Data on Gross State Product prior to 2017 has disappeared from the main page of the Bureau of Economic Analysis. It is also gone from some third party hosts like FRED. It turns out BEA is in the middle of revising how they calculate state GDP; they have the new version done back to 2017, and took down the older inconsistent estimates until they can recalculate them. After that, they tell me they will repost pre-2017 state Gross Domestic Product:

In the mean time, they offer some messy and seemingly incomplete versions of pre-2017 GDP here, and you can find 1980-2021 state GDP (along with many other nice variables) in a nice panel from the University of Kentucky Center for Poverty Research’s National Welfare Data.

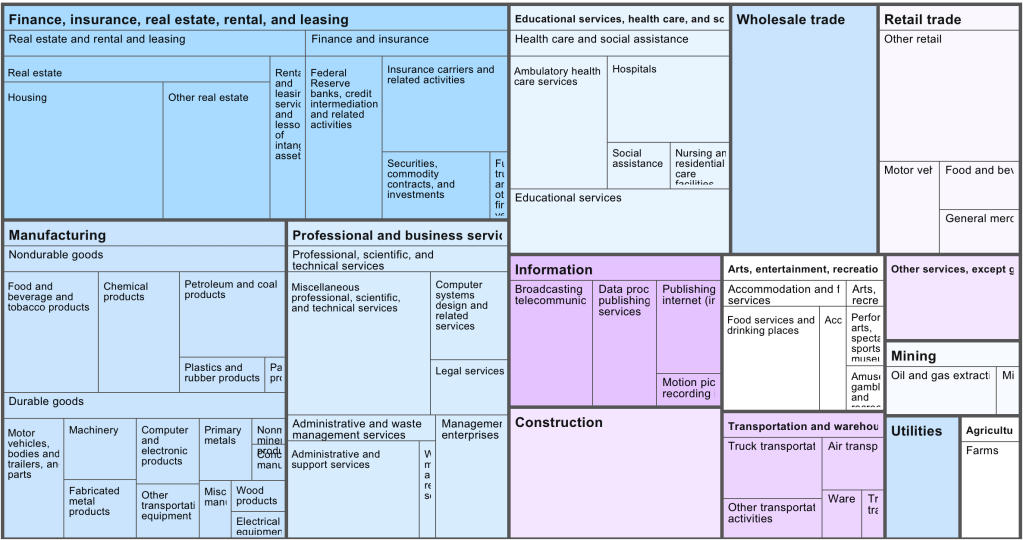

You can find more details on the actual changes BEA is making to how they calculate GDP here. Most changes seem relatively minor for states, but might have more impact on the measured relative size of industries. For instance, “equity REITs will be reclassified from the funds, trusts, and other financial vehicles industry to the real estate industry, while mortgage REITs will remain classified as funds, trusts, and other financial vehicles”.