Where is that recession that pundits have been predicting for over a year now? The suspense is killing me. Despite savage hikes in interest rates that have led to a collapse in regional banks and in home buying, the economy just keeps chugging along, and inflation continues to run way above the targeted 2% level. What’s going on?

An article I just read on the Seeking Alpha applied finance website points to three interrelated factors. I will cite and credit the author (whose moniker is “Long-Short Manager”; he runs a couple of investment funds) for the content here, while noting that I agree with his points based on other reading. These points all relate to ongoing strong financial position of the (average) American consumer, who mainly drives the spending in our economy.

( 1 ) Reduced Debt Service

The article notes:

The graph above shows household debt payments as a percent of disposable personal income going back to 2000. Since peaking at 13% right before the financial crisis, it steadily improved to 2020, with a subsequent large drop due primarily to lowered mortgage rates (usually the largest debt obligation of a household). It is the lowest it has been this century.

(Although mortgage rates have jumped in the past year, most existing mortgages were taken out pre-2023, when interest rates had been pushed to near zero by the Fed.)

( 2 ) Robust Wage Growth

The next graph from the Atlanta Fed’s wage tracker (note that the methodology used by this tracker is fundamentally different from the Fed’s employment cost index …) shows that job hoppers on average are making about 3% more than core inflation (call that 5%) whereas the average stayer is making a half percent over core inflation. This is allowing people to catch up for the year that they got behind on inflation.

Likewise, the author notes that although job quits have come down in the past year, they remain well above re-COVID levels.

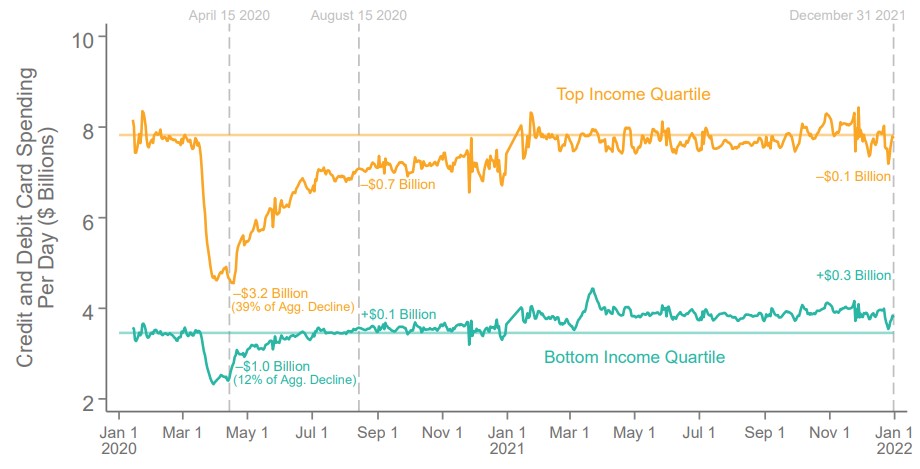

( 3 ) We Are Still Spending Down Gigantic Pandemic Stimulus Windfall

As we have noted earlier, the government/Fed combination dumped some $4 trillion into our collective pockets in 2020-2021. This includes enhanced unemployment benefits as well as direct stimulus payments, at a time when much of our normal spending (e.g., on travel, sports, commuting, etc.) was curtailed. We are still spending down these excess savings at a good clip, which seems to be a fundamental driver of the currently robust economy:

The last figure on the consumer shows how excess savings (defined as the extra savings consumers accumulated during the pandemic due to fiscal transfers and reduced spending due to lockdowns) has evolved – it should now be around 700 billion and ought to be fully depleted by the end of the year – leaving the consumer still with the lowest debt service ratios of the century and wages caught up with inflation. If you are wondering why we haven’t had a recession despite economists saying we will have it within 6 months for about 12 months now, these charts should tell you why. The tailwind from consumers has exceeded any headwinds from reduced investment due to higher rates.

And there you have it.