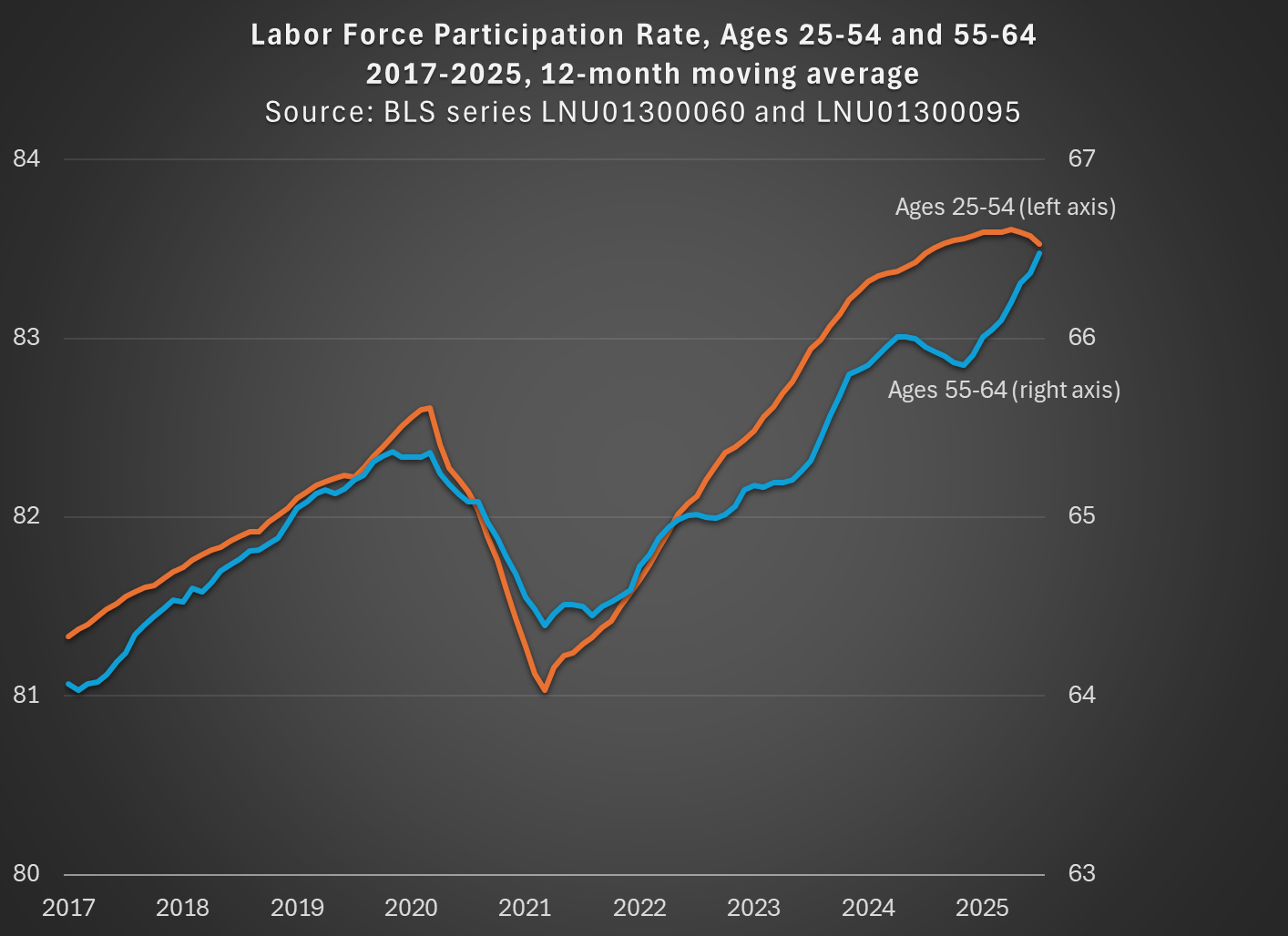

“Both younger and older workers withdrew from the labor force in large numbers during the pandemic: In fact, their participation rates plummeted. Yet, within two years, the younger workers had bounced back to their pre-pandemic participation rates. But the older workers have not.”

They include a chart which seems to back up that assertion:

However, if you look closely, you will see that the older workers’ age group is open-ended. It includes 55-year-olds, as well as 95-year-olds. Given that the US population is aging, this seems like a poor choice.

While not available currently in the FRED database, there is data from BLS available for older workers that is not open-ended. For example, we can look at workers ages 55-64, who are older but still young enough that they are mostly below traditional retirement age. I use that data and compare with the 25-54 age group (note: because the 55-64 data isn’t available seasonally adjusted, I use the non-adjusted data for both age groups, then use a 12-month average, so my chart doesn’t exactly replicate the chart above):

By using a closed-end age group for older workers, we see that labor force participation has not only recovered from the pandemic, but it exceeds the pre-pandemic peak for both prime-age and older workers, and had done so by the Spring of 2023. In fact, both are now about 1 percentage point above February 2020. If we want to go to the first decimal place, older workers have actually increased their labor force participation slightly more: 1.1 vs 0.9 percentage points. But these are close enough, given that this is survey data, to say the recovery has been roughly equal.

The St. Louis Fed blog concludes by saying that early workforce retirements “will continue to depress the labor force participation rate of workers aged 55 and older for the foreseeable future.” But it’s not true that the LFPR of older workers is depressed! Provided that we exclude those 65 and older.

You may have heard that there are roughly 7 million men of working age that are not currently in the labor force — that is, not currently working or looking for work. The statistic has been produced in various ways using slightly different definitions by different researchers, but the most well-known is from Nicholas Eberstadt who uses the age cohort of 25-55 years old and gets about 7 million (in 2015). More recently and perhaps more prominently is from Senator JD Vance, and as with almost all issues he has tied this to illegal immigration.

The 7-million-men statistic is true enough, and if we limit it to native-born American men with native-born parents (I assume this is the group Vance is concerned about), we can get right at 7 million non-working men in 2024 by expanding the age cohort slightly to 20-55 year olds.

Why are these men not working? According to what they report in the CPS ASEC, here are the reasons broken down by 5-year age cohort (I drop 55-year-olds here to keep the group sizes equal, which shrinks the total to 6.7 million men):

By far the largest reason given for not working is illness or disability, which is 42% of the total for all of these men, the largest reason for every age group except 20-24 (who are mostly in school if they aren’t working), and it’s the majority for workers ages 30-54 (about 56% of them report illness or disability). Slightly less than 10% report “could not find work” as the reason they weren’t working, which is about 650,000 men in this age group (and are native-born with native-born parents). And over half of those reporting that they couldn’t find work are under age 30 — for those ages 30-54, it’s only about 7% of the total.

More men report that they are taking care of the home/family (800,000) than report not being able to find work (650,000). And a lot more report that they are currently in school — almost 1.5 million, and even though they are mostly concentrated among 20–24-year-olds, about one-third of them are 25 or older.

It’s certainly true that the number of working age men in the labor force has fallen over time. In 1968, 97% of men ages 20-54 had worked at some point in the past 12 months (that’s for all men regardless of nativity, which isn’t available back that far in the CPS ASEC). In 2024, that was down to about 87%. But even if we could wave a magical wand and cure all of the men that are ill or disabled, this would add less than 3 million people to the labor force, not nearly enough to make up for all of the immigrants that Vance and others are suggesting have taken the jobs of native-born Americans.

I keep reading about how inflation has peaked (even peaked many months ago) and so any minute now the Fed will relent on raising interest rates, and will in fact start reducing them. Every data point that seems to support an early Fed pivot and a gentle “soft landing” for the economy is greeted with optimistic verbiage and a rip higher in stocks.

Except – – other meaningful data points regularly appear which show that inflation (especially core inflation) is remaining stubbornly high. The Personal Consumption Expenditures (PCE) Index is the Fed’s preferred way to track core inflation. It did peak in early 2022, and is falling, but very slowly and fitfully. Just when it seems like it is about to cascade downward, along comes another uptick. The latest report for 02/24/23 showed the PCE index (excluding the volatile categories of food and energy) increasing 0.6 percent during the month of January, which translated to a 4.7 percent year-on-year gain. That was considerably higher than the 0.4 percent monthly gain (4.3 percent year-on-year) that economists expected.

The chart below illustrates the chronic tendency of the economists at the Fed to lowball the estimates of future inflation. Each of the ten bars depicts quarterly projections of what inflation would be for 2023, starting back in September 2020 (first, green bar). No one in the craziness of 2020 could be held particularly responsible back then for accurately projecting 2023 conditions. But the Fed embarrassed themselves badly into late 2021 by airily dismissing inflation as “transitory”, due mainly to supply chain constraints that would quickly pass. (See towards the middle of the chart, yellow Sept 2021 and blue Dec 2021 bars projecting a mere 2.2% inflation for 2023.)

Only as of December 2022 did estimates of inflation jump up to 3.1% for 2023, and that estimate will surely get revised upward even further.

Many factors probably went into this systematic failure on the part of the Fed economists. There are probably political reasons for erring on the rosy optimistic side, which I will not speculate on here.

One factor in particular was mentioned in the Minutes of the Jan 31/Feb 1 Fed meeting that I thought was significant:

A few participants remarked that some business contacts appeared keen to retain workers even in the face of slowing demand for output because of their recent experiences of labor shortages and hiring challenges.

Jeremy LaKosh notes regarding this feature, “If true across the economy, the idea of keeping employees for fear of facing the labor force shortage would represent a fundamental shift in the employment market. This shift would make it harder for wage increases to mitigate towards historical norms and keep upward pressure on prices.”

This all rings true to my anecdotal observations. In bygone days, when business slowed down, factories would lay off or furlough workers, with the expectation on all sides that they would call the workers back (and the workers would come back) when conditions improved. However, employers have had to struggle so hard this past year to find willing/able workers, that employers are loath to let them go, lest they never get them back. I have read that even though homebuilders are not sure they can sell the houses they are building, they are so worried about losing workers that they are keeping them on the payroll, building away.

Other inflation data points show big decreases in prices for goods (and energy), but not for services. Wages, of course, are the big driver for service costs.

So the inflation story in 2023 seems to come down largely to a labor shortage. This is a large topic cannot be fully addressed here. I will mention one factor for which I have anecdotal support, that the enormous benefits (stimulus money plus enhanced unemployment) paid out during 2020-2021 set up a large number of baby boomers to leave the workforce early and permanently. Studies show that this is a major factor in the drop in workforce participation rate post-Covid. Maybe some of those folks had not planned ahead of time for such early retirement, but they got a taste of the good life (NOT getting up and going to work every day) in 2020-2021 along with the extra cash to pad their savings, and so they decided to just not return to work. That exodus of trained and presumably productive workers has left a hole in the labor force which now manifests as a labor shortage, which drives up wages and therefore inflation and therefore interest rates, which will eventually crater the economy enough that struggling firms will finally lay off enough workers to mitigate wage gains.

I wonder if this unhappy scenario could be staved off with increased legal migration of targeted skilled workers from other countries to alleviate the labor shortage. Dunno, just a thought.

More than 47 million workers quit their jobs in 2021, in what has become known as The Great Resignation. However, many of these workers are getting re-hired elsewhere. Hiring rates have outpaced quit rates since November, 2020.

The U.S. Chamber of Commerce has published some statistics on this reshuffling of the labor force, which I will reproduce here. As shown in the chart below, quit rates in leisure and hospitality (which require in-person attendance and pay lower salaries) were enormous. However, the recent hiring rates have been even higher in this area, so the shortage of labor there is only moderate.

When taking a look at the labor shortage across different industries, the transportation, health care and social assistance, and the accommodation and food sectors have had the highest numbers of job openings.

But yet, despite the high number of job openings, transportation and the health care and social assistance sectors have maintained relatively low quit rates. The food sector, on the other hand, struggles to retain workers and has experienced consistently high quit rates.

I am not sure I understand exactly what the following chart represents, but it was deemed important:

I think the % of yellow is the ratio of unemployed persons with experience in the field (i.e., who could readily participate) to the total job openings in that field. E.g., “…if every unemployed person with experience in the durable goods manufacturing industry were employed, the industry would only fill 65% of the vacant jobs.” These are interesting data, although I’d be even more interested in seeing numbers on unfilled job openings as fraction of total (filled and unfilled) job openings to give a better idea on how much each industry is hurting for labor. Anyway, here is some of the commentary from the article:

It is interesting to look at labor force participation across different industries. Some have a shortage of labor, while others have a surplus of workers. For example, durable goods manufacturing, wholesale and retail trade, and education and health services have a labor shortage—these industries have more unfilled job openings than unemployed workers with experience in their respective industry. Even if every unemployed person with experience in the durable goods manufacturing industry were employed, the industry would only fill 65% of the vacant jobs.

Conversely, in the transportation, construction, and mining industries, there is a labor surplus. There are more unemployed workers with experience in their respective industry than there are open jobs.

The manufacturing industry faced a major setback after losing roughly 1.4 million jobs at the onset of the pandemic. Since then, the industry has struggled to hire entry level and skilled workers alike.

And finally:

Some industries have been less impacted by labor shortages but are grappling with how to deal with the rise of remote work. For example, the rise of remote work might explain why there has been less “reshuffling” in business and professional services.

A better battery is an excellent gift, but for the gift that never needs recharging, a book is always a great idea. So this week Joy asked us to recommend a book. Again, this would be great as a gift or for yourself!

My recommendation is a very new book: Claudia Goldin’s Career and Family, which just came out this month. Confession: the book is so new, that I’ve only read about half of it so far! But this book is, as they say, self-recommending.

Goldin has spent almost her entire academic career studying the history of women’s participation in the US labor force. I think it’s fair to say that there is no person living today that knows more about the subject, possibly no one ever. This book is her attempt to sum up much of her research into a cohesive narrative about the changes in women’s labor force participation throughout the 20th century.

Her 2006 AEA Ely Lecture, “The Quiet Revolution,” was an earlier attempt to explain these long changes, and it is highly readable still today. Her 2014 AEA Presidential Address, “A Grand Gender Convergence,” is also excellent (watch the video of it too!). But this book brings all the ideas together into a complete narrative, tracking five cohorts of women and their experience in the labor force from 1900 to 2000. The last of these five cohorts matches the title of her book, the generation of women that entered the labor force since 1980 and now have a reasonable chance of achieving both an career and a family, rather than having to chose between the two.

This does not mean, and certainly Goldin would not say, that the journey is over and all is well for women today. Goldin focuses primarily on college graduates in this story, since they are the group most well-positioned to achieve the goal of having a career and a family. Obviously there are still challenges, and Goldin spends some time discussing one that the COVID pandemic revealed but was always there: the challenge of finding affordable childcare.

If you want a taste of the book, you can read or watch her 2020 Feldstein Lecture, “Journey Across a Century of Women.” But really the story is so complex that it does take a book to explain it all.