Pablo Budassi has created a logarithmic map of the entire known universe, that shows the distances and relative sizes of objects above the earth’s surface. I think you will find it a worthwhile use of your 30 seconds of attention to click on the link below, scroll to the bottom to start down at the earth’s surface (the image quality at the link is much better than I can convey in these snips here):

And then scroll your way up and up, through planets and stars to galaxies (not every star and every galaxy is shown, of course) and galaxy clusters:

And out through galaxy superclusters, to the very edge of the observable universe:

I am awed by the sheer sizes of things compared to familiar earth-scale objects. We know that our observable universe has not existed forever; presumably whatever caused this vast universe is incomprehensibly vaster. [1]

I am also impressed that humans are able to figure all this out; it is not obvious to the naked eye. An enormous amount of collective brainpower over the years has gone into making instruments (including space-based telescopes) to collect data at many electromagnetic frequencies and to figure out what it all means.

Bonus: In case you haven’t seen them already, here is a link to compelling infrared images from the newly-deployed $10 billion Webb space telescope (your tax dollars at work):

[1] I don’t want to distract from the sheer visual enjoyment of this graphic with a controversial discussion of what is responsible for bringing our universe into existence. All I will say here is that it did not come from “nothing”, as a certain dishonest physicist is fond of claiming. See the “Thinking About the Existence and Attributes of God” section of Christian Apologetics Insights from David Geisler, Ray Ciervo, and Prem Isaac [2020 NCCA, 9], including footnotes 1 and 2, for a brief discussion of these issues, and implications for a nonmaterial sustainer of physical reality.

For those who were unaware, we are apparently a Severanceblog now, a trend made all the better since nobody else is talking about the show anymore. Like all high concept fiction, the show can be consumed as a metaphor, in this case usually as a metaphor for modern office work. While I consume more than my share of metaphors, I usually find speculating about the “true” underlying metaphor driving a piece of storytelling to be more fun than useful. Instead, let’s talk about what the central conceit of the show actually is, namely a return to explicit slavery. Not almost slavery. Not wage slavery. Not “I’d rather be playing Minecraft on Twitch than making pivot tables in Excel ” slavery.

Actual slavery. The hook, through a clever bit of science fiction, is that it is slavery through a channel that allows a person to enslave the only person that we can imagine the world allowing to pass as anything but grossly criminal: themselves. The person you are enslaving to toil on your behalf happens to be a partitioned-off portion of your own consciousness (known as an “innie”) who continues to operate within a now shared bodily meat sack while your “outie” consciousness goes into a apparent blacked-out stasis. The innie does all the work, while the outie reaps (nearly all) all of the material rewards.

One take away is that there are people so desperate to not have to go to their jobs that they will carve off 8 hours a day out of their own claim to existence, a full third of their life, grant independent sentience to that third, and then enslave it. Putting aside the moral repugnance of such a decision for a second, one can’t help but ponder the preferences being revealed by an individual paying such a price.

Never trust a “unified theory” of damn near anything. It’s usually bullshit from the first moment, a cheap trick for gaining attention while grotesquely overreaching for importance in what is either a relatively mundane insight or a bit of intellectual sleight of hand designed to misdirect the reader from a deep underlying fallacy.

Anyway..

The price we’re willing to pay to not do something we don’t like often reveals more about ourselves than the prices we pay for the things we do like. The cost we’re willing to inflict on others reveals it all the more.

One of my little mental tricks when trying to understand human behavior that I can’t quite grok is to swap out a “utiliity maximizing” model for a “disutility minimizing” model. Trying to understand why a person would enslave a portion of themselves within the framework of “what are they maximizing?” lends itself to complex speculation on dimensions of their lives we can’t observe. Flipping it around, however, and asking what they are minimizing is immediately more intuitive. Without getting too deep into spoilers, there’s clearly a motive to minimize the disutility of work itself. Of toil, tedium, and drudgery. Of being told what to do and doing what you are told.

The hypothesis of Severance is that people will create an enslaved conscious person and explicitly deny the humanity of that person if, in doing so, they can minimize their own disutility of work. The corporation that creates these institutions in this fictional world will probably turn out to be either decadently evil in pursuit of pure profit or banally evil in pursuing some sort of yet unseen greater good. Even if they have rich and tragic back stories, the middle management that keep the plantation functioning are morally wretched individuals who have chosen to enable slavery to preserve their own status quo. The corporation, the managers, these are the bad guys. The heavys. The bullys who gain from the suffering of others.

But they’re not the monsters. The only monsters in the world of Severance are the individuals who made a choice to create and enslave another person solely so they themselves might enjoy a life without toil or tedium.

The cost that you are willing inflict on another in an effort to minimize your own discomfort reveals a lot about you. Whether you’re a socialist preaching “solidarity”, an economist who knows that Smithian “sympathy” is the glue of modern society, or just someone who thinks that it all comes down to coping with the prisoner’s dilemma, how a person values the suffering of others is a defining attribute.

Which brings me to a question I think only the creaters of Severance can answer. Is the conceit of their show to show that people will enslave a portion of themselves because they deny the humanity of their creation? Or is it that an office job is so abhorrent that opportunity to offload that burden to another while keeping the rewards for themselves overcomes any sympathy they might have for the other?

This show isn’t a metaphor. It’s a model. In this sense, Severance may be the most misanthropic hypothesis of humanity in the economically developed world I’ve ever observed. That humans, freed of the disutility of possible starvation or annihilation, will take any opportunity to minimize their own discomfort, even at the cost of a third of their lives and moral rot that comes with the enslavement and denied humanity of another. Somewhere, in the deep dark noughaty core of this piece of fiction is the consideration that, freed from our need for one another, our antipathy for discomfort will birth an idle, half-drunk decadence that will lead us to literally eat away at ourselves.

Or maybe the creators just all had office jobs while they were trying to make it in hollywood, and they really, really hated them.

I have written three blogs on the TV show Severance this summer. My newest post is up at the Online Library of Liberty.

I discuss how job perks are portrayed in the show. The bosses in the show are creepy and we come to find out that they are totally evil. Given the way everything feels in the show, you could come to the conclusion that perks are generally manipulative and false. Someone implied that in an op-ed published by the NYT.

My argument is that free adults can use “perks” to motivate themselves and each other to do the right thing.

We are all just trying to get that dopamine, in the short term. Should people only feel happy when they are doing drugs or playing video games? Should bosses not be allowed to create a fun moment at work?

Trivial gifts and prizes must be cheap, so that their cost does not start to outweigh the benefits of incentivizing things we should be doing anyway. Finding ways to make a responsible life exciting is in fact the key to maintaining our liberty. Most people do not want to be martyrs. They want life to be fun.

The following tweet shows the character Dylan and his performance prize.

— OutofContextSeverance (@SeveranceOutof) June 24, 2022

Behavioral scientists have documented lots of quirks in human behavior. We aren’t solely motivated by our (real wage) salaries to produce effort. The good news is that we are capable of self-reflection. We can make these quirks work for us. Lots of successful people will promise themselves a small reward at the end of the week if they accomplish something hard.

Perks aren’t all bad at work, but, on the other hand, Severance could make you more alert to genuine manipulation that is out there.

Watching Severance prompts good questions. Who are you? (That’s the opening line of the show.) What are you doing with your life? Whose purposes are you serving?

I liked the show because it has great characters, funny moments, and it gets you thinking. If you watch the show, don’t take it too seriously. Ben Stiller is a co-director. The man (the genius) brought us Zoolander (2001).

One give-away that this ain’t the new 1984 is a plot hole concerning how the main character Mark decided to sever himself and join the evil corporation. According to the show, his wife died and he was so sad that he quit his job as a history professor after three weeks of feeling sad. I know a lot of academics. History professors have worked too hard and too long to quit their jobs after three weeks of feeling sad. Take everything with a grain of salt from these writers. Mark’s general lack of executive control is at odds with the backstory that he once obtained a job as a history professor.

Severance is described as science fiction but it clearly takes place in the United States of America. For one thing, a “senator” has a role. For another thing, the work schedule is pretty American. This is a funny video on how Europeans view the American work schedule:

What Finland thinks an American workday looks like

I have no idea how far down the rabbit hole the writers will feel like they have to do in Season 2. Will there be a role for a POTUS?

The second blog was posted to EWED: my thoughts about relating Severance to Artificial Intelligence.

A question this raises is whether we can develop AGI that will be content to never self-actualize.

And, back in May, OLL ran my first blog about Severance and drudgery.

The first line in the show is, “Who are you?” Themes about identity and purpose are explored alongside the thrilling hijinks of the prisoner innies. Outie Mark has nothing except his personal life to think about, which in his case is tragic. Innie Mark has nothing but work. Neither man is happy or complete.

Michael Maynard and I wrote about giving a good gift. A good gift is one in which the giver has an information advantage. Gifting an object or a service can provide a consumption bundle to the recipient that they didn’t know was even possible or that they didn’t know that they would prefer. They would have chosen the items themselves, if only they had known about them. Giving a gift card can be similar if the recipient did not know about the vendor previously. Cash is a good gift when the giver does not have an information advantage over the recipient.

In our previous post, we showed diagrammatically that ‘better off’ was indicated by the higher utility. But this spurs an important question:

No big post this week, I’m in the Maine Woods without reliable internet or electricity.

The one economics angle to all this is that like many seemingly ancient Maine forests, the one I’m in used to be a farm. Notice the barbed wire running right through the middle of a huge old tree; the farm was abandoned so long ago that the tree had time to grow that big around it.

Why was the farm abandoned? Maine is cold and our soil is rocky, so agriculture tends to be unproductive relative to the Midwest. Many people left their farms in the late 1800s and early 1900s for new land in the West or, more commonly, manufacturing jobs in the cities. Maine used to be half farms, but now its land is 90% forest.

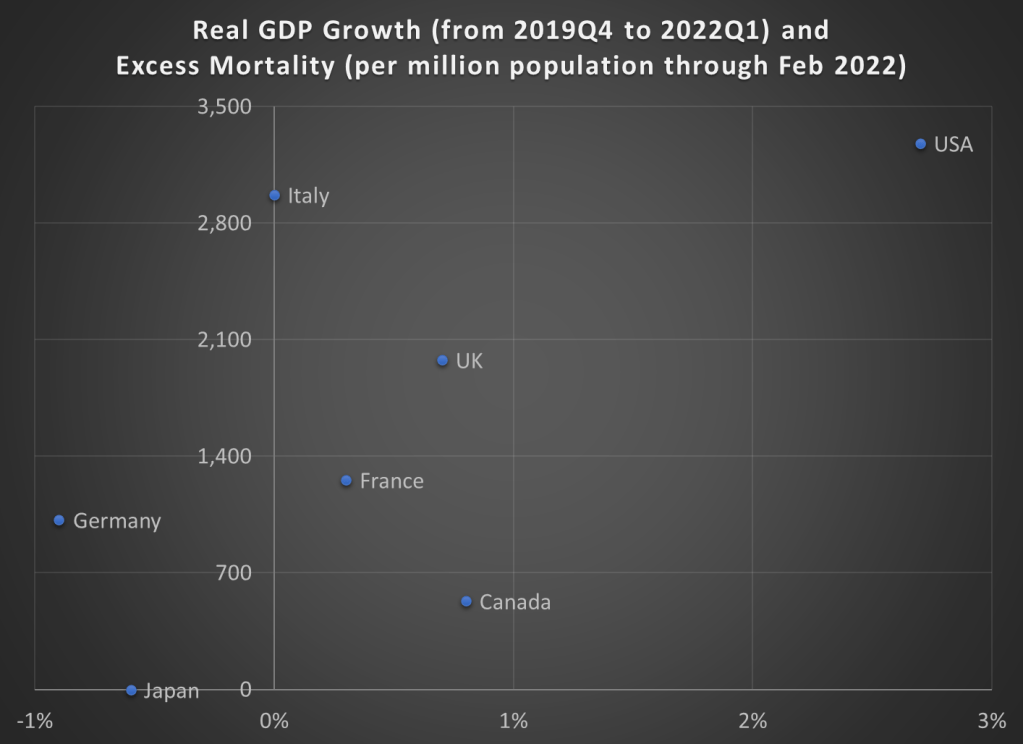

Today, my chart looks at the G7 countries (representing roughly half of global wealth and GDP), showing both their economic performance (as measured by real GDP growth) and health performance (as measured by excess mortality through February 2022).

The US has clearly had the best economic performance. But the US also had the highest level of excess deaths per capita (not all of this is from COVID — US drug overdoses are also way up — but even using official COVID deaths, the US still tops this group).

Japan had the best health performance, in fact amazingly no cumulative excess deaths through February 2022 (this has risen very slightly since then, but I stopped in February so all countries had complete data). However, Japan also had slightly negative economic growth.

Which country ends up looking the best? Canada! Very low levels of excess deaths, and at least some positive economic growth. Not as much growth as the US, but Canada is the second best performer in the G7.

To give some context of just how low the level of deaths have been in Canada, first recognize that the US had 1.1 million excess deaths in the pandemic through February 2022. If instead our excess deaths had been roughly equal to Canada on a per capita basis, we would have only had 180,000 excess deaths in the US, saving over 900,000 lives.

Some of Canada’s COVID policy have been overly restrictive, such as the vaccine mandates that sparked protests in February 2022. But by then, Canada had already largely achieved it’s COVID victory over the US and most other G7 nations. Compare excess mortality in Canada with the US: the only big wave in Canada that came close to the US was the Spring 2020 wave. After that, Canada was always much lower.

Ah, the delicious crypto bubble of 2021. Major cryptocurrencies like Bitcoin and Ethereum more than tripled in value. Every week, some new coin would get minted, letting early adopters 10X their money in a month. Decentralized finance (DeFi) based on blockchain technology was The Next Big Thing. Move over, stodgy old Bank of America.

That was then, this is now. The chart below of Bitcoin price serves as a proxy for the fortunes of the whole sector:

This has the smell of a bubble bursting. First, why did crypto soar in 2021? I think COVID gets some credit for that. Most adults in the developed world sat home for many months in 2020-2021, and in countries like the U.S. were handed thousands of dollars of stimulus money, in addition to giant unemployment checks. Much of that money went to buying “stuff” on Amazon, but much of it went into financial assets like stocks and crypto. Something like half of men in the United States between the ages of 18 and 49 dabbled in crypto. As you saw your friends making money effortlessly, classic tulip bulb FOMO set it.

All bubbles end eventually. Crypto has imploded from a $ 3 trillion market to a $ 1 trillion dollar market in just a few months. That is two trillion (with a “t”) gone. If Bitcoin were the only significant factor in the crypto universe, the latest bust would be a fairly trivial matter. Since Bitcoin goes up and Bitcoin goes down, that is nothing new. But part of the hype of 2021 was all the breathless commentary on how DeFi would sweep the world and Change Everything. No more centralized banking controlled by old men in suits – – power to the people! And in fact, a whole industry of lending and borrowing in the crypto world has sprung up. That is where some more consequential problems have shown up.

Warren Buffet is known for the saying, “When the tide goes out, you find out who is swimming naked.” The rapid fall in crypto valuations has set off a cascade of failures in DeFi. A key event was the implosion of the Luna/Terra (un!)stablecoin, in April-May 2022, which we wrote about here. A more widespread problem has been the unwinding of the crypto lending/borrowing system. Various firms loaned out the coin holdings of their customers to parties that wanted to trade (speculate) with them, and who were willing to pay something like 4-9% interest for get ahold of these coins. The parties doing the lending thought they were keeping themselves safe by requiring excess collateral for these loans.

Oversimplified example: I will lend you $100 (real dollars) if you deposit $140 of Dogecoin with me. If Dogecoin falls in value to close to $100, I would require more collateral from you within say ten days, or else I would sell your Dogecoin into the market and get my $100 back (and you eat the $40 loss). The big problem comes if Dogecoin falls so fast that by the contracted grace period ends, its value is down to $80. Now I as well as you realize losses, and widespread panic ensues. Now, if I have been lending out your Dogecoin to yet more parties who (it turns out) can’t pay me back in full, I am doubly hosed. And now the solid customers start withdrawing their funds/coins from these firms, and we have an old-fashioned bank run. It doesn’t help that Celsius Network froze customers’ accounts last month, so they could not withdraw the coins they had deposited. That sort of thing really gets clients nervous.

And so a number of significant DeFi firms are going bust, and calls get louder for more government regulation, which is largely antithetical to the whole DeFi enterprise. I will paste below a summary of this carnage, and then in the interests of full disclosure, tell how it has affected me personally:

The crypto and the DeFi industry boomed over the past few years but the recent crypto crash has plundered the fortunes of several crypto companies. The following crypto companies have recently encountered financial difficulties:

Vauld

Business Today broke the news on Monday that Vauld, the Singapore-based crypto lending and investment firm operating in India announced that it has halted withdrawals and deposits for its more than 8,00,000 clients. Vauld’s CEO Darshan Bathija said in a blog post that unstable market circumstances had created “financial challenges” for the company. The CEO also announced that investors had withdrawn over $197 million in the past few months.

Terraform Labs

Terraform Labs was the company that had triggered the recent crypto crash. They created the algorithmic stablecoin TerraUSD which de-pegged from the US Dollar and led to the crash of Terra Luna another token of the ecosystem causing massive panic and sell off in the crypto markets.

Terra co-founder Do Kwon announced a “recovery plan” in May that included infusion of additional funding and the rebuilding of TerraUSD so that it is backed by reserves rather than depending on an algorithm to maintain its 1:1 dollar peg.

Voyager Digital

On July 6, the American crypto lender disclosed that it had filed for bankruptcy. In its Chapter 11 bankruptcy petition, Voyager stated that it had over 1,00,000 creditors, assets between $1 billion and $10 billion in value, and liabilities in the same range.

Three Arrows Capital (3AC)

The Singapore-based cryptocurrency hedge firm went bankrupt on June 29, just two days after receiving a notice of default on a crypto loan from lender Voyager Digital for failing to make payments on an approximately $650 million crypto loan. The company filed a petition for protection from its creditors under Chapter 15 of the United States’ bankruptcy code on July 1. This section of the code permits overseas debtors to safeguard their U.S.-based assets.

Celsius Network

Celsius Network also suspended withdrawals and transfers last month due to “extreme” market conditions. They also hired consultants in preparation for a future bankruptcy filing. The American-Israeli business reportedly disclosed on July 4 that a quarter of its workers had been let go.

Babel Finance

The Hong Kong-based cryptocurrency lender stated on June 17 that it had temporarily halted crypto-asset withdrawals as it scrambled to reimburse consumers. According to the company, “Babel Finance is suffering unprecedented liquidity issues due to the current market situation,” emphasising the severe volatility of the market for cryptocurrencies.

CoinFLEX

In a blog post published on Thursday, CoinFLEX’s CEO Mark Lamb announced that the company would temporarily halt withdrawals due to “extreme market conditions” and uncertainty about a certain counterparty. The company is facing serious financial troubles and there seems to be no way out.

My Confessions

Briefly — I bought into Bitcoin and Ethereum in the form of the funds GBTC and ETHE towards the end of 2020. As crypto started to unwind this year, I sold out of ETHE to de-risk, coming out a little ahead there. I decided to hang in with the Bitcoin fund, riding it up, and now down, down, down. I am so far in the red on this one that I am just going to hold it indefinitely, hoping for some recovery someday.

I bought into Voyager (see above, it has recently crashed and burned) and sold half after it doubled, and the rest at about breakeven price, so came out ahead there. Another, similar firm, Galaxy Digital, I bought has also plummeted to near zero. I got out of that, but waited too long and lost about 30% there.

Readers with exquisite memories might recall that I wrote an article some months back here on EWED touting the DeFi model as a great way to earn interest to keep up with inflation: “Earning Steady 9% Interest in My New Crypto Account.” I chose BlockFi rather than Celsius Network to put my funds in for this, since Celsius (an offshore enterprise) seemed a little shady, whereas BlockFi made a point of being audited and compliant with U.S. regulations. Good choice, in light of Celsius’ recent freeze on customer withdrawals.

Now, even solid firms like BlockFi are hurting. Customers spooked by all the other crypto drama are withdrawing assets “just to be on the safe side.” BlockFi is seeking cash infusions from white knight Sam Bankman-Fried to stay afloat. The 30-year old crypto billionaire looks to be able to acquire the firm for pennies on the dollar, wiping out the initial (private) investors in BlockFi. I am one of these BlockFi customers withdrawing funds (half of my deposit there) – – just to be on the safe side.

Pete Buttigieg is the Secretary of Transportation in the Biden administration. He has made an interesting habit of going on Fox News and willingly submitting himself to what his interlocutors clearly anticipate to be difficult “gotcha” questions that will leave their liberal target squirming on camera. Secretary Buttigieg seems to always come out the clear winner and I think there is something to be learned from it.

The easy answer is that Buttigieg is smarter and more polished than the Fox News interviewers, which he is, but I think that’s easy to overrate. There is no shortage of smart people who wouldn’t fair half as well as the Secretary does. Part of it is his calm and poise, but credit should also go to just being nice. That niceness really puts people on the back foot. The secret sauce, in my estimation, is that he never for a second sounds like he is arguing. There’s no sense that he is interested in a back in forth. He never gives anyone an opening to raise their voice, to seem attacked.

But it’s not just being nice. The interviewer in the first clip quickly realizes that his question has failed to get the desired reaction, and subsequently tries to interrupt him at multiple points. The Secretrary simply ignores him and proceeds with his answer without missing a beat or raising his voice. He’s the G-d— Secretary of Transportation. He doesn’t have to be deferential to some teleprompter anchorman trying to raise points of political decorum and social norms with a member of the opposition party that has been given no quarter on their network for 20 years.

So how do you be like Pete?

Be nice.

Know your stuff.

Never defer to anyone who isn’t nice and doesn’t know their stuff.

Being nice is inclusive of being polite, but there is more to it. It means being generous in the motives you assume in others, including those who are questioning or arguing with you. It means using tones of voice and choices of language that don’t imply you are dealing with an enemy or a fool, even when dealing with a foolish enemy.

Knowing your stuff means that you can explain choices and positions clearly and concisely in a manner than allows the people listening to you to actually learn something. Knowing you stuff, however, also confers on you the right to finish your thoughts. If others prefer your conversation be more akin to a verbal brawl, that’s their prerogative, but that doesn’t mean they get to dictate where your thoughts begin and end just because they’ve lost control of the outcome. Knowledge should confer some privleges, be them however limited.

And finally, being like Pete means never deferring to people who don’t want to play by the rules of basic civility and have nothing to contribute to the conversation. You’ve got a job to do and being nice will help you do it all the better. So be nice, until it’s time to not be nice.

Have you heard of The World Games? It’s the Olympics for sports that are too random to be in the real Olympics. It is happening right now in Birmingham, AL. It’s not too late to get your tickets to see Canoe Polo.

For people interested in regional politics, this blog about the city successfully hosting a major event might be interesting. His references to people in “the suburbs” is something you won’t understand without some context and history. But you don’t have to be a local to learn that history, since everything is online.

We are living in volatile times. With covid-19, big federal legislation packages, and the Ruso-Ukrainian conflict disruptions to grain, seed oils, and crude oil, relative prices are reflecting sudden drastic ebbs of supply and demand. I want to make a small but enlightening point that I’ve made in my classes, though I’m not sure that I’ve made it here.

Economists often get a bad rap for being heartless or unempathetic. Sometimes, they are painted as ideologues who just disguise their pre-existing opinions in painfully specific terminology and statistics. Let’s do a litmus test.

Consider two alternative markets. One is a perfect monopoly, the other has perfect competition. All details concerning marginal costs to firms and marginal benefits to consumers are the same. In an erratic world, which market structure will result in greater price volatility for consumers? Try to answer for yourself before you read below. More importantly, what’s your reasoning?

Extreme Market Power

A distinguishing difference between a competitive market and a monopoly concerns prices. While firms maximize profits in both cases, the price that consumers face in a competitive market is equal to the marginal cost that the firms face. There is no profit earned on that last unit produced. In the case of monopoly, the price is above the marginal cost. Profits can be positive or negative, but the consumer will pay a price that is greater than the cost of producing the last unit.

Below are two graphs. Given identical marginal costs of production and benefits that the consumers enjoy, we can see that:

The monopoly price is higher.

The monopoly quantity produced is lower.

But static models only go so far. What about when there is volatility in the world?

Volatile Costs

Oil and gasoline are important inputs for producing many (most?) physical goods. Not only that, they are short-lived, meaning that they disappear once they are used, making them intermediate goods. Therefore, changes in the price of oil constitutes a change in the marginal cost for many firms. If the price of oil rises, or is volatile otherwise, then which type of market will experience greater price and quantity volatility?

Below are two figures that illustrate the same change in the marginal cost. We can see that:

Monopoly price volatility is lower (in absolute terms and percent).

Monopoly quantity produced volatility is lower (in absolute terms, though no different as a percent).

The take-away: While monopoly does constrict supply and elevate prices, Monopoly also reduces price and output volatility when there are changes in the marginal cost.

Volatile Demand

That covers the costs. But what about volatile demand? A large part of the Covid-19 recession was the huge reallocation of demand away from in-person services and to remote services and goods. What is the effect of market power when people suddenly increase or decrease their demand for goods?

Below are two figures that illustrate the same change in demand. We can see that:

Monopoly price volatility is higher (in absolute terms, though no different as a percent).

Monopoly quantity produced volatility is lower (in absolute terms, though no different as a percent).

Monopolies Don’t Cause Inflation

Economists know that inflation can’t very well be blamed on greed (does less greed beget deflation?). Another problematic story is that market concentration contributes to inflation. But the above illustrations demonstrate that this narrative is also a bit silly. Monopolistic markets cause the price level to be higher, it’s true. But inflation is the change in prices. Changing market concentration might be a long term phenomenon, but can’t explain acute price growth. If demand suddenly rises, monopolies result in no more price growth than perfectly competitive markets. If the marginal cost of production suddenly rises, monopolies result in less price growth.

All of this analysis entirely ignores welfare. Also, no market is perfectly competitive or perfectly monopolistic. They are the extreme cases and particular markets lie somewhere in between.

Did you guess or reason correctly? Many econ students have a bias that monopolies are bad. So, in any side-by-side comparison, students think that “monopolies-bad, competition-good” is a safe mantra. But the above illustrations (which can be demonstrated mathematically) reveal that economic reasoning helps to reveal truths about the world. Economists are not simply a hearty band of kool-aid drinking academics.