Inflation is colloquially defined as, “Too much money chasing too few goods (and services)”. Supply chain constraints get talked about, and these are widely blamed for the inflation we are seeing. Of course, supply limitations play into inflation, but to focus on them is to miss the elephant in room. The primary driver of this inflation is not “too few goods”, but “too much money.”

Such is the thesis of a widely circulated article by Ray Dalio’s investing firm Bridgewater Associates, “It’s Mostly a Demand Shock, Not a Supply Shock, and It’s Everywhere.” The point is summarized:

While the headlines tend to focus on the micro elements of the supply shock (the LA port, coal in China, natural gas in Europe, semiconductors globally, truckers in the UK, etc.), this perspective largely misses the macro cause that is likely to persist and for which there is no idiosyncratic solution. This is not, by and large, a pandemic-related supply problem: as we’ll show, supply of almost everything is at all-time highs. Rather, this is mostly an MP3-driven upward demand shock. [emphases in the original]

In Bridgewater’s terminology, “MP3” is “Monetary Policy #3”, and refers to massive deficit spending combined with central bank quantitative easing. We saw this implemented in 2020-2021 when the federal government pumped out trillions of dollars of stimulus payments and enhanced unemployment benefits, and the Fed instantly soaked up the bonds that were issued to pay for these trillions. This fed/Fed combo amounts to simply printing money on an enormous scale.

Those trillions of dollars funded a huge surge in durable goods purchases. By late 2021 the supply of these goods was well above 2019 (pre-COVID) levels, and even above normal growth trendlines. However, the supply and transport systems simply could not grow fast enough to accommodate this insatiable demand. Charts below substantiate this. To focus on supply chain bottlenecks of themselves is misleading. The primary driver for this inflation has been the trillions of dollars of federal largesse. The Fed knows all this, obviously, but Jay Powell (the Chief Enabler of this deficit spending) would likely not have been reappointed if he spoke too directly about the cause of this inflation. Hence the endless prattle about supply chains.

This is not to say that the federal largesse was right or wrong, too little or too much. We are simply trying to get the causes and effects straight here.

With deficit spending down to more “normal” (still high) levels, and supply creaking upward, will inflation now taper off by itself? I don’t know. It seems by now we all must have replaced our TVs with even bigger TVs twice over, yet the consuming boom continues. There has been a permanent step down in willing workers, since many of the resignations over the past year have been over age 55 folks, who may be permanently retiring. The tight labor market will lead to higher wages. Expectations for continued inflation tend to beget more inflation, as workers who get an 8% raise this year may not be satisfied going back to the old 3% annual raises.

With inflation raging on and on, well above its nominal 2% target, the Fed is finally being shamed into action. Tapering of QE is underway, and talk of raising short term rates may actually translate into action. Last time the Fed tried to raise rates (late 2018), the stock market puked and the Fed beat a hasty retreat. Time will tell how it plays out this time.

Here are some charts showing what is the primary driver here:

The two charts above, showing China production well above trendline, are from the Bridgewater article. The charts below are from an article by Rida Morwa on Seeking Alpha with the rather pointed title, Inflation & The Great Supply Lie.

Gross outputs for U.S. Industries are well above pre-COVID levels:

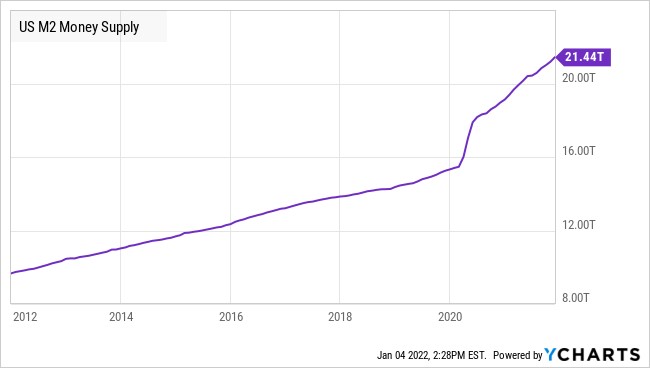

Thanks to COVID-related deficit spending and related QE, the money supply has exploded, and much of that ended up in consumers’ pockets:

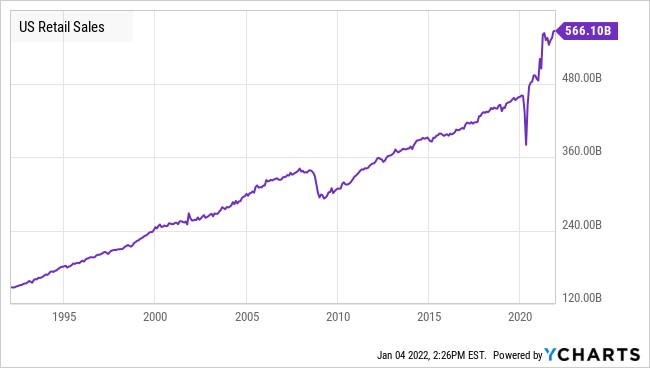

…and hence retail sales have surged, again showing demand well above trendline:

Reblogged this on Utopia, you are standing in it!.

LikeLike

People bought goods because they were locked down and couldn’t go out to purchase services.

We could see a reversion later as the covid lockdown finally ends.

LikeLike