A few weeks ago I wrote about several measures of the labor market, and whether the labor market was actually doing well. It’s a good idea to look beyond the headline unemployment rate, but even looking at alternative unemployment rates, labor force participation, employment rates, and unemployment insurance claims, I concluded in that post that the labor market is still looking healthy.

Lately I have heard another objection to the job growth numbers: part-time employment. I’ve seen this pop-up a few times on Twitter lately and just yesterday my co-blogger Scott Buchanan (in a post primarily about excess savings) stated that “much of the jobs creation this year has been in the part-time category.”

So is the jobs recovery mostly about part-time jobs? What is going on?

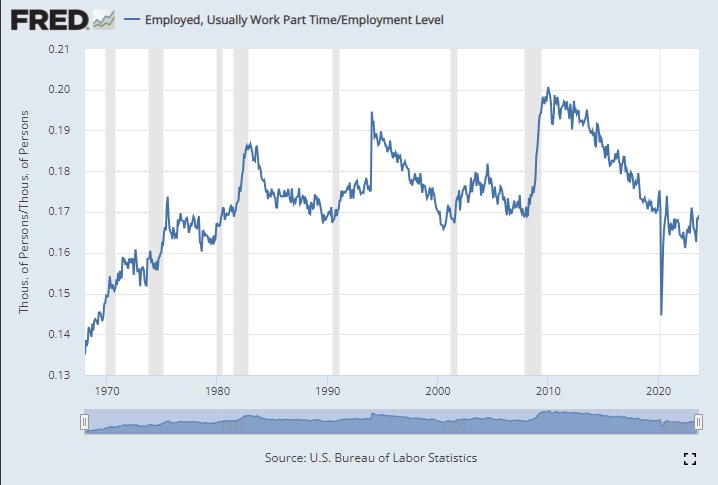

First things first: most of the data on part-time employment is from the household survey. There’s already a lot of noise in the household survey, due to the sample size, and part-time workers are a small share of the workforce, so expect it to be even noisier. In short, don’t trust one-month fluctuations too much. Furthermore, most of the data folks look at is seasonally adjusted. That’s generally good practice! But again, for a small number in a small sample, the seasonal adjustment factors won’t be perfect. Don’t read too much into one or a few months of data.

Let’s get the big picture first. How much of the labor force in the US is usually working part-time (defined in most data as less than 35 hours per week)? As usual FRED is the best place to go for graphing BLS data:

Well, the great “Recession Starting Next Quarter” that has been predicted for nearly two years is nowhere in sight. In fact, the Bureau of Labor Statistics just last week posted an absolute blowout jobs number:

The U.S. economy churned out a blockbuster 336,000 jobs in September, smashing economists’ expectations and heightening the risk that policymakers will have to push even harder to slow down the economy. The data released Friday by the Bureau of Labor Statistics offered yet another snapshot of the job market’s remarkable strength, with the unemployment rate holding at 3.8 percent and wage growth outpacing inflation in a boost to workers. But it was also the latest example of an economy that simply refuses to slow down, despite the Federal Reserve’s aggressive attempts to get prices and hiring closer to normal levels…The September report, which showed the largest number of gains since January, had been expected to indicate continued moderation in the labor market, with forecasts of around 170,000 jobs created. Instead, it came in at nearly twice that amount. (Lauren Kaori Gurley and Rachel Siegel , Washington Post)

Before we get too excited, let’s note that the BLS numbers have a strong component of BS: nearly every jobs number they put out is quickly, quietly revised downward by 20% or so. Also, much of the jobs creation this year has been in the part-time category (so employers don’t have to pay health benefits). That said, it is indisputable that despite ferocious interest rate hikes, the economy continues to hum along, much more robustly that nearly anyone predicted six or twelve months ago. Why?

I suggest that we follow the time-tested approach of investigative reporters, which is to follow the money. We have noted earlier that since 2020 a key factor in consumer spending, which constitutes about 70% of the economy, has been the ginormous windfall of free money, over $4 trillion, that was put into the economy via various pandemic-related programs (enhanced unemployment benefits, direct stimmie payments, etc.). The story of the recent strong jobs market is largely the story of spending down that windfall.

When we were locked down in late 2020-early 2021, we consoled ourselves with ordering tons of goods on Amazon. While this generated some jobs for longshoremen and UPS and Amazon drivers, it was mainly Chinese workers who benefited from this phase. But for the past year and a half, we are out there in planes, trains, automobiles, and cruise ships, spending for services and restaurant food at a brisk pace. This has buoyed up the domestic economy, which in turn is keeping inflation far above the Fed’s 2% target.

Part of the incoming-recession story has been that the COVID windfall money is about to run out. For instance, here is a June, 2023 chart from Fed authors de Soyres, et al. showing that in the U.S. (black curve below) this money has already been exhausted:

A different set of Fed authors (Abdelrahman and Oliveira of the San Francisco Fed) wrote, also in June, that there remained a smidge of excess savings, but that “would likely be depleted in the third quarter of 2023.”

However, the Bureau of Economic Analysis (BEA) recently completed an update of national economic data that lowered the savings rate prior to the pandemic and increased it in 2020 and 2021. This basically reflected a change in the way the BEA accounts for income from mutual funds and REITS. The bottom line is that it has forced Wall Street economists to increase their excess savings projections to date by as much as $600 billion to $1 trillion, depending on the economics team. This in turn leads them to delay forecasts of recession by yet another 6-12 months.

For instance, James Knightley of ING Global Markets Research writes that there are still plenty of excess savings around; recent revisions in their numbers show the remaining hoard is even larger than they originally thought:

They did not break down this excess saving by income group, so it is possible that much of it remains with the upper 10-20% who may hoard/invest it, versus the bottom quartiles who have been spending it all into economy and now may be tapped out. We shall see how this continues to play out.

Have you not gotten around to trying ChatGPT for yourself yet?

Ethan and Lilach Mollick have released a series of YouTube videos that encapsulate some current insights, aimed at beginners, posted on Aug. 1, 2023. It covers ChatGPT, Bing, and Bard. Everyday free users are using these tools.

Practical AI for Instructors and Students Part 2: Large Language Models (LLMs)

If you are already using ChatGPT, then this video will probably feel too slow. However, they do have some tips that amateurs could learn from even if they have already experimented. E. Mollick says of LLMs “they are not sentient,” but it might be helpful to treat them as if they are. He also recommends thinking of ChatGPT like an “intern” which is also how Mike formulated his suggestion back in April.

I used GPT-3.5 a few times this week for routine work tasks. I am not a heavy user, but if any of our readers are still on the fence, I’d encourage you to watch this video and give it a try. Be a “complement” to ChatGPT.

I’ll be posting new updates about my own ChatGPT research soon – the errors paper and also a new survey on trust in AI.

I hear regular complaints from my colleagues all over the country about poor attempts by college students to get GPT to do their course work. The experiment is being run.

It was only back in December 2023 that I did a live ChatGPT demonstration in class, and figured that I was giving my students there first ever look at LLMs. Today, I’d assume that all my students have tried it for themselves.

In my paper on who will train for tech jobs, I conclude that the labor supply of programmers would increase if more people enjoyed the work. LLMs might make tech jobs less tedious and therefore more fun. If labor supply shifts out, then quantity should increase and wages should fall – good news for innovative businesses.

I don’t like when celebrities are ‘caught’ saying deplorable things in a heated moment. Sometimes they say really awful things, specifically about observables such as race, weight, sex, nationality, odor, etc. Plenty of people have done it. I won’t mention the names or link to any particulars here.

My problem isn’t that I wish celebrities had better behavior – although I do. My problem is with the entire fallout of how we’re all supposed to take the celebrity seriously when they were enraged. When people get angry they say things that are designed to hurt others. People will say things that they don’t mean or wouldn’t normally say. And it’s not like they are betraying some unspoken belief that they’ve hidden. Angry people often say wicked things for the sole purpose of hurting someone else’s feelings. In the moment, the offender tries hard to communicate disrespect – not due to a lack of respect – but due to how it will make the other person feel.

I find the entire circumstance weird. If someone is boiling over and saying patently ridiculous things to me and calling me names, then I have a very hard time taking them seriously. All the same, context matters and words can hurt. It’s weird that we know that people can say untrue things in order to hurt us, and then it actually hurts us. Strange.

The last post where I attempted a macro prescription was in April 2022, when I said the Fed was still under-reacting to inflation. That turned out right; since then the Fed has raised rates a full 500 basis points (5 percentage points) to fight inflation. So I’ll try my luck again here.

Headline annual CPI inflation has fallen from its high of 9% at the peak last year to 3.7% today. Core PCE, the measure more closely watched by the Fed, is at a similar 3.9%. Way better than last year, but still well above the Fed’s target of 2%. Are these set to fall to 2% on the current policy path, or does the Fed still need to do more?

The Fed’s own projections suggest one more rate hike this year, followed by cuts next year. They expect inflation to remain a bit elevated next year (2.5%), and that it will take until 2026 to get all the way back to 2.0%. They expect steady GDP growth with no recession.

What do market-based indicators say? The yield curve is still inverted (usually a signal of recession), though long rates are rising rapidly. The TIPS spread suggests an average inflation rate of 2.18% of the next 5 years, indicating a belief the Fed will get inflation under control fairly quickly. Markets suggest the Fed might not raise rates any more this year, and that if they do it will only be once. All this suggests that the Fed is doing fine, and that a potential recession is a bigger worry than inflation.

Some of my other favorite indicators muddy this picture. The NGDP gap suggests things are running way too hot:

M2 shrank in the last month of data, but has mostly leveled off since May, whereas a year ago it seemed like it could be in for a major drop. I wonder if the Fed’s intervention to stop a banking crisis in the Spring caused this. Judging by the Fed’s balance sheet, their buying in March undid 6 months of tightening, and I think that underestimates its impact (banks will behave more aggressively knowing they could bring their long term Treasuries to the Fed at par, but for the most part they won’t have to actually take the Fed up on the offer).

The level of M2 is still well above its pre-Covid trend:

Before I started looking at all this data, I was getting worried about a recession. Financial markets are down, high rates might start causing more things to break, the UAW strike drags on, student loan repayments are starting, one government shutdown was averted but another one in November seems likely. After looking at the data though, I think inflation is still the bigger worry. People think that monetary policy is tight because interest rates have risen rapidly, but interest rates alone don’t tell you the stance of policy.

I’ll repeat the exercise with the Bernanke version of the Taylor Rule I did in April 2022. Back then, the Fed Funds rate was under 0.5% when the Taylor Rule suggested it should be at 9%- so policy was way too loose. Today, the Taylor Rule (using core PCE and the Fed’s estimate of the output gap) suggests:

3.9% + 0.5*(2.1%-1.8%) + 0.5%*(3.9%-2%) + 2% = 7%

This suggests the Fed is still over 1.5% below where they need to be. Much better than being 9% below like last April, but not good. The Taylor rule isn’t perfect- among other issues it is backward-looking- but it tends to be at least directionally right and I think that’s the case here. Monetary policy is still too easy. Fiscal policy is still way too easy. If current policy continues and we don’t get huge supply shocks, I think a mild “inflationary boom” is more likely than either stagflation or a deflationary recession.

Last weekend I had the opportunity to visit an arcade, but not one of those modern fancy arcades with virtual reality, laser tag, etc. This arcade specializes in having old-school games, primarily pinball, but also early video arcade games. You pay a cover charge ($5 for kids, $10 for adults), and then you use quarters to play the games. But here’s the cool part: the price of the games is the same as it was when the games were first released.

As an economist, of course, I was very interested in the prices.

They had pinball machines that dated back the 1960s, and video games from the late 1970s. Most video arcade games were around 50 cents for the early games (late 1970s and early 1980s). But the pinball machines started out at 25 cents, with the earliest game they had being a Bally Blue Ribbon machine, manufactured in 1965 (interestingly, some of the earlier machines had slots for both dimes and quarters — I assume the price was adjustable mechanically). Notably, you also got to play 5 balls for this price (3 balls seems to be standard later on).

How should we think about that 25 cents? A standard reaction is to adjust the number for inflation. Using the CPI-U as the inflation index, that means the 25 cents from 1965 is “worth” about $2.40 now. That’s interesting, but I don’t think it really provides the relevance that we want today.

An alternative is to calculate the “time price” of playing the game. Using the average hourly wage of $2.67 in December 1965, we can calculate that it would take about 5.5 minutes of work to pay for that game — a game which probably only lasts about 5.5 minutes, unless you are really good at it!

Another comparison we could do is with the cost of video games today compared with wages today. But that’s not really a fair comparison — video games are much more advanced today. We would need to do some sort of quality adjustment, which is overly complicated.

But, at least in my case, there is no need to do the quality adjustment — I can play the exact same game as 1965. In fact, I did (several times). There was also that $10 cover charge that I mentioned, and if I spread that fixed cost over 40 games, it cost me about 50 cents per play (including the 25 cents to start the machine) to play the 1965 Bally’s Blue Ribbon Pinball machine. At the average wage today of $29 per hour, it takes about 1 minute to afford a play of that same game. In other words, my Blue-Ribbon-Pinball standard of living is about 5.5 times greater than in 1965.

Now this isn’t to say we are 5.5 times better off overall than 1965. Prices don’t stay constant for most goods! But hopefully it is a useful way to think about that 25 cent price tag from the past, and how to compare it to today.

I have an oldish Honda that still runs smoothly. It is true that the cruise control does not work, and the left front fender is held on by a large binder clip, and I had to patch over a big rust hole in a rear wheel well, but as I said, it runs.

I sometimes park it down at the end of the street, under some shade trees, to get it out of the hot summer sun. A couple of times, for no reason, the antitheft system kicked on, so the car was honking and honking for hours on end because we didn’t hear it down there. Some neighbors down there finally figured out who it was and came and told us. They were nice about it, but I heard some other folks down there were pretty irritated.

That happened again two weeks ago, so I decided to keep it in front of our house all the time where we could keep an ear on it. Supposedly the alarm is triggered when the car thinks that a door or the trunk or the front hood has been opened without a legitimate unlocking by a key or a fob. Therefore, I opened and closed all four doors, and the trunk and the hood, and locked the car and hoped all will go well. But a few hours later there it was: honk, honk, honk….

As a temporary measure, I simply left it unlocked, so the system would not arm. But that’s not a long-term fix. So, I rolled up my sleeves and went to the internet to see what help I could find there. One common suggestion was to find the fuse that controls the alarm system and just pull it out of the fuse box. That would be great, but I checked multiple fuse diagrams for my model, and it does not seem to be a fuse that controls just the alarm system.

Other web sites mentioned that day sensor on the front hood latch is a common failure point. The sensor there can start giving spurious signals when it gets old. If you are sure that’s the problem, you can have a garage replace it for labor plus maybe 100 bucks for the replacement latch.

Alternatively, you can just pull apart the connector that connects the hood latch sensor to the alarm system. That connection is in plain sight near the latch. If the latch is the problem, disconnecting that sensor should make the alarm system think the latch is always firmly closed, so it will not trigger an armed system.

But what if the hood latch is not a problem? What if the problem is the common but elusive damage to wiring caused by rodents gnawing on the insulation which contains soybean derivatives?? After sifting through about 10 links that were thrown up by my DuckDuckGo search on the subject, I finally found a useful discussion on the “civicsforum.com”.

A certain “andrickjm” wrote that he had disconnected that wire junction, and his car alarm was still randomly going off. Some savant going by the moniker “ezone” wrote that what you needed to do then is to insert a little wire jumper between the two sockets of the connector that go to the alarm system. That will make the alarm system think the hood is always raised, never closed, and this will keep a system from ever arming.

So I cut a 1-inch piece of wire, stripped the insulation from the two ends, bent it into a U-shape, jammed the two bare wire ends into the two holes in the connector socket, and sealed it all up with duct tape.

The alarm has not sounded since. Victory at last, thanks to the distributed intelligence of the internet, resting on the efforts of millions of good-hearted souls who share their problems and solutions in all areas of life.

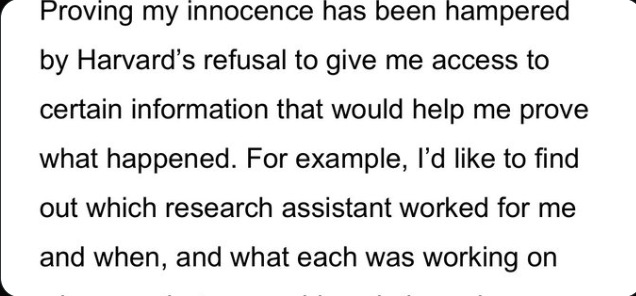

Francesca Gino has been acused of academic fraud. She claims she is innocent. I am not going to adjudicate here whether she committed fraud. What I am going to argue is that she and many other high volume researchers aren’t actually engaged in research. They are grant procurers, managers, high volume writers, globetrotting presenters. But they are not researchers because they are too far removed from the actual production of research. Now, to be clear, that doesn’t necessarily mean the world is worse off. Their comparative advantage may lie in everything from management to carnival barking, but there is a threshold, a degrees-too-far removed from the problem solving at which point you are you no longer a scholar. What that threshold is, I can’t say, but I would argue that if you can’t defend your work, investigate it’s own integrity, if you don’t know who your research assistants are or what they did, then you have likely crossed that thresold. From Gino’s (since updated) website:

We’ve all see the presentations or heard the stories of the leading scholar called on the carpet about something in their project or analysis, only to respond “I’m not sure. My RA did that.” Which is fine. But at some point that started to become assumed as characterizing whole researchers, whole agendas, whole fields. There are always going to be the prodigiously productive, but those people used to be one or two in a generation. Glorious anomalies. Universities are now littered with faculty with hundreds of publications, sometimes dozens in a single year, and we all know that it is physically impossible for them to conduct that work themselves. Gino received her PhD in 2004 and in the 19 years since has 460 (!!!) publications listed on google scholar. Some of those are probably duplicate listings, but it’s probably safe to say she has more than 20 publications per year for 20 years. It’s hard enough to imagine having energy enough to write and present that many papers even if they are produced entirely by others. This is not unique to Gino and thereis no doubting the prodigious work ethic in evidence within her and others. What is in question is whether the ever raising bar on output is lowering the quality of work done by the field as a whole. It’s a tax on us all if research concentrated within the labor of the most qualified, competent, and creative no longer produces an acceptable return to scale. Some people really are better managers of other people’s work, at some point the work has to be attributable to one or more people. Who is doing the work? Who is responsible for the work?

Maybe this isn’t really useful and I don’t feel like yelling at clouds for 5000 words. As I was saying…

But I’ll tell you this- truly great researchers work with other greater researchers, employ smart people, mentor promising RAs. And they know who they are and what they did. Because when you’re in the weeds trying to answer questions, its almost impossible not to know. That doesn’t mean mistakes won’t be made and errors overlooked. But when it comes time to audit your work, you’ll know where to start and what might have gone wrong. If you don’t know, well, maybe you’re lying, but maybe more likely you just weren’t around when the work was getting done. You were promoting your last project and getting your next grant. Because you’re not a researcher. At least not anymore.

You’re a manager, promoter, figurehead, pitchman, traveling roadshow. You’re likely useful and valuable. Publication and Grant, LLC.

But you’re not a scholar. And the institutions employing you aren’t producing scholarship. These faculty are following their incentives, and those incentives are at the moment treating research as a game to be played. Not science. Not the answering of questions. An expensive hustle to grind and empty race to win. They’re getting what they’re paying (and tenuring) for.

Joy: This post was written by my friend and fellow econ professor Cameron Hardwick.

One of my biggest ongoing teaching challenges is keeping students engaged during lectures.

Sure, there are ways to add interactivity here and there, but sometimes there’s just no way around an old-fashioned lecture.

There are a few ways of dealing with this, and I haven’t been satisfied with any.

It’s their grade, if they zone out that’s on them. In terms of the incentives, sure, the externalities are all internalized. But as a macroeconomist, I also know: if time-inconsistency problems are hard for policymakers, how much more for students! We shouldn’t be surprised when students do poorly if the main feedback they get from paying attention or not comes a week later with the homework grade.

Posing questions and waiting for answers. Either you get a minute of awkward silence, or you get the same two engaged students answering everything while everyone else keeps zoning out.

Cold calling. I started doing this a few years into teaching. The advantage is that it keeps students on their toes and paying attention. But a few problems left me unsatisfied:

“How about you in the red shirt”. Hard to catch a student’s attention that way, and in a class of 40 or more, learning names takes a good chunk of the semester.

I had no systematic way of keeping track of participation. Every semester I’d look at the roster and still have a few names I couldn’t put a face to.

Humans are really bad at making random choices! Much as I tried, I couldn’t guarantee I wasn’t biased toward or against (say) the corners of the room, or students whose names I knew.

LMS software. These can offer a lot of great student participation tools. But students have to pay for them – which isn’t worth it if you’re just looking for one feature. On top of that, then you’re locked into an ecosystem.

So, I made an app myself. It does one thing and does it well.

Pick.al (pronounced Pickle) picks students at random from a roster and keeps track of participation points. I can now pose a question in class, ask “what do you think…”, pull out my phone and hit a button, and have a name.

I can also record the quality of their answers:

✓: 1 point, good attempt! (Since this is for participation points, I record ✓ whether right or wrong, as long as they give it a good shot)

?: 0.5 points, if they ask “wait, what was the question?”

×: 0 points, if they’re not there or don’t respond at all.

There’s also a 1-5 scale option, for those who want a more fine-grained evaluation.

This has a lot of benefits in the classroom:

Since I can call on students by name, I learn names more quickly.

Pick.al chooses randomly from the pool of students who have been called on the least so far. So, I know my participation points are as fair as possible.

Students know they can get called on at any time, so they pay attention more in class, and then do better on the homeworks and tests.

Students appreciate being brought in more frequently. One noted on the evaluations the first semester I piloted it: “something specific I like is he got the class involved by calling people out which forced them to test their knowledge which is something teachers need to do more of.”

Using Pick.al is as simple as registering (with an email address or an OrcID), uploading a roster, and then hitting a button during class. You can also swipe through the history and edit or undo participation events, and go back in the admin interface and add, edit, and remove participation events after the fact if necessary.

Pick.al is secure and password-protected, and has a number of handy features:

You can set excused absences if a student lets you know beforehand, so their name doesn’t come up until a certain date.

You can select specific students from the roster in a sidebar, if you want to give credit to – say – a student who raises his hand unbidden.

If you’d like to use the classroom computer instead of pulling out a phone, you can use it with full keyboard navigation.

Scores can be downloaded as a CSV to be put in your own gradebook.

Private notes can be added to students to show up when their names are selected, e.g. “sits in the back corner”

If you use it and find a bug or have an idea that would make it more useful to you, feel free to let me know. It’s been a great tool in my own classes, and I hope it’ll be useful for other teachers to keep students engaged too.

It’s been almost a decade since I taught principles of economics classes. One major allocation of my time this semester is course prep, since I am teaching 3 different classes.

For my Principles of Microeconomics course, I chose Modern Principles of Economics, because I figured Tyler and Alex had done a good job and I have heard good reviews from others.

I’m writing a short review of their instructor resources, and then I’ll have to get back to course prep.

Like most textbooks, they provide you with slides that you can modify. Not having to start from scratch on lecture slides is great.

They also have teacher guides for each chapter. I find these helpful, because I have not taught this class in many years. Even though “I’m an economist,” there is still a technique to presenting these ideas for the first time to undergraduates. No need to re-invent that wheel completely.

They have suggestions for in-class activities. For example, to illustrate demand shifts, ask the students about a recent celebrity scandal and how that created a fall in the demand for concert tickets. It works. Everyone loves talking about celebrity scandals. It will be an evergreen idea. There are always new scandals for each semester – the students know more about it than the professors. My students (Fall 2023) informed me that Lizzo got in hot water for fat-shaming.

Their online learning platform called Achieve within MacMillan works well. It integrates really well with Canvas, our LMS. One warning I would give you is to make sure that students buy Achieve through an account on their .edu email address. I have headaches over students signing up with a personal email address and then not having their data integrate with Canvas.

You can sign up for EconInbox, which will email you topical relevant news stories right before you would want to present them in class. You’ll have to tell them ahead of time what your schedule of topics is, but that is something you ought to have worked out in your syllabus at the beginning of the semester. Obviously, you can’t cover every chapter in one semester. There are far more resources, generally, than you can use. But picking and choosing from a great library is easier than trying to build something from scratch yourself.

Lastly, the Cowen Tabarrok textbook integrates nicely with the free Marginal Revolution University video library. MRU is free to all. So, as an instructor you could still use it heavily even if you are not assigning their textbook or even if you are not doing Achieve. Still, I think that making use of the MRU resource is easiest if you are using their textbook. A fun video that might even be worth using class time for is Avengers: The Story of Globalization