I expected the meetings would shrink, but I was still surprised by how much they did:

That said, I mostly didn’t notice the smaller numbers on the ground, because most of the missing people are those on the job market, who used to spend most of their time shut away doing interviews anyway. There was still a huge variety of sessions and most seemed well-attended. ASSAs is also still unparalleled for pulling in top names to give talks; I got to talk to Nobel laureate Roger Myerson at a reception. But there may be a trend of the big names being more likely to stay remote:

The big problem with attendance falling to 6k is that they’ve planned years worth of meetings with the assumption of 12k+ attendance. Getting one year further from Covid and dropping mask and vaccine mandates might help some, but the core issue is that 1st-round job interviews have gone remote and aren’t coming back. The best solution I can think of is raising the acceptance rate for papers, which in recent history has been well under 20%.

In terms of the actual economic research, two sessions stood out to me:

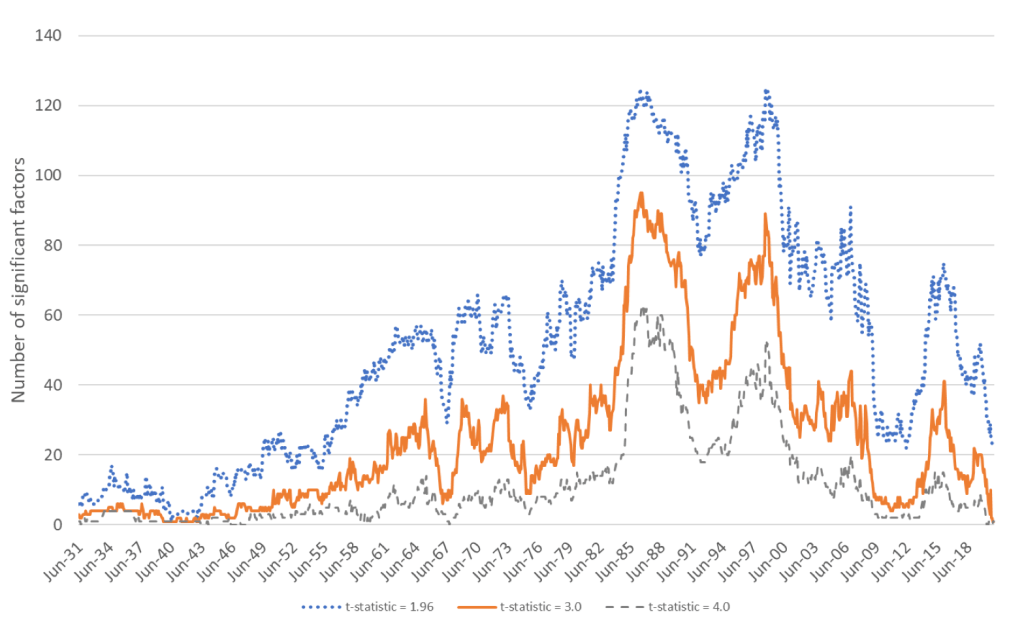

How many factors are there in the stock market? Classic work by Fama and French argues for 3 (size, value, and market risk), but the finance literature as a whole has identified a “zoo” of over 500. Two papers presented one after the other at ASSA argued for two extremes. “Time Series Variation in the Factor Zoo” argues that the number of factors varies over time, but is quite high, typically over 20 and sometimes over 100:

In contrast, “Three Common Factors” argues that there really are just 3 factors, though they are latent and not the same as the Fama-French 3 factors. In this case, the whole zoo of factors in the literature is mostly non-robust results driven by p-hacking and a desire to find more factors (fortune and fame potentially await those who do). Overall these asset pricing papers make me want to look into all this myself; when reading them I’m always struck by an odd mix of reactions- “I don’t understand that”, “why would you do it that way, it seems wrong and unnecessarily complicated”, and “why didn’t the field settle such a seemingly basic question decades ago?”.

Hayek: A Life this session covered the new book by Bruce Caldwell (who taught me much of what I know of the history of economic thought) and Hansjoerg Klausinger. Discussants Emily Skarbek and Stephen Durlauf agreed it is surprisingly readable for a long work of original scholarship, calling it a beautifully written 800p pageturner. Vernon Smith asked Caldwell if Hayek read the Theory of Moral Sentiments. Caldwell: “he cited it.” Smith: “but did he read it? Seems like he didn’t understand it very well.” Caldwell agreed he may not have, or if he did it was a German translation.

Vernon Smith’s own talk featured great comments on market instability: instability in markets comes from retrading. Markets are stable when consumers just value goods for their use, like haircuts and hamburgers. The craziness and potential for bubbles and crashes comes in when people are thinking about reselling something, whether it be tulips, stocks, houses, or crypto.

I asked Bruce Caldwell at a reception how he was able to finish writing such a big book that involved lots of archival work and original research. He said “one chapter at a time”, and noted that its fine to write the easiest chapters first to get the ball rolling.

Overall, while ASSA is diminished from the pre-Covid days and I often disagree with the AEAs decisions, its still a top-tier conference, especially when in New Orleans.

One thought on “Highlights from ASSA 2023”