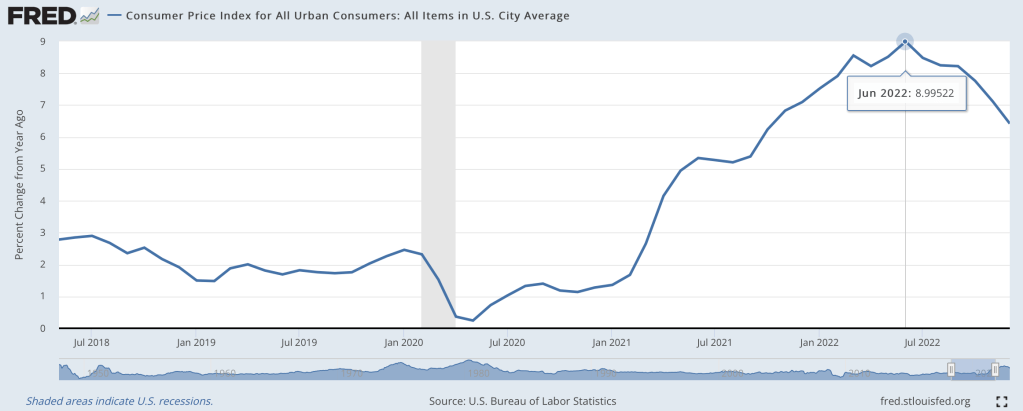

Last June I wondered if we were seeing the peak of inflation, and by at least one major measure I called the peak exactly:

At the moment, though, I’m feeling more confused than prophetic. The big question a year ago was how long it would take the Fed to get inflation down to reasonable levels, and how much collateral damage they would do to the real economy in that effort. Today most current indicators make it look like they pulled off the miraculous “soft landing”. Inflation over the last 12 months is still high, but over the last 6 months we’re nailing the Fed’s 2% annualized target. This has hit a few sectors of the real economy hard, with housing slowing dramatically and tech doing mass layoffs, but the overall picture is great: GDP growth was around 3% the last 2 quarters, and the 3.4% unemployment is the lowest since 1969.

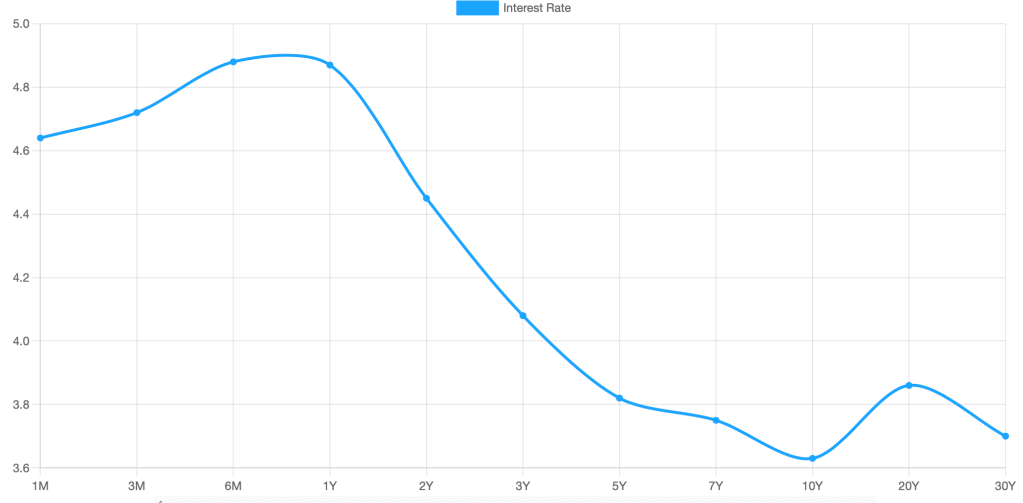

What’s confusing about this is that we have a hard time believing we really got this lucky. Its like your plane lost power, you diverted course for an emergency crash landing, and once you touch down and find yourself seemingly unharmed you look around and wonder if the plane is about to explode. Consumer sentiment is worse than it was in the depths of Covid; business sentiment has been falling for over a year and is almost down to March 2020 levels. Betting markets forecast a 50% chance of a recession in 2023, and the yield curve is strongly inverted (one of the best predictors of a recession, though the guy who first noticed this says it might not work this time):

Finally, M2 money supply is shrinking for the first time since at least 1960, and I believe the first time since the Great Depression. This bodes well for inflation continuing to moderate, but its also one more indicator of a potential recession.

To sum up, most of the indicators of the current state of the economy look great, while most indicators of its near-term future look awful. So which do we trust?

My guess is that we avoid recession in 2023, but honestly this is mostly the gut feeling of an optimist. There’s no one knock-down piece of data I’d point to in support; its more that things are currently going well, and usually the best prediction is that tomorrow will be like today unless you have a good reason to think otherwise. The main reason people expect a slowdown is because of the Fed’s actions to fight inflation. The Fed itself predicts that they will cause a slowdown, but not a recession. Their most recent summary of economic projections from December predicts GDP growth slowing to 0.5% in 2023 and unemployment rising to 4.6%.

I think the “so what” outlook is also murky. Stocks have already fallen a lot from their highs and a recession already seems somewhat ‘priced in’, so even if I thought one was coming I wouldn’t necessarily sell stocks. On the flip side US stocks are still quite expensive by historical standards, so I don’t want to buy more on the assumption that they’ll rise more on good economic news this year. You might want to lock in decent rates on long-term bonds if you think the Fed will cut rates in response to a recession, but the inverted yield curve shows this is already somewhat priced in. 1-year bonds yielding almost 5% seems decent in either scenario, I have some and I’ll probably buy more, but 5% returns are nothing to get excited about. I’d like to hear suggestions but to me the small direct betting market on a potential recession is the clearest “so what” for anyone who does have a confident view about this year’s macro picture.

Good post.

So long as AD grows at a smooth rate (see url), I’m not too worried about a Fed-caused recession. IMO, any recession will be minor, sectoral, or caused by a real shock.

https://fred.stlouisfed.org/graph/?g=100PD

LikeLike