I’m heading to New Orleans tomorrow for the 2023 meeting of the Southern Economic Association, where I’ll present research on the labor market effects of Certificate of Need laws.

I’ll take this as an excuse to re-up two previous posts on New Orleans:

I recommend reading the whole thing, but here’s the conclusion:

As much as things have changed since 2013, my overall assessment of the city remains the same: its unlike anywhere else in America. It is unparalleled in both its strengths and its weaknesses. If you care about food, drink, music, and having a good time, its the place to be. If you’re more focused more on career, health, or safety, it isn’t. People who fled Katrina and stayed in other cities like Houston or Atlanta wound up richer and healthier. But not necessarily happier.

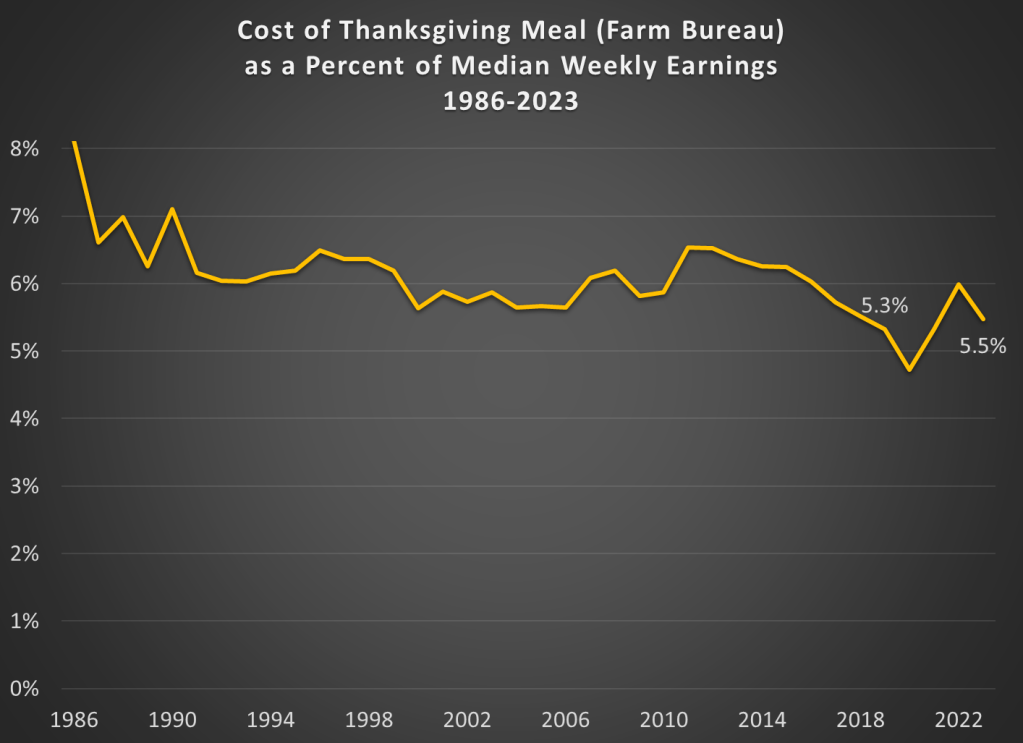

Continuing my tradition of Thanksgivingposts, Farm Bureau released today the latest data on the cost of a traditional Thanksgiving meal. There is welcome news for consumers, as the nominal price of the dinner is slightly lower than last year: $61.17 vs. $64.05 in 2022. The big factor in this decline was the fall in the price of turkeys, though eight of the 12 items in this meal are lower than 2022. As they note in the press release, this is still significantly higher than 2019: about 25% higher.

Regular readers will know what’s coming. Let’s compare those prices (and some historical prices) to earnings:

The Farm Bureau turkey dinner stands at about 5.5 percent of median weekly earnings from the third quarter of this year. That’s a touch higher than 2019, when it was 5.3 percent of weekly earnings. But notice that other than 2019, the figure for 2023 is the lowest ever! (Ignoring the weird years of the pandemic, when wage data is hard to interpret.) So we haven’t quite gotten back to 2019 levels, but we are at the same level as 2018. And lower than 2017. And all prior years too.

The last few Thanksgivings have been tough for Americans. This year, we can all be thankful for falling prices and rising wages.

That extra $4 trillion or so that the feds dumped into our collective checking accounts in 2020-2021 – -where did it come from? Certainly not from taxes. It was created out of thin air, via a multi-step alchemy. The government does not have the authority to simply run the printing presses and crank out benjamins. The U.S. Treasury sells bonds to Somebody(ies), and that Somebody in turn gives the Treasury cash, which the Treasury then uses to fund government operations and giveaways. In 2020-2021, the Somebody who bought all those bonds was mainly the Federal Reserve, which does have the power to create unlimited amounts of cash, in exchange for government bonds or certain other investment-grade fixed income securities.

What is causing a bit of a kerfuffle recently is public assessment of what sorts of bonds that Janet Yellen’s Treasury issued back then. Interest rates were driven down to historic lows in that period, thanks to the Fed’s monster “quantitative easing” (QE) operations. The Fed was buying up fixed income hand over fist: government bonds, mortgage securities, even corporate junk bonds (which was probably illegal under the Fed’s charter, but desperate times…). This buying frenzy drove bond prices up and rates down.

All corporate CFOs with functioning neurons and with BB+ credit ratings refinanced their company debt in that timeframe: they called in as much of their old bonds as they could, and re-issued long-term debt at near-zero interest rates. Or they just issued 5, 10, 20 year low-interest bonds for the heck of it, raising big war-chests of essentially free cash to tide them through any potential hard times ahead. And of course, millions of American homeowners likewise refinanced their mortgages to take advantage of low rates.

What about the federal government? Was the Treasury, under Secretary Yellen, similarly clever? No, not really. Because there is little serious doubt that the U.S. government will be able to pay its debts (grandstanding government shutdowns aside), the government can always find takers for 20- and 30-year bonds, as well as shorter maturity securities. A mainstay of government financing is the 10-year bond. And in 2020-2021, the Fed would have consumed whatever kinds of bonds the Treasury wanted to sell, so the Treasury could have issued a boatload of long-term bonds.

It seems that the Treasury issued a lot of 2-year bonds, rather than longer-term bonds. If they had issued say ten-year bonds, the government would have had a decade of enjoying very low interest payments on that huge slug of pandemic-related debt. But now, all those 2-year bonds are being rolled over at much higher rates and thus much greater expense to the government. (Since the federal debt only grows, almost never shrinks, maturing earlier bonds are not simply paid down, but are paid by issuing yet more bonds).

Veteran hedge fund manager Stanley Druckenmiller (reported net worth: $6 billion) commented in an interview:

When rates were practically zero, every Tom, Dick and Harry in the U.S. refinanced their mortgage… corporations extended [their debt],” he said. “Unfortunately, we had one entity that did not: the U.S. Treasury….

Janet Yellen, I guess because political myopia or whatever, was issuing 2-years at 15 basis points[0.15%] when she could have issued 10-years at 70 basis points [0.70 %] or 30-years at 180 basis points [1.80%],” he said. “I literally think if you go back to Alexander Hamilton, it is the biggest blunder in the history of the Treasury. I have no idea why she has not been called out on this. She has no right to still be in that job.

Ouch.

Druckenmiller went on:

When the debt rolls over by 2033, interest expense is going to be 4.5% of GDP if rates are where they are now,” he warned. “By 2043—it sounds like a long time, but it is really not—interest expense as a percentage of GDP will be 7%. That is 144% of all current discretionary spending.

“Well, I disagree with that assessment,” Yellen said when asked to respond to the accusation during an interview on CNN Thursday night. She said the agency has been lengthening the average maturity of its bond portfolio and “in fact, at present, the duration of the portfolio is about the longest it has been in decades.”

According to Druckenmiller, this is not quite true. It does seem that of the federal bonds held by the public (including banks), the average maturity (recently as long as 74 months) has indeed been a bit longer than usual in the past several years. However, this ignores the huge amount of government bonds held at the Fed:

“The only debt that is relevant to the US taxpayer is consolidated US government debt,” Druckenmiller said. “I am surprised that the Treasury secretary has chosen to exclude $8 trillion on the Fed balance sheet that is paying overnight rates in the repo market. In determining policy, it makes no sense for Treasury to exclude it from their calculations.”

Druckenmiller makes an important point. However, how this plays out depends on how the Fed treats these bonds going forward. If the Fed keeps these bonds on its balance sheet, and buys the replacement bonds, there will be actually very little interest expense to the government going forward. The reason is that the Fed is required to remit 90% of its profits back to the Treasury, so the gazillions of interest payments on those bonds and their replacements will largely flow right back to Treasury. However, if the Fed continues with reducing its balance sheet, forcing the Treasury to go the open market to roll these bonds over, Druckenmiller’s dire warnings will prove correct.

Because of this enormous debt overhang and the ongoing need for the government to sell bonds, I do not expect interest rates to go down as low as 2021 or even 2019 levels, unless there is a financial catastrophe requiring the Fed to become a gigantic net buyer of bonds once again.

I keep reading and hearing people who are waiting for the shoe to drop on the next recession. They see high interest rates and… well, that’s what they see. Employment is ok and NGDP is chugging along.

One indicator of economic trouble is the delinquency rate on debt. That’s exactly what we would expect if people lose their job or discover that they are financially overextended. They’d fail to meet their debt obligations. But the broad measure of commercial bank loans is quiet. Not only is it quiet, it’s near historic lows in the data at only 1.25% in 2023Q2. Banks can lend with a confidence like never before.

But maybe that overall delinquency rate is obscuring some compositional items. After all, we know that many recessions begin with real-estate slowdowns. Below are the rates for commercial non-farmland loans, farmland loans, and residential mortgages. All are near historical lows, though there are hints that they’re might be on the rise. But one quarter doesn’t a recession make. I won’t show the graph for the sake of space, but all business loan delinquency rates have also been practically flat for the past five years.

The RWI − Leibniz Institute for Economic Research has funding for researchers to replicate papers in development economics:

RWI invites applications for several positions of Replicator on a self-employed basis to conduct a robustness replication of a published microeconomic study in the field of Development Economics. The successful applicant will work with us on the project “Robustness and Replicability in Economics (R2E)”, funded by the German Science Foundation (DFG) Priority Programme “Meta-Rep”….

The ultimate goal is to contribute to the ongoing debate about replicability and replication rates in eco- nomics. We collaborate closely with the Institute for Replication (I4R). All robustness replications will contribute to a meta-paper summarizing the collective findings. We plan to publish this meta-paper by the end of 2024, and all replication fellows will be co-authors….

The position starts as soon as possible and is limited to six months. The work can be done fully remotely. The applicant will receive compensation of 2,500 € gross in total, possible distributed in installments based upon predetermined deliverables. Additionally, replication fellows will be listed as co-authors on the meta-paper. At the conclusion of the project, it is foreseen to gather all fellows for a final workshop at RWI in Essen, Germany.

I don’t know the team here but I’m alwayshappy to see more attempts to make economic research more reliable. The funding and the planned publication make this potentially a good deal for applied microeconomists, especially grad students. Full details are here (warning: PDF).

Last week I gave some advice on how to save money on food. Food prices are up a lot in the past 4 years, but especially since the beginning of 2021. Over the 32 months since January 2021, grocery prices (according to the CPI) are up 20 percent (keep that number in mind). To give you an idea of how unusual that is, in the 32 months before the pandemic (up to January 2020), grocery prices only rose 2 percent. Perhaps even more astonishingly, if we look at October 2019 grocery prices, they were slightly lower on average than 4 years earlier in October 2015. From a flat 4 years to a 25 percent increase over the next 4 years. That’s a huge change for consumers.

But we also shouldn’t overstate the price increases. As you might guess, the best place for overstatements is social media. You can find plenty of them. For example, this very viral video claims that her family’s grocery prices doubled (in fact, almost exactly doubled, to the penny, which is suspicious) in just one single year, from August 2021 to August 2022. According to the CPI data, grocery prices were up 13.5 percent over that period — which, don’t get me wrong, is a lot! But it’s not 100 percent. I’ll focus on this one example, but I’m sure you will believe me that you can find dozens of examples like this on social media every single day (for example, yesterday someone claimed bread prices had tripled since 2019).

Let’s leave aside for a moment that in that viral video she claims to spend $1,500 per month on groceries. This would be a massive outlier for 2022. A family in the middle income quintile spent $460 per month on groceries in 2022, and $713 on all food including restaurants. So even if this family eats every single meal at home, they are still spending twice as much as a middle income family. Even a family with 5 or more people (the largest bucket BLS uses in that report) spent $755 per month on groceries ($1,232 on all food). According to the Consumer Expenditure survey, the middle quintile grocery spending went up 16%, and the five-person household went up 19% from 2021 to 2022. Big increases, no doubt! But not 100%.

So who are we to believe? Have prices roughly doubled since 2021? Or are they up about 20 percent? People are sometimes skeptical of the consumer price index, so let’s look at the actual price data that goes into the index. BLS has data on hundreds of individual food items, but here’s a summary chart with eight common food items. Here’s the change in the prices of those items since January 2021:

This week I was in Bretton Woods, New Hampshire. The Mount Washington Resort there is lovely on its own terms as a grand old hotel surrounded by mountains, but it is better known (at least among economists) as the site of the 1944 conference that gave us the International Monetary Fund, the World Bank, and the postwar international monetary system.

This got me thinking about what other destinations should top the list of sites for economics tourism. Adam Smith’s house in Scotland has to be on there. In the US I’ve been trying to visit all 12 Federal Reserve banks; they tend to have nice architecture as well as a Money Museum. You can stay at Milton and Rose Friedman’s cabin in Vermont, Capitaf. I’d like to go to Singapore for many reasons, but one is that they seem to listen to economists more than any other country; I’m not sure what places to visit within Singapore that best reflect that, though.

The places I’ve listed so far are somewhat inward looking to the economics profession; you could get a much bigger list by looking outward to the economy itself, doing “economic tourism” rather than “economics tourism”. Visit a port, a mine, or a factory (like Adam Smith visiting a pin factory and getting ideas for the Wealth of Nations); visit a stock exchange or a bazaar. Visit whatever country currently has the fastest economic growth, or the worst inflation.

Those are my ideas, but I’d love to hear yours: what are the best places for econ tourism?

It’s the time of the year when we share ideas for things to buy, possibly as Christmas or other holiday gifts. But I’m going to share with you not a specific thing to buy, but instead a method for buying things. And probably not the kind of thing you might think of sticking in a wrapped present: food.

We’ve all heard about and felt inflation lately. But food prices have been especially noticeable to consumer, and not just because it’s a product you frequently buy and probably know the price of many food items. Food prices, both at home and restaurants, have increased much more than the average price levels.

On average, prices are up about 20 percent in the US over the past 4 years. But food prices are up about 25 percent, on average.

Wages (the purple line) actually have increase faster than the general price level over the past 4 years — that may shock you given what we constantly hear in the traditional and social media about “price increases outpacing wage gains” — but it is true when we are talking about food. Your dollar doesn’t go quite as far as it used to for food.

In some sense these costs are hard to avoid: food is a necessity. But there are ways to reduce your costs, and you probably know the general tips. Eat less at restaurants. Buy generic. Buy in bulk. Etc. These are good tips, but they all involve some sacrifice or annoyance. Is there anything else a consumer can do?

Yes. Here’s a few tips that can save you money, without the sacrifice. There is some thought involved, and perhaps a slight annoyance, but I’ve found that once you get in these habits, the mental and time cost is pretty low.

1. RESTAURANT APPS

You should always be ordering your food through restaurant apps when possible, especially for fast food. I try to track limited good deals on Twitter, but most restaurants offer on-going good deals. For example, McDonalds usually has a 20% off coupon, just for using the app. Taco Bell has a $6 box you can build, which would cost around $10 to order as a combo or à la carte at the restaurant. That’s a 40% discount for using the app.

Using apps also means you are using the restaurant’s rewards programs. Valuations vary, but McDonald’s rewards are roughly worth 10% cash back.

2. CHASE THE SALES AT GROCERY STORES

Clipping coupons is the classic way of saving money at the grocery store (we even have reality shows about it), but in the modern world grocery stores have expanded the ways to effectively save the same amount of money. The clearest example is, once again, the rise of apps. Stores will often have “digital only” coupons that you need to access through their app (which is also tied to your rewards account, just like restaurants).

While I’m a strong advocate of coupon clipping (and the virtual equivalent), it can be time consuming. Another strategy that can save you is thinking ahead about seasonal and other cyclical prices. For example, my kids like M&M’s. We usually buy a bulk 62-ounce container at Sam’s Club (already a savings), but today I took the additional saving step of buying the Halloween-themed bulk container. It was 36 percent less than the identical Christmas-themed M&M’s container right next to it. And I was replacing the Easter-themed bulk container that we purchased back in April, and they just finished.

Of course, I had to be planning ahead and know that November 1st was a great day to buy M&M’s. That takes some mental effort, sure. And you might think these kinds of deals are fairly limited in nature. But holidays aren’t the only kind of seasonal deals. For example, even though most fruit is generally available year-round now, there are still predictable price cycles of when things are “in season” and when they have to be imported from expensive locations. Even if you are only able to find these cyclical deals for 10 percent of your purchases, saving 30-50% on cyclical goods will shave another 3-5% off your grocery bill — bringing it closer in line to the average increase in prices (and wages).

3. CASH BACK CREDIT CARDS

I could write an entire post about credit card rewards. But let me focus here on credit cards that are especially good for buying food. At a minimum you should be getting 2 percent back on all of your purchases, as there are several no-annual-fee cards that give you 2 percent: the Citi Double Cash and Wells Fargo Active Cash are good examples.

But on food purchases, you should be able to beat 2 percent. For example, the Citi Custom Cash card gives you 5 percent back on your top spending category each month, up to $500 of spending. This can be on either groceries or restaurants. And since a family in the median quintile spends $250 at restaurants and $460 on groceries per month, you should be getting 5 percent back on basically all of your purchases in one of these two categories. (Personally I stick to restaurants for this card, because I buy most of my groceries at Walmart and Sams Club, which don’t count towards the grocery cash back.) Or if you want a simple card that gives you 3 percent back on both groceries and restaurants, check out the Capital One SavorOne card (again, no annual fee).

There are also several cards that have rotating 5 percent cash back categories each quarter, and they often include either restaurants or groceries. How do I keep track of which card to use for what kind of purchase? Simple: put a strip of masking tape on the card with a label. This will get some chuckles from your friends or the server at the restaurant, but that’s just an opportunity to tell them how to save money too!

Is There Really a Free Lunch?

Some of my economist friends are probably skeptical at this point. Aren’t I say there is a free lunch here? Isn’t the extra hassle of the steps I suggested going to outweigh any discount you get?

The answer is No. And while economists are quick to bring up the concept of opportunity cost, I find that most people tend to overestimate their opportunity cost. But even if you don’t overestimate your opportunity cost, you can bring in another useful economic concept: price discrimination.

Restaurants are very much in the business of price discrimination, and always have been. Tuesday Night specials, happy hours, etc. Every consumer has a different willingness to pay, and since it’s hard to resell a restaurant meal, restaurants can potentially use this technique to their advantage (and yours, if you are willing to look for discrimination). Grocery stores don’t have as much of an opportunity to discriminate, but they still find ways.

Don’t be afraid of price discrimination: use it to your advantage!

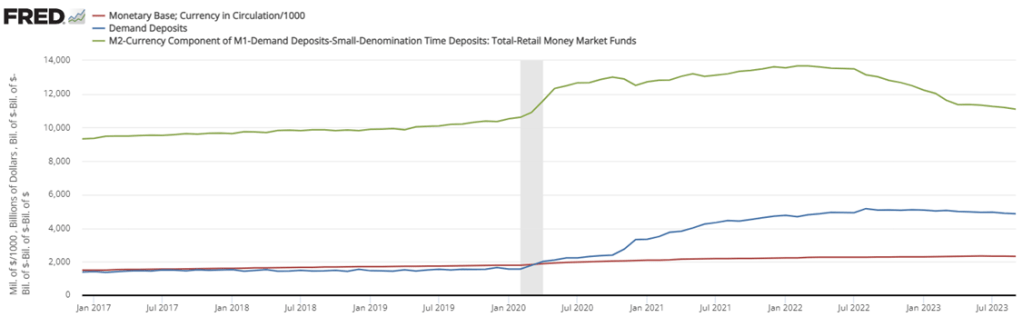

Money and interest rates have been in the news because the Fed wants to slow the rate of inflation, maintain financial stability, and avoid a recession. Let’s break it down. First, some broad context. The M1 and M2 were all chugging along prior to 2020. M2 was growing along with NGDP and, after raising interest rates, the Fed had begun lowering them again. Then Covid, the stimuli, and the redefinition of M1 happened. Now, we’re trying to get back to something that looks like normal. See the graphs below.

But these aggregates gloss over some relevant compositional changes. Let’s go one-by-one.

The monetary base includes both bank reserves and currency in circulation. We could break it down further, but I’ll save that for another time. What we see is that while currency in circulation did grow faster post-covid, it was nothing compared to the growing reserve balances. From January to May of 2020, currency grew by 7.5% while reserves almost doubled. That means a few things. 1) People weren’t running on banks. Covid was not a financial crises in the sense that people were withdrawing huge sums of cash. 2) Banks were well capitalized, safe, and stable. Further, uncertainty aside, banks were ready to lend. And they did. Not long after the recession, everyone and their brother was re-financing or taking on new debt. More recently, we can see that currency has stabilized and, again, most of the action has been in reserve balances. As of September 2023, reserve balances are down 23% from the high in September 2021.

The thing about the monetary base, however, is that reserves don’t translate into more spending unless the reserves are loaned out. The money supply that people can most easily spend, M1, is composed of currency held outside of banks, deposit balances, and “other liquid deposits” (green line below).* See the graph below. Again, most of the action wasn’t in the physical printing of hard, physical cash. People’s checking account balances ballooned thanks to less spending on in-person services and thanks to the stimulus checks and other relief programs. Deposit balances more than doubled from January to December of 2020. Ultimately, deposit balances were 3.3 *times* higher by August of 2022. Since then, the balances have been on a slow, steady decline of about 5.8% over the course of the year. But even then, it’s those “other” deposits, previously categorized as M2, where most of the action is. The value of those balances have fallen by a whopping 2.5 *trillion* and 19% dollars in the past 18 months. People are drawing down their savings.

Finally, we get to M2, the less liquid measure of the money supply. Besides the M1 components, it also includes small time deposits, such as CD’s, and money market funds (not including those held in IRA and Keogh accounts). Money market funds and small time deposits have *increased* in value since the post stimulus tightening as people chase the allure of higher interest rates on offer. Measured by volume, the declines in the broad money supply have darn near all come from declines in M1 (again, the jump is redefinition). And of that, it’s almost entirely coming out of “other” liquid deposits, as illustrated above. That’s savings balances. It’s true that there is some other-other balances, but it’s mostly savings accounts.

Zooming in on just those “other” balances (below left), people still have higher balances than they did prior to the pandemic. But by now, they’re below the pre-pandemic trend. Savings accounts are depleted. However, since many people don’t use savings account anymore due to the decade plus of low interest rates, it’s appropriate to consider both “other” accounts and demand deposits (below right). By that measure, we still have plenty of post-Covid liquidity at our disposal.

*Other liquid deposits consist of negotiable order of withdrawal (NOW) and automatic transfer service (ATS) balances at depository institutions, share draft accounts at credit unions, demand deposits at thrift institutions, and savings deposits, including money market deposit accounts.

PS. So where is all this above-trend NGDP coming from, if not the money supply? Hmmmm.

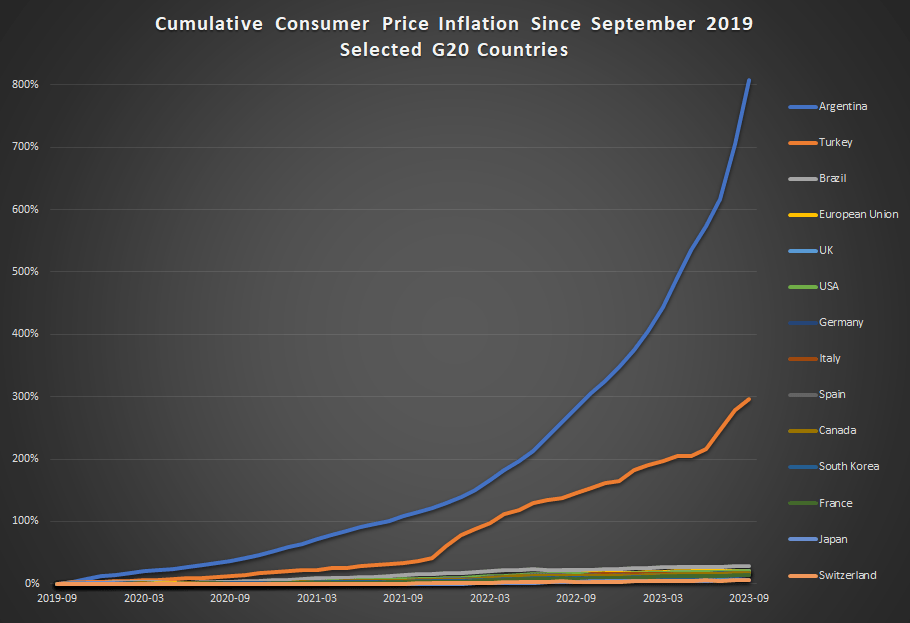

Inflation has been constantly in the news over the past 2 years, but it has especially been in the news lately with regards to one country: Argentina. That country has been experiencing triple-digit annual inflation lately, and it has become one of the key issues in the current presidential race.

How bad is inflation in Argentina? Here’s a comparison to some other G20 countries from September 2019 through September 2023 (data from the OECD).

Cumulative consumer price inflation in Argentina over the past 4 years is over 800 percent. That means goods which cost 100 pesos in September 2019 now costs 900 pesos, on average. Well, they did in September. It’s almost November now, so if the recent inflation rates persisted, those goods are around 1,000 pesos now.

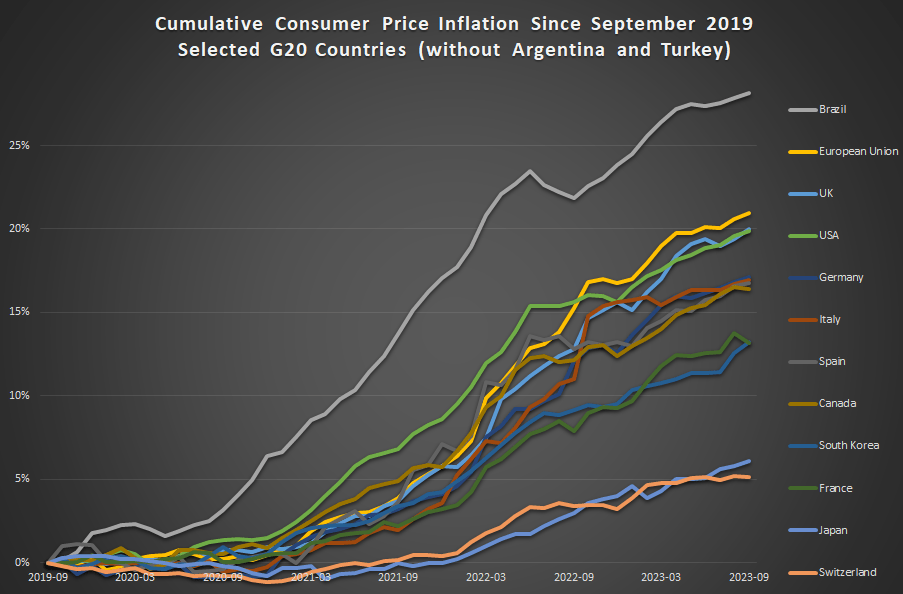

Turkey also stands out as a country with very rapid inflation the past 4 years — without Argentina on the chart, Turkey would clearly stand out from the rest. But other than Turkey, all the other countries are bunched at the bottom. Has there not been much difference among them? Not quite.

This next chart removes Argentina and Turkey:

In this second chart we see two standouts on the opposite end of the spectrum: Japan and Switzerland have had extremely low inflation, just 6 and 5 percent cumulatively since late 2019 (and this is not unusual for these two countries in recent history).

For us here in the USA, things don’t look so good. Only Brazil and the EU are higher (and the EU is mostly due to energy price inflation in Eastern Europe), so other than that we are basically tied with the UK for the worst inflation performance among very high income countries during the pandemic. That’s bad news! But perhaps one silver lining is that average wages in the US have outpaced inflation slightly: 23 percent vs 20 percent growth over this time period. That’s not much to celebrate — except relative to most of the rest of the world.