Most economists know that the CPI is overestimated and therefore prefer the PCE price index. However, monthly CPI data is consistently released before PCE data for a given month. One would think that they move in the same direction and be highly correlated. Indeed, in the past five years, the correlation is 0.96. Therefore, it stands to reason that the there is less new relevant information on the PCE release dates than on the CPI release dates. Yes, CPI is biased, but it still contains some information about prices and it is known well prior to the more accurate PCE numbers.

Supply and Demand react to new information. Sometimes the new information changes our expectations about the future, and other times we learn that our beliefs about goods and assets were previously not quite right. So, with new relevant information comes new prices as people update their beliefs and expectations.

Let’s get financial.

The S&P500 is an index of assets. If the rate of inflation is important for the supply and demand of the constituent stocks that compose the index, then we should expect news with more information to change the prices by more than news with less information. Of course, the news may be no news at all. It’s possible that people already have a good idea of the underlying information prior to news reaching media outlets. If the CPI and PCE price index contain any information that the market doesn’t already have, then we should expect greater asset price changes on the CPI release dates than on the PCE release dates.*

The difficulty with measuring price changes is that any news can cause asset prices to either rise or fall. What matters is how the news compared to the expected news. And, we can’t quite observe that expectation (though there are some fun ways that economists try). Therefore, we have no reason to expect asset price to either rise or fall given any particular news release about inflation.

GARCH

Luckily, the sub-field of time-series statistics gives us a tool that can measure price changes while also being agnostic about the direction of change. Specifically, we can use the Generalized-Autoregressive-Conditional-Heteroskedasticity model – or just GARCH for short – to measure whether price changes more on CPI versus PCE release dates. This is not usually the domain of economics. Typically, we might go to FRED and observe one series or another during the period that they describe. But here, we are not interested in the actual rate of inflation that is announced and how it coincided with other variables during the same time period. Rather, we are interested in how the information regarding inflation affected beliefs about the world.

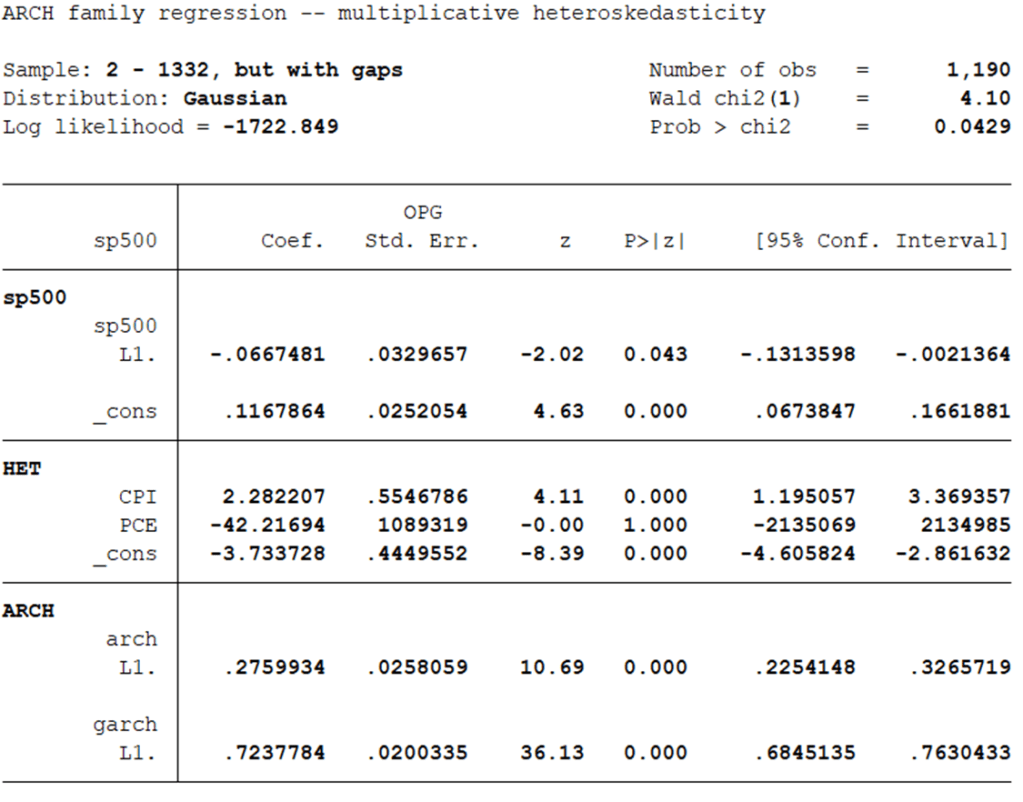

I won’t bore your with the details, but the bottom line is that we can specify variables that we think cause volatility (interested folks can read page 13 of the stata entry for model specific info). Using an indicator variable for release dates, we should observe a more positive coefficient for CPI releases and a smaller coefficient for PCE releases when we try to model daily S&P returns. Below are the results for the past 5 years of data.

Wait, how do we interpret the above? The sp500 heading gives us information about the mean. The ARCH heading gives us information about the component of the variance that is serially correlated. The part that we care about is the HET heading. If CPI contains more new information, then we should observe a more positive coefficient. Dang! How about them apples? Isn’t that nice? The data implies that CPI release dates cause price changes and that PCE release dates are not significant. The data seems to comport nicely with the logic. Almost like economists have a reasonable way of thinking about the world.

Beautiful.

This post is quite late because I spent this week grading final papers, projects, presentations, and exams. Time has been scarce. Students sometimes think that I’m overly pedantic with my expectations for clarity. But there is a reason. Sound and specific logic describes the world because the world is a logical place of cause and effect. Students will often skip one or more steps in their exposition of an idea and leave me wondering whether they actually ‘get it’. This post is no joke. Believe it or not, running the regression and writing this paragraph were the last things that I did. I described the results before I even saw them. I’m not a genius. I’m just a big believer in the power of applied logic.

*Of course, the PCE release dates also include other information about nominal and real spending. So, the PCE release is not entirely redundant.