That’s the title of a blockbuster new paper by Shikhar Singla. The headline finding is that increased regulatory costs are responsible for over 30% of the increase in market power in the US since the 1990’s. That’s a big deal, but not what I found most interesting.

One big advance is simply the data on regulation. If you want to measure the effect of regulation on different industries, you need to come up with a way to measure how regulated they are. The crude, simple old approach is to count how many pages of regulation apply to a broad industry. The big advance of Mercatus’ RegData was to use machine learning to identify which specific industry is being discussed near “restrictive words” in the Code of Federal Regulation that indicate a regulatory restriction is being imposed. But not all regulatory words (even restrictive ones) are created equal; some impose very costly restrictions, most impose less costly restrictions, and some are even deregulatory. Singla’s solution is to take the government’s estimates of regulatory costs and apply machine learning there:

This paper uses machine learning on regulatory documents to construct a novel dataset on compliance costs to examine the effect of regulations on market power. The dataset is comprehensive and consists of all significant regulations at the 6-digit NAICS level from 1970-2018. We find that regulatory costs have increased by $1 trillion during this period.

The government’s estimates of the costs are of course imperfect, but almost certainly add information over a word-count based approach. Both approaches agree that regulation has increased dramatically over time. How does this affect businesses? Here’s what’s highlighted in the abstract:

We document that an increase in regulatory costs results in lower (higher) sales, employment, markups, and profitability for small (large) firms. Regulation driven increase in con- centration is associated with lower elasticity of entry with respect to Tobin’s Q, lower productivity and investment after the late 1990s. We estimate that increased regulations can explain 31-37% of the rise in market power. Finally, we uncover the political economy of rulemaking. While large firms are opposed to regulations in general, they push for the passage of regulations that have an adverse impact on small firms

More from the paper:

an average small firm faces an average of $9,093 per employee in our sample period compared to $5,246 for a large firm

a 100% increase in regulatory costs leads to a 1.2%, 1.4% and 1.9% increase in the number of establishments, employees and wages, respectively, for large firms, whereas it leads to 1.4%, 1.5% and 1.6% decrease in the number of establishments, employees and wages, respectively for small firms when compared within the state-industry-time groups. Results on employees and wages provide evidence that an increase in regulatory costs creates a competitive advantage for large firms. Large firms get larger and small firms get smaller.

The fact that large firms benefit while small firms are harmed is what drives the increase in concentration and market power.

What I like and dislike most about this paper is the same thing: its a much better version of what Diana Thomas and I tried to do in our 2017 Journal of Regulatory Economics paper. We used RegData restriction counts to measure how regulation affected the number of establishments and employees by industry, and how this differed by firm size. I wish I had thought of using published regulatory cost measures like Singla does, but realistically even if I had the idea I wouldn’t have had the machine learning chops to execute it. The push to quantify what “micro” estimates mean for economy-wide measures is also excellent. I hope and expect to see this published soon in a top-5 economics journal.

Thinking about one of my older papers today, since I just heard it won the Eckstein award for best paper in the Eastern Economic Journal in 2019 & 2020.

One big selling point of the Affordable Care Act was that by offering more non-employer-based options for health insurance, it would free people who felt locked into their jobs by the need for insurance. This would free people up to leave their jobs and do other things like start their own businesses. Did the ACA actually live up to this promise?

It did, at least for some people. The challenge when it comes to measuring the effect of the ACA is that it potentially affected everyone nationwide. If entrepreneurship rises following the implementation of the ACA in 2014, is it because of the ACA? Or just the general economic recovery? Ideally we want some sort of comparison group unaffected by the ACA. If that doesn’t really exist, we can use a comparison group that is less affected by it.

That’s what I did in a 2017 paper focused on younger adults. I compared those under age 26 (who benefit from the ACA’s dependent coverage mandate) to those just over age 26 (who don’t), but found no overall difference in how their self-employment rates changed following the ACA.

In the 2019 Eastern Economic Journal paper, Dhaval Dave and I instead consider the effect of the ACA on older adults. We compare entrepreneurship rates for people in their early 60’s (who might benefit from the availability of individual insurance through the ACA) with a “control group” of people in their late 60’s (who are eligible for Medicare and presumably less affected by the ACA). We find that the ACA led to a 3-4% increase in self-employment for people in their early 60’s.

Figure 1 from our 2019 EEJ paper

Why the big difference in findings across papers? My guess is that it’s about age, and what age means for health and health insurance. People in their 60s are old enough to have substantial average health costs and health insurance premiums, so they will factor health insurance into their decisions more strongly than younger people. In addition, the community rating provisions of the ACA generally reduced individual premiums for older people while raising them for younger people.

In sum, the ACA does seem to encourage entrepreneurship at least among older adults. At the same time, our other research finds that the employer-based health insurance system still leads Americans to stay in their jobs longer than they would otherwise choose to.

The US government is great at collecting data, but not so good at sharing it in easy-to-use ways. When people try to access these datasets they either get discouraged and give up, or spend hours getting the data into a usable form. One of the crazy things about this is all the duplicated effort- hundreds of people might end up spending hours cleaning the data in mostly the same way. Ideally the government would just post a better version of the data on their official page. But barring that, researchers and other “data heroes” can provide a huge public service by publicly posting datasets that they have already cleaned up- and some have done so.

That’s what I said in December when I added a data page to my website that highlights some of these “most improved datasets”. Now I’m adding the Behavioral Risk Factor Surveillance Survey. The BRFSS has been collected by the Centers for Disease Control since the 1980s. It now surveys 400,000 Americans each year on health-related topics including alcohol and drug use, health status, chronic disease, health care use, height and weight, diet, and exercise, along with demographics and geography. It’s a great survey that is underused because the CDC only offers it in XPT and ASC formats. So I offer it in Stata DTA and Excel CSV formats here.

Let me know what dataset you’d like to see improved next.

The key lesson, the thing I would impart to any aspiring bloggers, content creators, or newsletter proprietors, is that the cornerstone of internet success is not intelligence or novelty or outrageousness or even speed, but regularity. There are all kinds of things you can do to develop and retain an audience — break news, loudly talk about your own independence, make your Twitter avatar a photo of a cute girl — but the single most important thing you can do is post regularly and never stop.

Granted, “work hard and keep doing the thing you’re doing” is probably above-replacement advice for any kind of entrepreneurial activity. But it’s particularly true for online content creation. As Yglesias suggests, the internet and feed-based social platforms have constructed an insatiable demand for content, so if you can produce content mechanically, without requiring expensive resources (such as time, wit, or subject-specific knowledge), you’re in an excellent position to take advantage. But most importantly, this demand is so insatiable that there is currently no real economic punishment for content overproduction. You will almost never lose money, followers, attention, or reach simply from posting too much.

That is from an excellent post by Max Read. It is fairly short and has some good examples, so I recommend reading the whole thing. Tyler Cowen made a similar point back in 2019:

There’s a certain way in which on the internet you can’t be overexposed. There’s just a steady stream of you, it feels like being overexposed compared to the standards of 1987 or whenever, but in fact it’s not and people are picking and choosing. And you end up just dominating a particular space in a particular kind of way. And I think most older people have not made that transition mentally to understanding how you should exist intellectually on the internet.

Of course, this is also part of Joy’s idea with this site and why we write every day:

It’s just time to start writing more. This is a model that I have learned from Tyler Cowen, and most writers I admire write every day whether or not they have time for it. David Perell has tweeted that writing and thinking are the same thing. Thus, if you are a thinker, writing is not a waste of time. Writing is the thing you are doing anyway in your muddled head.

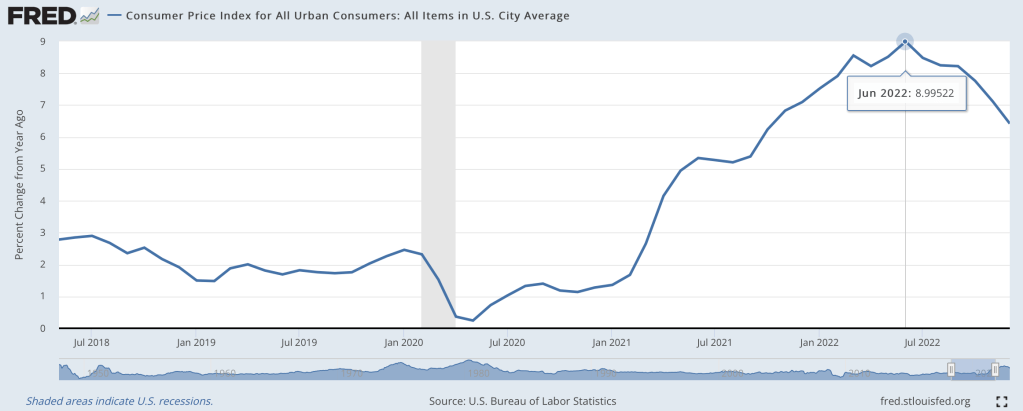

Last June I wondered if we were seeing the peak of inflation, and by at least one major measure I called the peak exactly:

At the moment, though, I’m feeling more confused than prophetic. The big question a year ago was how long it would take the Fed to get inflation down to reasonable levels, and how much collateral damage they would do to the real economy in that effort. Today most current indicators make it look like they pulled off the miraculous “soft landing”. Inflation over the last 12 months is still high, but over the last 6 months we’re nailing the Fed’s 2% annualized target. This has hit a few sectors of the real economy hard, with housing slowing dramatically and tech doing mass layoffs, but the overall picture is great: GDP growth was around 3% the last 2 quarters, and the 3.4% unemployment is the lowest since 1969.

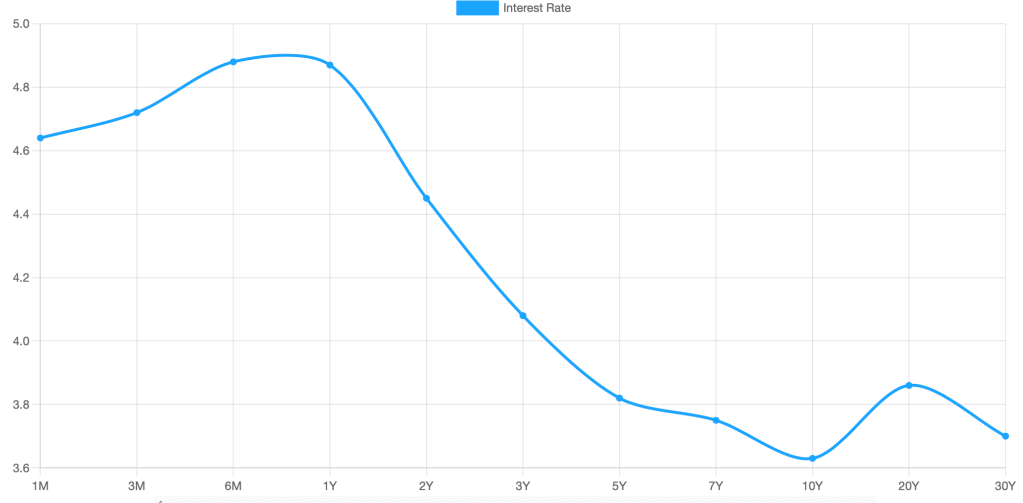

What’s confusing about this is that we have a hard time believing we really got this lucky. Its like your plane lost power, you diverted course for an emergency crash landing, and once you touch down and find yourself seemingly unharmed you look around and wonder if the plane is about to explode. Consumer sentiment is worse than it was in the depths of Covid; business sentiment has been falling for over a year and is almost down to March 2020 levels. Betting markets forecast a 50% chance of a recession in 2023, and the yield curve is strongly inverted (one of the best predictors of a recession, though the guy who first noticed this says it might not work this time):

Finally, M2 money supply is shrinking for the first time since at least 1960, and I believe the first time since the Great Depression. This bodes well for inflation continuing to moderate, but its also one more indicator of a potential recession.

To sum up, most of the indicators of the current state of the economy look great, while most indicators of its near-term future look awful. So which do we trust?

My guess is that we avoid recession in 2023, but honestly this is mostly the gut feeling of an optimist. There’s no one knock-down piece of data I’d point to in support; its more that things are currently going well, and usually the best prediction is that tomorrow will be like today unless you have a good reason to think otherwise. The main reason people expect a slowdown is because of the Fed’s actions to fight inflation. The Fed itself predicts that they will cause a slowdown, but not a recession. Their most recent summary of economic projections from December predicts GDP growth slowing to 0.5% in 2023 and unemployment rising to 4.6%.

I think the “so what” outlook is also murky. Stocks have already fallen a lot from their highs and a recession already seems somewhat ‘priced in’, so even if I thought one was coming I wouldn’t necessarily sell stocks. On the flip side US stocks are still quite expensive by historical standards, so I don’t want to buy more on the assumption that they’ll rise more on good economic news this year. You might want to lock in decent rates on long-term bonds if you think the Fed will cut rates in response to a recession, but the inverted yield curve shows this is already somewhat priced in. 1-year bonds yielding almost 5% seems decent in either scenario, I have some and I’ll probably buy more, but 5% returns are nothing to get excited about. I’d like to hear suggestions but to me the small direct betting market on a potential recession is the clearest “so what” for anyone who does have a confident view about this year’s macro picture.

Since early in graduate school I’ve kept a running list of ideas for economics papers I’d like to write and publish some day. I’ve written many of the papers I planned to, and been scooped on others, but the list just keeps growing. As I begin to change my priorities post-tenure, I decided it was time to publicly share many of my ideas to see if anyone else wants to run with them. So I added an ideas page to my website:

Steal My Paper Ideas! I have more ideas than time. The real problem is that publishing papers makes the list bigger, not smaller; each paper I do gives me the idea for more than one new paper. I also don’t have my own PhD students to give them to, and don’t especially need credit for more publications. So feel free to take these and run with them, just put me in the acknowledgements, and let me know when you publish so I can take the idea off this page.

Here’s one set of example ideas:

State Health Insurance Mandates: Most of my early work was on these laws, but many questions remain unanswered. States have passed over a hundred different types of mandated benefits, but the vast majority have zero papers focused on them. Many likely effects of the laws have also never been studied for any mandate or combination of mandates. Do they actually reduce uncompensated hospital care, as Summers (1989) predicts? Do mandates cause higher deductibles and copays, less coverage of non-mandated care, or narrower networks? How do mandates affect the income and employment of relevant providers? Can mandates be used as an instrument to determine the effectiveness of a treatment? On the identification side, redoing older papers using a dataset like MEPS-IC where self-insured firms can be used as a control would be a major advance.

You can find more ideas on the full page; I plan to update to add more ideas as I have them and to remove ideas once someone writes the paper.

Thanks to a conversation with Jojo Lee for the idea of publicly posting my paper ideas. I especially encourage people to share this list with early-stage PhD students. It would also be great to see other tenured professors post the ideas they have no immediate plans to work on; I’m sure plenty of people are sitting on better ideas than mine with no plans to actually act on them.

The scars of Hurricane Katrina were still obvious eight years afterward when I moved to New Orleans in 2013. Where I lived in Mid-City, it seemed like every block had an abandoned house or an empty lot, and the poorer neighborhoods had more than one per block. Even many larger buildings were left abandoned, including high-rises.

Since then, recovery has continued at a steady pace. The rebuilding was especially noticeable when I spent a few days there recently for the first time since moving away in 2017. The airport has been redone, with shining new connected terminals and new shops. The abandoned high-rise at the prime location where Canal St meets the Mississippi has been renovated into a Four Seasons. Tulane Ave is now home to a nearly mile-long medical complex, stretching from the old Tulane hospital to the new VA and University Medical Center complex. There are several new mid-sized health care facilities, but most striking is that Tulane claims to finally be renovating the huge abandoned Charity Hospital:

Old Charity Hospital, January 2023

The new VA hospital opened in 2016 as mostly new construction, but they’ve now managed to fully incorporate the remnants of the abandoned Dixie Beer brewery:

VA Hospital incorporating old Dixie Beer tower, January 2023

Dixie beer itself opened a new beer garden in New Orleans East, and just renamed itself Faubourg Brewery. Some streets named for Confederates have also been renamed, though you can still see plenty of signs of the past, like the “Jeff Davis Properties” building on the street renamed from Jefferson Davis Parkway to Norman C Francis Parkway.

Statue of Diana, Original Sculpture GardenPart of the Expanded Sculpture Garden

Of course, even with all the improvements, many problems remain, both in terms of things that still haven’t recovered from the hurricane, and the kind of problems that were there even before Katrina. The one remaining abandoned high-rise, Plaza Tower, was actually abandoned even before Katrina.

My overall impression is that large institutions (university medical centers, the VA, the airport, museums, major hotels) have been driving this phase of the recovery. The neighborhoods are also recovering, but more slowly, particularly small business. Population is still well below 2005 levels. I generally think inequality has been overrated in national discussions of the last 15 years relative to concerns about poverty and overall prosperity, but even to me New Orleans is a strikingly unequal city; there’s so much wealth alongside so many people seeming to get very little benefit from it.

The most persistent problems are the ones that remain from before Katrina: the roads, the schools, and the crime; taken together, the dysfunctional public sector. Everywhere I’ve lived people complain about the roads, but I’ve lived a lot of places and New Orleans roads were objectively the worst, even in the nice parts of town, and it isn’t close. The New Orleans Police Department is still subject to a federal consent decree, as it has been since 2012. The murder rate in 2022 was the highest in the nation. Building an effective public sector seems to be much harder than rebuilding from a hurricane.

As much as things have changed since 2013, my overall assessment of the city remains the same: its unlike anywhere else in America. It is unparalleled in both its strengths and its weaknesses. If you care about food, drink, music, and having a good time, its the place to be. If you’re more focused more on career, health, or safety, it isn’t. People who fled Katrina and stayed in other cities like Houston or Atlanta wound up richer and healthier. But not necessarily happier.

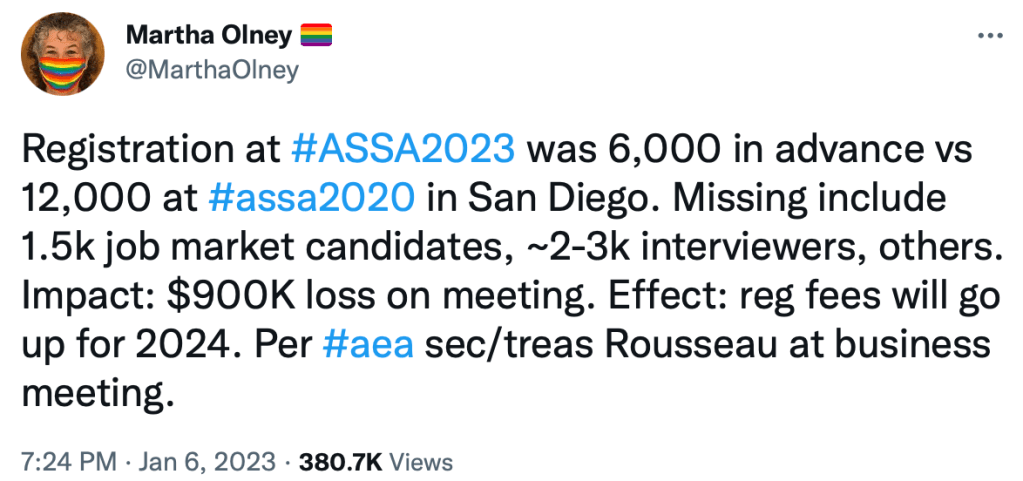

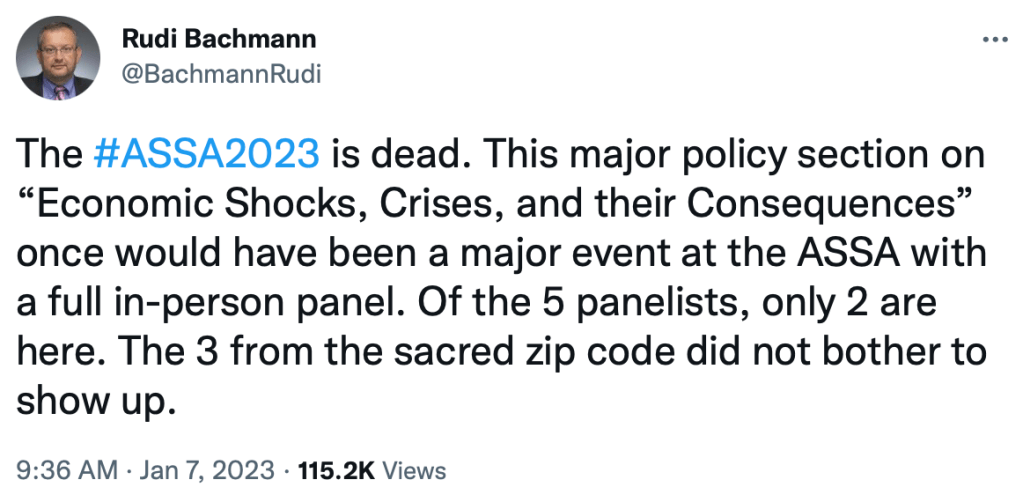

I expected the meetings would shrink, but I was still surprised by how much they did:

That said, I mostly didn’t notice the smaller numbers on the ground, because most of the missing people are those on the job market, who used to spend most of their time shut away doing interviews anyway. There was still a huge variety of sessions and most seemed well-attended. ASSAs is also still unparalleled for pulling in top names to give talks; I got to talk to Nobel laureate Roger Myerson at a reception. But there may be a trend of the big names being more likely to stay remote:

The big problem with attendance falling to 6k is that they’ve planned years worth of meetings with the assumption of 12k+ attendance. Getting one year further from Covid and dropping mask and vaccine mandates might help some, but the core issue is that 1st-round job interviews have gone remote and aren’t coming back. The best solution I can think of is raising the acceptance rate for papers, which in recent history has been well under 20%.

In terms of the actual economic research, two sessions stood out to me:

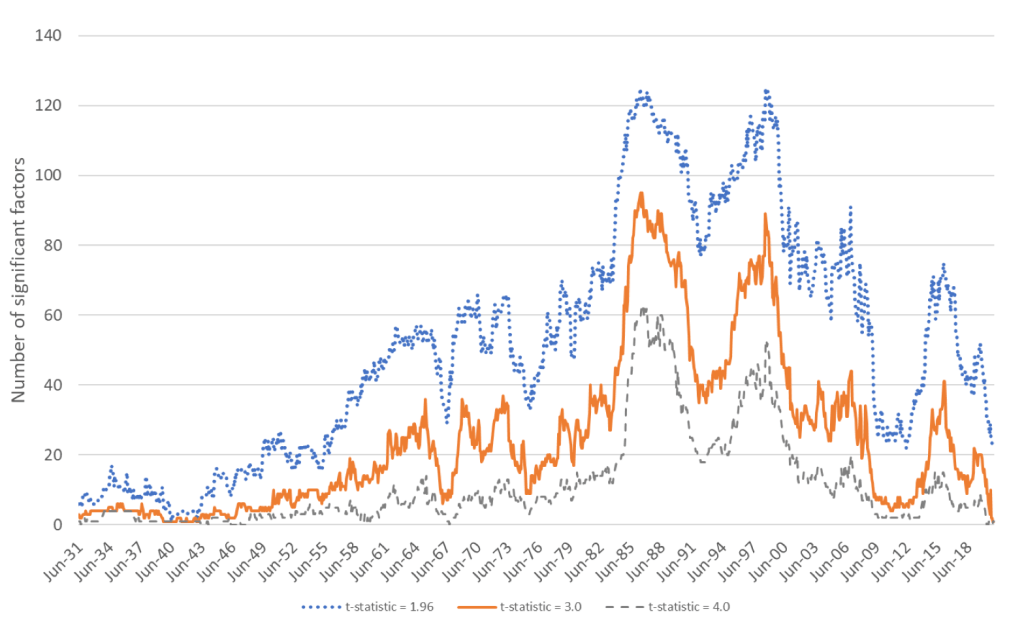

How many factors are there in the stock market? Classic work by Fama and French argues for 3 (size, value, and market risk), but the finance literature as a whole has identified a “zoo” of over 500. Two papers presented one after the other at ASSA argued for two extremes. “Time Series Variation in the Factor Zoo” argues that the number of factors varies over time, but is quite high, typically over 20 and sometimes over 100:

In contrast, “Three Common Factors” argues that there really are just 3 factors, though they are latent and not the same as the Fama-French 3 factors. In this case, the whole zoo of factors in the literature is mostly non-robust results driven by p-hacking and a desire to find more factors (fortune and fame potentially await those who do). Overall these asset pricing papers make me want to look into all this myself; when reading them I’m always struck by an odd mix of reactions- “I don’t understand that”, “why would you do it that way, it seems wrong and unnecessarily complicated”, and “why didn’t the field settle such a seemingly basic question decades ago?”.

Hayek: A Life this session covered the new book by Bruce Caldwell (who taught me much of what I know of the history of economic thought) and Hansjoerg Klausinger. Discussants Emily Skarbek and Stephen Durlauf agreed it is surprisingly readable for a long work of original scholarship, calling it a beautifully written 800p pageturner. Vernon Smith asked Caldwell if Hayek read the Theory of Moral Sentiments. Caldwell: “he cited it.” Smith: “but did he read it? Seems like he didn’t understand it very well.” Caldwell agreed he may not have, or if he did it was a German translation.

Vernon Smith’s own talk featured great comments on market instability: instability in markets comes from retrading. Markets are stable when consumers just value goods for their use, like haircuts and hamburgers. The craziness and potential for bubbles and crashes comes in when people are thinking about reselling something, whether it be tulips, stocks, houses, or crypto.

I asked Bruce Caldwell at a reception how he was able to finish writing such a big book that involved lots of archival work and original research. He said “one chapter at a time”, and noted that its fine to write the easiest chapters first to get the ball rolling.

Overall, while ASSA is diminished from the pre-Covid days and I often disagree with the AEAs decisions, its still a top-tier conference, especially when in New Orleans.

Today the largest annual gathering of economists begins, in-person for the first time in 3 years. It won’t be as big as the pre-Covid conferences, but I’m excited to spend a few days in New Orleans for the first time since I moved away in 2017. I lived there for 4 years; in the eventful 5 years since my knowledge likely became somewhat out of date, but I hope I can still provide some guidance for those new to the city.

For most people the main destination is the French Quarter. People are right about this; it is great to walk through to see the old colonial buildings, hear the street music, and eat the food. Some of the ASSA hotels are in the Quarter, but for those staying downtown or in the Warehouse district its definitely worth the walk. The Quarter is a big, diverse place, not only for tourists. Bourbon Street is the tourist trap. It is probably worth seeing once, but be prepared for crowds, loud music, and touts trying to get you into bars and strip clubs. The standard advice now is to skip Bourbon St and hang out on Frenchman street instead- which is in the Marigny, just east of the Quarter. There are two blocks entirely packed with bars / jazz clubs. Any evening you will have at least 5 shows to choose from, usually jazz, usually with no cover. Café du Monde is the other Quarter attraction that everyone does, and with good reason. They have decent coffee, and great beignets (a donut / fried dough sort of thing drowned in powdered sugar). There is often a long line to get a table or to get to-go, but usually not for both at once. There is a river walk just south of Café Du Monde, and the Jackson Brewery building is just east- there is a good place to sit and look at the river beside their food court.

In a short trip it would be entirely reasonable to just stay in the Quarter. But if you’d like to get out, the main attraction of New Orleans to me is the parks. Audobon Park is west of the Quarter in Uptown. It stretches from the Mississippi river to the Tulane and Loyola campuses. City Park is north of the Quarter in Mid-City, and is home to the Art Museum and Sculpture Garden. Both can be reached by trolley, and both are full of lovely ponds and interesting waterfowl. At the big lake in city park you can rent kayaks, or get a ride in a gondola.

People associate New Orleans with Cajun food, but most of the Cajuns settled to the west. The traditional New Orleans cuisine is Creole- a blend of the Italian, French, and other settlers. When I think about what makes restaurants attractive, I think about three things- food, prices, and everything else (service, wait times, ambience). In New Orleans it is very easy to find places with great food at good prices, but rare to find good places that also have short wait times and good service (Commander’s Palace, the best restaurant in the city, is already booked solid). My restaurant recommendations are the thing most likely to be out of date, so I’ll keep it short:

Central Grocery- original home of the Mufalleta, a creole sandwich. In the French quarter.

Dat Dog- fancy hot dogs (mostly sausages) with more toppings than you could ever want to choose from (including crawfish etouffee). One location is on Frenchman St- you can often hear live jazz from the bars by while sitting on their balcony. Cheap.

Hotel Monteleone- classy bar, often with live jazz, home to the rotating Carousel bar. One of many good places to try old New Orleans cocktails like the Sazerac. I’ll be staying here trying to get a spot on the Carousel.

New Orleans is unlike anywhere else in the US, almost like a Caribbean island (it practically is an island, surrounded by lakes, rivers, and swamps). The highs (food, music, knowing how to have a good time) are higher than just about anywhere else here, though the lows are also lower. One of the most special things about it is Mardi Gras. Mardi Gras day isn’t until February 21st this year, but Mardi Gras is really a whole season in New Orleans- and the first parade, Krewe of Joan of Arc, starts right in the Quarter on Friday January 6th (Twelfth Night).

Enjoy the city, and let me know if you’d like to meet up.