As a dedicated supporter of Tottenham Hotspur Football Club, it is with much shame that I have referenced the anthem of Liverpool FC, but the sentiment implied by their club slogan is a powerful one.* To promise someone they will never have to suffer the torments of loneliness is to promise them a lifetime of riches. When we soft, vulnerable human beings find a source of community and support, we are loathe to give it up. Which is to say the promise of membership and threat of banishment are powerful means of solving collective action problems.

The promise of forever walking within columns of lockstep compatriots is a big part of why Gamestop (GME) went to the moon 🚀🚀🚀, but also why it came back down to earth. As Scott noted in his post, the story of the last, and most meteoric, stage of the Gamestop saga was the “short-squeeze”– short-sellers suddenly desperate to cover their positions found themselves needing more shares than existed, while the “unsophisticated” gamblers of r/wallstreetbets refused to sell their shares. Specifically, the large, but uncoordinated institutional short-position holders all pursued their independent self-interest, while the seemingly disaggregated redditors managed to solve their collective action problem. Which raises what, to me, is the most interesting question of the whole saga: if coordinating a short-squeeze is so lucrative, why doesn’t it happen more often? Put another way, why were a large number of strangers able to coordinate a complex financial gambit rarely pulled off by sophisticated institutional investors?

The answer, in part, is that they weren’t strangers. They may be anonymous to one another, absent recognition or connection in real life (IRL aka meatspace), but that doesn’t make them strangers. These men and women had built a community so deep they had their own (often incredibly offensive) language. Their own jokes. They had a culture and sources of status, going so far as to create their own within-group celebrities. And, absent any visible coordination, that culture had evolved in this moment toward a single idea: hold the stock. They were playing a massive prisoner’s dilemma game with each other. Can you form a group for the express purpose of creating a short-squeeze? Probably not – the very action of creating an identity around profit from financial speculation belies the prospect of building an identity valued more than pure profit by its members. That’s the rub – if you want to pull off a massive collective financial action, you’re going to have to build a group of people interested in financial collective action that nonetheless values the identity of the group above the profits of collective financial action. That’s what makes this Planet Money podcast about Gamestop so special– more than anyone anyone else, they seemed to understand that the absurdist emoji usage and language, the elaborate memes, the actual freaking sea-shanties, those weren’t just color for the story, they were the story. Hedge funds weren’t losing tens (hundreds?) of millions of dollars in a zero sum game to a bunch of idiots obsessed with chicken tender-centric memes and sea shanties. They were losing a millions of dollars in a zero sum game because of the memes and sea shanties.

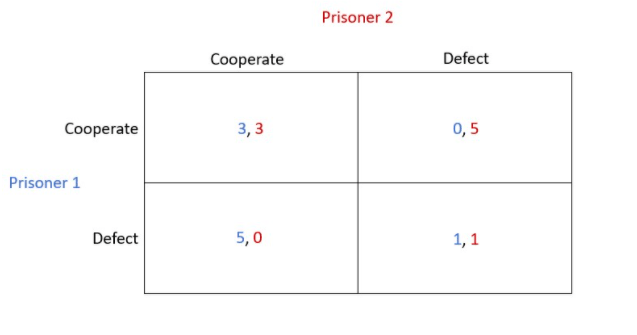

Put succinctly, at every stage leading up to and during the short-squeeze, each and every holder of Gamestock shares would have been better “defecting” on their r\wallstreetbets comrades-in-arms. Yes, the group is better off if everyone holds, but everyone knows the incentives faced by everyone else, which creates a seemingly irresistible economic gravity of self-interest (defect, defect). So how do we solve these collective action problems? Well, first and foremost, we change the payoffs. That’s what we do in successful families, mafias, and religious groups. It’s what we fail to do in our misfiring coups, cooperatives, and communes.

Yes, your bank account balance will increment upwards if you defect and sell your stock. But that also means you’re no longer a true Son of Gondor. Sure, no one else on the subreddit knows it, but you’ll know it. You’ll know it in your cold, lonely, traitorous heart. Sure, you can use the words and participate in the jokes, but will you ever know the same sense of fellow-feeling within the community as you knew before. That’s a real cost. Is it worth cashing in $5000 in profit a week early, especially knowing it might be worth more next week? Remember – the benefit of group identity doesn’t have to be greater than the profit at hand, it only has to be greater than the risk holding the stock bears for your future profit. Combined with a little motivated reasoning, and it quickly becomes clear how a community, formed independent of profit-via-collective-action, now suddenly becomes an engine of pro-social decision-making sufficient to create an existential threat to any institution over-leveraged on a short position.

The same payoff matrix, however, also demonstrates that a short-squeeze built around a group identity is living on borrowed time. With every short position that gets closed out, the price climbs both higher and closer to its (actually) inevitable peak. There are a finite number of short positions, and there is a finite number of days their share lenders will allow them to hold out, all of which mean a peak will be reached, after that point the price will begin to rapidly decline. Which all means that as the price rises the risk to holding also rises, both of which are increasing the opportunity costs of holding the stock, shifting the payoffs back to a classic Prisoner’s Dilemma. Sure, your group identity might be worth $5K, or even $50K, but there’s a point at which anonymous community is dominated by the prospect of material wealth. I’m not saying you can buy true friends, but eventually you can buy something that offers a close substitute for anonymous friends. Or an island.

*I mean, I personally believe “To Dare is to Do” is a far smarter and sexier slogan.