This is my last post in a series that uses the AS-AD model to describe US consumption during and after the Covid-19 recession. I wrote about US consumption’s broad categories, services, and non-durables. This last one addresses durable consumption.

During the week of thanksgiving in 2020, our thirteen-year-old microwave bit the dust. NBD, I thought. Microwaves are cheap, and I’m willing to spend a little more in order to get one that I think will be of better quality (GE, *cough*-*cough*). So, I filtered through the models on multiple websites and found the right size, brand, and wattage. No matter the retailer, at checkout I learned that regardless of price, I’d be waiting a good two months before my new, entirely standard, and unexceptional microwave oven would arrive. I’d have to wait until the end of January of 2021.

¡Que Ridiculo!

And I wasn’t the only one facing a delay. Stories abounded of people facing 6-month waits for refrigerators and ovens. Sure, stores seemed to be out of some basic foods a bit more often. But supply chain disruptions really gained salience when people couldn’t purchase a new kitchen device when their old one unexpectedly died. Compared to others, I was lucky that it was only two months and that it was only a microwave (we borrowed someone else’s spare until the new one arrived).

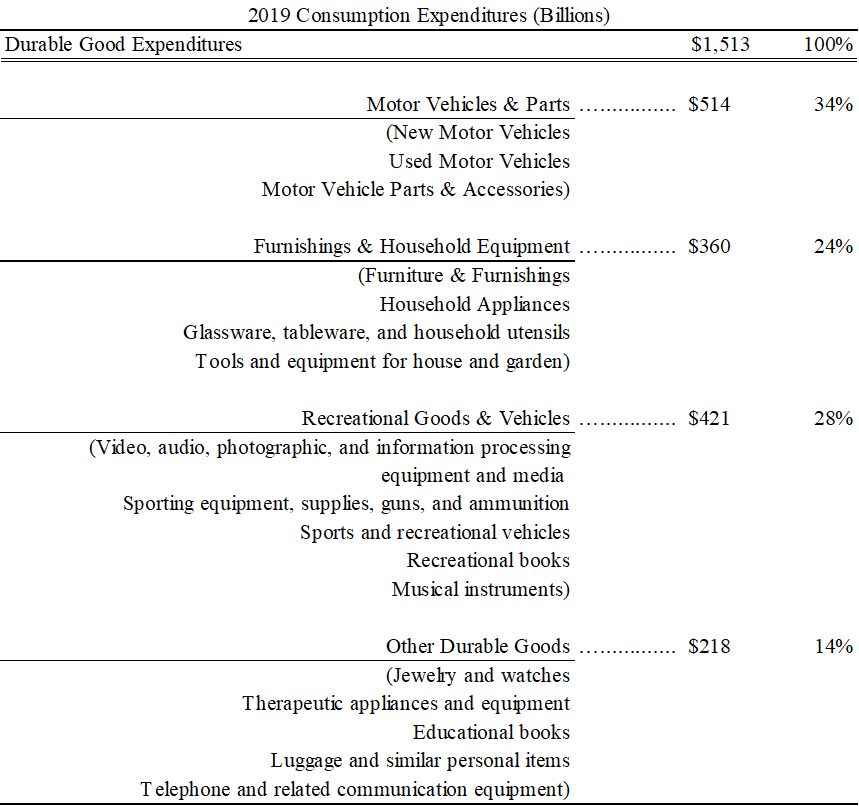

As of 2019, durable goods composed only 10.5% of all US consumption expenditures. Below is the break-down of the largest components. Durables are a bit different from the other consumption categories in that the constituent components are much more diverse. Although the categories of goods are divided into three large categories and ‘other’ durables, there is a lot of diversity in those three sets.

First, I must share a moment of humility. I teach principles of macroeconomics, and I had no idea that some of these things were included in consumer durables. Textbooks? Guns? Luggage? Really? It’s never come up before, but this is a way more interesting list than the household appliances list that I usually provide to students.

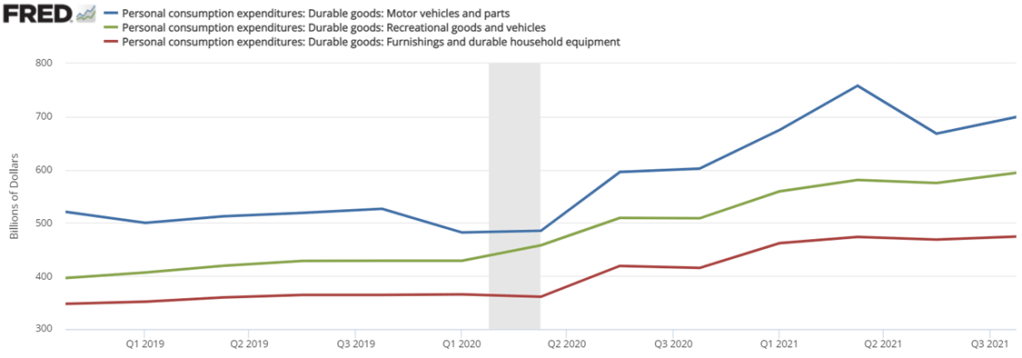

Regardless, let’s first get a handle on what happened to spending in the big three areas. Spending on vehicles fell by a hefty 8.5% in 2020Q1, spending on furnishings and household equipment by 1.2% in 2020Q2, and spending on recreational goods and vehicles never fell at all. But, as we know, spending is made up of both quantities and prices. So let’s delve in.

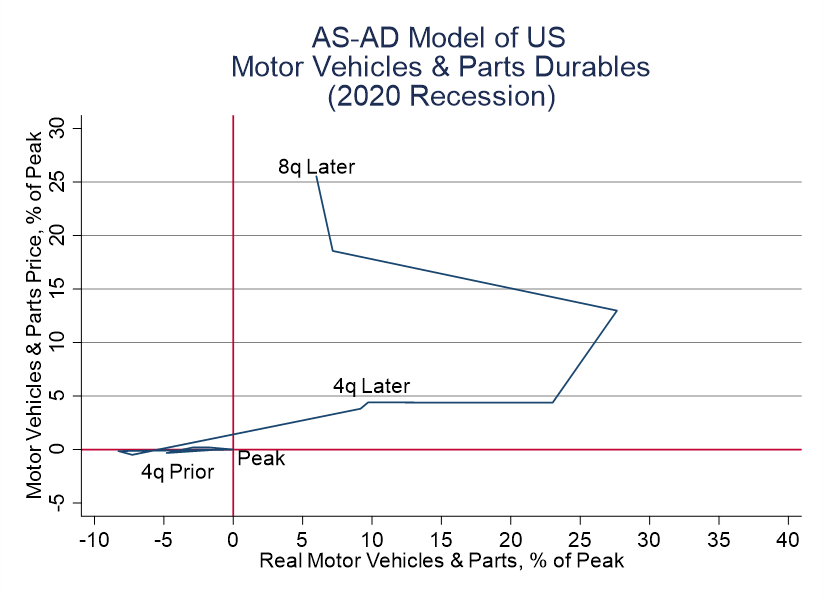

Below is the AS-AD graph for vehicles and parts. We can clearly see the decline in demand for vehicles and we can easily imagine the practically flat SRAS through 2020Q2. But both prices and quantities were up through 2021Q2 reflecting the increasing demand for these goods. Immediately at the start of the pandemic, people were wary of their incomes and were going to be staying home a lot anyway, so demand for cars was weak. But, as we learned more and built social norms around Covid-19, being by yourself or with your family in a vehicle – maybe on your way to an outdoor event – became more popular. I haven’t examined the commercial automotive data, but I’d be willing to bet that personal motor vehicles rebounded much more strongly that did large passenger van or bus production. Regardless, we can see the increase in inflation expectations as the price proceeded higher and output fell closer to its pre-recession peak.

As much as there has been talk about supply chain disruption and a shortages of semi-conductors, the aggregate data don’t show it. In total, we’ve been purchasing more cars and have more than made up for the two recessionary quarters of low real purchases. It’s true that prices are up by 25%. But that’s what happens when spending rises by 33% in the course of two years.

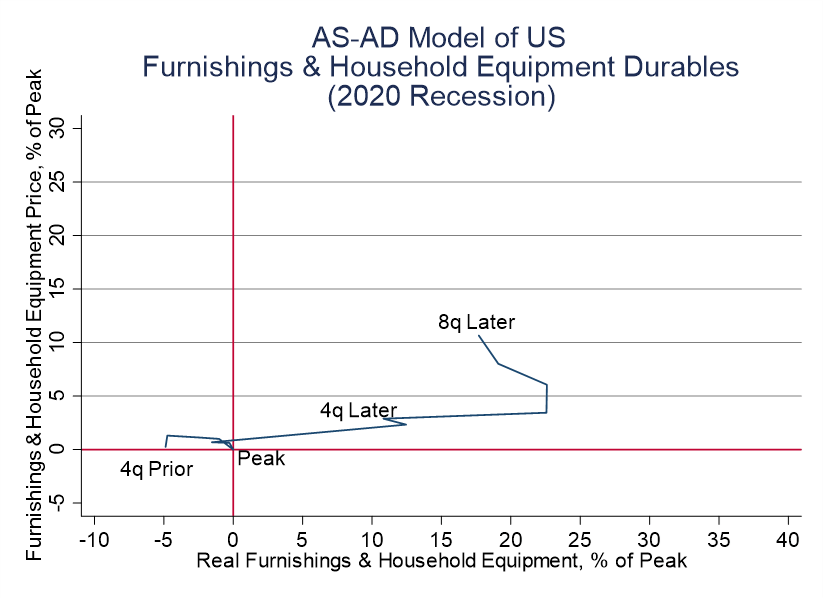

The story is similar for furnishings and household equipment, but to a less extreme degree. There was an immediate stutter at the outset of the pandemic, then explosive demand. That demand initially resulted in greater quantities produced, but has been increasingly composed of higher prices and retrenching output. But, it’s worth noting that the initial stutter does appear to be supply-side related. Where do we get our sectional couches and clothes dyers anyway? From the delivery men, of course! But from March through June of 2020, we weren’t so keen on having strangers enter our homes and posing a threat of contagion. The rise in prices and decline in real consumption for these goods was a blip, and a small one at that.

This is weird, right? How is it that we were hearing pervasive stories of shortages and long wait times if home furnishings and equipment were selling like nobody’s business? Well, the answer is in the question. Business was great. Firms couldn’t keep kitchen appliances from walking out the door with happy customers. It wasn’t that Covid-19 mucked up the supply chains. It was your fellow home-dwelling, stimulus check-receiving, home-improving brethren that strained the supply chains with greater demand.

How is it that we’re talking about electronics shortages for cars, and yet nobody is talking about the shortage of other electronic equipment? We’ve all seen the inside of a computer, a tv, or stared into the whirling wheels of a VCR. Don’t those have semiconductors? Why haven’t there been news stories about the booming prices and shortages of laptops and flat-screen TVs? Indeed, delving into the data reveals that eight quarters after the pre-recession business cycle peak, real TV consumption was up 24% and TV prices were down 2.5%. (I’m not making this up. The official government data is here for everyone to see.)

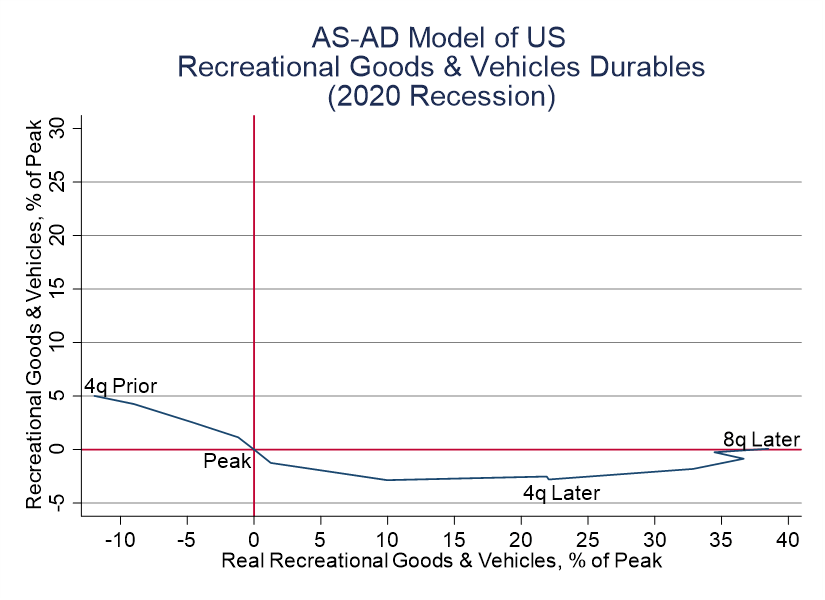

The broader category of recreational goods and vehicles sketch the same story. Demand was and is increasing. However, unlike with vehicles and home furnishings, prices declined. People began buying on the order of 50% more computers, video & audio equipment, and recreational vehicles such as motorcycles and jet skis. That’s an inflation adjusted number folks!

Increasing output and falling prices is consistent with a positive supply shock. I wish that I knew the specifics on this one, but I just don’t. Maybe manufacturers had a bunch of unutilized capacity that they were happy to ramp up (unlikely)? Or maybe several producers in this space saw the remote-work writing on the wall, decided that it was now or never and that they’d lose market share if they didn’t take advantage of the surging demand for home video and audio accoutrements. Eight quarters after the pre-recession business cycle peak, and real recreational goods and vehicles consumption was up 38%. However, I don’t want to paint too rosy a picture. In the same time period, prices rose by a cumulative 0.07%.

The first two graphs above show us a brief negative demand shock, followed by an unambiguously positive and large demand shock. The 3rd graph shows us the same positive demand shock AND a positive supply shock.

At this point, I feel like I’m a little bit crazy. Is no one else examining the data? Am I missing something fundamental? By now, I’m quite convinced that our supply chain issues… Which affected goods and not services… Which experienced greater demand during the recession and recovery… WERE NOT A RESULT of NEGATIVE SUPPLY SHOCKS. We were/are waiting for goods to be in stock, not because goods are slow to arrive. But because our neighbors keep clearing the shelves with their purchases.

” It wasn’t that Covid-19 mucked up the supply chains. It was your fellow home-dwelling, stimulus check-receiving, home-improving brethren that strained the supply chains with greater demand.” – – yup!

LikeLike

“But, as we learned more and built social norms around Covid-19”

“But, as we learned more and stopped being afraid of Covid-19”

fify

LikeLike

You don’t mention the container ships back up in LA or Shanghai.

LikeLike

That’s right. The traffic jams in and of themselves do not exclude either explanation (lower supply or greater demand). But, that there is more traffic and no fewer ports or ships is consistent with greater demand. The post was long enough, so I prioritized.

LikeLike