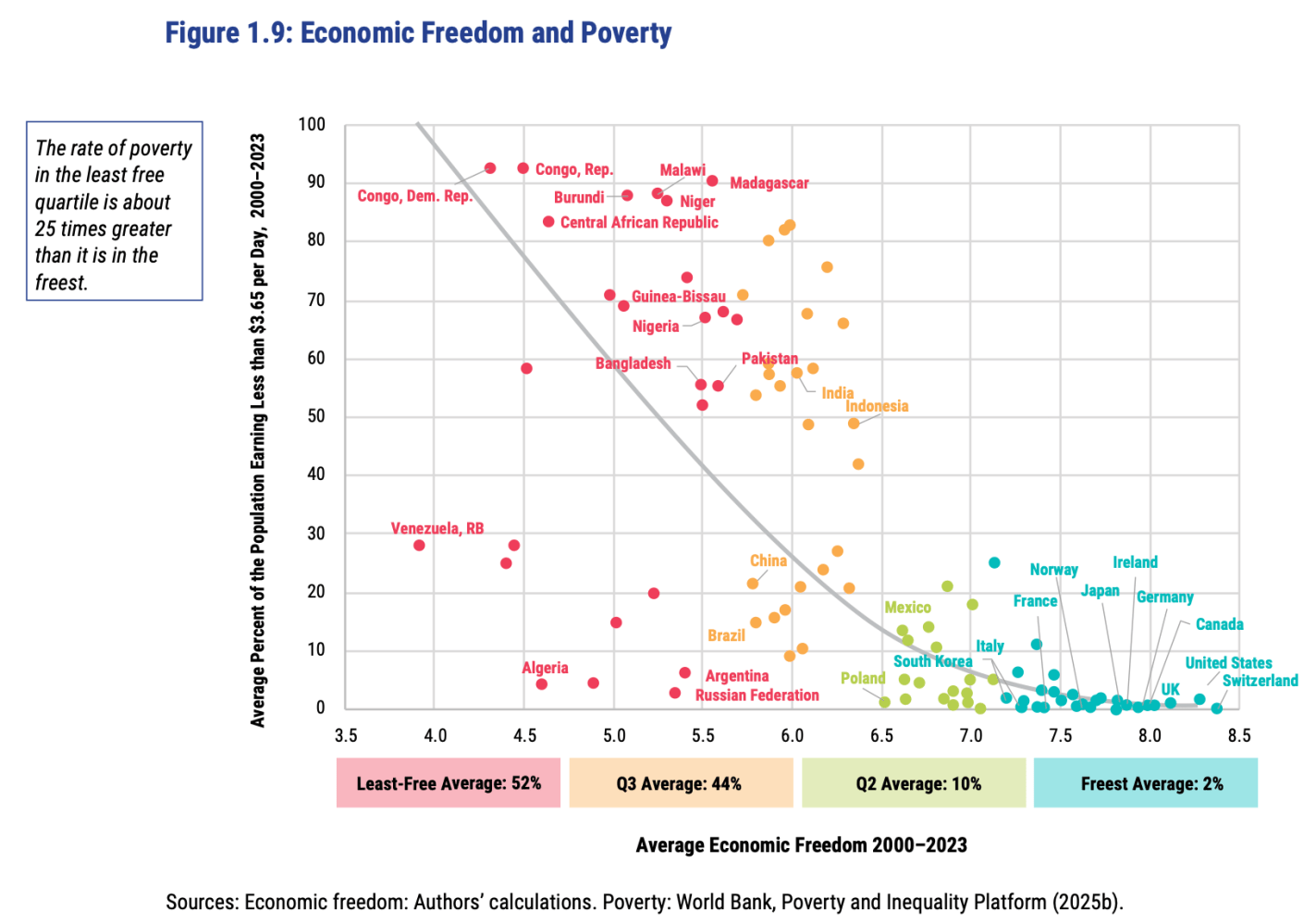

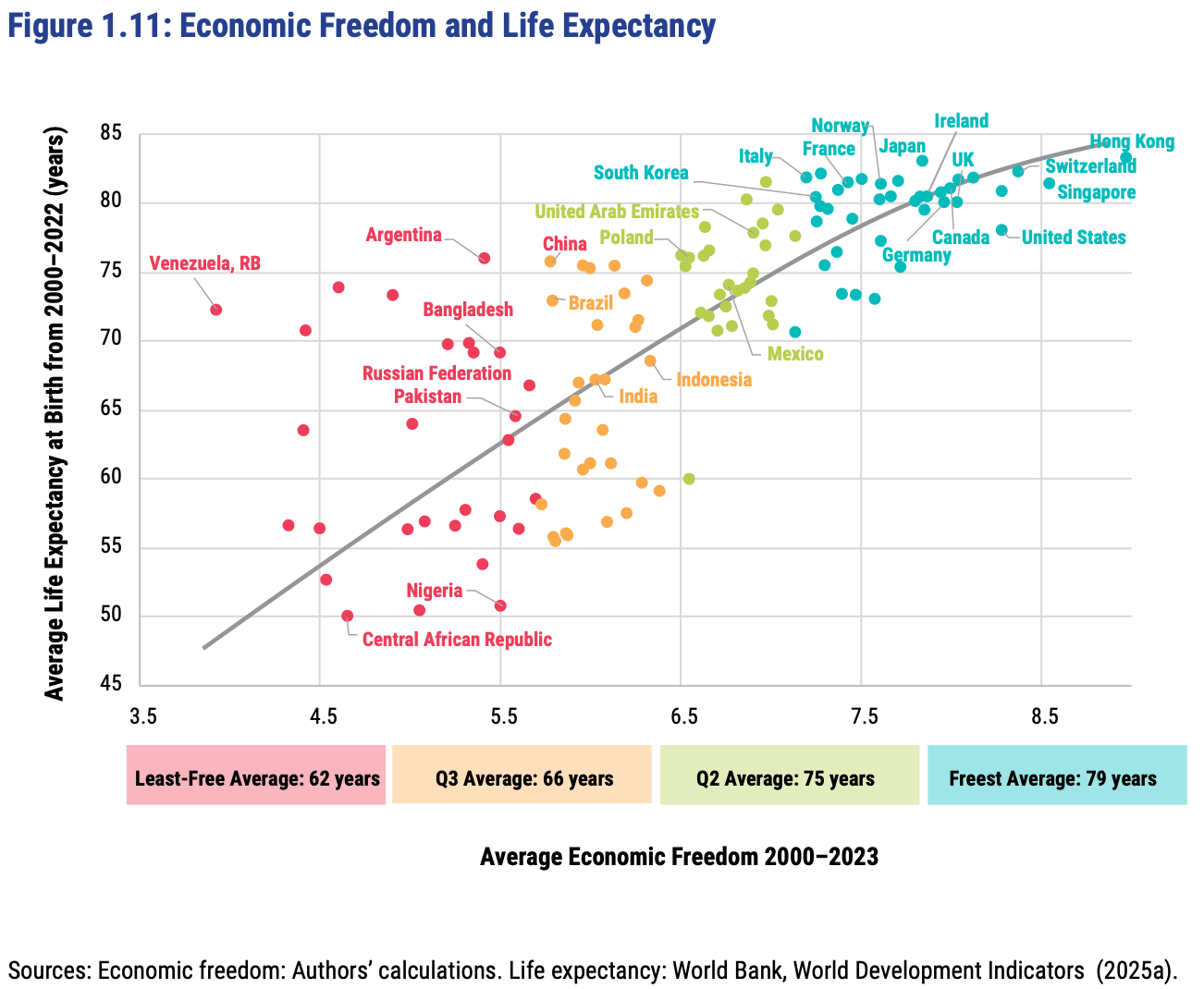

The Fraser Institute released their latest report on the Economic Freedom of the World today, measuring economic policy in all countries as of 2023. They made this excellent Rosling-style graphic that sums up their data along with why it matters:

In short: almost every country with high economic freedom gets rich, and every country that gets rich either has high economic freedom or tons of oil. This rising tide of prosperity lifts all boats:

This greater prosperity that comes with economic freedom goes well beyond “just having more stuff”:

The full report, along with the underlying data going back to 1970, is here. The authors are doing great work and releasing it for free, so no complaints, but two additional things I’d like to see from them are a graphic showing which countries had the biggest changes in economic freedom since last year, and links to the underlying program used to create the above graphs so that readers could hover over each dot to identify the country (I suppose an independent blogger could do the first thing as easily as they could…).

FRDM is an ETF that invests in emerging markets with high economic freedom (I hold some), I imagine they will be rebalancing following the new report.

Housing is certainly more expensive than in the past. I have written about this several times, including a post from last year showing that between about 2017 and 2022 housing started to get really expensive almost everywhere in the US, not just on the West Coast and Northeast (as had previously been the case). I don’t think the housing affordability crisis is in serious doubt anymore, and it can’t be explained over the past few years by increasing size and amenities, since those haven’t changed much since 2017 (though it is relevant when comparing housing prices to the 1970s).

But why did this happen? Knowing why is crucial, not merely to blame the causes, but because the policy solution is almost certainly related to the causes. I and many others have argued that supply-side restrictions, such as zoning laws, are the primary culprit. The policy solution is to reduce those restrictions. But a recent op-ed titled “Why your parents could afford a house on one salary – but you can’t on two,” the authors place the blame for housing prices (as well as the stagnation of living standards generally) on a different factor: Nixon’s 1971 “severing the dollar’s link to gold.” The authors have a book on this topic too, which I have not yet read, but they provide most of the relevant data in this short op-ed.

Does their explanation make sense? I am skeptical. Here’s why.

But as Jeremy often points out here, young adults have actually been doing pretty well at building wealth. So why are they so gloomy?

Since I’ve now aged out of the young adult category, I’m obligated to start by wondering if kids these days are just whinier, and need to quit doomscrolling and toughen up. But if I try to see things their way, here’s what I can come up with for why their pessimism could be rational:

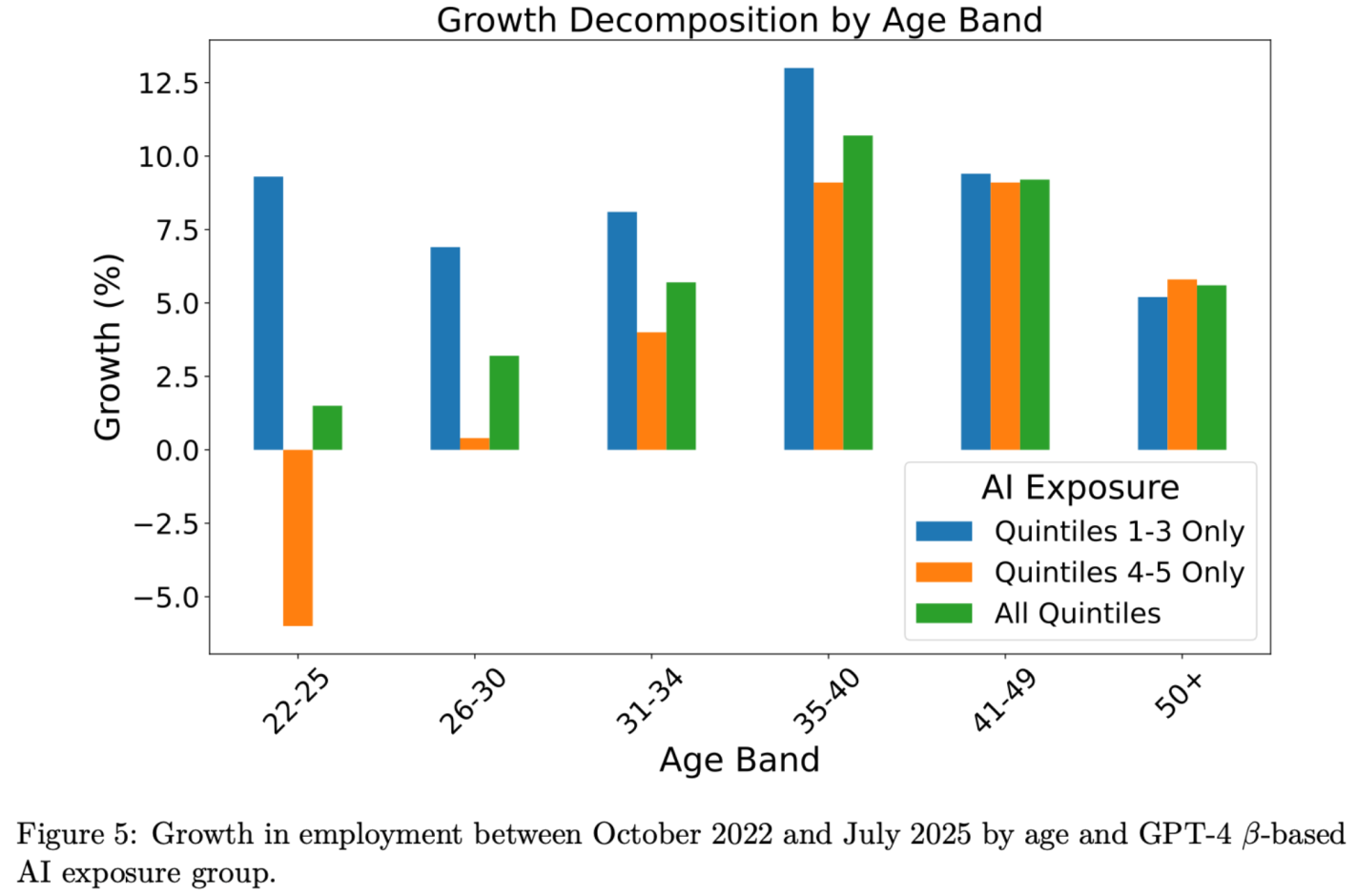

It’s About The Future: Sure things have been fine, but that is about to change. The more farsighted youth know they will be the ones expected to pay back the big deficits the Federal government is running. They have student loans to pay today now that payments have fully resumed. I predicted after the 2022 student loan forgiveness that we would be back to all-time highs in student debt by 2028, but in fact we are there already. The youth unemployment rate is now 10.5%, up from 6.6% in April 2023, and could rise a lot more if AI really starts displacing jobs:

Source: Brynjolfsson, Chandar and Chen 2025.Source: Michigan Consumer Survey

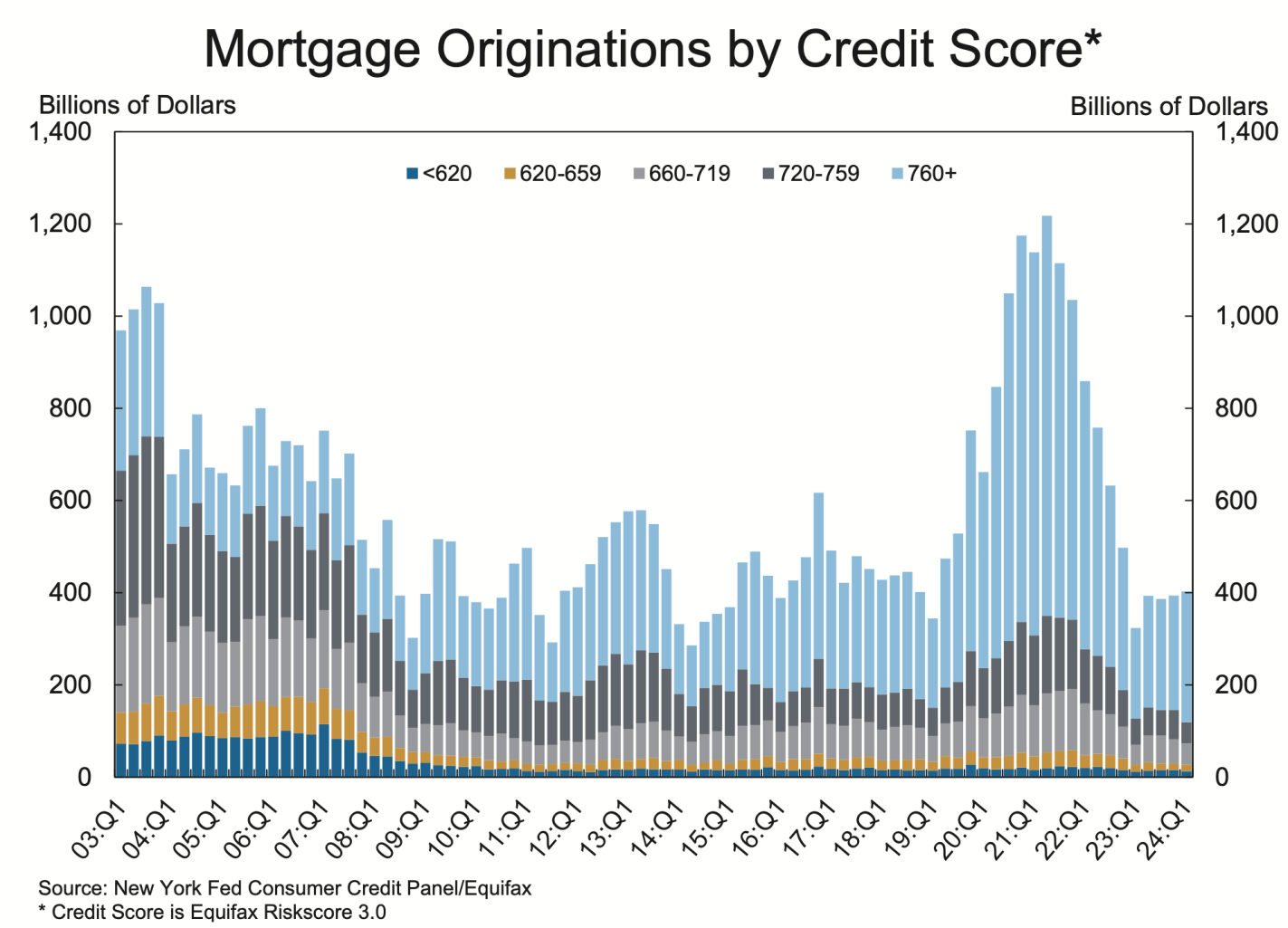

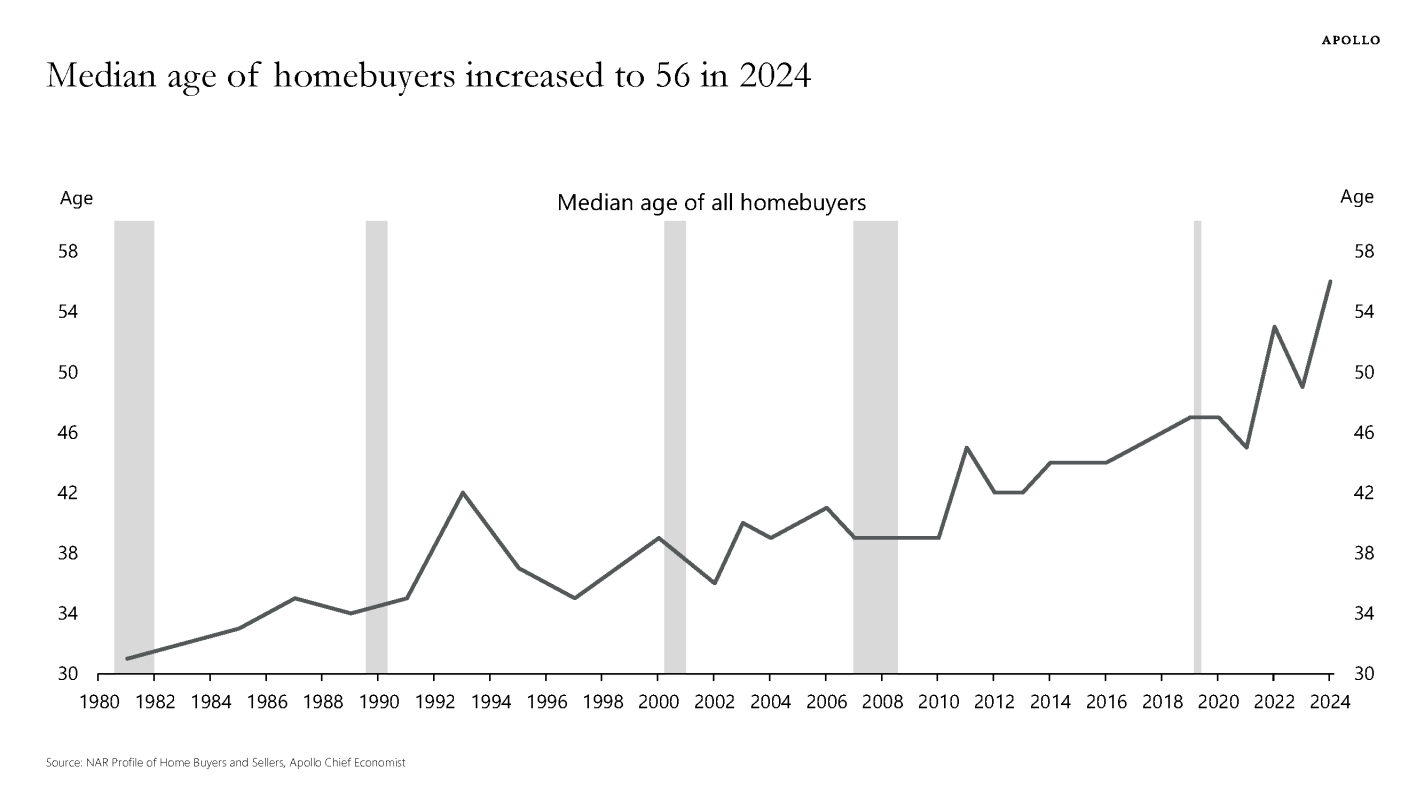

2. It’s About Housing: House prices are at all time highs (far above the prices during the 2000s “bubble”). Mortgage rates remain high, and to the extent that Fed rate cuts push them down, they will likely push prices higher, leaving homes hard to afford. High credit standards post-Dodd-Frank mean younger buyers in particular find it hard to get a mortgage; homeownership rates are falling while the average age of homeowners shoots upward. Most older people already own a house, while most young people want to buy but see that as increasingly out of reach.

Good luck getting a mortgage without super-prime creditEveryone thinks it’s a bad time to buy a house, but this matters most if you’re young and don’t already own oneThe median American is 39 years old but the median homebuyer is 56