Predicting elections is hard. Poll aggregators and prediction markets can help. Many of the usual suspects like FiveThiryEight and PredictIt aren’t covering Sunday’s election in Turkey, partly due to their ownissues, and partly because US organizations often ignore foreign elections. But we do have several good predictors to consider, and they all list opposition candidate Kiliçdaroglu as a slight favorite.

Polymarket is most optimistic for the opposition, giving them a 67% chance. British betting site Smarkets gives them a 61% chance. Play-money site Manifold Markets gives them 56%. Finally, no-money prediction site Metaculus gives a 60% chance that the opposition wins, and a 79% chance that Erdogan leaves office if he loses the election. I’m not sure how the count the Swift Centre, a small closed panel of forecasters, but they are the exception in seeing Erdogan as a slight favorite.

My economist’s instinct is to trust the real-money markets more here, although Manifold and Metaculus outperformed them in the 2022 US midterms. The usual bias is to predict a win for the candidate you like more (which for Westerners on these markets means betting against Erdogan), and have real money on the line can help counteract this. On the other hand, some might use betting markets as a hedge and bet on the outcome they don’t want. In this case the betting markets are slightly more favorable to the opposition, but the gap is small.

Of course, the biggest real-money markets are those that don’t ask directly about the election: the markets for Turkish stocks and bonds. These have generally performed well in the past year as the opposition’s chances have risen, which may indicate that markets think a new Prime Minister with more conventional economic views will get inflation under control.

Economics involves human beings making decisions. Where there are humans, drama is never absent. Hence, somewhere in the broader financial sphere, there is always some drama. The chart below displays gyrations in the exchange rate of the Turkish lira which may be fairly characterized as “dramatic”. This chart shows the lira-per-dollar exchange rate over the past six months; a higher number here means lower lira valuation.

Foreign Exchange Market Prices, Turkish Lira per Dollar. Source: TradingView.com

What is going on here? Why the spike up in November/December, followed by an even more sudden drop?

As usual, loss of value in foreign exchange goes hand in hand with domestic inflation. Inflation within Turkey for the month of December was reported to 36% on an annualized basis. Now, an orthodox economic response to runaway inflation includes raising interest rates. Higher interest rates tend to make a currency more valuable. Higher interest rates encourage people to hold onto their currency, since they are rewarded by interest on their savings. Conversely, low interest rates, especially when coupled with inflation, motivates people to spend down their money before it loses more value. In the case of emerging market countries like Turkey, high inflation/low interest drives people to exchange their local currency for more stable foreign currencies, like dollars or euros (or crypto stablecoins like Tether).

But Turkey is Turkey, and Turkey is run by the authoritarian President Erdogan. He has economic views which might most charitably characterized as “heterodox”. Erdogan claims that high interest rates actually cause inflation. His views may be influenced by the prohibition on charging interest in classic Islamic practice. The Turkish president has stated, “My belief is that interest rates are the mother of all evils. Interest rates are the cause of inflation. Inflation is a result, not a cause. We need to push down interest rates.” President Erdogan has sacked numerous treasury officials who disagreed with him, and pressured the central bank to implement four interest rates cuts in the last four months of 2021.

It seems he hopes to stimulate enough internal growth to paper over any other problems. I think there could be some merit to that notion, but the current inflation level is toxically high. Lower- and middle-class Turks find it hard to purchase necessities.

Lowering the value of your currency to make your exports more attractive has been practiced successfully by various Asian nations, but Turkey is too exposed to foreign exchange to weather such a huge drop in the value of the lira. A large part of Turkey’s recent economic growth has been funded by foreign investors, and that may dry up because of the currency instability. Turkey is dependent on imports for many essentials, including all of its energy needs, so imports have become much more expensive for Turks as their currency depreciates. Furthermore, because of the fluctuating value of the local currency, many loans are denominated in dollars or euros. This makes it burdensome for borrowers to keep up payments of interest and principal, when these foreign currencies have become more expensive.

Modern currencies have essentially no intrinsic value. Money is a big confidence game. A shopkeeper will take my dollar bill in exchange for some candy, because he is confident that some other party will in turn accept that dollar bill in exchange for something else of value. If confidence in a currency collapses, so does its exchange value.

Foreign creditors and domestic Turkish consumers were becoming more and more nervous about the prospects for the lira in late 2021, as inflation was fueling further inflationary expectation. It crashed to a record high exchange rate of 13.44 against the dollar on November 23 after the Turkish leader insisted that rate cuts would continue.

Things really started getting out of control in mid-December. Turks frantically ditched their currency in exchange for euros and dollars, which led to further devaluation of the lira. On December 21st, however, the Turkish government unleashed an innovative initiative. They offered to backstop the value of the lira deposits of Turkish residents, as long as those deposits were held in lira for a certain period of time. Besides offering interest on the deposits, the offer was to compensate depositors for any loss in value against the dollar. The intent was to motivate residents to keep their lira as lira.

Turkey’s new Finance Minister Nureddin Nebati has no real finance background; his main qualification for office appears to be a willingness to do what his boss wants. When Nebati was asked to give details of this initiative, he reportedly answered thus: “”I won’t give a number now. Can you look into my eyes? What do you see?… The economy is the sparkle in the eyes.” Hmm.

President Erdogan has said he is protecting the country’s economy from attacks by “foreign financial tools that can disrupt the financial system.” Western economists are not impressed. Market strategist Timothy Ash commented, “ More complete and utter rubbish from Erdogan…Foreign institutional investors don’t want to invest in Turkey because of the absolutely crazy monetary policy settings imposed by Erdogan.”

At any rate, this unusual measure, combined with old-fashioned central bank intervention (the Turkish central bank is believed to have used some 10 billion dollars’ worth of its foreign reserves to buy lira), seemed to stem the immediate panic. Within a day, the exchange rate thudded down from about 18 to about 13, which is roughly the level today.

It has been pointed out that it simply is not feasible for the government to backstop all relevant bank deposits against a huge currency depreciation; the Turkish government and central bank would burn through all their foreign reserves, and have to resort to printing ever more worthless lira. However, sometimes the mere promise of such a guarantee (whether or not it is practical) is enough to restore some measure of confidence, which in turn means that the currency will not collapse and thus the resources of the central bank will not be put to the test. As we said, confidence is what it is all about. We will see how this plays out.

The 2007-9 Financial Crisis turned Iceland into a major tourist destination, as a newly cheap currency combined with affordable flights and natural beauty. For anyone with plenty of time and a moderate amount of money, chasing the newly-cheap destination seems like a good travel strategy.

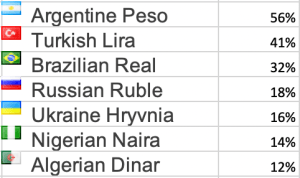

Since January 2020, here are the countries where the US dollar has gained the most vs the local currency: