Institutional vandalism is neither privatization nor creative destruction. It’s just cruelty masquerading as genius that plans to simply plead the necessary risk of endeavor when exposed as gratuitous incompetence. We may, within 10 years, see a newer, better NIH (or, preferably, cluster of baby NIHs) rise from the ashes. We may see a revitalized NSF and a whole slew of new institutions funding educaton research domestically and supporting the broader world through American aid programs. Maybe, maybe not.

But make no mistake: this is not a controlled burn. There is no plan, other than perhaps the wholly articulated belief that destruction wrought from chaos is a plan. This is a series of forest fires set by gleefull children with matches, wholly unable to even comprehend the risks they are taking on behalf of everyone else. We’ll probably get through to the other side, but for those of us who have been thinking about tail risk for a decade of Trump, the number of standard deviations between us and the unthinkable keeps getting smaller.

2004: In September 2004, Ukrainian presidential candidate Viktor Yushchenko was poisoned while running against pro-Russian candidate Viktor Yanukovych. After a dinner meeting, Yushchenko fell severely ill and his face became dramatically disfigured with cysts and lesions (chloracne). Medical tests in Vienna confirmed extreme dioxin poisoning. https://www.bbc.com/news/av/world-europe-43611547 The American liberal mind struggles to understand the difficulty of using elections under these conditions.

2018: “On March 4, 2018, British authorities say Russian agents poisoned Sergei Skripal—a former Russian military intelligence officer and U.K. double agent—and his daughter using a Novichok nerve agent…. With the immediate attack area isolated and the cleanup underway, the nation was shocked once again when two British nationals were poisoned by the same nerve agent nearly three months later in the neighboring town of Amesbury. One of the two, Dawn Sturgess, fell ill within 15 minutes of contact with the agent and died just over a week later. ” https://mwi.westpoint.edu/modern-day-nerve-agent-attack-military-lessons-salisbury/

If you get news from the internet and social media, be aware that some online participants are paid trolls from foreign governments.

Another pillar of this strategy involves botnets: swarms of fake, automated accounts created and controlled by Russian agents. These botnets hijack trending algorithms on social media platforms and thereby expose Western audiences to particular messages. They often share precisely worded posts to ensure that certain phrases—such as #WelcomeRefugees or #EndNetZero—trend in people’s news feeds. And they incessantly ‘like’ and repost content from pro-Kremlin influencers and trolls.

The aim here is twofold. First, it is an attempt to expand the reach of what would otherwise remain fringe opinions. They expose ever more people to Russian propaganda, and help create an illusion of popularity that serves to normalise pro-Kremlin talking points. But this is not merely intended to convert people into passionate Putinistas. The second goal is to promote the most inflammatory and divisive voices on either side of a given political issue. This helps spread the distrust and disillusionment that are so corrosive to liberal democratic society—and which have reached record levels on social media.

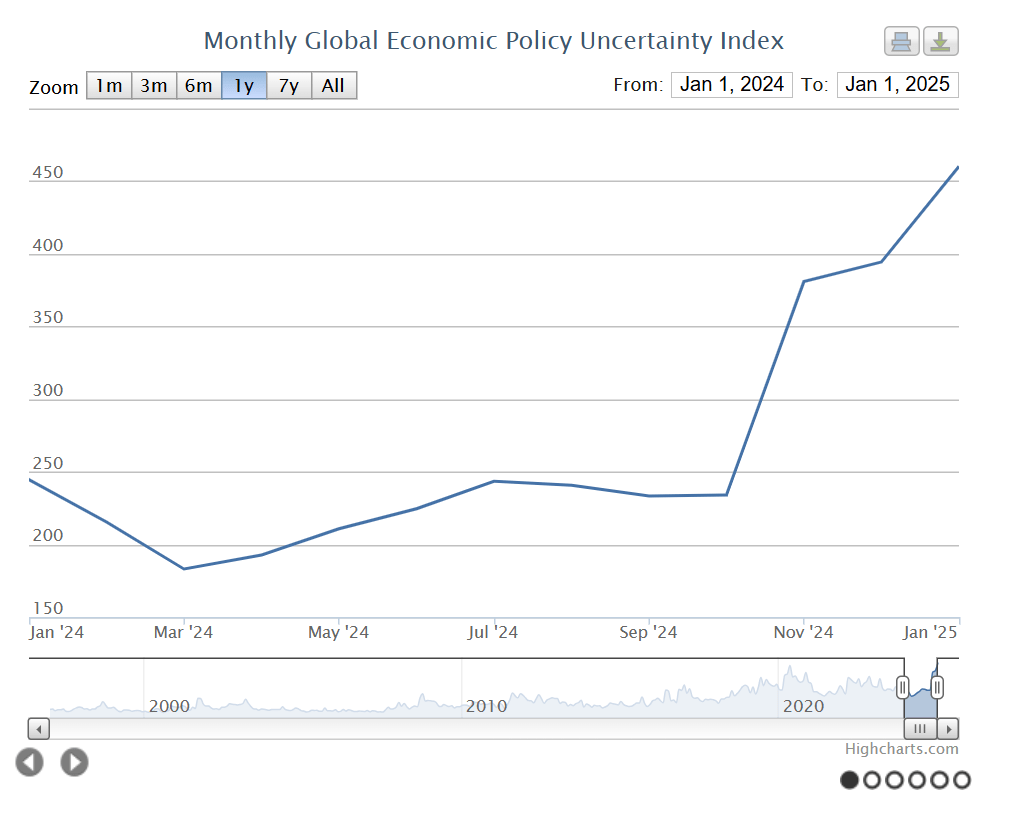

I was on a panel of economists last night at an event titled “The Economic Consequences of President Trump”. We each gave a 5-minute summary from our area of expertise and then opened up the floor for questions. This is a truncated summary of my talk. Since the panel included an investor, two industry economists, and another macro economist, I wanted to discuss something that was distinct from their topics. I’ve published a paper and refereed many articles concerning economic policy uncertainty (EPU) and asset volatility. I wanted to look at the data concerning President Trump – especially in contrast to Presidents Obama and Biden.

EPU matters because uncertainty can cause firms and individuals to delay investment and hiring decisions. Greater uncertainty can also cause divergent views concerning forecasted firm profitability. The result is that asset prices tend to become more volatile when EPU rises. One difficulty is that uncertainty occurs in our heads and concerns our beliefs, making it hard to measure. We try to get at it by measuring how often news media articles include the terms related to uncertainty, policy, and the economy. Since news content tends to report what is interesting, relevant, or salient to customers, there’s good reason to think that the EPU index is a decent proxy.

Using the Obama years as a baseline, the figure below simply charts out EPU. It was relatively low during Trump’s first term and then it was higher during Biden’s term – even after accounting for the Covid spike. The sharp increase toward the end is after Trump won the 2024 election. The EPU series conflicts with my perception of social media and media generally. My experience was that the media was far more attentive to the uncertainty that Trump caused. But, it may just be that the media outlets had plenty to report on rather than it being particularly indicative of EPU. After all, if the president exercises his power, then there is a certain swift decisiveness to it.

But if we look at a couple of particular policy areas, Trump’s administration faired worse. Specifically, Trump caused a ruckus concerning trade policy and immigration. Remember when Biden continued the aggressive trade policy that Trump had adopted? That’s consistent with lower EPU. Similarly, Biden made the immigration process much easier and faster while Trump’s deportation haranguing results in a somewhat stochastic means by which people are deported. Again, that spike at the end is after Trump won the 2024 election.

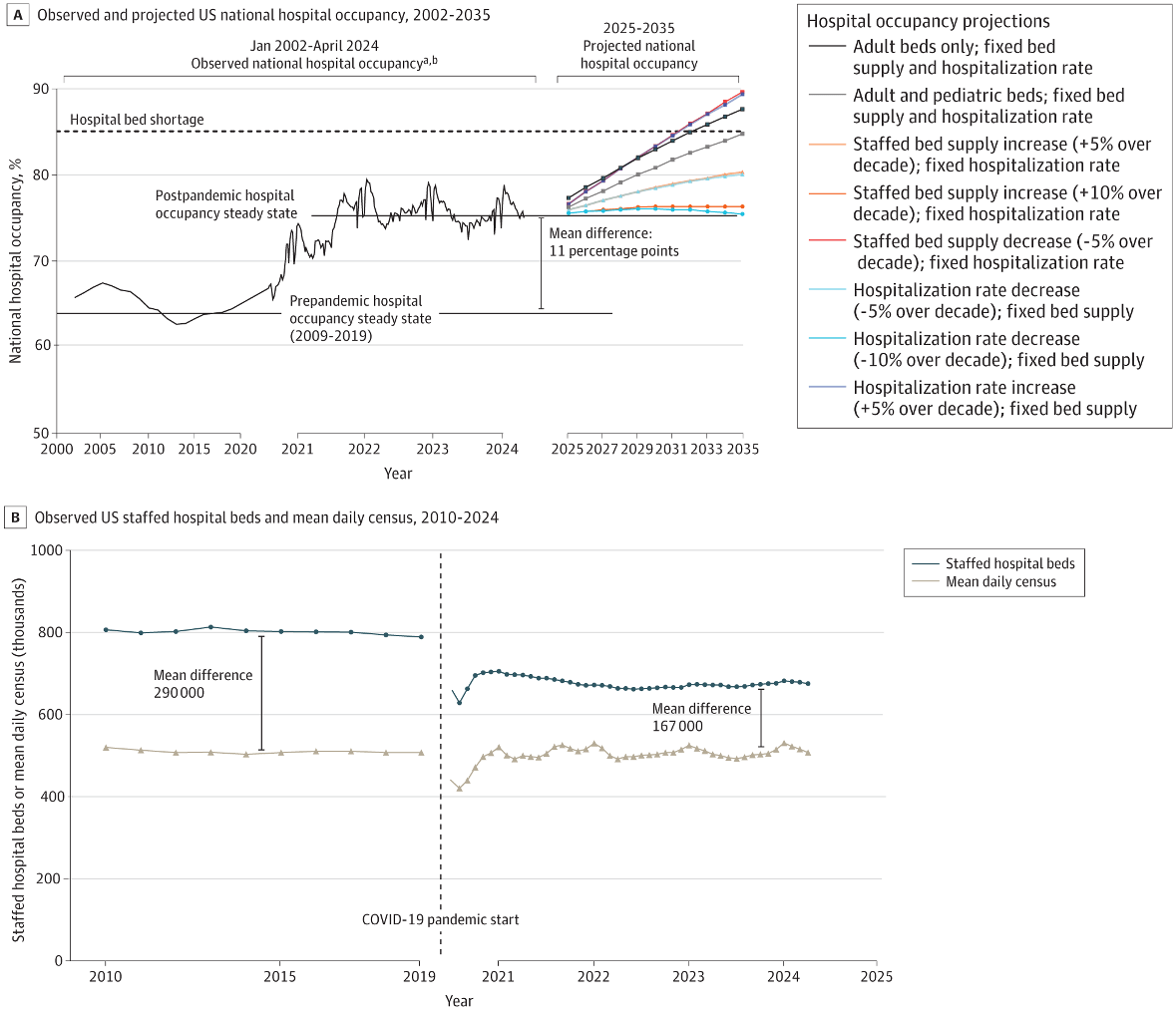

The average hospital is now 3/4 full- more full than during much of the worst of the Covid pandemic, and well above the 2/3 occupancy rate that prevailed during the 2010s. This is according to a study out yesterday in JAMA Open:

This seems to be due to a reduction in bed supply, rather than an increase in demand:

The number of staffed hospital beds declined from a prepandemic steady state of 802 000 (2009-2019 mean) to a post-PHE steady state of 674 000, whereas the mean daily census steady state remained at approximately 510 000

To me this is one more reason to reform Certificate of Need laws that put barriers in the way of hospitals opening or adding beds. Luckily I see a lot of momentum for CON reform this legislative season, including the highest-occupancy state, Rhode Island:

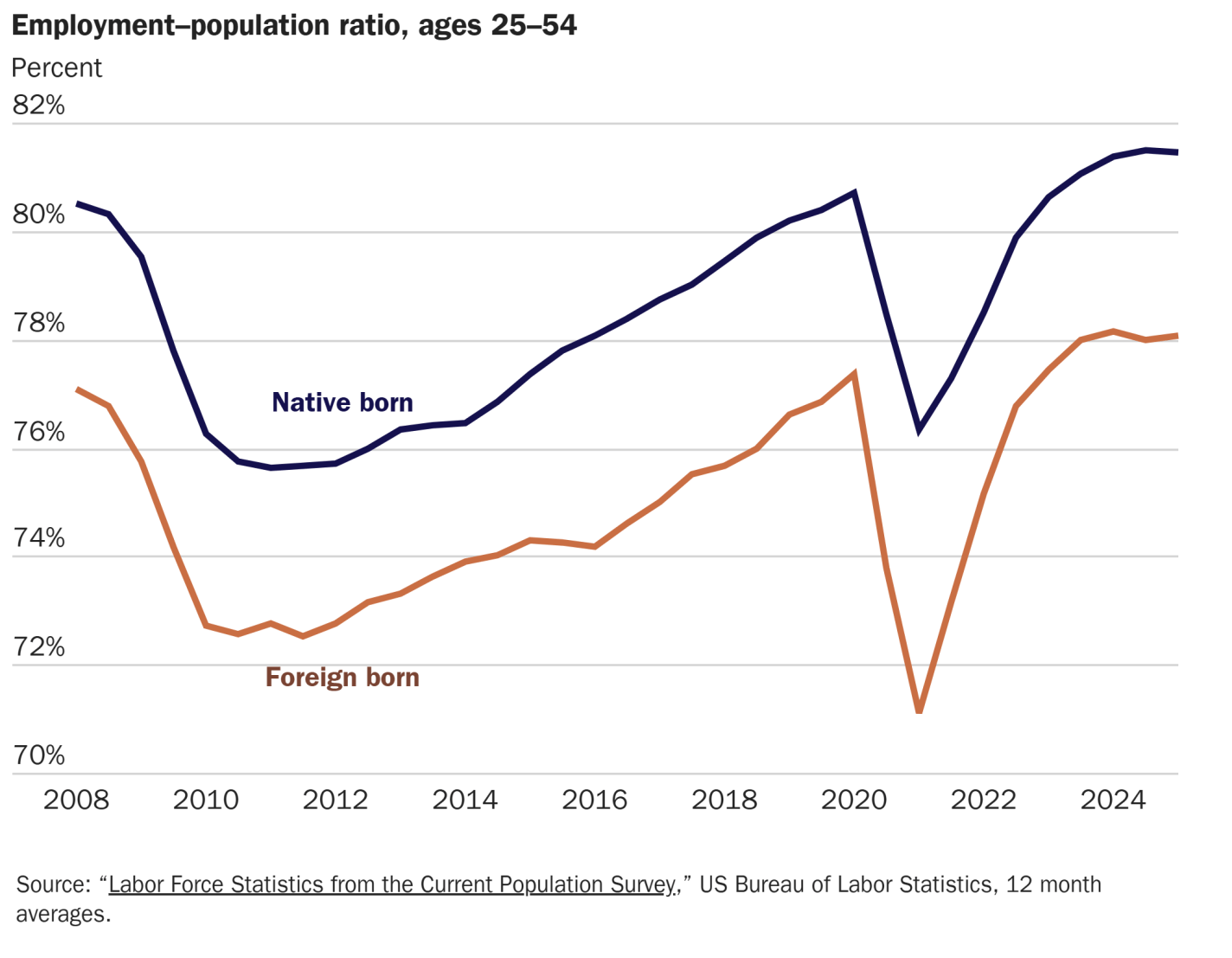

Are foreigners taking the jobs of native-born Americans? The fear that foreigners are displacing domestic workers has long been feared, and remains one of the major economic objections to immigration. And recently there seems to be some evidence this is happening in the US, with almost all net job creation in the US in the past 5 years going to foreigners, while native-born employment has been flat.

But this is not evidence that foreigners are taking our jobs, as I explain in my latest piece for the Cato Institute. The reason is simple: the native-born, working-age population hasn’t been growing. If we looking at the employment-rate of native-born Americans, it is higher than it has ever been, and higher than for the foreign-born population:

Last week I visited a family member in Saint Petersburg, Florida. We had a very nice time, walking around the pier area of the city and going out on his boat. Every day was the same weather: sunny, and a high of 80° F (in mid-February).

I was out walking in the neighborhood, and I saw signage for a shop that piqued my curiosity. It offered cannabis products, which I knew about, but also “kava” and “kratom”, and apparently “nitro”. When I came back to the house, I asked my host what kava was. He indicated it was some kind of recreational drug, whose use seemed to be expanding, at least in that area. I did a superficial check online, finding that kava is an extract from the roots of a plant native to some South Pacific islands, which is reputed to have anxiety-reducing and other feel-good properties.

A couple of days later I walked into the shop and introduced myself as an out-of-state tourist, who saw the sign out front and was curious. There were no other customers at the time, so the saleswoman patiently graciously answered my questions.

I started off asking about kava. But she indicated there was actually more interest in kratom. That is what she imbibes herself, although not frequently. Kratom is extracted from the leaves of an evergreen, Mitragyna speciosa, which is native to Southeast Asia. It seems to have stronger effects than kava, and a physician I spoke with felt that kratom was more likely to be addictive. (I plan to do a deeper dive into the pharmacology of kava and kratom in later articles on this blog).

I was told that kratom comes in three main types: red, green, and white. These are extracted at different stages of leaf maturity. Red is for pain relief, white is for energy, and green is in between. “Train wreck” has all three colors. The products in the shop with kratom, or kratom plus kava greatly outnumbered those with kava alone.

For pure kava, I would have to buy a can of soda (photo below) or buy a prepared drink at the bar.

While we were there, a customer came and ordered two drinks from the bar. He was a middle-aged, upstanding citizen, not some alienated youth covered in tattoos and body-piercings. He told us he has been using kratom for two weeks now, and it has helped him considerably. He said he suffers pain from arthritis and from operations, and that his alcohol use has gone way down since he started kratom. Normally, this man uses white kratom, but since the bar was out of the white extract, he walked out with two large cups of “train wreck”.

The shop also sells various cannabis related products. They mainly contain THCA, which is a legal and less potent version of THC, which is the most active ingredient in marijuana.

The sign out front offered mushrooms as well; I am not sure how “magic” they are. As for “nitro”, it turns out that that is not another psychotropic drug. It is just cold-brewed coffee infused with nitrogen gas, to give a somewhat creamy emulsion. Just another way for Americans to spend $6.00 on a cup of coffee.

I thought about buying and trying some kava or kratom drink, for the sake of science, but at my age I figured I needed to keep all my brain cells. I recalled that decades ago it was emphatically stated that marijuana (unlike alcohol) was not harmful, but now we know better. So, I thanked the clerk and walked out empty-handed.

POST-SCRIPT: See my follow-up article on effects of kava and kratom. Kava seems fairly safe and pleasant, maybe on a par with weed, but kratom functions largely like an opioid and should probably be avoided. Also, based on my additional reading, the kava beverages depicted above are likely to be ineffective; the way to go is to fresh-squeeze ground-up kava root in water. This can be done by you, or for you at a kava bar.

How bad are things? You know, in terms of our democracy and economy crumbling under the great wheel of history as the current administration tries to waddle us into fascist kakistrocracy. Are they bad? Maybe! Or maybe things are mostly fine and all we have to cope with is fear-peddling journalists and neurotic academics hyperventilating through what promises to be a four-year panic attack.

Well, Tyler is looking for market indicators. Signs that the market is internalizing the possibility of deteriorating government and political institutions into prices. That’s a really tall order, even more so than what it might seem to those of us who tend to rely on prices to reveal collective wisdom and the best underlying forecast. Prices reflect the expected benefits and the opportunity cost of an asset or choice in question. Opportunity cost can be explained in a number of ways, but they all boil down to the best outside option. It’s always going to be trickier to expect convenient and obvious price indicators for risk that is inescapable, where there is little in the way of an outside option. If you want a good forecast for avian flu, poultry and egg prices work pretty well, reflecting culled supply, reduced demand from a fearful public that thinks carnitas is sufficiently tasty, and the moves made by speculators who think that things are (or are not) going to get worse. So what are the analogous prices for those speculating that the center will or will not continue to hold in the Great American Project?

If you believe that the Trump administration is, in fact, trying to backdoor in an authoritarian revolution while walling off the largest economy from the rest of the world into a protectionist backwater, all while undermining the global reserve currency, what exactly is the outside option? Where can the money go? The people? The ideas? There are no doubt answers to those questions, but while most of the developed world is struggling with protectionist and authoritarian fevers, all while many entertain the prospect of a Russian invader who is already actively attacking a democratic nation, a host of obvious answers don’t rush to mind.

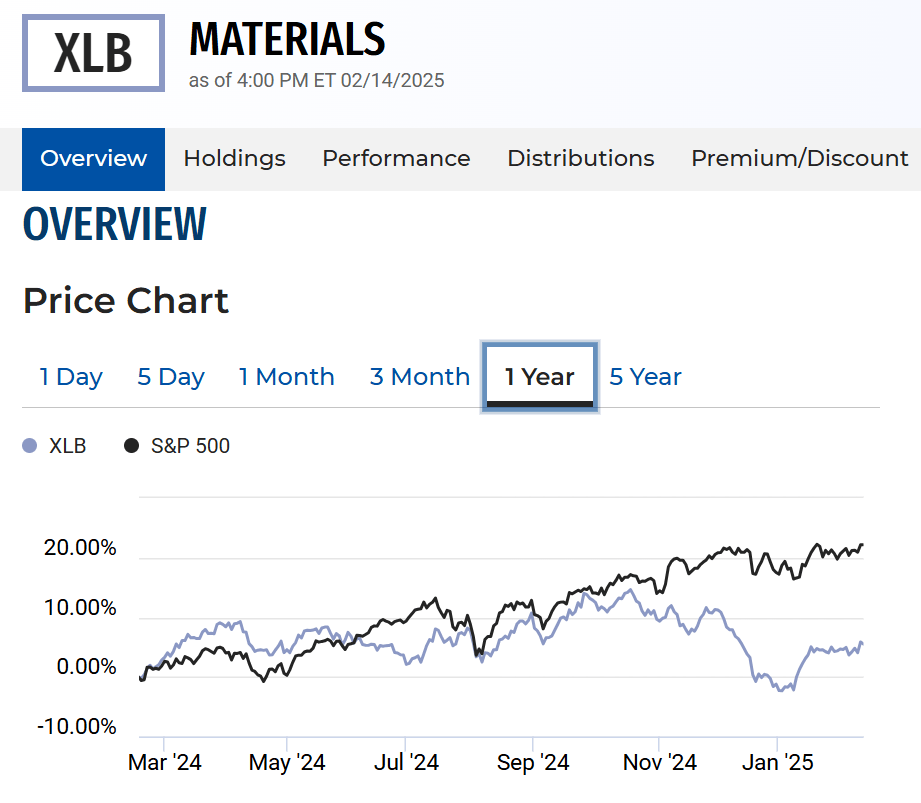

But let’s not punt entirely. Let’s get a little more micro. Is the market internalizing a more protectionist future for the US market and the global economy? Here’s the S&P 500 index for the “Materials” sector vs the entire S&P 500 over the last year:

Correlation is not causation, but the rapid drop off in the value of “chemicals, construction materials, containers and packaging, metals and mining, and paper and forest products” since what was effectively a coin-flip election is certainly convenient to the hypothesis that the market thinks materials previously circulating the global economy are not as likely to find their most valued uses under the Trump administration. If the market thinks we should take the threats of protectionism seriously, why shouldn’t we treat the administration’s threats to default on the debt similarly? Of weaponizing the DOJ against political opponents or ignoring court decisions? There’s not going to be a silver bullet composite price, but for each individual threat we should be looking for a relevant price.

If we are going to accept the hypothesis that any one single price indicator is going to be hard to identify, how about a forecasting index? The folks beind the Policy Uncertainty Index have a measure that reflects the language used in a large variety of publications combined with professional forecasters to reveal not what the future of policy is likely to be, but how much disagreement there is about it. Again quite the increase in the aftermath of a coin-flip election, which is odd because you would expect their to be more uncertainty before a coin-flip election, not afterwards. Shouldn’t we know what we are getting to a greater degree now what we know who is holding the office? I mean, assuming we actually know who is wielding power and influence within the office…

So there are some metrics that point towards a more isolationist future characterized by less predictable government institutions. That’s not nothing. We should be careful not to expect the markets to hand us a forecast on a silver platter, however. In both 1962 and 1983, it’s entirely possibe that nuclear war was averted by Stanislav Petrov and Vasily Arkhipov, who respectively refused to launch missiles and report (erroneously indicated) US missile launches, as dictated by Soviet protocol. As chaos is injected into the US government, including those tasked with overseeing the nuclear arsenal, we should perhaps look to the past. What were the prices that revealed how close we were to history-forking events? Did any price reflect the ebbs and flows in that underlying risk, the changing cultures within the Soviet military and the growing and shrinking prospects of nuclear war? Or did prices instead remain largely untouched by such tides of history? Not to get melodramatically apocalyptic, but perhaps prices cannot accurately reflect the prospect of a world without connection to the markets of today. So it goes. There’s some risk you simply can’t diversify, insure, or reallocate against.

Last week I had the honor of hosting Vernon Smith at Samford University and then being with him on his second day of the tour in Tuscaloosa, AL.

To introduce Vernon Smith’s new book about Adam Smith, I articulated a point that I had taken from reading Tyler Cowen’s GOAT book. Not all undergraduates have read Adam Smith, so I explained that Adam Smith was one of the first people to have a vision of a growing economy on a global scale. Afterward, I wondered if I had stated everything entirely correctly in my bold assertion. I went to consult with the source material via https://econgoat.ai/en/chat/gpt.

Joy: Does Tyler say that Adam Smith was one of the first people to imagine economic life on a globalized scale and how great the gains from trade could be?

EconGOAT GPT-4: Indeed, Tyler suggests that Adam Smith was one of the pioneering thinkers in envisioning economic life on a global scale and highlighting the immense gains from trade. In discussing Smith’s contributions, Tyler notes how Smith saw trade as a process by which nations could exchange their surplus or “superfluities” for goods they value more. While Smith didn’t quite articulate the theory of comparative advantage—later developed by Ricardo and Torrens—he was certainly heading in the right direction with his understanding of trade. This insight pointed towards a broader, more interconnected economic worldview that has since become central to economic theory (Chapter 8).

Tyler also gives Smith credit for recognizing issues with mercantilist views of trade, which often focused on stockpiling precious metals. Instead, Smith emphasized the expansion of consumption opportunities as the real benefit of trade, emphasizing its potential to enhance global prosperity. Smith’s multifaceted intellectual approach laid the groundwork for thinking about economies beyond just national borders, making him a key figure in the development of global economic thought.

Joy: When I think of a grand global vision prior to Smith, I think about religious leaders and military conquerors. Was Adam Smith the first to think of a grand global vision that fundamentally rests on individual freedom within a tolerant framework of laws and protections from harm?

EconGOAT GPT-4: Tyler acknowledges that Adam Smith played a pivotal role in developing the idea of economic globalization and the gains from trade. However, noting Smith as the absolute first might overlook other contributors. Before Smith, there were philosophers like the Scholastics and early mercantilists who considered economic ideas on a substantial, if not global, scale. The physiocrats, for example, were very much aware of how agriculture and trade could lead to prosperity for nations.

One could argue against Smith’s primacy by pointing out how people have always been aware of trade’s benefits, even if they didn’t articulate it quite as elegantly as Smith did. There’s historical evidence of trade routes as old as human civilization itself, such as the Silk Road or the trade networks of the Phoenicians. These early systems relied on a rudimentary understanding of economies of scale and specialization, even if they weren’t formalized.

Regarding your second point about religious leaders and conquerors, Smith’s vision indeed differs markedly. While others dreamt of unification through conquest or religious means, Smith’s framework empowered individuals to pursue their self-interest within a system of natural laws. This wasn’t just a vision of economic prosperity, but a moral and social vision as well. His “invisible hand” concept implies that individuals, left to their own devices within a safe legal framework, can contribute to the common good more efficiently than any central directive. This is highlighted in Chapter 8, where Tyler discusses Smith’s broader social and philosophical contributions. Smith’s ideas paved the way for modern market economies and significantly influence contemporary thought on economic freedom and globalization.

Joy: Would it be accurate to say that most people in Smith’s time had a very narrow view of the world, indeed hardly thinking beyond the borders of their own regions?

EconGOAT GPT-4: That’s a fair assessment. During Adam Smith’s time in the 18th century, most people indeed had a much narrower view of the world than we do today. Many individuals’ perspectives were limited to their immediate surroundings—villages, towns, or regions. The vastness of the globe, with its diverse cultures, economies, and possibilities for trade, wasn’t as accessible or imaginable to the everyday person as it is now.

Smith’s work in “The Wealth of Nations” was revolutionary in part because it broadened this horizon, not just for economists and policymakers but for anyone interested in economic activity. Smith’s ideas about the division of labor, specialization, and free markets opened up the concept of international trade as a means to prosperity beyond the local economy. His ability to foresee the potential for global interconnectedness in economies was ahead of his time.

I won’t excerpt our entire conversation. I eventually asked how to broaden one’s horizons.

EconGOAT GPT-4: While traveling Europe might seem like a grand adventure ripe for expanding one’s horizons (cue the “Eat, Pray, Love” montage), Adam Smith had reservations about the educational value of the “grand tour,” as it was then known. In Smith’s view, travel often led to “frivolous dissipation” rather than genuine intellectual or moral growth. Instead, he believed that real learning happened through competitive and commercial constraints—the kind you experience when you’re not just sightseeing but actively engaging with a community (Chapter 8).

That was when the bot made a genuinely funny joke about a silly modern book.

After raising rates in 2022 to belatedly combat inflation, the FOMC was feeling successful in 2024. They were holding the line and remaining steadfast while many people were getting all in a tizzy about pushing us into a recession. People had been predicting a recession since 2022, and the Fed kept the federal funds rate steady at 5.33% for an entire year. Repeatedly, in the first half of 2024, betting markets were upset that the Fed wasn’t budging. I had friends saying that the time to cut was in 2023 once they saw that Silicon Valley Bank failed. I remained sanguine that rates should not be cut.

I thought that rates should have been higher still given that the labor market was strong. But, I also didn’t think that was going to happen. My forecasts were that the Fed would continue to keep rates unchanged. At 5.33%, inflation would slowly fall and there was plenty of wiggle room for unemployment.

Then, we had a few months of lower inflation. It even went slightly negative in June 2024. Some people were starting to talk about overshooting and the impending recession. I documented my position in August of 2024. Two weeks later, Jerome Powell gave a victory lap of a speech. He said that “The time has come for policy to adjust”. Instead of discerning whether the FOMC would cut rates, the betting markets switched to specifying whether the cut would be 0.25% or 0.5%. The Fed chose the latter, followed by two more cuts by the end of the year.

I was wrong about the Fed’s policy response function. But why? Was the FOMC worried about the downward employment revisions? That was big news. Did they think that they had inflation whipped? I’m not sure. There was a lot of buzz about having stuck the soft landing. In late 2024, I leaned toward the theory that the Fed was concerned about employment. Like, they thought that we had been doing better until then.

The NSCH is the latest casualty of the new administration taking down major datasets from government websites. Between Archive.org and what I had downloaded for old projects, I was able to get all the 2016-2023 topical NSCH files and post them on an Open Science Foundation page.

I took this as a chance to improve the data- the government previously only made the topical Public Use Files available in SAS and Stata formats one year at a time, so I added a merged version for all available years in both Stata and Excel formats.

I hope and expect that the National Survey Children’s Health will be back up at official websites soon. But I expect that other datasets will be taken down permanently, so now is the time to download what you think you might need and add it to your data hoard– especially if you want anything from the Department of Education.