If you didn’t know, China has had negative population growth for the past 4 years. Japan has had negative population growth for the past 15 years. The public and economists both have some decent intuition that a falling population makes falling total output more likely. Economists, however, maintain that income per capita is not so certain to fall. After all, both the numerator and denominator of GDP per capita can fall such that the net effect on the entire ratio is a wash or even increase. In fact, aggregate real output can still continue to grow *if* labor productivity rises faster than the rate of employment decline.

But this is a big if. After all, some of the thrust of endogenous growth theory emphasizes that population growth corresponds to more human brains, which results in more innovation when those brains engage with economic problems. Therefore, in the long run, smaller populations innovate more slowly than larger populations. Furthermore, given that information can cross borders relatively easily no one on the globe is insulated from the effects of lower global population. Because information crosses borders relatively well, the brains-to-riches model doesn’t tell us who will innovate more or experience greater productivity growth.

What follows is not the only answer. There are certainly multiple. For example, recent Nobel Prize winner Joel Mokyr says that both basic science *and* knowledge about applications must grow together. That’s not the route that I’ll elaborate.

I’m writing because I am catching up on the backlog of The Answer is Transaction Costs (TAITC), a podcast hosted by Michael Munger. Specifically, in an episode published August 27, 2024, a listener writes asking about what seems to be the extremely costly practice of interviewing college applicants prior to acceptance.

As it turns out, I work at a private university that enacted an interview policy in a quasi-random way and the university president gave me permission to share.

Initially, my university did not interview standard applicants. Our aid packages were poorly designed because applicants tend to look similar on paper. There was a pooling equilibrium at the application stage. As a result, we accepted a high proportion and offered some generous aid packages to students who were not good mission fits and we neglected some who were. Aid packages are scarce resources, and we didn’t have enough information to economize on them well.

The situation was impossible for the admissions team. The amount of aid that they could award was endogenous to the number of applicant deposits because student attendance drives revenue. But, the deposits were endogenous to the aid packages offered! There was a separating equilibrium where some good students attended along with some students who were a poor fit and were over-awarded aid. The latter attended one or two semesters before departing the university, harming retention and revenues. Great but under-awarded students tended not to attend our university. Student morale was also low due to poor fits and their friends leaving.

Have you ever looked up and wondered where the time went? One moment you’re living your life, and the next moment you realize that you’ve just lost time that you’ll never get back? That’s what happened to Japan’s economy at the turn of the century in an episode that’s known as ‘the lost decades’. It was a period of slow or null economic growth. Economists differ with their explanations. One cause was the prevalence of ‘zombie firms’.

Japan’s Economy

Japan had a current account surplus from 1980-2020, which means that they had more savings than they effectively utilized domestically. Metaphorically, they were so full of savings that they exhausted productive domestic investment opportunities and their savings spilled out into other counties in the form of foreign investments. This was driven by high household savings and slow growth in domestic investment demand. The result was the Japanese firms had easy access to credit. Maybe a little too easy…

Private corporate debt ballooned throughout the 1980s. That’s not intrinsically a problem. In the 1990s, households began saving somewhat less, and most firms began to drastically deleverage… But not all firms. The net effect of the mass deleveraging was that interest rates fell. The firms that remained in debt were the ones that risked insolvency. Less productive firms had slim profits and their Earnings Before Interest, Taxes, Depreciation, and amortization (EBITDA) was slim. So slim, that they couldn’t pay their debts. Faced with the prospect of insolvency, firms did what was sensible. They refinanced at the lower interest rates. Firms went to their banks and to bond markets and rolled over their debt, which they couldn’t afford, and replaced it with debt that had a lower interest rate. This occurred across industries, but especially in non-tradable goods and services that were insulated from international competition. Crisis averted.

Except this process of refinancing, while avoiding acute defaults and a potential financial crises, ensured that the less productive firms would survive. Not exactly failing and not exactly thriving, they could sort of just hold on to something that looks like life. Well, high debt and low profits aren’t much of a life for a firm. It’s more like being undead – like a zombie. Between 1991 and 1996, the share of non-finance firm assets held by zombie firms ballooned from 3% to 16%. The run-up differed by industry: Manufacturing zombie assets rose from 2% to 12%, from 5% to 33% in real estate, and from 11% to 39% in services. These zombie firms linger on, tying up valuable resources with low-productivity activities and drag on the economy.

China’s Economy

I’m not prone to China hysteria generally. However, I do have uncertainty about the plans and actions of the Chinese government because I don’t know that domestic economic welfare is its priority. That makes forecasting more political and less economic and outside my expertise. Regardless, the Chinese economy is a constraint on the government, whether they like it or not. And there are some echoes of the Japanese economy’s lost decades.

Economists overwhelmingly see tariffs as clearly welfare-reducing. Tariffs on imports result in higher prices, fewer imports, less consumption, and more domestic production. In fact, it is the higher prices that solicit and make profitable the greater domestic production. We don’t get the greater domestic output at the pre-tariff price. We can show graphically that domestic welfare is harmed with either export or import tariffs. The basic economics are very clear.

However, the standard model of international trade makes a huge assumption: Peace. That is, the model assumes that there are secure property rights and no threats of violence. All transactions are consensual. This is where the political scientists, who often don’t understand the model in the first place, say ‘Ah ha!. Silly economists…’ They proceed to argue for tariffs on the grounds of national security and the need for emergency manufacturing capacity. But is an intellectual mistake.

Just as economists have a good idea for how to increase welfare with exchange, we also have good ideas about how to achieve greater or fewer quantities transacted in particular markets. This is not a case of economists knowing the ideal answer that happens to be politically impossible. Rather, if it pleases politicians, economists can provide a whole menu of methods to increase US manufacturing, vaccine manufacturing, weapons manufacturing… Heck, we can identify multiple ways to achieve more of just about any good or service. Let the politicians choose from the menu of alternatives.

The problem with tariffs is that they reduce consumer welfare a lot, given some amount of increased production in the protected industry. Importantly, this assumes that the tariffs aren’t hitting inputs to those industries and are only being applied to direct foreign competitors. The below argument is even stronger against imperfectly applied tariffs, like the US tariffs of 2025.

What’s the alternative?

The alternative is a more focused tack. If the government wants more missile or ship production, then what should it do? There’s plenty, but here’s a short list of more effective and less harmful alternatives to tariffs:

This post illustrates a couple of things that I learned this year with an application in finance. I learned about the simplex when I was researching amino acids. I learned some nitty-gritty about portfolio theory. These combined with my pre-existing knowledge about game theory and mixed strategy solutions.

Specifically, I learned a way of visualizing all possible portfolio returns. This post narrowly focuses on 3 so that I can draw a picture. But the idea generalizes to many assets.

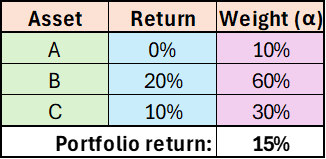

Say that I can choose to hold some combination of 3 assets (A, B, & C), each with unique returns of 0%, 20%, and 10%. Obviously, I can maximize my portfolio return by investing all of my value in asset B. But, of course, we rarely know our returns ex ante. So, we take a shot and create the portfolio reflected in the below table. Our ex post performance turns out to be a return of 15%.

That’s great! We feel good and successful. We clearly know what we’re doing and we’re ripe to take on the world of global finance. Hopefully, you suspect that something is amiss. It can’t be this straightforward. And it isn’t. At the very least, we need to know not just what our return was, but also what it could have been. Famously, a monkey throwing darts can choose stocks well. So, how did our portfolio perform relative to the luck of a random draw? Let’s ignore volatility or assume that it’s uncorrelated and equal among the assets.

Visualizing Success with Two Assets

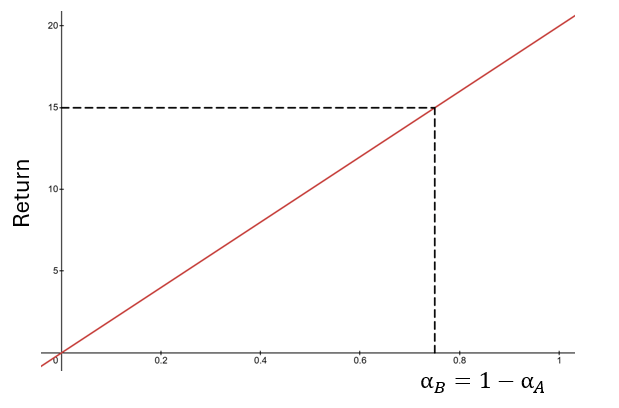

Say that we had only invested in assets A and B. We can visualize the weights and returns easily. The more weight we place on asset A, the closer our return would have been to zero. The more weight that we place on asset B, the closer our return would have been to 20%.

If we had invested 75% of our value in asset B and 25% in A, then we would have achieved the same return of 15%. In this two-asset case, it is clear to see that a return of 15% is better than the return earned by 75% of the possible portfolios. After all, possible weights are measures on the x-axis line, and the leftward 75% of that line would have earned lower returns. Another way of saying the same thing is: “Choosing randomly, there was only a 25% that we could have earned a return greater than 15%.”

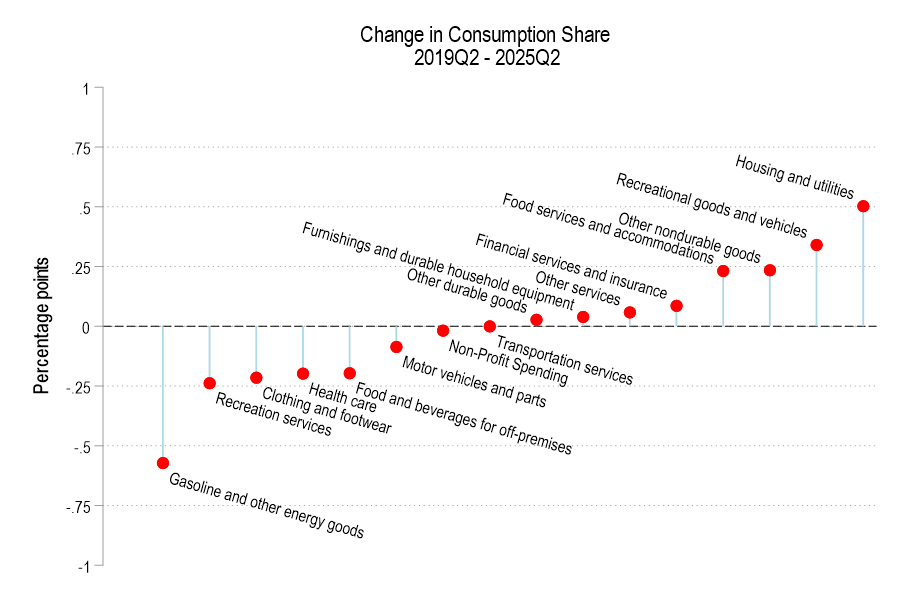

In aggregate, consumer spending on different broad categories of goods is relatively stable. The year 2019 feels like forever ago – and it was more than half a decade ago. But since then we’ve been hit by a pandemic and an AI shock and a trade war, and tariffs, and… plenty. We live in different times. Except, broadly, consumers are spending their money much as they did six years ago. Let’s compare some data from the 2nd quarter of 2019 and 2025.

First the Spending

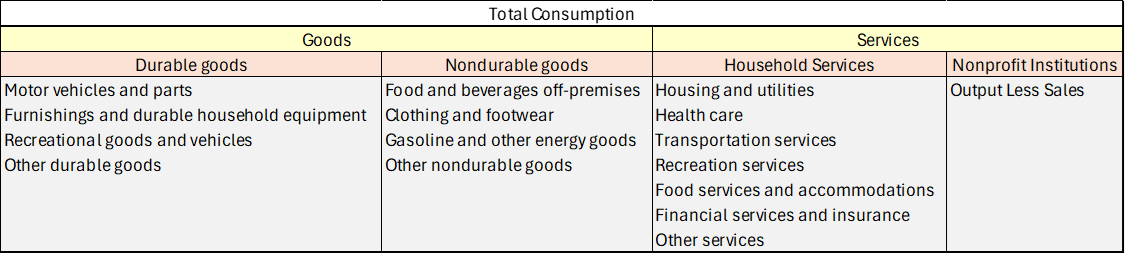

Consumption spending is categorized in the below table.

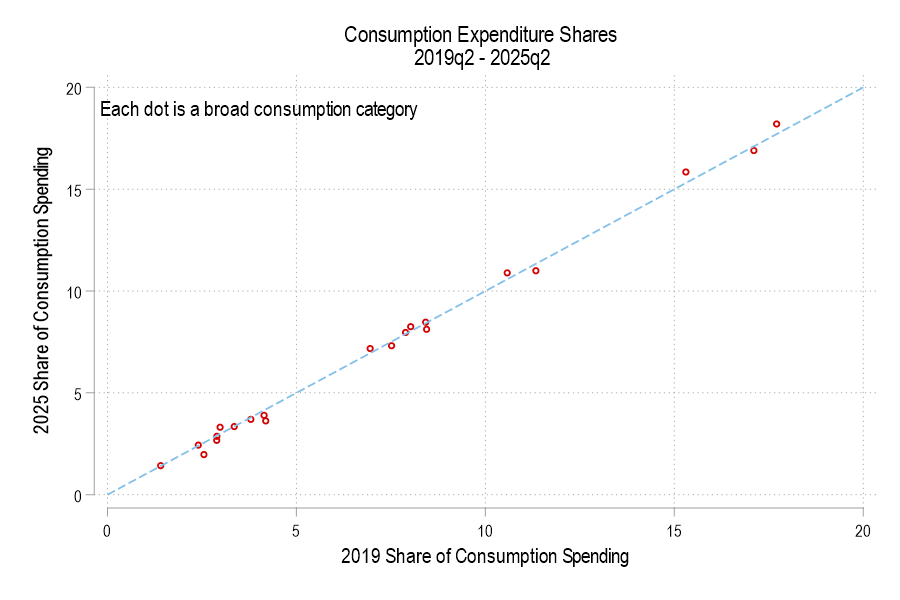

If total consumption spending (not inflation-adjusted) is 100%, then how has the allocation of spending changed? Below is a graph comparing each consumption component’s 2019 share versus 2025. The dotted line denotes an identical share. I haven’t labeled the categories because, suffice it to say, that spending shares are little different. None is more than one percentage point different.

The below figure displays the spending share difference. We’re spending less of our consumption on gasoline and the like, recreational services, and clothing. Surprisingly, we’re also spending less on healthcare and food for off-premises consumption (non-restaurants). However, we’re spending a greater share on housing, recreational goods, food services for on-premises consumption (restaurants).

Much of what economics has to say about tariffs comes from microeconomic theory. But it’s mostly sectoral in nature. Trade theory has some insights. But the effects on the whole of an economy are either small, specific to undiversified economies, or make representative agent assumptions that avoid much detail. Given that the economics profession has repeatedly said that the Trump tariffs would contribute to inflation, it seems like we should look at the historical evidence.

Lay of the Land

Economists say things like ‘competition drives prices closer to marginal cost’. Whether the competitor lives abroad is irrelevant. More foreign competition means lower prices at home. But that’s a partial equilibrium story. It’s true for a particular type of good or sector. What happens to prices in the larger economy in seemingly unrelated industries? The vanilla thinking that it depends on various elasticities.

I think that the typical economist has a fuzzy idea that the general price level will be higher relative to personal incomes in some sort of real-wages and economic growth mental model. I don’t think that they’re wrong. But that model is a long-run model. As we’ve discovered, people want to know about inflation this month and this year, not the impact on real wages over a five-year period.

Part of the answer is technical. If domestic import prices go up, then we’ll sensibly see lower quantities purchased. The magnitude depends on the availability of substitutes. But what should happen to total import spending? Rarely do we talk about the expenditure elasticity of prices. Rarely do we get a simple ‘price shock’ in a subsector. It’s unclear that total spending on imports, such as on coffee, would rise or fall – not to mention the explicit tax increase. It’s possible that consumers spend more on imports due to higher prices, or less due to newly attractive substitutes. The reason that spending matters is that it drives prices in other parts of the economy.

For example, I argued previously that tariffs reduce dollars sent abroad (regardless of domestic consumer spending inclusive of tariffs) and that fewer dollars will return as asset purchases. I further argued that uncertainty makes our assets less attractive. That puts downward pressure on our asset prices. However, assets don’t show up in the CPI.

According to the above discussion, it’s unclear whether tariffs have a supply or demand impact on the economy. The microeconomics says that it’s a supply-side shock. But the domestic spending implications are a big question mark.

What is a Tariff Shock?

That’s the title of a recent working paper from the Federal Reserve Bank of San Francisco. It’s a fun paper and I won’t review the entirety. They start by summarizing historical documents and interpreting the motivation of tariffs going back to 1870. They argue that tariffs are generally not endogenous to good or bad moments in a business cycle and they’re usually perceived as permanent. The authors create an index to measure tariff rates.

Here’s the fun part. They run an annual VAR of unemployment, inflation, and their measure of tariffs. Unemployment in negatively correlated with output and reflects the real side of the economy. Along with inflation, we have the axes of the Aggregate Supply & Aggregate Demand model. Tariffs provide the shock – but to supply or demand?. Below are the IRF results:

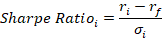

We all like high returns on our investments. We also like low volatility of those returns. Personally, I’d prefer to have a nice, steady 100% annual return year after year. But that is not the world we live in. Instead, there are a variety of returns with a diversity of volatilities. A general operating belief is that assets with higher returns tend to be associated with greater return volatility. The phrase ‘scared money don’t make money’ implies that higher returns are risky. The Sharpe ratio is a tool that helps us make sense of the risk-reward trade-off.

Let’s start with the definition.

By construction, the risk-free return is guaranteed over some time period and can be enjoyed without risk. Practically speaking, this is like holding a US treasury until maturity. We assume that the US government won’t default on its debt. Since there is no risk, the volatility of returns over the time period is zero.

Since an asset’s return doesn’t mean much in a vacuum, we subtract the risk-free return. The resulting ‘excess return’ or ‘risk premium’ tells us the return that’s associated with the risk of the asset. Clearly, it’s possible for this difference to be negative. That would be bad since assets bear a positive amount of risk and a negative excess return implies that there is no compensation for bearing that risk.

The standard deviation of an asset’s returns are a measure of risk. An asset might have a higher or lower value at sale or maturity. Since the future returns are unknown and can end up having any one of many values, this encapsulates the idea of risk. Risk can result in either higher or lower returns than average!

Putting all the pieces together, the excess return per risk is a measure of how much an asset compensates an investor for the riskiness of the returns. That’s the informational content of the Sharpe ratio, which we can calculate for each asset using historical information and forecasts. Once we’ve boiled down the risk and reward down to a single number, we can start to make comparisons across assets with a more critical eye.

Sometimes friends or students will discuss their great investment returns. They achieve the higher returns by adopting some amount of risk. That’s to be expected. But, invariably, they’ve adopted more risk than return! That means that their success is somewhat of a happy accident. The returns could easily have been much different, given the volatility that they bore.

Let’s get graphical.

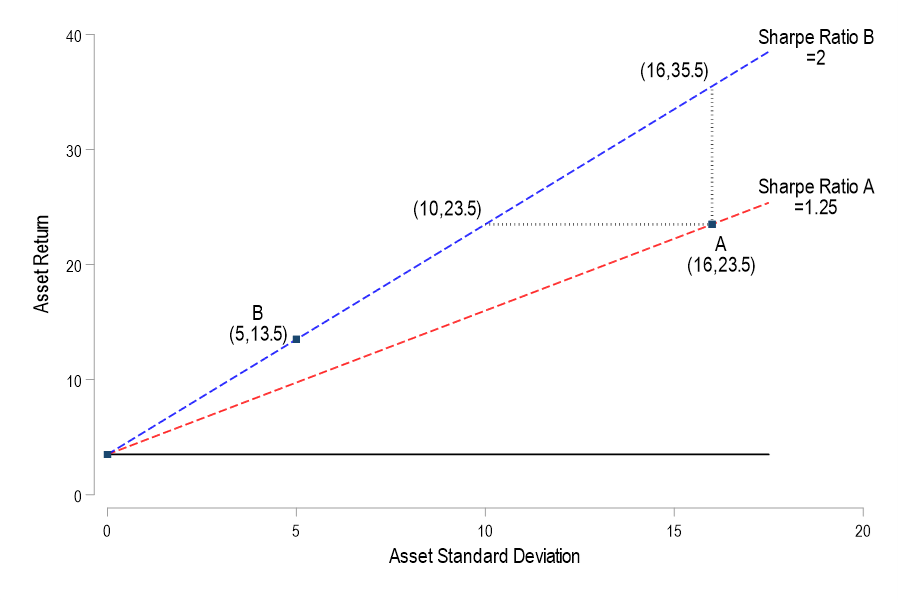

Consider a graph in (standard deviation, return) space. In this space we can plot the ordered pair for some portfolios. The risk-free return occurs on the vertical intercept where the return is positive and the standard deviation is zero. Say that a student was thrilled with asset A’s 23.5% return and that it’s standard deviation of returns was 16%. Meanwhile, another student was happy with asset B’s 13.5% return and 5% standard deviation. With a risk-free rate of 3.5%, the Sharpe ratios are 1.25 & 2 respectively. We can plot the set of standard deviation and return pairs that would share the same constant Sharpe ratio (dotted lines). Solving for the asset return:

The above is simply a linear function relating the return and standard deviation. In particular, it says that for any constant Sharpe ratio, there is a linear relationship between possible asset returns and standard deviations. The below graph plots the two functions that are associated with the two asset Sharpe ratios. The line between the risk-free coordinate and the asset coordinate identifies all of the return-standard deviation combinations that share the same Sharpe ratio. This line is known as the iso-Sharpe Line.

With this tool in hand, we can better interpret the two student asset performances. There are a couple of ways to think about it. If asset A’s 23.5% return had been achieved with an asset that shared the Sharpe ratio of asset B, then it would have had risk that was associated with a standard deviation of only 10%. Similarly, if asset A’s volatility remained constant but enjoyed the returns of asset B’s Sharpe ratio, then its return would have been 35.5% rather than 23.5%. In short, a higher Sharpe ratio – and a steeper iso-Sharpe line – imply a bigger benefit for each unity of risk. The only problem is that a such an nice asset may not exist.

What do portfolio managers even get paid for? The claim that they don’t beat the market is usually qualified by “once you deduct the cost of management fees”. So, managers are doing something and you pay them for it. One thing that a manager does is determine the value-weights of the assets in your portfolio. They’re deciding whether you should carry a bit more or less exposure to this or that. This post doesn’t help you predict the future. But it does help you to evaluate your portfolio’s past performance (whether due to your decisions or the portfolio manager).

Imagine that you had access to all of the same assets in your portfolio, but that you had changed your value-weights or exposures differently. Maybe you killed it in the market – but what was the alternative? That’s what this post measures. It identifies how your portfolio could have performed better and by how much.

I’ve posted several times recently about portfolio efficient frontiers (here, here, & here). It’s a bit complicated, but we’d like to compare our portfolio to a similar portfolio that we could have adopted instead. Specifically, we want to maximize our return given a constant variance, minimize our variance given a constant return or, if there are reallocation frictions, we’d like to identify the smallest change in our asset weights that would have improved our portfolio’s risk-to-variance mix.

I’ll use a python function from github to help. Below is the command and the result of analyzing a 3-asset portfolio and comparing it to what ‘could have been’.

Over the last two weeks I’ve been learning and writing about possible portfolios, the risk-return boundaries, and the efficient frontiers. This won’t be the last post either. I created a python function that can accept a vector of asset returns and a covariance matrix, then produce the piece-wise parabolic function for all of the possible frontiers. It also optionally graphs them, noting the minimum possible variance.