I am not worried about inflation and I’m not worried about the total spending in the economy. As I’ve said previously, total spending is on track with the pre-pandemic trend and, I think, that helped us experience the briefest recession in US history. When output growth declines below trend, we face higher prices or lower incomes. The former causes inflation, the latter causes large-scale defaults. Looking at the historical record, I’m for more concerned about the latter.

I do, however, want to call special attention to the composition of the Fed’s balance sheets. Specifically, its Mortgage Backed Security (MBS) assets. Having learned from the 2008 recession, the Fed was very intent on maintaining a stable and liquid housing market. Purchasing MBS is one way that it maintained that stability. Its total MBS holdings almost doubled from March of 2020 to December of 2021 to $2.6 trillion. Should we be concerned?

At first, a doubling sounds scary. And, anything with the word ‘trillion’ is also scary. Even the graph below looks a little scary. MBS holdings by the Fed jumped and have continued to increase at about a constant rate. Is the housing market just being supported by government financing? What happens when the Fed decides to exit the market?

Luckily for us, there is precedent for Fed MBS tapering. The graph below is in log units and reflects that a similar acceleration in MBS purchases occurred in 2013. Fed net purchases were practically zero by 2015 and total MBS assets owned by the Fed were even falling by 2018. Do you remember the recession that we had in 2013 when the Fed stopped buying more MBS’s? Wasn’t 2018-2019 a rough time for the economy when the Fed started reducing its MBS holdings? No. We experienced a recession in neither 2013 nor 2018. Financial stress was low and RGDP growth was unexceptional.

Although there was no macroeconomic disruption, what about the residential sector performance during those times? Here is a worrisome proposed chain of causation:

- Relative to a heavier MBS balance sheet, the Fed reducing its holdings increases supply on the MBS market.

- This means that the return on creating new MBS’s falls (the price rises).

- A lower return on MBS’s means that there is less demand from the financial sector for new loans from loan originators.

- A tighter secondary market for mortgages decreases the eagerness with which banks lend to individuals.

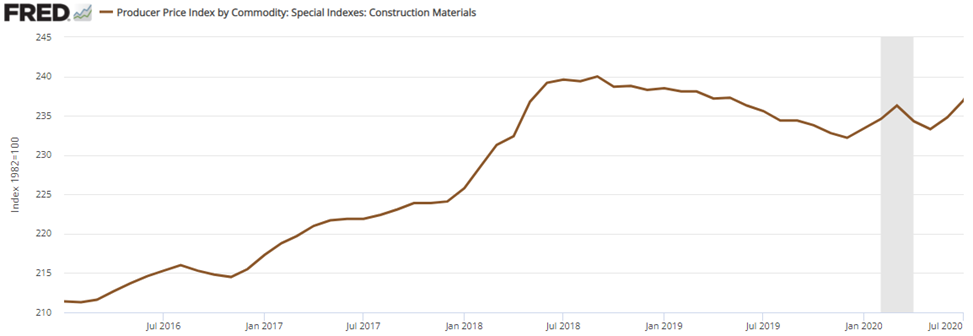

- Fewer loans to individuals puts downward pressure on the demand for houses and on the price of the associated construction materials.

The data fits this story, but without major disruption.

Less eager lenders went hand-in-hand with higher mortgage rates and less residential construction spending. The substitution effect pushed more real-estate lending and spending to the commercial side. Whereas residential spending was almost the same in late 2019 as it was in early 2018, commercial real-estate spending rose 13% over the same time period.

But, importantly in the story, the income effect of a Fed disruption should have been negative, resulting in less total spending and lower construction material prices. And that’s not what happened. Total Construction spending rose and so did construction material prices. Both of these are the opposite of what we would expect if the Fed had caused disruption in the housing construction sector due to its MBS holding changes. Spending on residential construction fell understandably. But spending on commercial construction and the price of construction materials rose.

My point is that you should not listen to the hysteria.

The Fed has a variety of assets on its balance sheet and it pays special attention to the residential construction sector. Do you think that there is a residential asset bubble? Ok. Now you have to address whether the high prices are due to demand or supply. Do you suspect that the Fed unloading its MBS’s will result a popped bubble and maybe even contagion? It’s ok – you’re allowed to think that. But the most recent example of the Fed doing that didn’t result in either a macroeconomic crisis or substantial disruption in the construction markets.

The Fed has a track record and it has a reputation that serves as valuable information concerning its current and prospective activities. The next time that someone gets hysterical about Fed involvement in the housing sector, ask them what happened last time? Odds are that they don’t know. Maybe that information doesn’t matter for their opinion. You should value their opinion accordingly.

This article was interesting and makes me think that the Fed buying MBS is similar to what Fannie and Freddie did? I understand the concerns re the Housing Market but is the Fed now standing behind the mortgage market to such an extent that without MBS purchases by the Fed the Housing Market couldn’t function commercially?

LikeLike

Fed share of outstanding MBS market:

2018: 1.76/9.7= 18.3%

2021: 2.5/11.9= 21.0% (as of September 2021)

It’s very likely higher since then. At 25% I would be concerned. 30% would be somewhat uncharted territory

BTW: A lot of the decline in the balance sheet was probably due to security maturation rather than sales. So the structure of the securities matters to a degree.

LikeLike

“downward pressure on the demand for houses and on the price of the associated construction materials” sounds like just what we need

LikeLike