Three weeks I wrote a blog post about how economists define a recession. I pretty quickly brushed aside the “two consecutive quarters of declining GDP,” since this is not the definition that NBER uses. But since that post (and thanks to a similar blog post from the White House the day after mine), there has been an ongoing debate among economists on social media about how we define recessions. And some economists and others in the media have insisted that the “two quarters” rule is a useful rule of thumb that is often used in textbooks.

It is absolutely true that you can find this “two quarters” rule mentioned in some economics textbooks. Occasionally, it is even part of the definition of a recession. But to try and move this debate forward, I collected as many examples as I could find from recent introductory economics textbooks. I tried to stick with the most recent editions to see what current thinking on the topic is among textbook authors, though I will also say a little bit about a few older editions after showing the results of my search.

Undoubtedly, I have missed a few principles textbooks (there are a lot of them!) so if you have a recent edition that I didn’t include, please share it and I’ll update the post accordingly. I also tried to stick with textbooks published in the last decade, though I made an exception for Samuelson and Nordhaus (2010) since Samuelson is so important to the history of principles textbooks (and his definition has changed, which I’ll discuss below).

But here’s my data on the 17 recent principles textbooks that I’ve found so far (send me more if you have them!). Thanks to Ninos Malek for gathering many of these textbooks and to my Twitter followers for some pointers too.

In short, here is what I found: while some textbooks mention the “two quarters” rule, the majority do not (9 out of 17). And among those that do mention it about three call it a “rule of thumb” rather than it being how we define recessions (some even say it’s not a good rule of thumb!). Just five of the 17 use it as a definition (one of these calls it a “working definition,” another also references NBER definition). Most definitions are much closer to how the NBER defines recessions using multiple other measures to define a recession, with many even referencing the NBER as the agency that defines recessions. For example, about half of the textbooks put something about employment declining and/or unemployment increasing in their definition.

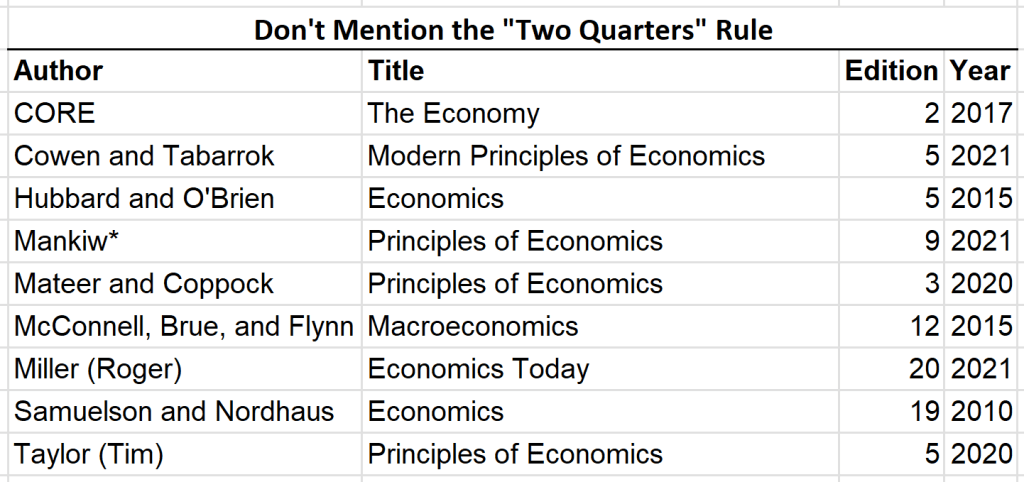

Here’s the list of textbooks that don’t mention the two quarters rule of thumb.

I put a star after Mankiw, since he does mention the two quarters rule of thumb, with two caveats. First, it’s not in the chapter where he defines and discusses recession; it’s in another chapter where he is discussing the GDP Deflator and other measures of inflation. Second, he says it’s not really a good rule of thumb: “There is no ironclad rule for when the official business cycle dating committee will declare that a recession has occurred, but an old rule of thumb is two consecutive quarters of falling real GDP.” (It’s also in parentheses in the text.)

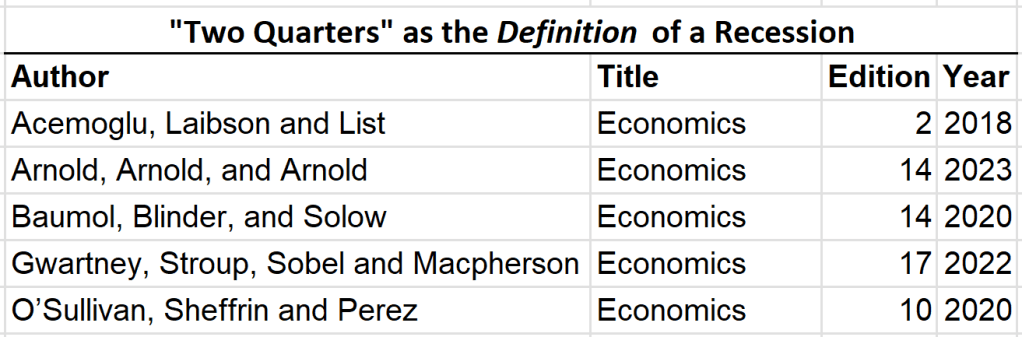

Next, here is the list of textbooks which include the “two quarters rule” as part of the definition of a recession.

I could put a few asterisks on this list too. For example, Baumol doesn’t mention this rule in Chapter 2 where they define a recession (“a period of time during which production falls and people lose jobs”). It does come up later in Chapter 21: “it has become conventional to say that a recession occurs when real GDP declines for two or more consecutive quarters” and “working definition of a recession as a period in which real GDP declines.” So they say it’s a “convention” and “working definition.” I won’t quibble too much, and I’ll count it in this list, but it’s not as clearly a hard definition as found in, say, the Arnold textbook.

In Arnold, they clearly stress that two quarters of GDP decline is the “standard definition.” They do mention and quote the NBER definition as well, but also add “the NBER definition is therefore different from the standard definition of a recession.” The Arnold textbook takes a clear position that I’ve seen a few other economists taking lately (“NBER is fine, but it’s not the standard definition”), though it’s really the only book to do so in exactly this way. I’ll also say a little more about an older edition of Arnold below.

Finally, here is the list of textbooks that say two quarters of decline is a “rule of thumb.”

The Frank textbook is interesting because they call the “two quarters rule” an “informal definition of a recession, often cited by reporters” which they say is “not a bad rule of thumb.” But they are clear that it’s not their definition, which is “a period in which the economy is growing at a rate significantly below normal.” Theirs is actually a broader definition than many textbooks use, since it would include some positive but low rates of growth. They also devote a bit of time (over half a page) to discussing the NBER Dating Committee and the measures that they use to define a recession.

Older Editions of Textbooks

I have been trying to collect some older editions of these textbooks too, because I have a theory: many textbooks probably changed their definition away from the two quarters rule in the wake of the 2001 recession, which did not have two quarters of consecutive GDP decline (it had two non-consecutive quarters). The NBER calls 2001 a recession year, as do (I assume) most economists looking at the situation. It probably would have been a bit awkward teaching the “two quarters” definition to college freshmen in the 2000s when really the only recession in their lifetime didn’t meet this definition.

In other words, connecting my theory to current political debates about the definition of a recession, it was not the Biden administration that changed the definition of recessions in 2022. It might have been economists themselves in the 2000s!

I’ve only found a few older editions that can test my theory so far, but they suggest I may be on to something. For example, the Arnold textbook discussed above is clear that “two quarters of GDP decline” is the rule. However, in the 7th edition published in 2005, they do add a line saying that in 2001 according to the NBER “the U.S. economy was in a recession even though Real GDP had not declined for two consecutive quarters.” They don’t change their own definition, but this feels like an admission the rule isn’t perfect (at some point in later editions discussion of the 2001 recession was dropped).

Most interesting though is older editions of Samuelson, which for years was the dominant textbook in the US and really set the standard for later textbooks. Phil Magness has done a good job digging up old editions of Samuelson, and here’s what he found. Samuelson first defines a recession in 1961 as “a moderate dip in the economy lasting about a year or more in length,” and this is relegated to a footnote. By the 1980s, recession is defined in the glossary of Samuelson using the now famous rule of thumb: “downturn in real GNP for two or more successive quarters.” By the 1998 edition it’s in the text as “a period in which real GDP declines for at least two consecutive quarters” (this is the one definition Phil cites in his recent Wall Street Journal op-ed).

However, in the most recent edition (and apparently final edition, with Samuelson’s death in 2009) the definition is now “a period of significant decline in total output, income, and employment, usually lasting from 6 months to a year and marked by widespread contractions in many sectors of the economy.” The “6 months to a year” part sounds similar to the old “two quarters rule,” but they say “usually,” and they define it in terms of a broader array of indicators (output, income, and employment) similar to the NBER (though no mention of the NBER). I’m not sure when the change occurred between 1998 and 2010 (there were two intervening editions, the 17th and 18th, that I don’t have access to at the moment), but there is a clear shift at some point after the 2001 recession to a more holistic and general definition of a recession.

Is It All Semantics?

Finally, are we being too pedantic in trying to figure out “the” definition of a recession? As is clear from my survey of recent introductory economics textbooks, there is no single definition. Some indeed use “two quarters of GDP decline,” though it’s a minority that use this as part of the definition itself.

I think we should care about the definition. Here’s why: recessions are serious business. They are serious because they are characterized by many bad things, but the primary common bad things are business failures and job losses (clearly these are connected). We want to know if a recession is coming! That’s why we follow the data, and that’s why we (both economists and policymakers) like to have a good definition of a recession.

The job losses part of this are key. As is well known, job losses always happen in a recession, but they are a lagging indicator. Job losses don’t happen immediately. NBER even includes a chart of the unemployment rate on their page about business cycles, despite the fact that they don’t use the unemployment rate as a measure of recessions. Why? Because that’s the bad thing we’d like to avoid if possible! Perhaps it’s too late in many cases to avoid the job losses, but for a variety of reasons it’s good to know that they are coming.

So if job losses are the lagging indicator, what are the leading indicators? For this, please read again my post from three weeks ago on the NBER definition of recessions. Those six measures start declining several months in advance of when the unemployment rate starts declining. That’s why we watch those measures (and have built models to predict the probability of a recession based on these measures).

Following real GDP declines is not really useful in real time (the lag in data availability is longer than the other measures), and it’s also not always predictive. In 2001, as previously mentioned, there weren’t two consecutive quarters of GDP decline. In the 1973-75 recession, there were eventually two consecutive quarters of GDP decline in the second half of 1974, but the job losses began in the first half of 1974. Watching GDP wasn’t helpful in 1973-75. But you know what was? Watching the other indicators, such as employment (not unemployment), real income, and industrial production provides a better prediction (and in that recession, employment was also a lagging indicator, which is why it’s useful to look at a broad set of measures).

So, the definition of a recession is simply a proxy for job losses, business failures, and other “bad things” that are correlated anyway? It’s basically like a traffic light protocol except there’s only two states (red and green). Maybe economists need a yellow light or caution light?

LikeLike

Reblogged this on Utopia, you are standing in it!.

LikeLike