If you follow libertarian media such as Reason Magazine or its ancillaries, then you are well acquainted with the humdrum of “it goes without saying that most US programs should be ended“. They kind of just say this and then continue with their news. One of the favorites is to say that we should get rid of the Department of Education (ED). After all, 90% of K-12 education is paid for by states and localities. Here I was thinking “what does the Department of Education even do”?

Agreement is different from trust. I trust the Brookings Institute. They have a nice explainer on what ED does. It’s a quick overview and has plenty of the appropriate citations. I learned that most of what ED does concerns K-12 and is achieved through grants that have strings attached. Funding primarily goes to serving “educationally disadvantaged” communities (that have a high poverty rate). Funding also goes to programs for disabled children, minority education programs (like Howard University), and Indian tribes. They also administer Pell Grants and fund & regulate college loans (which are privately administered).

ED’s appropriated budget is online for anyone to see and includes pretty good detail about costs. The total discretionary cost of FY 2024 was $79 billion. The “mandatory” spending, which does not need to be voted on by congress every year, was $45 billion. For context, the entire federal FY 2024 expenditure was $6.75 trillion. So, eliminating the department of education *and* it’s responsibilities (an unpopular position) would reduce federal expenditures by 1.8%. For even more context, the budget deficit is $1.83 trillion or 27.1% of total federal expenditures. Eliminating ED and consolidating its responsibilities to other departments would save $0.6 billion. That assumes eliminating program administration, the ED office of civil rights, and the ED office of the inspector general.

I was on a panel of economists last night at an event titled “The Economic Consequences of President Trump”. We each gave a 5-minute summary from our area of expertise and then opened up the floor for questions. This is a truncated summary of my talk. Since the panel included an investor, two industry economists, and another macro economist, I wanted to discuss something that was distinct from their topics. I’ve published a paper and refereed many articles concerning economic policy uncertainty (EPU) and asset volatility. I wanted to look at the data concerning President Trump – especially in contrast to Presidents Obama and Biden.

EPU matters because uncertainty can cause firms and individuals to delay investment and hiring decisions. Greater uncertainty can also cause divergent views concerning forecasted firm profitability. The result is that asset prices tend to become more volatile when EPU rises. One difficulty is that uncertainty occurs in our heads and concerns our beliefs, making it hard to measure. We try to get at it by measuring how often news media articles include the terms related to uncertainty, policy, and the economy. Since news content tends to report what is interesting, relevant, or salient to customers, there’s good reason to think that the EPU index is a decent proxy.

Using the Obama years as a baseline, the figure below simply charts out EPU. It was relatively low during Trump’s first term and then it was higher during Biden’s term – even after accounting for the Covid spike. The sharp increase toward the end is after Trump won the 2024 election. The EPU series conflicts with my perception of social media and media generally. My experience was that the media was far more attentive to the uncertainty that Trump caused. But, it may just be that the media outlets had plenty to report on rather than it being particularly indicative of EPU. After all, if the president exercises his power, then there is a certain swift decisiveness to it.

But if we look at a couple of particular policy areas, Trump’s administration faired worse. Specifically, Trump caused a ruckus concerning trade policy and immigration. Remember when Biden continued the aggressive trade policy that Trump had adopted? That’s consistent with lower EPU. Similarly, Biden made the immigration process much easier and faster while Trump’s deportation haranguing results in a somewhat stochastic means by which people are deported. Again, that spike at the end is after Trump won the 2024 election.

This week has been busy with the enjoyable task of hosting a distinguished economist in Alabama. I can only briefly follow up on my campfire post. (Yes, this is apropos of everything.)

I do not usually use LLMs to write even part of my posts but since I am pressed for time, I will just take this as a chance to assess Claude. I pay for Claude and Grok, currently. Both of those subscriptions resulted from a particular moment when I thought I could get a particular task done with them and was in a hurry. If I could do it all over again, I would undo those subs, I think, and go more in on the OpenAI Pro products.

Prompt: Finger wagging is surprisingly ineffective; telling a compelling story is surprisingly effective. Can you expand that out into a paragraph for a blog?

Claude response: The art of persuasion often defies our intuitive assumptions. While many of us default to stern lectures and admonishing fingers when trying to change minds, research consistently shows this approach tends to backfire, causing people to become defensive and dig deeper into their existing beliefs. What proves remarkably more effective is the simple act of storytelling. When we encounter a compelling narrative, our brains react differently than they do to facts and figures alone – we become emotionally invested, our neural patterns sync with the story’s flow, and we naturally lower our defensive barriers. Stories create a shared experience that bridges ideological divides, allowing new ideas to take root not through force, but through the gentle power of narrative empathy. This explains why parables and fables have been humanity’s preferred teaching tools for millennia, while memories of being lectured rarely inspire lasting change.

Claude is always a little too verbose, in my opinion. Still, the logic and grammar are good. The machines can write.

I might write more soon about how AI’s used narrative to influence humans in the novel The Diamond Age.

I normally like the Wall Street Journal; it is the only news page I check directly on a regular basis, rather than just following links from social media. But their “Biggest News Stories of 2024” roundup makes me wonder if they are overly parochial. When I try to zoom out and think of the very biggest stories of the past five to ten years, three of the absolute top would be the rapid rise of China and India, together with the astonishing growth in artificial intelligence capabilities.

All three of those major stories continued to play out this year, along with allsorts of otherthings happening in the two most populous countries in the world, and all the ways existing AI capabilities are beginning to be integrated into our businesses, research, and lives. But the Wall Street Journal thinks that none of this is important enough to be mentioned in their 100+ “Biggest Stories”.

To be fair, China and AI do show up indirectly. AI is driving the 4 (!) stories on NVIDIA’s soaring stock price, and China shows up in stories about spying on the US, hacking the US, and the US potentially forcing a sale of TikTok. But there are zero stories regarding anything that happened within the borders of China, and zero that let you know that AI is good for anything besides NVIDIA’s stock price.

Plus of course, zero stories that let you know that India- now the world’s most populous country, where over one out of every six people alive resides- even exists.

AI’s take on India’s Prime Minister using AI

This isn’t just an America-centric bias on WSJ’s part, since there is lots of foreign coverage in their roundup; indeed the Middle East probably gets more than its fair share thanks to “if it bleeds, it leads”. For some reason they just missed the biggest countries. They also seem to have a blind spot for science and technology; they don’t mention a single scientific discovery, and only had two technology stories, on SpaceX catching a rocket and doing the first private spacewalk.

The SpaceX stories at least are genuinely important- the sort of thing that might show up in a history book in 50+ years, along with some of the stories on U.S. politics and the Russia-Ukraine war, but unlike most of the trivialities reported.

I welcome your pointers to better takes on what was important in 2024, or on what you consider to be the best news source today.

The US Federal government has been considering major reforms like the REINS Act, which would require Congressional approval of major regulations proposed by executive branch agencies, or bringing back the “two in one out” rule from the first Trump administration. What would these do?

Right now it’s hard to say much for sure. But similar reforms have already been implemented in the states; as usual, the states provide a laboratory for investigating how policies work and whether they deserve broader adoption. It’s especially valuable to inform the debate over reforms like the REINS act that are still being considered at the federal level. Even for federal reforms that have already happened, it can be easier to evaluate the state version, since states make better control groups for each other than other countries do for the US.

But so far we’ve mostly been ignoring our laboratory results from recent state regulatory reforms. For instance, Broughel, Baugus, and Bose (2022) released a dataset that could be used to evaluate state regulatory reforms, but it has only been cited 3 times. This is why I’m adding this to my ideas page as a good subject for future academic research. Do state REINS or Red Tape Reduction Acts actually reduce either the stock or flow of regulation? If so, which types of regulations are affected, and does this have any effect on downstream measures like economic growth or new business formation?

Any research along these lines could help inform policy debates in the states, as well as for a new Presidential administration coming in with hopes of boosting economic growth through deregulation.

I thought this was going to be another election post, but it didn’t turn out that way.

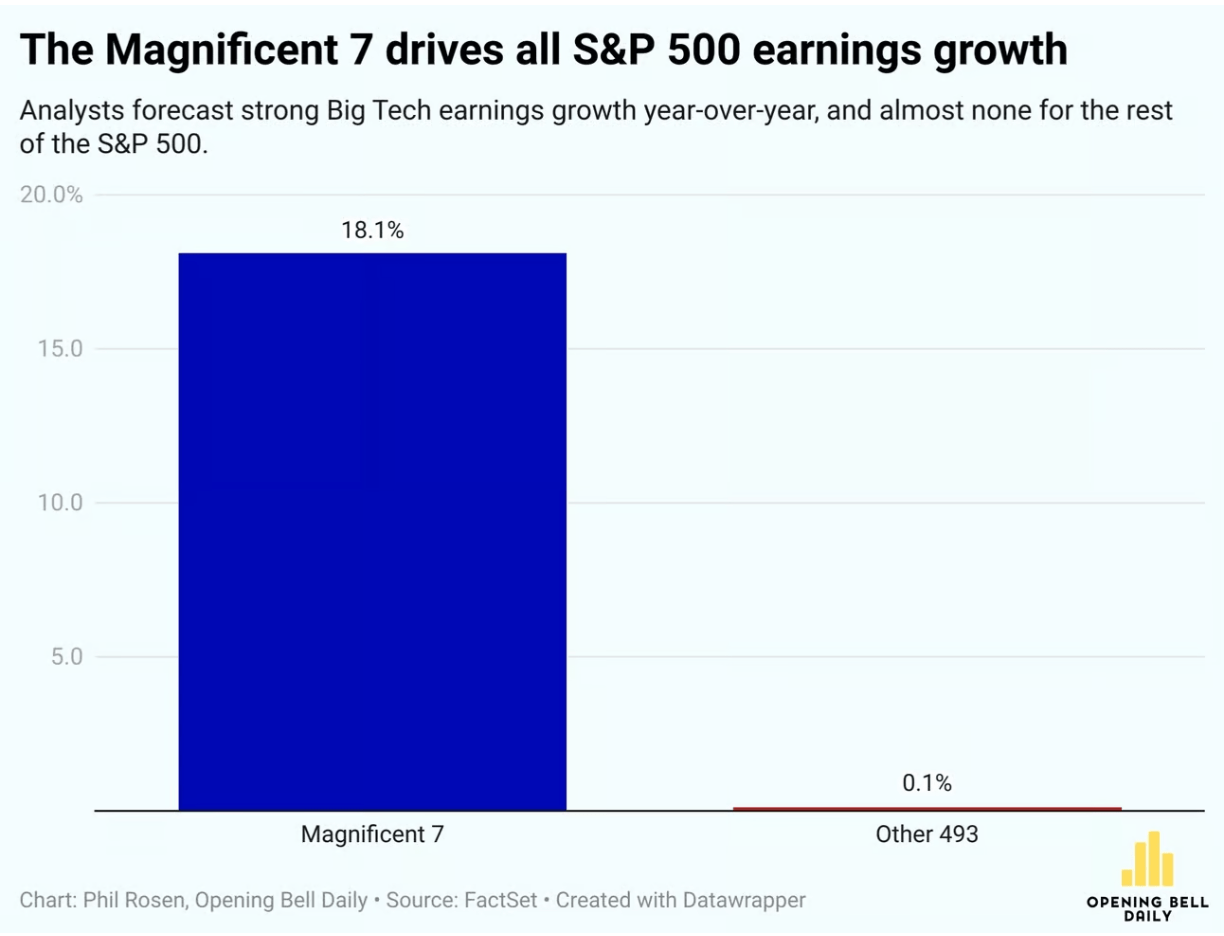

My plan was to do another annual portfolio review, with a focus on changes I’ll make to my portfolio as a result of how the election impacts various market themes, and how my take on the election differs from the market’s take. But as I looked at my portfolio, what struck me wasn’t how the election changes things, but instead how severely my stock picks underperformed the incredible 26% return the S&P has posted so far this year.

My first couple years of stock picking tended to match the S&P, roughly what you’d expect if markets are efficient and I’m just throwing darts. But more recently so much of the overall return of the market has been driven by just 7 mega-cap stocks, the “Magnificent 7”, that if you don’t own them you are probably underperforming big time.

Of course buying a broad index, especially a market-cap-weighted one like the S&P, is a way to ensure you own at least a piece of the big winners, which is one reason economists usually recommend buying the broad index. And I did this with 80% of my portfolio, to match my 80% belief in the efficient markets hypothesis. But I’m now back up to 90% belief in efficient markets, at least for stocks.

This efficiency seems to change a lot over time. Probably fewer than 10% of US stocks have obvious mis-pricings right now; really none stand out as super mispriced to a casual observer like me. Instead, it seems like every 10 years or so a broad swathe of the market is driven crazy by a bubble or a crash, and you get lots of mispricing- like tech in 2000, forced/panic selling at the bottom in 2009, or meme stocks in 2021. The rest of the time, the stock market is quite efficient. So, in typical times, just be boring and buy and hold a broad index fund.

Of course, you might think that AI is a bubble now. I certainly don’t love the 68 P/E on NVIDIA, but this doesn’t strike me as a true bubble driven by irrational hope- peoples’ hopes have proven well justified so far, with AI performing miracles and the Mag 7 delivering huge profits. So like Scott, I’m finally giving up on being overweight value stocks. Perhaps our capitulation is the sign that growth’s decade-plus run is finally about to reverse; but if so, I’ll try not to regret it. After all, the S&P has plenty of value stocks too.

When MOOCs (Massive Open Online Courses) burst onto the education scene in the early 2010s, they were hailed as the future of learning. With the promise of democratizing education by providing free access to world-class courses from top universities.

Leading universities rushed to put their courses online, venture capital poured in, and platforms like Coursera and edX grew rapidly. Yet today, while MOOCs still exist, they’ve largely retreated to the margins of education. Meanwhile, long-form podcasts have emerged as a surprisingly powerful force in American intellectual life.

Is this ironic? I wanted to learn a bit about MOOCs while I took a walk before writing this blog post. I typed “MOOCs” into the Apple Podcasts search bar.

I learned about MOOCs from Russ Roberts at a reasonable pace (when I listen to podcasts, I do it at 1x speed but I’m almost always doing something like driving or folding laundry).

I consider myself a lifelong learner. I buy and read books. Like hundreds of millions of people around the world, I like podcasts. I will attend lectures sometimes, especially if I personally know someone in the room. I did sit in classrooms for course credit throughout college and graduate school. I took extra classes that I did not need to graduate purely out of interest, and yet I have never once been tempted to sign up for a MOOC.

Enough introspection from me. My viral “tweet” this week was: “MOOCs never took off, as far as I can tell, and yet long-form podcasts are shaping the nation.”

Did MOOCs fail? Many millions of people signed up for MOOCs. A much smaller percentage of people completed MOOCs. Some users find MOOCs worth paying for.

However, if you listen to the podcast with John Cochrane in 2014, you can see the promise that MOOCs failed to live up to. The idea was that many people who did not have access to a “top quality” education would get one through MOOCs. Turns out that access is not the bottleneck.

Last week I laid out my own expectations for what economic policy would look like in a Trump or Harris presidency. Now after yesterday’s market reaction, we can infer what market participants as a whole expect by roughly doubling the size of yesterday’s market moves. Prediction markets had a 50-60% change of Trump winning as of Tuesday morning’s market close, which moved to a 99+% chance by Wednesday morning. Look at how other markets moved over the same time, multiply it by 2-2.5x, and you get the expected effect of a Trump presidency relative to a Harris presidency. So what do we see?

Stocks Up Overall: S&P 500 up 2%, Dow up 3%, Russell 2000 (small caps) up 6%. My guess this is mostly about avoiding tax increases- the odds that most of the Tax Cuts and Jobs Act gets renewed when it expires in 2025 just went way up. Lower corporate taxes boost corporate earnings directly, while lower taxes on households mean that they have more money to spend on their stocks and their products. Lower regulation and looser antitrust rules are also likely to boost corporate earnings.

Bond Prices Down (Yields Up): 10yr Treasury yields rose from 4.29% to 4.4%. This is the flip side of the tax cuts- they need to be paid for, and markets expect they will be paid for through deficits rather than cutting spending. The government will issue more bonds to borrow the money, lowering the value of existing bonds.

Dollar Up: The US dollar is up 2% against a basket of foreign currencies. I think this is mostly about the expected tariffs. People like the sound of the phrase “strong dollar” but it isn’t necessarily a good thing; it makes it cheaper to vacation abroad, but makes it harder to export, even before we consider potential retaliatory tariffs.

Crypto Way Up: Bitcoin went up 7% overnight, Ethereum is now 15% up since Tuesday. Crypto exchange Coinbase was up 31%. Markets anticipate friendlier regulation of crypto, along with a potential ‘strategic Bitcoin reserve’.

Single Stock Moves: Private prison stocks are up 30%+. Tesla is up 15%, mostly due to Elon Musk’s ties to Trump, but also due to tariffs. Foreign car companies were way down on the expectation of tariffs- Mercedes-Benz down 8%, BMW down 10%, Honda down 8%.

Sector Moves: Steel stocks are up on the expectation of tariffs, while solar stocks (which can’t catch a break, doing poorly under Biden despite big subsidies and big revenue increases) were down 12% in the expectation of falling subsidies. Bank stocks did especially well, with one bank ETF up 12%. This gives us one hint on what to me is now the biggest question about the second Trump administration- who will staff it? I could see Trump appointing free-market types, or wall-streeters in the mold of Steve Mnuchin, or dirigiste nationalist conservatives in the JD Vance / Heritage Foundation mold, or an eclectic mix of political backers like Elon Musk and RFK Jr, or a combination of all of the above. The fact that bank stocks are way up tells me that markets expect the free-marketers and/or the Wall-Street types to mostly win out.

Just Ask Prediction Markets: If you want to know what markets expect from a Presidency, you can do what I just did, look at moves the big traditional markets like stocks and bonds and try to guess what is driving them. But increasingly you can skip this step and just ask prediction markets directly- the same markets that just had a very goodelection night. Kalshi now has markets on both who Trump will nominate to cabinet posts, as well as the fate of specific policies like ‘no tax on tips‘

I doubt anyone has been waiting for my take on the Trump and Harris economic plans to decide their vote. More than that, it is entirely reasonable to vote based on things other than their economic plans entirely- like foreign policy, character, or preservingdemocracy. But either Trump or Harris will soon be President, and thinking through their economic plans can help us understand how the next 4 years are likely to go.

The bad news is that both campaigns keep proposing terrible ideas. The good news is that, thanks to our system of checks and balances, most of them are unlikely to become policy. The other good news is that our economy can handle a bit of bad policy- as Adam Smith said, there’s a lot of ruin in a nation. After all, the last Trump admin and the Biden-Harris admin did all sorts of bad economic policies, but overall economic performance in both administrations was pretty good; to the extent it wasn’t (bad unemployment at the end of the Trump admin, bad inflation at the beginning of Biden-Harris), Covid was the main culprit.

Note that this post will just be my quick reactions; the Penn Wharton Budget Model has done a more in-depth analysis. They find that Harris’ plan is bad:

We estimate that the Harris Campaign tax and spending proposals would increase primary deficits by $1.2 trillion over the next 10 years on a conventional basis and by $2.0 trillion on a dynamic basis that includes a reduction in economic activity. Lower and middle-income households generally benefit from increased transfers and credits on a conventional basis, while higher-income households are worse off.

We estimate that the Trump Campaign tax and spending proposals would increase primary deficits by $5.8 trillion over the next 10 years on a conventional basis and by $4.1 trillion on a dynamic basis that includes economic feedback effects. Households across all income groups benefit on a conventional basis.

We are already running way too big a deficit; candidates should be competing to shrink it, not make it worse. This isn’t just me being a free-market economist; Keynes himself would be saying to run a surplus in good economic times so that you have room to run a deficit in the next recession.

Now for my lightning round of quick reactions:

No tax on tips: both campaigns are now proposing this; it is a silly idea, there is no reason to treat tips differently from other income. The good news is that this almost certainly won’t make it through Congress.

Taxes: Trump’s Tax Cuts and Jobs Act of 2017 is set to expire in 2025. He says he wants to renew it and add more tax cuts, though he will need a friendly Congress to do so. Harris wants to let most of it expire, but renew and expand the Child Tax Credit while raising taxes on the wealthy and corporations. There’s a good chance we end up with divided government, in which case probably only the most popular parts of TCJA (increased standard deduction and child tax credit) get renewed and no big new changes happen.

Price controls: both campaigns, especially Harris‘, have talked about fighting ‘price gouging’, leading economists to worry about the price controls (any intro micro class explains why these are a bad idea). My guess is that no real bill gets passed, President Harris gets the FTC to make a show of going after grocery stores but nothing major changes.

Tariffs: Harris would probably leave them where they are; Trump is promising to raise them 10-20% across the board and 60% on China. This would lead to higher prices for US consumers and invite retaliation from abroad; we saw the same things when Trump raised tarriffs in his first term, but he is promising bigger increases now. This is worrisome because the President has a lot of power to change tariffs unilaterally; it would take a bill getting through Congress to stop this, and I don’t see that happening.

Regulation / One in two out: The total amount of Federal regulation stayed fairly flat during the Trump administration thanks to his one in two out rule, while regulation increased during the Biden-Harris administration. I expect that a second Trump admin would behave like the first here, while a Harris admin would continue the Biden-Harris trend.

Antitrust: FTC and DOJ have been aggressive during the Biden-Harris administration, blocking reasonable mergers and losing a lot in court. But Trump’s VP candidate JD Vance thinks FTC Chair Lina Khan is “doing a pretty good job”, so we could see this poor policy continue either way. More generally, voters should consider what a Vance presidency would look like, because making him Vice President makes it much more likely (Trump is 78 and people keep trying to shoot him; plus VPs get elected President at high rates).

Immigration: Immigration rates have been high under the Biden-Harris admin, while Trump’s top two planks in his platform are “seal the border” and “carry out the largest deportation operation in American history”. Economically, this would lead to a reduction in both supply and demand in many sectors, with the relative balance (so whether prices go up or down) depending on the sector. The exclusion of Mexican farmworkers in the 1960’s led to a huge increase in mechanization, to the point that domestic farmworkers saw no increase in their wages; presumably this also limited the potential harm to the food supply.

Crypto: The Biden admin has been fairly negative on crypto; both Harris and Trump are making pro-crypto statements in their campaigns, particularly Trump.

Marijuana: The Biden admin is in the process of rescheduling marijuana to no longer be in the most restricted category of drugs. I think Trump would probably see the process through, while Harris definitely would.

Elon Musk / Civil Service: Elon Musk has thrown his support hard behind Trump, spending lots of money, tweeting continuously, and attending rallies. It’s hard to know how much of this is genuine support for a range of Trump’s policies, how much is to get the Federal government to stop suing his companies so much, and how much is to get himself a direct role in government. In any case, it is a safe bet that more Federal civil servants get fired in a Trump admin than in a Harris admin. What’s much harder to say is how many get fired, and what proportion of firings come from a genuine attempt to improve efficiency vs a purge of those Trump sees as disloyal. Personally I think government could stand to treat its employees a bit more like the private sector, making it easier to fire people for genuine poor performance (not political views), but also allowing for more flexibility on improved pay, benefits, and the ability to focus on achieving goals more than following the way things have always been done. But I doubt that’s on the table either way.

CFTC/ Prediction Markets: The Biden CFTC has tried to crack down on prediction markets, though they have mostly failed in the courts, and the growth of Kalshi and Polymarket mean that prediction markets are now bigger than ever. Most of the anti-prediction-market decisions have been 3-2 votes of the democrats vs the republicans, so a new republican appointee could lock in the legal gains prediction markets have made, though this is far from guaranteed (not all Rs support this).

Final Thoughts: So much of how things turn out will depend not just on who wins the Presidency, but on whether their party wins full control of Congress. Because the Democrats have a lot more Senate seats up for grabs this year, Harris is much more likely to be part of a divided government (especially once you consider the Supreme Court).

Because of this, and because of the ability of the President to raise tariffs unilaterally, I see Trump as the bigger risk when it comes to economic prosperity, as well as non-economic issues. Harris with a Republican Senate is the best chance of maintaining something like the status quo, whereas a Trump victory is likely to see bigger changes, many of them bad.

That said, predicting the future is hard, and this applies doubly to Presidential terms. I’m struck by how often in my lifetime the most important decisions a President had to make had nothing to do with what the campaign was fought over. Who knew in 1988 that the President’s biggest task would be managing the breakup of the Soviet Union? In 2000, that it would be responding to 9/11? Bush specifically tried to distinguish himself from Gore as being the candidate more against “nation-building”, then went on to try just that in Afghanistan and Iraq. In 2004, who knew that the biggest issue of the term would be not Social Security or foreign policy, but a domestic financial crisis and recession? In 2016, who knew that they were voting on the President that would respond to the Covid pandemic? In 2020, who knew that they were voting on who would respond to Russia’s invasion of Ukraine?

The most important issue for the next President could easily be how they address China or AI, because those are clearly huge deals. I won’t vote based on this, because I don’t know who has the better plan for them, because I have no idea what a good plan looks like. Or the most important issue could be something that comes completely out of left field, like Covid did. Not even the very wise can see all ends.

What I do know is that, while much of the Libertarian Party has recently gone from its usual “goofy-crazy” to “mean-crazy“, Chase Oliver is so far the only candidate pandering to me personally. But it’s not too late for other politicians at all levels to try the same.

See you all again next Thursday, by which time the election will, I hope, be over.

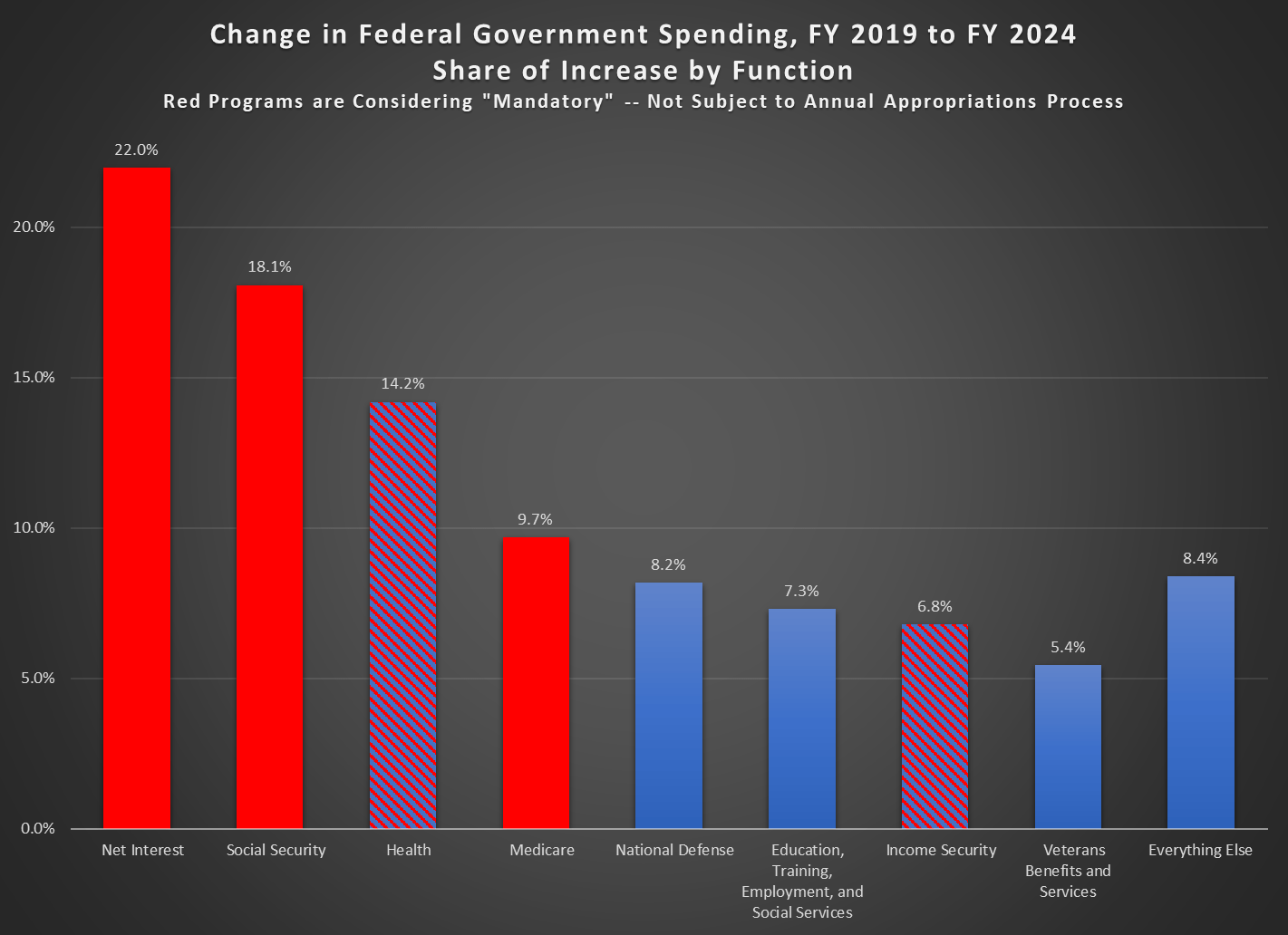

In Fiscal Year 2019, the US federal government spent $4.45 trillion dollars. In Fiscal Year 2024, spending was $6.75 trillion, or an increase of $2.3 trillion dollars. If you adjusted the 2019 number for inflation with the CPI, it would only be about $1 trillion more. Where did that additional $2.3 trillion go?

It will probably not surprise you that most of the increase in spending went to the largest categories of spending. Historically these have been health, Social Security, and defense, but now we must also include interest spending (roughly equal in size to defense and Medicaid in 2024). Indeed, with these areas of spending, 72 percent of the increase is accounted for. Add in the next three functions, and we’ve already accounted for over 90 percent of the increase.

Importantly, most of these categories are outside of the annual federal budget process, meaning that Congress does not need to approve new spending each year (Congress could change them, just as it could change any law, but it’s not part of the annual budgeting process). The “mandatory” categories, as they are called in federal law, are shaded red. I’ve striped with red and blue the health and income security functions, because some of this is subject to the annual budget process, but most of it is not. For example, Medicaid is not subject to the budget process (biggest part of the “health” function) and SNAP is not subject to the budget process (a big part of income security — it is set by the Farm Bill, usually on a five-year cycle).

So, when we talk about the $2 trillion increase since 2019, or the roughly $2 trillion cuts that would be needed to balance the budget, keep in mind that most of this is not subject to the annual budget process. It would require Congress to consider them specifically to enact cuts — though some big categories, such as Social Security, would be automatically cut under current law once their trust funds are exhausted (coming up on about a decade for the Social Security Old-Age Trust Fund).