Where would you expect Federalism to occur? In other words, where would expect a government to devolve authority to a lower government. Importantly, this is different from freedom vs authoritarianism. The lower government might choose to be more or less free. For example, right now in Florida there is a state-wide constitutional amendment on the ballot that would enshrine each individual’s right to hunt and fish. Ignoring the particulars of what that means, it’s clearly a step toward centralizing policy rather than decentralizing it. Central governments can be strong and protect citizens, or they can strip us of rights. Either way, being small players and far-removed, it’s difficult for us to affect the policy decisions.

That concern is philosophical, however. Maybe my opinion shouldn’t matter (one could easily argue). Even as a matter of prudence, one-size-fits all sets a standard, but the standard may not be a good fit for every locality and circumstance. There is a trade-off between ease of navigating a uniform policy across the land and customized policies that are particular to local priorities. Given that Americans can vote, is there a way for us to think about when a policy will be (should be?) centralized vs decentralized?

There is a great case study by Strumpf & Oberholzer-Gee* on the matter of alcohol policy after the end of national prohibition. The US has a dizzying array of liquor laws across the country and even across states. Some states have a central policy of dry or wet, while others devolve the authority to lower governments. How should we think about that policy? What determines the policy of central versus devolved authority?

Are you better off than you were four years ago? That question was asked at the Presidential debate last night. But more importantly, we also got a massive amount of new data on income and poverty from Census yesterday. That data allows us to make that just that comparison, although somewhat imperfectly.

The Census data is excellent and detailed, but it’s annual data, meaning that the release yesterday only goes through 2023. We won’t have 2024 data for another year. Such is the nature of good data. (Note: I’ve tried to address this same question with more real-time data, such as average wages). Still, it’s a useful comparison to make. It’s especially useful right now because the new 2023 data on income are (for most categories) the highest ever with one exception: 4 years ago, in 2019.

A reasonable read of the data on income (whether we use households, families, or persons) is that in 2023 the median American was no better off than in 2019, after adjusting for inflation. In fact, they were probably slightly worse off. I fully expect this will no longer be true when we have 2024 data: it will certainly be above 4 years prior (2020) and likely above 2019 too (more on this below). But we can’t say that for sure right now.

So let’s do a comparison of “are you better off than 4 years ago” for recent Presidents that were up for reelection (treating 2024 as a reelection year for Biden-Harris too), using the 4-year comparison that would have been available at the time using real median family income. Notice that this data would be off by one year, but it’s what would have been known at the time of the election.

The headlines often read with the criminal threats that illegal/undocumented immigrants pose to the US native population. The story usually includes a heart wrenching and tragic story about a native minor who was harmed by an immigrant and a politician to help propose a solution. There’s also usually a number cited for how many such crimes happened in the most recent year with data. Stories like this are designed to provoke feelings – not to provoke thinkings.

First, the tragic story is probably not representative. Even if it is, the citation of a raw count of crimes is not communicative in a helpful way. Sometimes politicians will say something like “one victim of a crime by an illegal immigrant is too many”. But that seems like a silly argument to make *if* immigrants reduce the probability of being a victim of a crime.

I argue that (1) immigrants who commit crimes at a lower probability than the native population cause the native population to be safer and, counterintuitively, (2) immigrants who commit crimes at a *higher* probability than the native population cause the native population to be safer.

I’ve been traveling. Here are some things I noticed (on the internet, not on my travels). (On my travels I learned that rental golf carts are as fun as they look.)

2. This is a poastmodern election. “Campaigners use the internet medium to dunk on their opponents instead of offer solutions to problems.”

“deeply online left wing instagram women are meeting, for the first time ever, deeply online right wing twitter guys. both have developed intricate, sacred language foreign to the other. both are waging war they thought already won. fyi in case you’re wondering about the meltdown”

deeply online left wing instagram women are meeting, for the first time ever, deeply online right wing twitter guys. both have developed intricate, sacred language foreign to the other. both are waging war they thought already won. fyi in case you're wondering about the meltdown

4. This woman who gave up professional dancing and now has 8 kids.

I don’t think people understand just how insane it is that #ballerinafarm left julliard to start a family. They chose 12 female dancers a year to be accepted into that program. She would’ve gone so far.

One does wonder if the skills that get a person into Julliard relate to the ability to turn family into an Instagram sensation. Is this Ambitious Parenting?

Hannah Neeleman, the mom at Ballerina Farm, has told her story in what appears to be her own words here: https://ballerinafarm.com/pages/about-us Neeleman says that when she was living in Brazil, she would vacation at, “farms and ranches. A place where you could eat farm fresh cheeses and meats, learn about animals, watch chores being done, etc. We were hooked.” I’m tempted to say that it’s weird to say she was into watching other people do chores. But maybe the word “weird” just has lost all meaning after this week.

Jeremiah Johnson points out that, “It doesn’t matter that their farm isn’t a very productive farm, because the husband’s family founded JetBlue.” My take is that these are rich people who are taking a reality-show approach to their lives like wholesome Kardashians. The Neelemans are into watching people do farm chores. (Yes, they do chores themselves, too, but clearly a large professional staff runs the place.) Good for them. As I said at the beginning, I’m into renting golf carts now.

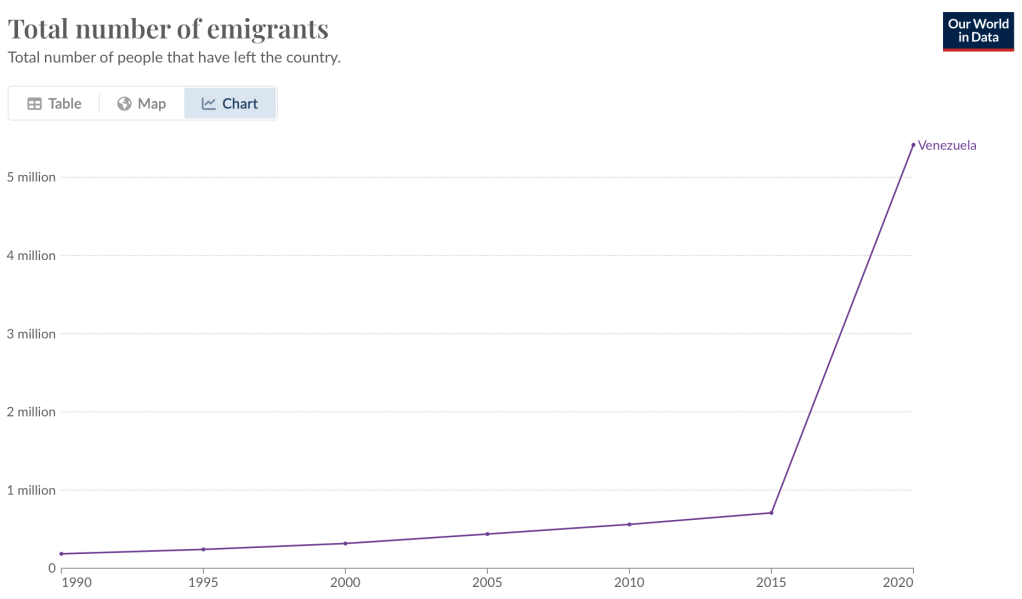

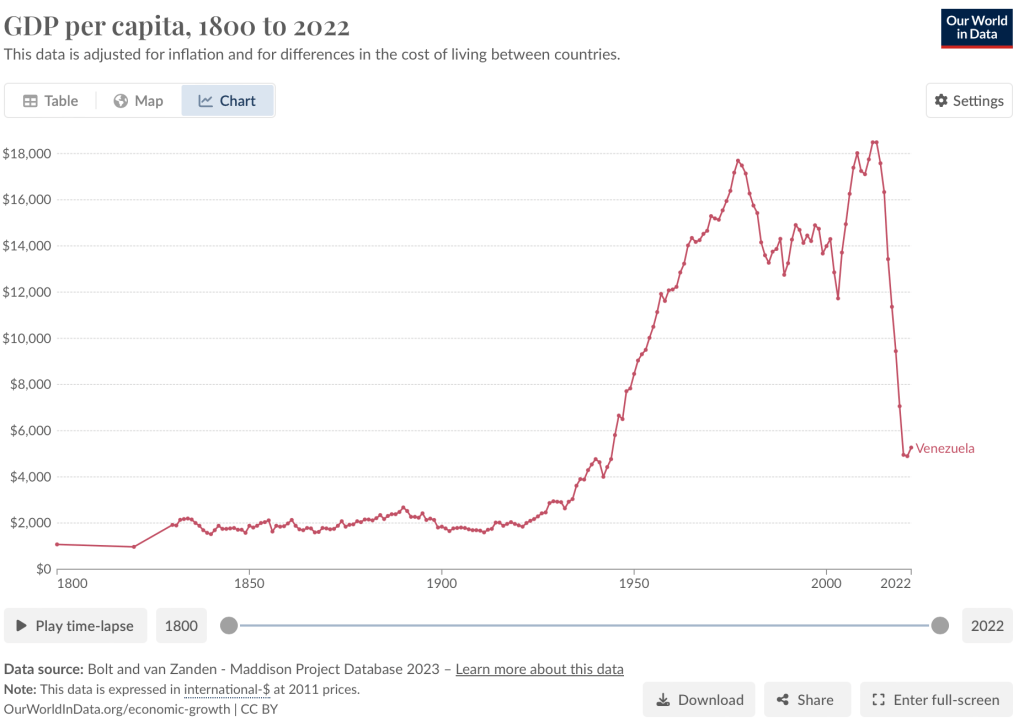

Venezuela held an election this week; President Maduro says he won, while the opposition and independent observers say he lost. Disputed elections like this are fairly common across the world, but where Venezuela really stands out is not how people vote at the ballot box- it is how they vote with their feet.

Reuters notes that “A Maduro win could spur more migration from Venezuela, once the continent’s wealthiest country, which in recent years has seen a third of its population leave.”

I don’t think we emphasize enough how crazy the scale of this is. After every US Presidential election, you hear some people who supported the losing side talk about leaving the country, but they almost never do. Leaving your home country behind is a dramatic step, one people only want to take if they think things are much better elsewhere. The US, even with a party you don’t like in power, has generally stayed a good place to live. The total number of Americans who have moved abroad for any reason (I would guess most feel more pulled by the host country rather than pushed by the US) is about 3 million. That is less than 1% of all Americans; by contrast more than 46 million people have immigrated to the US from other countries, and many more would come if we allowed it.

Even in poor countries, seeing anything like one third of the population leave is dramatic, especially when almost all the migration happens in only 10 years as in Venezuela:

Source. Note this only goes through 2020, and emigration has grown since

This makes Venezuela the largestrefugee crisis in the history of the Americas, and depending on how you count the partition of India, perhaps the largest refugee crisis in human history that was not triggered by an invasion or civil war.

Instead, it has been triggered by the Maduro regime choosing terrible policies that have needlessly and dramatically impoverished the country:

I hope that the Venezuelan government will soon come to represent the will of its people. I’m not sure how that is likely to happen, though I guess positive change is mostly likely to come from Venezuelans themselves (perhaps with help from Colombia and Brazil); when the US tries to play a bigger role we often make things worse. But what has happened in Venezuela for the past 10 years is clearly much worse than the “normal” bad economic policies and even democratic backsliding that we see elsewhere. People everywhere complain about election results and economic policy, but nowhere else have I seen such a case of people going past simple cheap talk, taking the very expensive step of voting against the regime with their feet.

One of my favorite economic journal articles is by Barry Weingast and has the short title “Market Preserving Federalism” (MPF). In this paper, Weingast lays out the conditions necessary for two tenuous equilibria: A) Federalism & B) Federalism that preserves a market economy. Given that we just celebrated Independence Day in the USA, it seems to me like a good opportunity to share some brief thoughts on this paper. I’ll speak in terms of the US for ease.

Weingast enumerates 5 features for MPF, starting with two that characterize a stable federalism:

F1) A hierarchy of governments, that is, at least “two levels of governments rule the same land and people,” each with a delineated scope of authority so that each level of government is autonomous in its own, well-defined sphere of political authority

F2) The autonomy of each government is institutionalized in a manner that makes federalism’s restrictions self-enforcing

Last Friday the Supreme Court overturned the doctrine of Chevron deference as part of its ruling in Loper Bright Enterprises v Raimondo. This might not have even been their most discussed ruling of the past week, but in my (non-lawyerly) opinion, there is a good chance it will be their most economically impactful ruling of the past decade. SCOTUSblog explains the basics:

the Supreme Court on Friday cut back sharply on the power of federal agencies to interpret the laws they administer and ruled that courts should rely on their own interpretation of ambiguous laws. The decision will likely have far-reaching effects across the country, from environmental regulation to healthcare costs.

By a vote of 6-3, the justices overruled their landmark 1984 decision in Chevron v. Natural Resources Defense Council, which gave rise to the doctrine known as the Chevron doctrine. Under that doctrine, if Congress has not directly addressed the question at the center of a dispute, a court was required to uphold the agency’s interpretation of the statute as long as it was reasonable. But in a 35-page ruling by Chief Justice John Roberts, the justices rejected that doctrine, calling it “fundamentally misguided.”

Justice Elena Kagan dissented, in an opinion joined by Justices Sonia Sotomayor and Ketanji Brown Jackson. Kagan predicted that Friday’s ruling “will cause a massive shock to the legal system.”

When the Supreme Court first issued its decision in the Chevron case more than 40 years ago, the decision was not necessarily regarded as a particularly consequential one. But in the years since then, it became one of the most important rulings on federal administrative law, cited by federal courts more than 18,000 times.

The most common reaction I’ve seen is that people expect this to reduce the power of executive branch agencies, both in general and relative to courts and businesses, likely resulting in deregulation. Thus those on the economic left have been mostly decrying the decisions, while free–marketers and businesspeoplehave mostly beencelebrating:

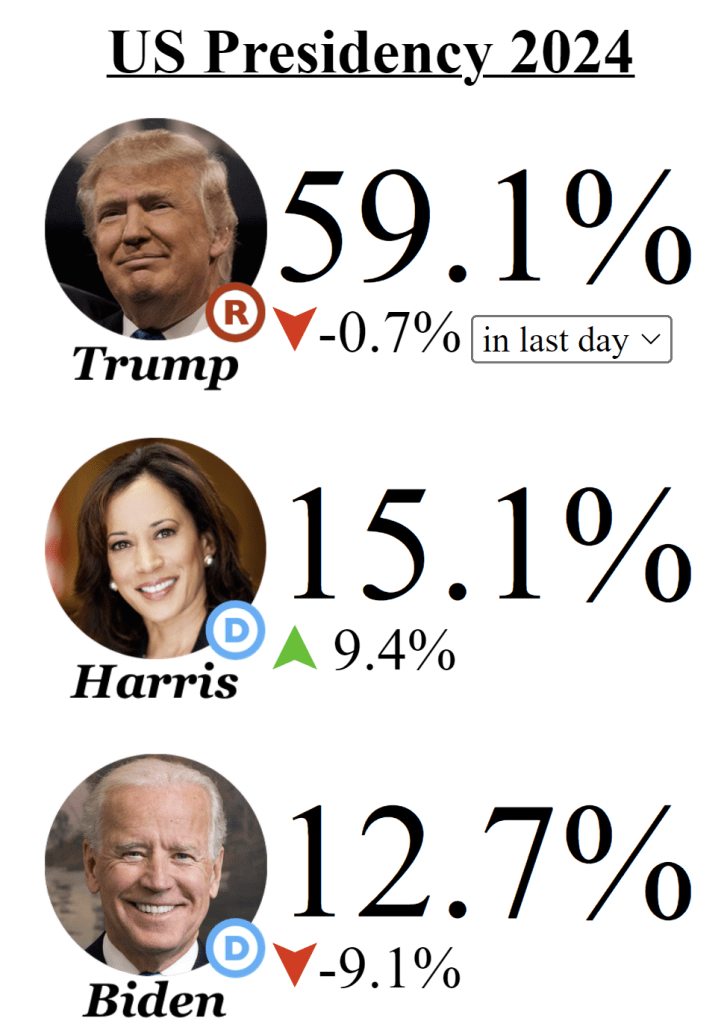

Back in January I encouraged you to follow the money in the Presidential race, by which I meant follow the betting markets. I suggested this was a good way to cut through the sometimes inaccuracy of polls, and the uncertainty of listening to any one expert or group of experts. Bettors in prediction markets can take all of these into account.

Lately of course the big question in the Presidential race is whether Biden will actually be the Democratic nominee. There is much uncertainty right now, and you will all kinds of predictions from experts, media quoting “inside sources,” and other such rumors. How are you, as a relatively uninformed outsider, supposed to know who to trust?

The answer again I will suggest is: watch the betting markets. And if you check the betting markets today (aggregated across multiple markets by EletionBettingOdds.com), you will see that Biden and Kamala Harris have roughly equal chances of becoming the next President (and Trump is about a 60% favorite):

As we enter election season, I can sympathize with those that want to ignore it as much as possible. But if you do want to follow it closely, here is my advice: talk is cheap, so follow the money.

And by money, I am not referring to campaign contributions. I mean prediction markets, where people are putting their money where their mouth is, rather than just making predictions based on their own intuition (or their own “model,” which is just a fancy intuition).

There are a number of betting markets online today, but a good aggregator of them is Election Betting Odds.

Companies and non-profit organizations tend to be managed day-to-day by a CEO, but are officially run by a board with the legal power to replace the CEO and make all manner of changes to the company. But last week saw two striking demonstrations that corporate boards’ actual power can be much weaker than it is on paper.

The big headlines, as well as our coverage, focused on the bizarre episode where OpenAI, the one of the hottest companies (technically, non-profits) of the year, fired their CEO Sam Altman. They said it was because he was not “consistently candid with the board”, but refused to elaborate on what they meant by this; they said a few things it was not but still not what really motivated them.

Technically it is their call and they don’t have to convince anyone else, but in practice their workers and other partners can all walk away if they dislike the board’s decisions enough, leaving the board in charge of an empty shell. This was starting to happen, with the vast majority of workers threatening to walk out if the board didn’t reverse their decision, and their partner Microsoft ready to poach Sam Altman and anyone else who left.

After burning through two interim CEOs who lasted two days each, the board brought back ousted CEO Sam Altman. Formally, the big change was board member Ilya Sutskever switching sides, but the blowback was enough to get several board members to resign and agree to being replaced by new members more favored by the workers (including, oddly, economist Larry Summers).

A similar story played out at IZA last week, though it mostly went under the radar outside of economics circles. IZA (aka the Institute for Labor Economics) is a German non-profit that runs the world’s largest organization of labor economists. While they have a few dozen direct employees, what makes them stand out is their network of affiliated researchers around the world, which I had hoped to join someday:

Our global research network ist the largest in labor economics. It consists of more than 2,000 experienced Research Fellows und young Research Affiliates from more than 450 research institutions in the field.

But as with OpenAI, the IZA board decided to get rid of their well-liked CEO. Here at least some of their reasons were clear: they lost their major funding source and so decided to merge IZA with another German research institute, briq. Their big misstep was choosing for the combined entity to be run by the the much-disliked head of the smaller, newer merger partner briq (Armin Falk), instead of the well-liked head of the larger partner IZA (Simon Jaeger). Like with OpenAI, hundreds of members of the organization (though in this case external affiliates not employees, and not a majority) threatened to quit if the board went through with their decision. Like with OpenAI, this informal power won out as Armin Falk backed off of his plan to become IZA CEO.

Each story has many important details I won’t go into, and many potential lessons. But I see three common lessons between them. First is the limits to formal power; the board rules the company, but a company is nothing without its people, and they can leave if they dislike the board enough. Second, and following directly from this, is that having a good board is important. Finally, workers can organize very rapidly in the internet age. At OpenAI nearly all its employees signed onto the resignation threat within two days, because the organizers could simply email everyone a Google Doc with the letter. Organizers of the IZA letter were able to get hundreds of affiliates to sign on the same way despite the affiliates being scattered all across the world. In both cases there was no formal union threatening a strike; it was the simple but powerful use of informal power: the voice and threatened exit of the people, organized and amplified through the internet.