In my previous post, I decomposed consumer expenditures to figure out which service sectors experienced the largest supply-side disruptions due to Covid-19. I illustrated that transportation & recreation services were the only consumer service to experience substantial and persistent supply shocks. Health, food, and accommodation services also experienced supply shocks, but quickly rebounded. Housing, utility, and financial services experienced no supply disruptions whatsoever.

What about non-durables?

Total consumption spending is the largest category of spending in our economy and is composed of services, durable goods, and non-durables. Services are the largest portion and durable goods compose the smallest portion. So, while there were plenty of stories during the Covid-19 pandemic about months-long delivery times for durables, they did not constitute the typical experience for most consumption.

Even though it’s not the largest category, many people think of non-durables when they think of consumption. Below is the break-down of non-durable spending in 2019. The largest singular category of non-durable spending was for food and beverages, followed by pharmaceuticals & medical products, clothing & shoes, and gasoline and other energy goods. Clearly, the larger the proportion that each of these items composes of an individual household budget, the more significant the welfare implications of price changes.

Further, just about everybody agrees by now that the current inflation is largely demand-driven rather than being driven by supply chain issues. My previous two posts and the current post do not imply that we can reduce inflation by targeting policy toward particular sectors. NGDP is the policy outcome that determines price levels. In these posts I identify which sectors of the economy experienced supply shocks due to the pandemic and the pandemic responses.

Non-durable goods differ from services insofar as inputs are harder to allocate. Employee hours can be increased and those hours have a very quick effect on service output. Non-Durables, on the other hand, require moving physical goods from the source of production. In the US we have fewer goods producers, and more consolidated supply networks. Think about the distribution of air conditioning repairmen in the US vs candy bar producers. Service production is WAY more decentralized and able to draw upon remote provision or distributed methods of transportation. Frozen foods, on the other hand, require a refrigerator truck and there’s no two ways about it. Non-durables rely on more purpose-specific physical capital goods that require greater transaction costs between users/renters.

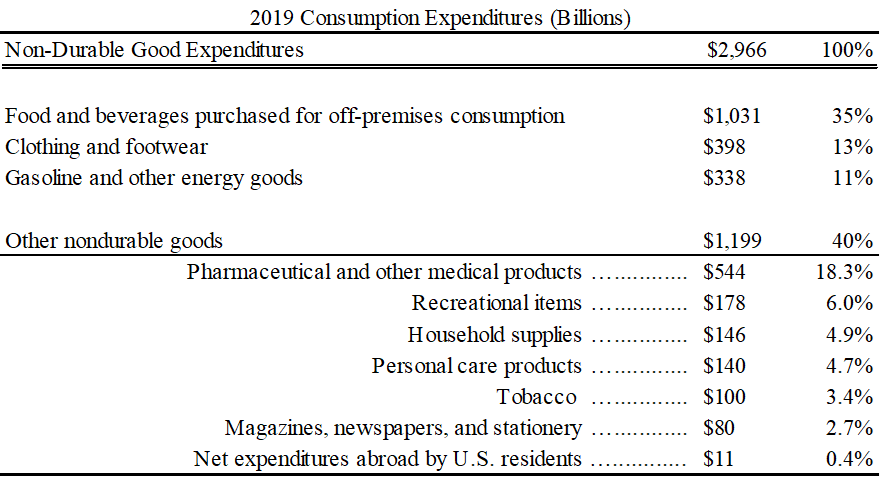

Food

Below are the Aggregate Supply – Aggregate Demand graphs for Food & Beverages and Clothing & Shoes. The former is for foods and beverages consumed off of the premises (so not restaurants). Since the pre-recession peak, total demand for food increased by 22% (that’s 22% over *two* years!). Except for a small hiccup in Q4 of 2020, the quantity of food purchased never fell during the pandemic and prices were constant for the first three quarters. Between 4 and 8 quarters after the pre-recession peak, food prices rose nearly 9.3%. AD increased for food with nary a supply disruption.

Clothes

Unlike food, most of the clothes that we consume are produced elsewhere. Recall that early in the pandemic, Covid-19 was only in China. We were already speculating on the supply chain disruptions in the US before the first domestic diagnoses appeared. In the below graph (right), prices rose and output declined. Given the time required to get clothes across the ocean, a supply shock is consistent with both the graph and the narrative. If AD for clothing was relatively steep, then there was probably a negative demand shock too. By the end of 2020, however, people were buying more clothes, with larger waists, than they were prior to the recession. Higher prices and output in 2021 reflect rebounding AD, though AS remained depressed. Demand for clothing ultimately rose by 20% from the pre-recession peak.

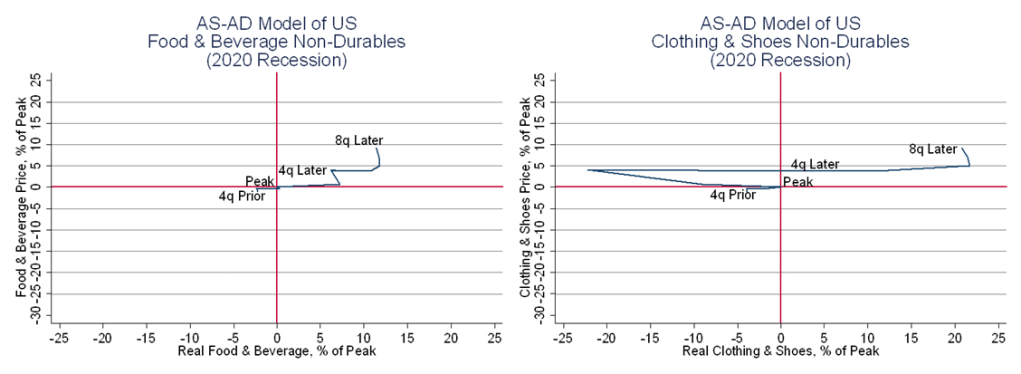

Gasoline

As we know, the market for gasoline was nuts. Aggregate demand for gas plummeted at the start of the pandemic, resulting in 22.9% less output and 28.6% lower prices (man, that was a nice time for people who were still out and driving). By the end of 2021, as we know, gas prices were up 23% relative to the pre-recession peak… Though, gasoline consumption still hasn’t returned to previous levels. AGAIN, by the end of 2021, after two years, US gas consumption was still not at its 2019 level. There was no initial supply shock to gasoline, but over the course of the two-year period our ability/willingness to produce seems to have atrophied somewhat.

Pharmaceuticals & Medical Products

Spending on pharmaceutical and medical products never fell. BUT, by the end of 2020, output was up, prices were down, and the trend continued during 2021 too. We became WAY better at providing pharmaceuticals. Some of this was the covid vaccine (prescription). But real non-prescription medical product consumption increased after the pre-recession peak by 22% – and producers were eager to supply. We’ve gotten much better at producing medical products since the start of the pandemic.

There is little evidence of a widespread pandemic supply shock in the non-durable consumables sector. Demand for clothes and shoes spending declined by 27% in the first two quarters of 2020 – and prices rose. There was, in fact, a brief supply shock to clothing. Given that many of the US’s clothes come from China and other countries that detected Covid-19 earlier, the decline in supply is unsurprising.

But clothes only composed 13% of pre-recession non-durable consumption spending. Gasoline demand fell and then rebounded. But, by the end of 2021, output never quite recovered and prices were already spiking. LRAS seems to have declined somewhat, but there was no initial SRAS shock. Food supply stayed relatively constant and demand rose as people sensibly substituted away from restaurants. Finally, Pharmaceuticals output increased and prices fell. We had a positive supply shock in pharmaceuticals! If we look at only the absolute essentials of food and medicine, one would be forgiven for asking ‘What recession?’.

One thought on “Dressed for Recess(ion)”