If you follow libertarian media such as Reason Magazine or its ancillaries, then you are well acquainted with the humdrum of “it goes without saying that most US programs should be ended“. They kind of just say this and then continue with their news. One of the favorites is to say that we should get rid of the Department of Education (ED). After all, 90% of K-12 education is paid for by states and localities. Here I was thinking “what does the Department of Education even do”?

Agreement is different from trust. I trust the Brookings Institute. They have a nice explainer on what ED does. It’s a quick overview and has plenty of the appropriate citations. I learned that most of what ED does concerns K-12 and is achieved through grants that have strings attached. Funding primarily goes to serving “educationally disadvantaged” communities (that have a high poverty rate). Funding also goes to programs for disabled children, minority education programs (like Howard University), and Indian tribes. They also administer Pell Grants and fund & regulate college loans (which are privately administered).

ED’s appropriated budget is online for anyone to see and includes pretty good detail about costs. The total discretionary cost of FY 2024 was $79 billion. The “mandatory” spending, which does not need to be voted on by congress every year, was $45 billion. For context, the entire federal FY 2024 expenditure was $6.75 trillion. So, eliminating the department of education *and* it’s responsibilities (an unpopular position) would reduce federal expenditures by 1.8%. For even more context, the budget deficit is $1.83 trillion or 27.1% of total federal expenditures. Eliminating ED and consolidating its responsibilities to other departments would save $0.6 billion. That assumes eliminating program administration, the ED office of civil rights, and the ED office of the inspector general.

John Bogle, the founder of Vanguard, wrote a short book in 2006 that explains his investment philosophy. I can sum it up at much less than book length: the best investment advice for almost everyone is to buy and hold a diversified, low-fee fund that tracks an index like the S&P 500.

Of course, a strategy that is simple to state may still take time to understand and effort to stick to. So the book helps to build intuition for why this strategy makes sense. I think Bogle makes his case well, though the book is getting a bit dated- the charts and examples end in 2006, and he sets up mutual funds as the big foil, when today it might be high-fee index funds or picking your own stocks.

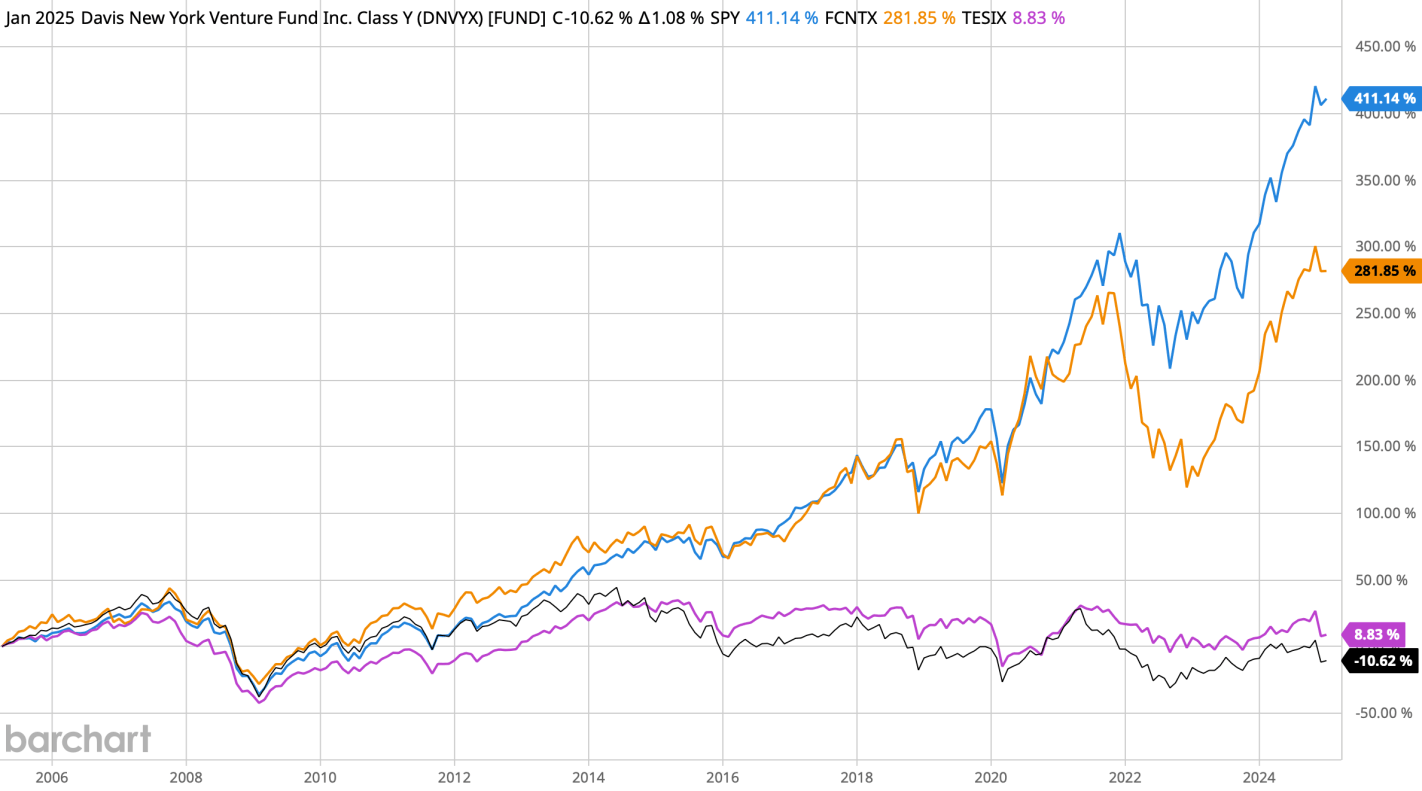

The silver lining of any dated investing book is that we can check up on how its predictions have fared. In chapter 8, Bogle compared the performance of the 355 equity mutual funds that existed in 1970 to that of the S&P over the 1970-2006 period. He notes that 223 of the funds had gone out of business by 2006, and even most of the surviving funds underperformed the S&P. But he identifies 3 funds that outperformed the S&P significantly (over 2% per year) on a sustained basis (consistently good performance, not just high returns at the beginning when they were small): Davis New York Venture, Fidelity Contrafund, and Franklin Mutual Shares. But how have they done since the book came out?

It is a huge victory for the S&P (in blue). Franklin Mutual Shares is basically flat over the past 20 years, while Davis New York Fund actually lost money. Fidelity Contrafund returned a respectable 281% (about 7% per year), and matched the S&P as recently as 2020. But as of 2025 the S&P is the clear winner, up 411% in 20 years (over 8% per year). Score one for Bogle.

But I still have to wonder if there is a way to beat the S&P- and I think one of Bogle’s warnings is really an idea in disguise. He warns repeatedly about “performance chasing”:

But whatever returns each sector ETF may earn, the investors in those very ETFs will likely, if not certainly, earn returns that fall well behind them. There is abundant evidence that the most popular sector funds of the day are those that have recently enjoyed the most spectacular recent performance, and that such “after-the-fact” popularity is a recipe for unsuccessful investing.

The claim is that investors pile into funds that did well over the past 1-3 years, but these funds subsequently underperform. But if this is true, could you succeed by reversing the strategy, buying into the unpopular sectors that have recently underperformed? I’ve been wondering about this, though I have yet to try seriously backtesting the idea. I was surprised to see Mr. Index Fund himself support such attempts to beat the market toward the end of his book:

Building an investment portfolio can be exciting…. If you crave excitement, I would encourage you to do exactly that. Life is short. If you want to enjoy the fun, enjoy! But not with one penny more than 5 percent of your investment assets.

He goes on to say that even for the fun 5% of the portfolio he still doesn’t recommend hedge funds, commodity funds, or closet indexers. But go ahead and try buying individual stocks, or actively managed mutual funds “if they are run buy managers who own their own firms, who follow distinctive philosophies, and who invest for the long term, without benchmark hugging.”

You may have seen on your social media recently that the price of TVs has fallen 98% since 2020. That’s certainly what the data from the BLS says. This would seem to imply that a one-thousand dollar TV in the year 2000 would now be priced at $20. While we have seen amazing things in the market for TVs, we’re not seeing $20 TVs. One take away might be that the data is just wrong. But that data is always wrong. The question is how the data is wrong and whether it’s a problem.

The reason for the disagreement between the data and the price on the shelves is due to something called ‘Hedonic Adjustment’. The idea is that some goods have quality features that change over time, even if the price doesn’t change so much. In the case of TVs, we might see higher resolution, flatter screens, larger screen sizes, smart features, etc. TVs are not a stable set of qualities. They are a bundle of characteristics, and those characteristics have some wiggle room while still satisfying some sensible criteria for being a TV. In theory, every single good is a bundle of services that we value. The reason that the some CPI categories have fallen so much is not only because the price has fallen necessarily. Rather, the amount of services that we get from a TV has increased so that each dollar that we spend can purchase more of those TV features.

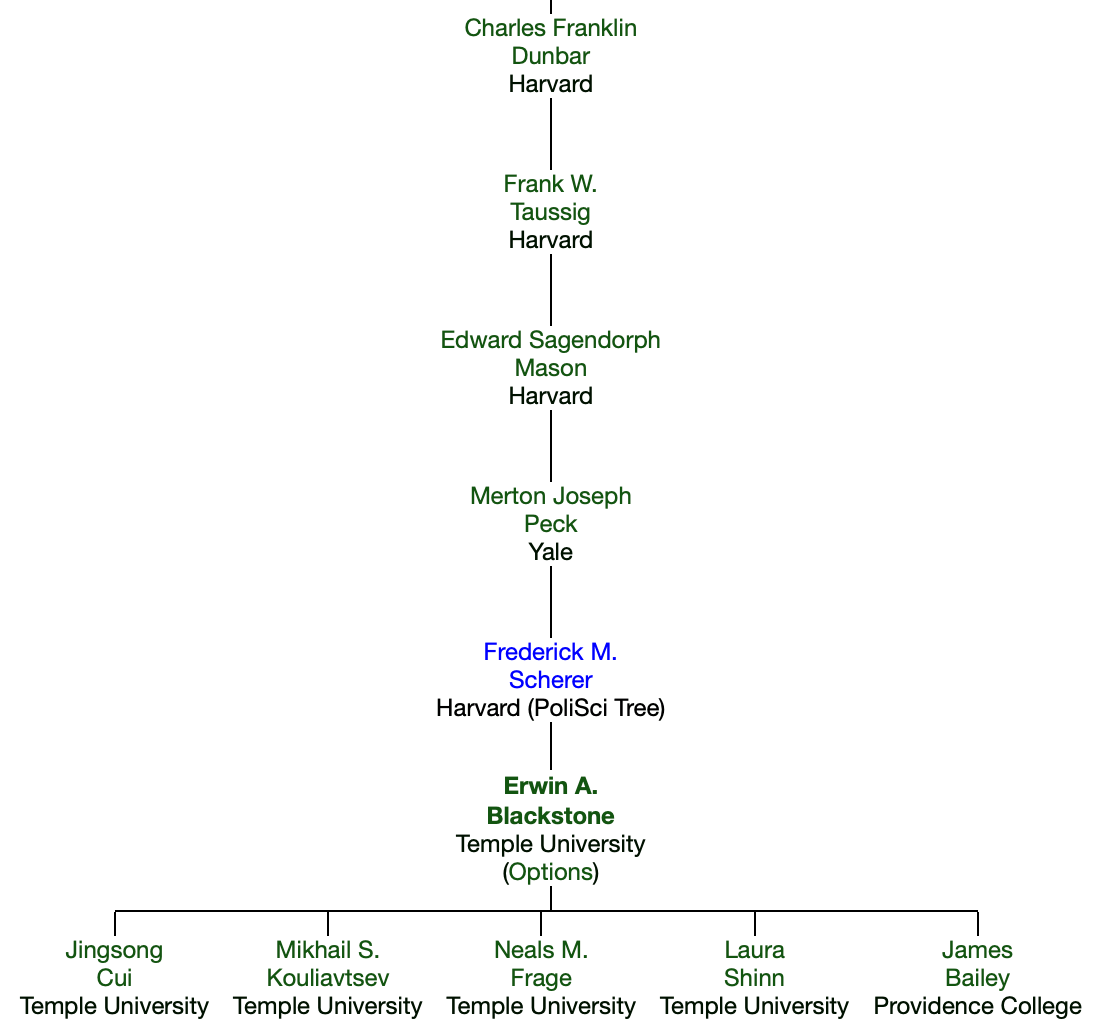

I’m told that Professor Erwin Blackstone died earlier this year, but I haven’t been able to find anything like an obituary online; consider this a personal memorial.

I knew Dr. Blackstone first as the professor of my Industrial Organization class at Temple University, where he taught since 1976. He was a model of how to take students seriously and treat them respectfully; he always called on us as “Mr./Ms. Last Name” and thought carefully about our questions.

Of course I learned all sorts of particular things about IO, especially US antitrust law and history- from Judge Learned Hand and baseball’s antitrust exemption to current merger guidelines and cases. I would later ask Dr. Blackstone to join my thesis committee, where he would heavily mark up my papers with comments and critiques.

He was a key part of how I was able to become a health economist despite the fact that Temple lacked a true health economist on the tenure-track economics faculty while I was there (as opposed to IO or labor economists who did some health). Blackstone’s coauthor Joseph Fuhr– a true health economist who also had Blackstone on the committee of his 1980 dissertation- came part-time to teach graduate health economics. Blackstone and Fuhr worked together to write the health economics field exam I took.

Finally, I learned from Blackstone by reading his papers. While he wrote many on health economics, my personal favorite was his work with Andrew Buck and Simon Hakim on foster care and adoption. It convincingly demonstrated the problems of having one fixed price in an area that most people don’t think about as a “price” at all- adoption fees. Having one fairly high fee for all children means the few seen as most desirable by adopting parents (typically younger, whiter, healthier) get adopted quickly, while those seen as less desirable by would-be adoptive parents linger in foster care for years. Like much of his work, it pairs a simple economic insight with a rich explanation of the relevant institutional details.

Academics hope to live on through our work- through our writing and the people we taught. Having taught many thousands of students at Cornell, Dartmouth, and Temple over 55 years, served on dozens of dissertation committees, and published over 50 papers and several books, I expect that it will be a long, long time before Erwin Blackstone is forgotten.

Source: Academic Tree. Charles Franklin Dunbar founded the Quarterly Journal of Economics in 1886.

Small, rural, private schools stand out to me as the most likely to show up on lists of closed colleges. This summer I discussed a 2020 paper by Robert Kelchen that identified additional predictors using traditional regression:

sharp declines in enrollment and total revenue, that were reasonably strong predictors of closure. Poor performances on federal accountability measures, such as the cohort default rate, financial responsibility metric, and being placed on the most stringent level of Heightened Cash Monitoring

Kelchen just released a Philly Fed working paper (joint with Dubravka Ritter and Doug Webber) that uses machine learning and new data sources to identify more predictors of college closures:

The current monitoring solution to predicting the financial distress and closure of institutions — at least at the federal level — is to provide straightforward and intuitive financial performance metrics that are correlated with closure. These federal performance metrics represent helpful but suboptimal measures for purposes of predicting closures for two reasons: data availability and predictive accuracy. We document a high degree of missing data among colleges that eventually close, show that this is a key impediment to identifying institutions at risk of closure, and also show how modern machine learning algorithms can provide a concrete solution to this problem.

The paper also provides a great overview of the state of higher ed. The sector is currently quite large:

The American postsecondary education system today consists of approximately 6,000 colleges and universities that receive federal financial aid under Title IV of the federal Higher Education Act…. American higher education directly produces approximately $700 billion in expenditures, enrolls nearly 25 million students, and has approximately 3 million employees

Falling demand from the demographic cliff is causing prices to fall, in addition to closures:

Between the early 1970s and mid-2010s, listed real tuition and fee rates more than tripled at public and private nonprofit colleges, as strong demand for higher education allowed colleges to continue increasing their prices. But since 2018, tuition increases have consistently been below the rate of inflation

Most college revenue comes from tuition or from state support of public schools; gifts and grants are highly concentrated:

Research funding is distributed across a larger group of institutions, although the vast majority of dollars flows to the 146 institutions that are designated as Research I universities in the Carnegie classifications…. Just 136 colleges or university systems in the United States had endowments of more than $1 billion in fiscal year 2023, but they account for more than 80 percent of all endowment assets in American higher education. Going further, five institutions held 25 percent of all endowment assets, and 25 institutions held half of all assets

Now lets get to closures. As I thought, size matters:

most institutions that close are somewhat smaller than average, with the median closed school enrolling a student body of about 1,389 full-time equivalent students several years prior to closure

As does being private, especially private for-profit (states won’t bail you out when you lose money):

As do trends:

variables measuring ratios of financial metrics and those measuring changes in covariates are generally more important than those measuring the level of those covariates

When they throw hundreds of variables into a machine learning model, it can predict most closures with relatively few false positives, though no one variable stands out much (FRC is Financial Responsibility Composite):

My impression is that the easiest red flag to check for regular people who don’t want to dig into financials is “is total enrollment under 2000 and falling at a private school”.

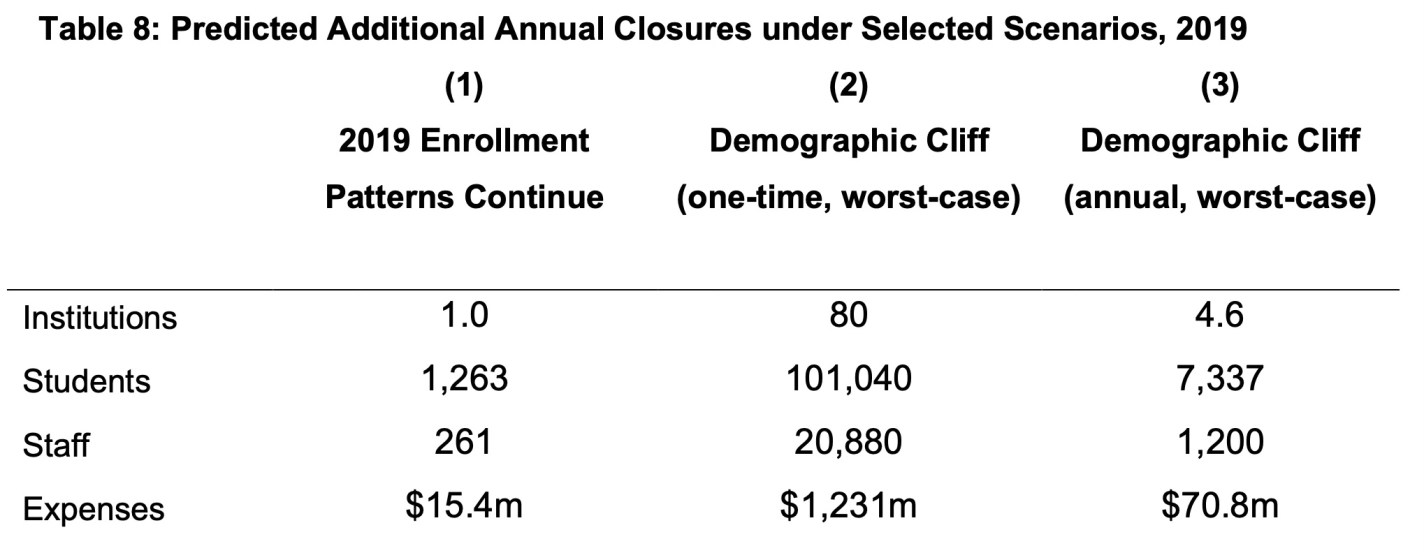

They predict that the coming Demographic Cliff (the falling number of new 18-year-olds each year) will lead to many more closures, though nothing like the “half of all colleges” you sometimes hear:

The full paper is available ungated here. I’ll close by reiterating my advice from the last post: would-be students, staff, and faculty should do some basic research to protect themselves as they consider enrolling or accepting a job at a college. College employees would also do well to save money and keep their resumes ready; some of these closures are so sudden that employees find out they are out of a job effective immediately and no paycheck is coming next month.

Rosenberg: What impact do you foresee in your field due to the increasing sophistication of AI, and what kind of skills do you think your students will need to be successful?

Buchanan: AI will reshape economic analysis and modeling, making complex data processing and predictive analytics more accessible. This will lead to more sophisticated economic forecasting and policy design. Economists will become more productive, and expectations will rise accordingly. While some fields might resist change, economics will be at the forefront of AI integration.

For students aiming to succeed, it’s crucial to embrace AI tools without relying on them excessively during college. Strong fundamentals in economic theory and critical thinking remain essential, coupled with data science and programming skills.

Interdisciplinary knowledge, especially in tech and social sciences, will be valuable. Adaptability and lifelong learning are key in this evolving field. Human skills like creativity, communication, and ethical reasoning will remain crucial.

While AI will alter economics, it will also present opportunities for those who can adapt and effectively combine economic thinking with technological proficiency.

Public choice economists emphasize the process by which we select political leaders. Electoral and voting rules influence the type of leaders we get. Institutional economists agree and go one step further. Who we choose matters less than the environment we place them in. Leaders, regardless of their personal qualities, respond to the incentives that surround them. The ultimate policies, therefore, largely conform to those incentives. From this perspective, it’s important to adopt institutional incentives for leaders to promote policies oriented toward economic growth and provide the option to flourish.

The same principle applies to the private economy. Productivity is crucial, and higher IQ often correlates with greater productivity. Yet, genetic endowment—including IQ—is beyond individual control. Many other determinants of productivity are not exogenous when we can affect policy. Let’s adopt policies that allow individuals with lower IQ to act productively as if they had higher IQ. Protecting the freedom to contract and private property rights creates conditions whereby even those at the lower end of the cognitive ability distribution can thrive. These principles expand their opportunities. Market signals give them valuable feedback on their activities and enable them to contribute to the economy.

When MOOCs (Massive Open Online Courses) burst onto the education scene in the early 2010s, they were hailed as the future of learning. With the promise of democratizing education by providing free access to world-class courses from top universities.

Leading universities rushed to put their courses online, venture capital poured in, and platforms like Coursera and edX grew rapidly. Yet today, while MOOCs still exist, they’ve largely retreated to the margins of education. Meanwhile, long-form podcasts have emerged as a surprisingly powerful force in American intellectual life.

Is this ironic? I wanted to learn a bit about MOOCs while I took a walk before writing this blog post. I typed “MOOCs” into the Apple Podcasts search bar.

I learned about MOOCs from Russ Roberts at a reasonable pace (when I listen to podcasts, I do it at 1x speed but I’m almost always doing something like driving or folding laundry).

I consider myself a lifelong learner. I buy and read books. Like hundreds of millions of people around the world, I like podcasts. I will attend lectures sometimes, especially if I personally know someone in the room. I did sit in classrooms for course credit throughout college and graduate school. I took extra classes that I did not need to graduate purely out of interest, and yet I have never once been tempted to sign up for a MOOC.

Enough introspection from me. My viral “tweet” this week was: “MOOCs never took off, as far as I can tell, and yet long-form podcasts are shaping the nation.”

Did MOOCs fail? Many millions of people signed up for MOOCs. A much smaller percentage of people completed MOOCs. Some users find MOOCs worth paying for.

However, if you listen to the podcast with John Cochrane in 2014, you can see the promise that MOOCs failed to live up to. The idea was that many people who did not have access to a “top quality” education would get one through MOOCs. Turns out that access is not the bottleneck.

I am one of several founders of a club with the abbreviation F.E.W. for Finance and Economics Women. This is a student organization that we have at Samford and that Dr. Darwyyn Deyo runs at San Jose State University.

Our short paper is mostly a how-to guide including a draft of a club charter document. We describe our institutions and how we use this group to engage and encourage students. Please read it for more details on how to start a club.

Like most student groups, the FEW model relies on student leaders who take initiative. Having done this for more than 6 years, we have a growing network of alumni and local business partners who connect to current students through FEW events. Personally, I am lucky that 3 faculty members total support the club at my school.

Women are often minorities in upper-division econ and finance classes. Women also have some unique challenges when it comes to choosing career paths and navigating the workplace. These events (e.g. bringing in a manager from a local bank to talk with student over lunch) allow a space for students to ask questions they might not normally ask in a classroom setting or in a standard networking environment.

We report the results of a small survey in our paper. We can’t infer causality, nor did we run any experiments. However, we did find that women were more likely to report that a role model in their chosen profession influenced their choice of major. Part of the purpose of the FEW model is to expose students to a variety of role models who they might not otherwise connect with.

Here’s a news article with a picture of the founding group at Samford. I have great appreciation and respect for our student leaders who keep it going, and I am grateful to the graduates who stay in contact with us.

If you didn’t know already, the past five years has been a whirl-wind of new methods in the staggered Differences-in-differences (DID) literature – a popular method to try to tease out causal effects statistically. This post restates practical advice from Jonathan Roth.

The prior standard was to use Two-Way-Fixed-Effects (TWFE). This controlled for a lot of unobserved variation over individuals or groups and time. The fancier TWFE methods were interacted with the time relative to treatment. That allowed event studies and dynamic effects.