Whether one might socially offend us or whether one commits a crime, we face a fundamental tension between punishment and forgiveness. Punishment is important because it acts as a deterrent to the initial offense or to subsequent offenses. But punishment is also costly. Severing social or commercial ties reduces the number of possible mutually beneficial transactions. We lose economies of scale and lose gains from trade when we exclude someone from the market. Forgiveness is important because it permits those who previously had conflict to acknowledge the sunk cost of the offense and proceed with future opportunities for trade. However, an excess of forgiveness risks failure to deter destructive behaviors.

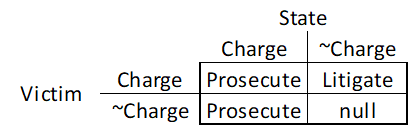

In the US, we enjoy a state that can prosecute alleged offenders and enforce punishments regardless of the economic status of the offended. While not perfect, the state incurs great cost by being the advocate of those who could not enforce great retributive punishment by their own means. A victim may choose to press charges against an offender, or the state can press charges despite a permissive victim.

In fact, our system of prosecution is somewhat asymmetrical. The state can press charges against a suspect, regardless of the victim’s wishes. While a victim can’t compel an unwilling state to press charges, say if the evidence is scant, an individual can engage in litigation against the accused.

Most of the possible combinations of victim and state strategies result in some kind of prosecution of the alleged offender. Except for litigation, our punishments in the US tend not to be remunerative – the victim isn’t compensated for the evils of the offender. ‘Justice’ is often construed as a type of compensation, however.

I was pleased to see yesterday the announcement of a new journal, the Journal of Comments and Replications in Economics. As the name implies, it will publish articles that comment on or attempt to replicate previously published economics papers.

While empirical economics papers have in some ways become more believable over time, it is still rare for anyone to verify whether the results can actually be replicated, and formal comments on potential problems in published papers have actually become less common over time (though Econ Journal Watch has been a good outlet for comments).

The ability to independently verify and replicate findings should be at the core of science. But economists, like most other disciplines, are generally too focused on publishing original work to test whether already-published papers hold up. When we do try to replicate existing work, the results aren’t very encouraging; at best 80% of economics papers replicate.

If we want people to trust and rely on our work, we need to do better than that. The US Department of Defense agrees, and funded a huge project to determine what types of social science research hold up to scrutiny. I’ve been a bit involved in this and hope to sum up some of the results once this semester is over. For now, I’ll just say I’m happy to see the new Journal of Comments and Replications in Economics (and that it is both free and open-access, a rare combo) and I hope this represents one more small step towards economics being a real science.

It’s pumpkin spice season. That means that not only can you get pumpkin spice lattes, but also pumpkin spice Oreos, pumpkin spice Cheerios, and even pumpkin spice oil changes.

The most important thing to know about “pumpkin spice” things is that they don’t actually taste like pumpkin. They taste like the spices that you use to flavor pumpkin pie. (Notable exception: Peter Suderman’s excellent pumpkin spice cocktail syrup, which does contain pumpkin puree.)

Last week economic historian Anton Howes posted a picture of the spice shelf at his grocery store and guessed that this would have been worth millions of dollars in 1600.

Just thinking about how much this shelf would have been worth in England in the year 1600. Presumably at least tens of millions in today’s money. pic.twitter.com/Vc9HDBlQxL

Some of the comments pushed back a little. OK, probably not millions but certainly a lot. Howes was alluding to the well-known fact that spices used to be expensive. Very expensive. Spices, along with precious metals, were one of the primary reasons for the global exploration, trade, and colonialism for centuries. Finding and controlling spices was a huge source of wealth.

But how much more expensive were spices in the past? One comment on Howes’ tweet points to an excellent essay by the late economic historian John Munro on the history of spices. And importantly, Munro gives us a nice comparison of the prices of spices in 15th century Europe, including a comparison to typical wages.

As I looked at the list of spices in Munro’s essay, I noticed: these are the pumpkin spices! Cloves, cinnamon, ginger, and mace (from the nutmeg seed, though not exactly the same as nutmeg). He’s even included sugar. That’s all we need to make a pumpkin spice syrup!

Last week in my Thanksgiving prices post I cautioned against looking at any one price or set of prices in isolation. You can’t tell a lot about standards of living by looking at just a few prices, you need to look at all prices. So let me just reiterate here that the following comparison is not a broad claim about living standards, just a fun exercise.

That being said, let’s see how much the prices of spices have fallen.

The U.S. “stock market” is represented by various collections of stocks, such as the Dow Jones Industrial Average (30 stocks), the NASDAQ Composite (securities listed on the NASDAQ; weighted towards information technology), and the Standard and Poor’s 500 Index. The S&P 500 is an index of the largest 500 companies listed on the New York Stock Exchange and the NASDAQ, weighted by capitalization. The version of the S&P usually cited just takes into account stock prices. History shows that, over a reasonably long-time frame, the U.S. stock market rises. Here is a chart, using a logarithmic axis, of the S&P from January, 1950 to February, 2016. It shows a rise in value by a factor of about 65 between 1950 and 2016.

Below is a chart of S&P values from 1980 to 2021 on a linear scale, which compresses the earlier data and magnifies more recent variations. This shows the Covid-related dip in early 2020, which was followed by a meteoric rise as Fed and federal money flooded the financial system:

Source: Yahoo Finance

A lab technician I knew in my company in the 1990s took every bit of savings he had (about $50,000) and plowed it all into the stock of America Online (AOL). This was when the internet was just taking off, and AOL was a leading company in that field. My friend held on while his investment doubled, then had the conviction to hang on until it doubled again. He then cashed out with around $200,000, quit his job, got an MBA in finance, and ended up managing money on Wall Street.

With these sorts of success stories, and the (so far) reliable performance of the stock market, how hard can it be for the average small investor to pick a winning basket of stocks? Surprisingly hard, it turns out.

A study of the returns of U.S. stocks from 1926 to 2015 was published by Hendrik Bessembinder, a business professor at Arizona State University. A draft copy is here . He worked with total returns (stock price plus dividends). He found that the rise of the S&P is entirely due to huge gains by a tiny subset of stocks. The average stock actually loses money over both short and long time periods. In statistical terms, this is an extremely skewed data set; the mean return is greater than the median. There is a sort of Darwinian selection that occurs in a market index like the S&P 500. The companies that are doing well tend to get more represented in the index as their stock prices rises relative to other companies, while the relative weighting of losers automatically diminishes.

This asymmetry between winners and losers is partly a result of the following math: If you invest $1000 in a company that then tanks, the most you can lose is $1000. But if that company is one of the rare firms that really takes off, you could make many times your initial investment. If you had put $1000 into Microsoft (MSFT) in 1986, your shares would now be worth nearly five million dollars.

According to Bessembinder’s study, half of the U.S. stock market wealth creation had come from a mere 0.33% of the listed companies. The top five companies (ExxonMobil, Apple, GE, Microsoft, and IBM, at that point) accounted for a full 10% of the market gain. Each of these companies had created half a trillion dollars or more for their shareholders. ( A similar list of the top five or ten value-creating companies drawn up in 2021 would have a different set of names, obviously, but a similar principal has held in recent years – a huge portion of the rise in “stocks” in the past five years has been due to a handful of internet superstars, the FAANGM stocks).

Out of some 26,000 listed companies, 86 of them (0.33%) provided 50% of the aggregate wealth creation, and the top 983 companies (4%) accounted for the full 100%. That means the other 25,000 companies netted out to zero return. Some gave positive returns, while most were net losers.

The average stock which you might pick by throwing darts at the Wall Street Journal listings lost money 52% of the time in any given month, and 51% of the time over the life of the company. The lifetime of the average company was only seven years, with only 10% of companies lasting more than 27 years.

This helps explain why actively managed stock funds, where diligent experts analyze and select some subset of stocks in an attempt to beat the market, typically underperform the broad market indices. (The fees charged by these funds also drags down their performance relative to the market indices). This also explains why about half the small-cap stocks I have bought over the years in my little recreational brokerage account have lost money. I had thought I was particularly inept at stock-picking. Turns out I was just about average.

In grad school, I learned about the overlapping-generations model. The idea is that we simplify people down to the fundamental parts of their life-cycle. Each person lives for 2 periods. In the first period, they can produce only. In the second period, they can consume only. A popular conclusion of the model pertains to old-age benefit programs such as Social Security.

The first beneficiaries receive a gift that is free to them, then each subsequent generation accepts the debt, pays it off, and then passes on new debt to the proceeding generation. In this manner, the program benefit of the current generation is limited by the income of the following generation. Therefore, every single generation can consume as if they lived a generation later – and a generation richer – in time. That’s exciting.

But this model is not unique to governments. With a little bit of finance, we can model every person as their own self-encapsulated overlapping-generations model – with two similarly exciting conclusions. Let’s consider a person who has monthly consumption expenditures of $1k per month and let’s assume a discount rate of half a percent per month.

Life is pretty good for this person. They earn income each month and they spend $1k of it during the same period. Now let’s give the person a credit card. It doesn’t matter what the interest rate is – they’re going to pay it off each subsequent month. Now let’s see what’s possible.

What’s going on here? The difference in the consumption pattern is that the first month with a credit card can enjoy twice the consumption. How’s that? $1k of that January consumption is just the typical monthly spending. The other $1k is running up a month’s worth of spending on the credit card. So long one pays-off the card in the following month, there are no interest charges. But wait – if one pays-off the credit card in February, then how does one consume in February? By borrowing from March’s income, of course! And so the pattern repeats ad-infinitum. With a credit card one can borrow against next month’s spending. You too can borrow from your future self. And your future self won’t mind because they’ll do the same thing.

Conclusion #1: Having a credit card entitles you to one free month of double consumption.

The above example includes identical income over time. But, what if your income grows? Let’s assume that your income and commensurate consumption grow at a rate of one quarter percent per month. Our consumption without a credit card is tabulated below.

Obviously, having income and consumption that grow is more enjoyable than ones that are constant each period. Now let’s observe below what happens when we again introduce a credit card that one pays-off each month.

What’s going on here? Just as happened previously with a credit card, one can enjoy an extra boost to consumption in the first period. But what does growing income do for us besides greater complication? Just as previously, one can pay their debt each period and consume by borrowing against the next month’s income. But with growing income, having a credit card means that one can enjoy the next month’s level of consumption today. That is, next month’s higher consumption is shifted sooner in time by one month. Notice that, with growing income, consumption for July without a credit card ($1,018) is the same as the consumption in June with a credit card. Even without the first-month-gift, credit cards increase the present value of one’s consumption by making next month’s greater income available today – and the same is true for every single month.

Conclusion #2: Having a credit card today entitles you to next month’s greater income.

How big a deal is this? Obviously, it will differ with the discount rate and the rate of income growth. Using the numbers above, having a credit card permits one to consume with a present value that is 10.5% higher. Let that sink in. People who have access to credit consume as if they are 10.5% percent richer. Access to credit can make the difference between a pleasant Christmas, having quality internet, paying for car repairs, and so on. Being poorer is one thing. Being poorer and lacking access to credit is like taking an instant haircut to one’s quality of life. On the flip side, people can be made better-off without additional improvements to their productivity. Increasing access to credit may be a less costly improvement to the value lifetime consumption than many of the other less politically feasible improvements to labor productivity.

In 1621 the pilgrims were starving after their communal farming system gave them little incentive to work hard, leading them to rely on the generosity of their native neighbors at the first Thanksgiving. But in the long run they were able to produce their own feasts after switching to a private property system. Economist Ben Powell tells the story briefly here, or you can read the primary source, William Bradford’s Diary here.

It is customary in many families to “give thanks to the hands that prepared this feast” during the Thanksgiving dinner blessing. Perhaps we should also be thankful for the millions of other hands that helped get the dinner to the table: the grocer who sold us the turkey, the truck driver who delivered it to the store, and the farmer who raised it all contributed to our Thanksgiving dinner because our economic system rewards them

Powell calls this “the real lesson of Thanksgiving”, and while I think there are other great angles to the story this is certainly a real lesson of Thanksgiving.

But is it true? In short: no. I’ll explain why, but my larger goal is to get you to think more clearly about inflation.

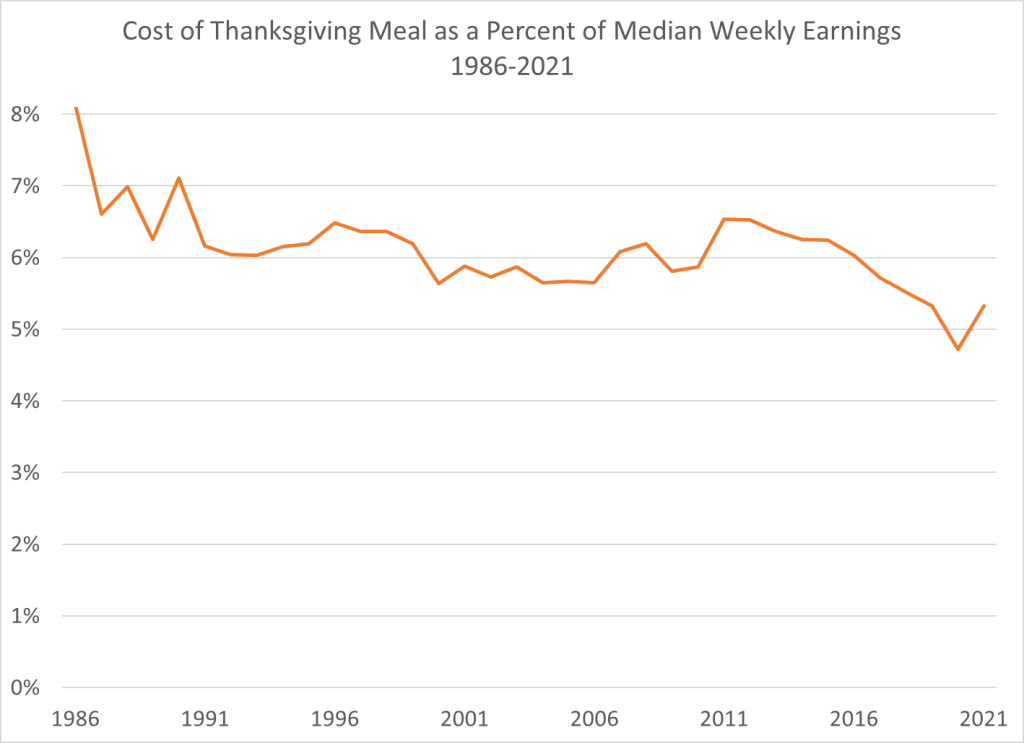

How should we measure the cost of a Thanksgiving meal? A widely used measure comes from the Farm Bureau, which shows that the cost of a traditional turkey-centric meal costs about 14% more than last year. In dollar terms it is $53.31 for a turkey, a pumpkin, cranberries, sweet potatoes, stuffing, etc. That’s more that it has ever been, in dollar terms. Farm Bureau has been tracking the cost of this same meal since 1986.

So in one sense, it seems like the headline claim is true. Most expensive Thanksgiving ever!

But we need to think deeper. A nominal price doesn’t actually tell us much. If a long-lost cousin from the Republic of Horpedahl told you it costs 1 million Jeremys to buy a Thanksgiving dinner, what would your reaction be? The first and best reaction is: how much do people earn in the Republic of Horpedahl?

We should ask the same question in the United States today: how do incomes today compare to incomes in the past? Which measure of income you use is important, but if we use median usual weekly earnings of full-time workers, we can make a simple comparison of how much of your weekly earnings would be needed to buy a traditional Thanksgiving meal. This chart shows exactly that. In 2021 that meal will be the second lowest it has ever been as a percent of median earnings — higher than last year, but tied with 2019 for the second lowest. And much less than in the late 1980s and early 1990s (I use third quarter data for each year, the most recent available).

Adjusting for income is the best way to look at this question. It’s not perfect — part of this depends on what income measure you use — but it’s much better than the alternative. The worst approach is to just look at nominal prices. This tells you virtually nothing.

A recent headline in the Dartmouth student newspaper reads, “Dartmouth’s endowment posts 46.5% year-over-year returns, prompting additional spending on students”. That seems like really great investing performance. But the sub-headline dismisses it as less-than-stellar, by comparison: “The endowment outpaced the stock market, but fell short when compared to other elite universities that have announced their endowment returns.” After all, fellow Ivy League university Brown notched a 50% return for fiscal 2021, which in turn was surpassed by Duke University at 55.9% and Washington University in St. Louis at 65%. The Harvard endowment fund managers are a bit on the defensive for gaining “only” 34% on the year.

The stock market has done well in the past year, but nothing like these results. What is the secret sauce here? Well, it starts with having money already, lots of it. That enables the endowment managers to participate in more esoteric investments. This is the land of “alternative investments”:

Conventional categories include stocks, bonds, and cash. Alternative investments include private equity or venture capital, hedge funds, managed futures, art and antiques, commodities, and derivatives contracts. Real estate is also often classified as an alternative investment.

It takes really big bucks to buy into some of these ventures, and it also takes a large professional endowment fund staff to choose and monitor these sophisticated vehicles. Inside Higher Ed’s Emma Whitford notes:

Endowments valued at more than $1 billion, of which there are relatively few, are more likely to invest in alternative asset classes like venture capital and private equity, recent data from the National Association of College and University Business Officers showed.

“Where you’re going to see higher performance are the institutions with endowments over a billion,” Good said. “If you look at the distribution of where they’re invested, they have a lot more in alternative investments — in private equity, venture capital. And those asset classes did really well. Those classes outperformed the equity market.”

…Most endowments worth $500 million or less invested a large share of their money in domestic stocks and bonds in fiscal 2020, NACUBO data showed. This is partially because alternative investments have a high start-up threshold that most institutions can’t meet, according to Good.

“You have to have a pretty big endowment to be able to invest in that type of asset class,” he said. “If you have a $50 million endowment, you just don’t have enough cash to be able to buy into those investments, which is why you won’t see big gains from alternatives in those smaller institutions.”

Virginia L. Ma and Kevin A. Simauchi report in The Crimson on Harvard’s Endowment, “Harvard Management Company returned 33.6 percent on its investments for the fiscal year ending in June 2021, skyrocketing the value of the University’s endowment to $53.2 billion, the largest sum in its history and an increase of $11.3 billion from the previous fiscal year.” This 33.6% gain, though, represents underperformance compared to Harvard’s peers; this is rationalized in terms of overall risk-positioning:

However, Harvard’s returns have continually lagged behind its peers in the Ivy League, a trend that appeared to continue this past fiscal year. Of the schools that have announced their endowment returns, Dartmouth College reported 47 percent returns while the University of Pennsylvania posted 41 percent returns.

Narvekar acknowledged the “opportunity cost of taking lower risk” in Harvard’s investments compared to the University’s peer schools.

“Over the last decade, HMC has taken lower risk than many of our peers and establishing the right risk tolerance level for the University in the years ahead is an essential stewardship responsibility,” Narvekar wrote.

In 2018, HMC formed a risk tolerance group in order to assess how the endowment could take on more risk while balancing Harvard’s financial positioning and need for budgetary stability. Under Narvekar’s leadership, HMC has dramatically reduced its assets in natural resources, real estate markets, and public equity, while increasing its exposure to hedge funds and private equity.

There it is again, the magical “hedge funds and private equity”.

Harvard’s fund manager went on to warn that the astronomical returns of the past year were something of an anomaly:

At the close of his message, Narvekar cautioned that despite the year’s success, Harvard’s endowment should not be expected to gain such strong returns annually. “There will inevitably be negative years, hence the importance of understanding risk tolerance.”

The following chart illustrates, at least in Harvard’s case, how extraordinary the past year has been:

The fiscal year of these funds typically runs September to September, so it’s worth recalling that back in September of 2020 we were still largely cowering in our homes, waiting for vaccines to arrive. The equity markets were still down in September of 2020, whereas a year later the tsunami of federal and Fed largesse had lifted all equity boats to the sky. So, it is not realistic to expect another year of 50% returns.

Final issue: can the little guy pick up at least a few crumbs under the table of this private equity feast? In most cases, you have to be an “accredited investor” (income over $200,000, or net worth outside of home at least $1 million) to start to play in that game. From Pitchbook:

Private equity (PE) and venture capital (VC) are two major subsets of a much larger, complex part of the financial landscape known as the private markets…The private markets control over a quarter of the US economy by amount of capital and 98% by number of companies….PE and VC firms both raise pools of capital from accredited investors known as limited partners (LPs), and they both do so in order to invest in privately owned companies. Their goals are the same: to increase the value of the businesses they invest in and then sell them—or their equity stake (aka ownership) in them—for a profit.

Venture capital (VC) is perhaps the more attractive, heroic side of this investing complex:

Venture capital investment firms fund and mentor startups. These young, often tech-focused companies are growing rapidly and VC firms will provide funding in exchange for a minority stake of equity—less than 50% ownership—in those businesses.

Some examples of VC-backed enterprises include Elon Musk’s SpaceX, and Google-associated self-driving venture WayMo.

Venture capital takes a big chance on whether some nascent technology will succeed (in the fact of competition) many years down the road, which has the potential to make the world a better place for us all. Private equity, on the other hand, tends to be somewhat more prosaic, predictable, and sometimes brutal. Here is putting it nicely:

Private equity investment firms often take a majority stake—50% ownership or more—in mature companies operating in traditional industries. PE firms usually invest in established businesses that are deteriorating because of inefficiencies. The assumption is that once those inefficiencies are corrected, the businesses could become profitable.

In practice, this often entails taking control of a company via a leveraged buyout which saddles the new firm with heavy debt, firing lots of employees, improving some strategy or operations of the firm, and sometimes breaking it up and selling off the pieces. This was the fate of several medium-sized oil companies that got in the cross-hairs of corporate raider T. Boone Pickens. “Chainsaw Al” Dunlop also became famous for this sort of “restructuring” or “creative destruction”.

Private equity activities can be very lucrative. But again, is there any way for you, the little guy, to get a piece of this action? Well, kind of. There are publicly traded companies who do this leveraged buyout stuff, and you can buy shares in these companies, and share in the fruits of their pruning of corporate deadwood. Some names are: Kohlberg Kravis Roberts (KKR), The Carlyle Group (CG), and The Blackstone Group (BX). The share prices of all these firms have more than doubled in the past year (100+ % return). If you had had the guts to plow all your savings into any one of these private equity firms a year ago, you would have had the glory of beating out all those university endowment funds with their piddling 50% returns.

This weekend I’ll be at the Southern Economic Association Conference in Houston Texas. I’m organizing and chairing a session called Education Policy Impacts by Sex (you should come by and see me if you will be there too!).

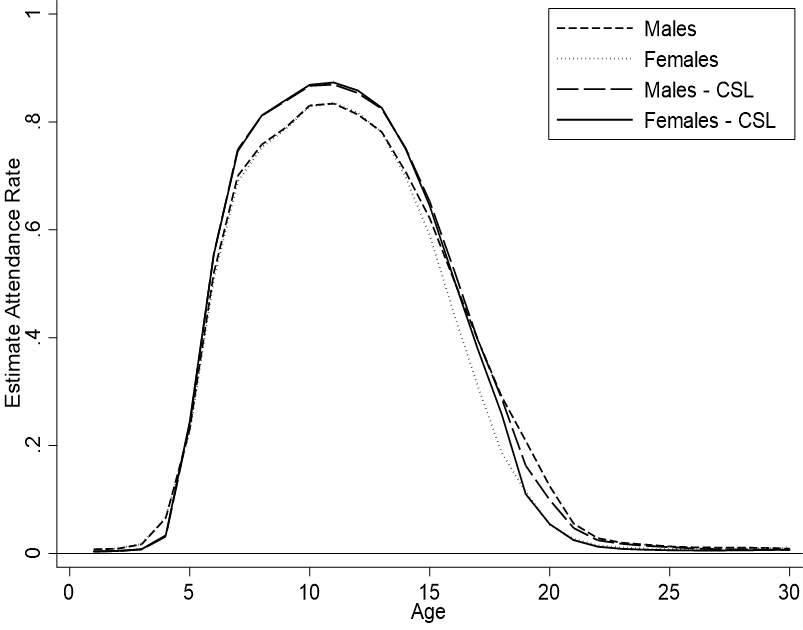

Personally, I will be presenting on the impact of compulsory school attendance laws on attendance. Today I just want to share and discuss a single graph that’s not my presentation.

Prior to my research, there was already a canon of existing literature on compulsory attendance legislation (CSL) and I’ve previously written on this blog about it (attendance, CSL, and differences by sex). However, the literature had some limitations. Authors examined smaller samples, ignored gender, or ignored different effects by age.

I examine full-count IPUMS data from the 1850-1910 US censuses of whites in order to investigate the so-far-omitted margins mentioned above. Here are some conclusions:

Prior to CSL:

Males and females attended school at similar rates until the age of 14.

After 14, women stopped attending school as much as men.

By the age of 18, the attendance gender gap was 10 percentage points.

After CSL

Male and female attendance increased from the ages of 6 to 14

Women began attending school more than prior to CSL until about age 18.

After the age of 18, women experienced no greater attendance than previously.

But, both sexes attended school less than prior to CSL for ages 5 and younger.

Men began attending school less after the age of 17.

CSL increased lifetime attendance for both males and females

Overall, examining the impact of CSL across many ages allows us to see when and not just whether people attended more school. Previous authors would say something like “CSL increased total years of school by about 5% on average”. For men, almost all of those gains were between the ages of 6 & 16. But women experienced greater attendance from ages 6 to 18.

Additionally, examining the data by age reveals that there was some intertemporal substitution. Once it became legally mandatory for children to attend school between the ages of 6 & 14, parents began sending their younger children to school at lower rates. Indeed – why invest in education for two or three early years of life if you’ll just have to send your children to school for another eight years anyway. Older boys dropped out of school at higher rates after CSL too. Essentially, the above figure became compressed horizontally. People ‘put in their time’, but then reduced investments at non-mandatory ages.

This reveals a shortcoming of the current literature, which focuses mostly on 14 year olds. By focusing on a popular age of attendance that was also compulsory, previous authors have missed the compensating fall in attendance at other ages. Granted, the life-time effect is still positive – but it’s attenuated by a richer picture. The picture reveals that individuals were not attending school by accident. Students or their parents had in mind an amount of educational investment for which they were aiming. When children were forced to attend school at particular ages, the attendance for other ages declined.

The recent debate over US inflation seems to be full of mood affiliation on both sides, where people start with a mood (“panic” or “don’t worry”) and then look for facts to fit the mood.

My natural temperament is “don’t worry” and that is what I’ve generally thought about inflation, but the latest number of 6.2% inflation over the last year is a bit concerning, and makes me glad the the Fed has announced they plan to taper off of new asset purchases. But overall I think people are still talking past each other, and I wish more people would answer these questions:

What will CPI inflation be over the next 12 months?

What specifically should the Fed do differently, if anything? How quickly should they taper and raise rates?

If you are currently thinking “panic” or “don’t worry”, what data could come in that would change your mind?

I’ll start with my answers, informed more by my gut than by quantitative models: my guess for inflation over the next year is 4-5%, the Fed has things about right but I’d say “tighten faster” rather than “tighten slower” if I had to pick. I expect inflation to slow noticeably in the spring as the economy transitions from the unusual boom in demand for goods back to demand for services after Christmas and the Delta wave, as more people get back to work and supply bottlenecks have time to work themselves out. I would start to get more seriously concerned if we see no slowing by June, or if market-based measures of inflation or NGDP projections start to move substantially (2pp) higher.

To the extent that I’ve been on the wrong side of this, I blame the cognitive bias I seem to fall prey to most often- mistaking reversed stupidity for intelligence. Just because lots of people make obviously incorrect predictions of hyperinflation doesn’t mean that inflation will be low.

No, 6.2% inflation per year is not in the same universe as hyperinflation (50% inflation per month)

*The usual disclaimer applies- my affiliation with the Fed gives me zero insider information about or influence over monetary policy and I don’t speak for them.