Small, rural, private schools stand out to me as the most likely to show up on lists of closed colleges. This summer I discussed a 2020 paper by Robert Kelchen that identified additional predictors using traditional regression:

sharp declines in enrollment and total revenue, that were reasonably strong predictors of closure. Poor performances on federal accountability measures, such as the cohort default rate, financial responsibility metric, and being placed on the most stringent level of Heightened Cash Monitoring

Kelchen just released a Philly Fed working paper (joint with Dubravka Ritter and Doug Webber) that uses machine learning and new data sources to identify more predictors of college closures:

The current monitoring solution to predicting the financial distress and closure of institutions — at least at the federal level — is to provide straightforward and intuitive financial performance metrics that are correlated with closure. These federal performance metrics represent helpful but suboptimal measures for purposes of predicting closures for two reasons: data availability and predictive accuracy. We document a high degree of missing data among colleges that eventually close, show that this is a key impediment to identifying institutions at risk of closure, and also show how modern machine learning algorithms can provide a concrete solution to this problem.

The paper also provides a great overview of the state of higher ed. The sector is currently quite large:

The American postsecondary education system today consists of approximately 6,000 colleges and universities that receive federal financial aid under Title IV of the federal Higher Education Act…. American higher education directly produces approximately $700 billion in expenditures, enrolls nearly 25 million students, and has approximately 3 million employees

Falling demand from the demographic cliff is causing prices to fall, in addition to closures:

Between the early 1970s and mid-2010s, listed real tuition and fee rates more than tripled at public and private nonprofit colleges, as strong demand for higher education allowed colleges to continue increasing their prices. But since 2018, tuition increases have consistently been below the rate of inflation

Most college revenue comes from tuition or from state support of public schools; gifts and grants are highly concentrated:

Research funding is distributed across a larger group of institutions, although the vast majority of dollars flows to the 146 institutions that are designated as Research I universities in the Carnegie classifications…. Just 136 colleges or university systems in the United States had endowments of more than $1 billion in fiscal year 2023, but they account for more than 80 percent of all endowment assets in American higher education. Going further, five institutions held 25 percent of all endowment assets, and 25 institutions held half of all assets

Now lets get to closures. As I thought, size matters:

most institutions that close are somewhat smaller than average, with the median closed school enrolling a student body of about 1,389 full-time equivalent students several years prior to closure

As does being private, especially private for-profit (states won’t bail you out when you lose money):

As do trends:

variables measuring ratios of financial metrics and those measuring changes in covariates are generally more important than those measuring the level of those covariates

When they throw hundreds of variables into a machine learning model, it can predict most closures with relatively few false positives, though no one variable stands out much (FRC is Financial Responsibility Composite):

My impression is that the easiest red flag to check for regular people who don’t want to dig into financials is “is total enrollment under 2000 and falling at a private school”.

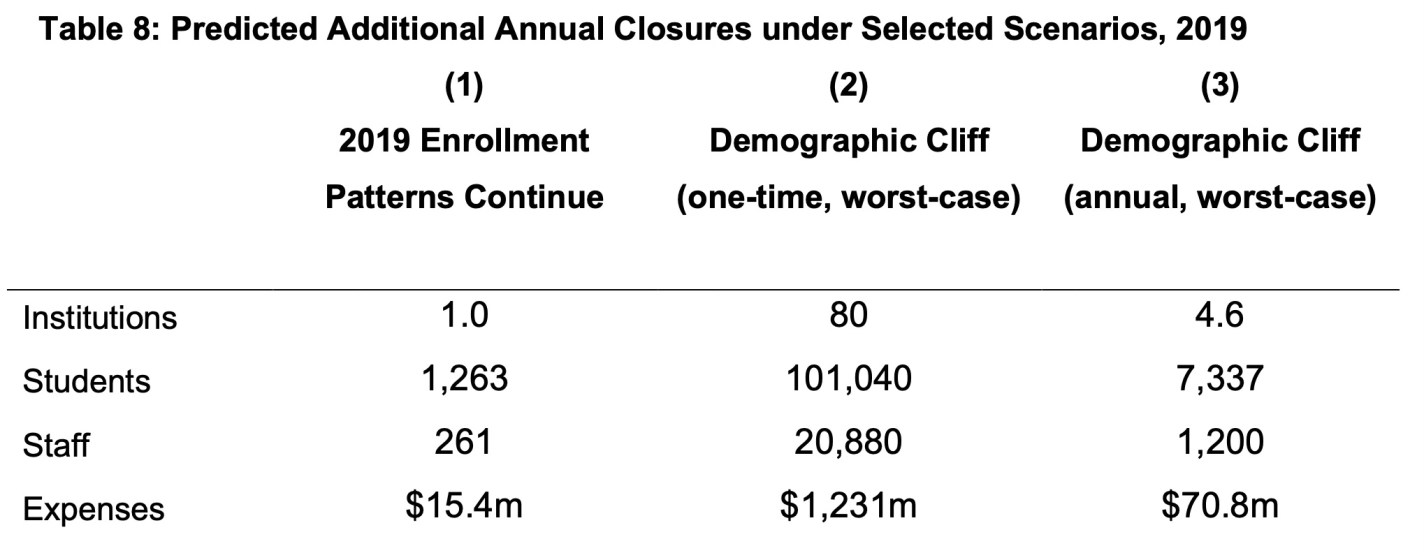

They predict that the coming Demographic Cliff (the falling number of new 18-year-olds each year) will lead to many more closures, though nothing like the “half of all colleges” you sometimes hear:

The full paper is available ungated here. I’ll close by reiterating my advice from the last post: would-be students, staff, and faculty should do some basic research to protect themselves as they consider enrolling or accepting a job at a college. College employees would also do well to save money and keep their resumes ready; some of these closures are so sudden that employees find out they are out of a job effective immediately and no paycheck is coming next month.

That’s the title of a recent book by Liran Einav and Amy Finkelstein, subtitled “Rebooting American Health Care”. I reviewed the book for Independent Review; the short version of my review is that while I don’t agree with all of their policy proposals, the book makes for an engaging, accurate, and easily readable introduction to the current US health care system. Here’s the start of the review:

Liran Einav and Amy Finkelstein are easily two of the best health economists of their generation. They have each spent twenty years churning out insightful papers published in the top economics journals. As a young health economist, I would read their papers and admire how well they addressed the technical issues at hand, but I was always left wondering what they thought about the big picture of health care in the United States….

The book’s prologue describes how Finkelstein’s father-in-law finally bullied her into writing on the topic, using almost the exact words I always wanted to: “I know these are hard issues. But come on … You’ve been studying them for twenty years. You must be one of the best placed people to help us understand the options. Do you really have nothing to say on this topic?”

The conclusion:

I learned a lot reading the book, despite having already studied U.S. health financing for over a decade—for instance, that the first compulsory health insurance program in the U.S. was a 1798 law pushed by Alexander Hamilton to cover foreign sailors. While the authors are more used to writing math-heavy academic papers, We’ve Got You Covered reads like the popular press book it is. Perhaps the highest endorsement comes from a non-academic family member of mine who picked up the book and noted, “These are not dry writers … this doesn’t sound like a book written by economists, no offense.”

The full review is free here, the book is for sale here.

The US Federal government has been considering major reforms like the REINS Act, which would require Congressional approval of major regulations proposed by executive branch agencies, or bringing back the “two in one out” rule from the first Trump administration. What would these do?

Right now it’s hard to say much for sure. But similar reforms have already been implemented in the states; as usual, the states provide a laboratory for investigating how policies work and whether they deserve broader adoption. It’s especially valuable to inform the debate over reforms like the REINS act that are still being considered at the federal level. Even for federal reforms that have already happened, it can be easier to evaluate the state version, since states make better control groups for each other than other countries do for the US.

But so far we’ve mostly been ignoring our laboratory results from recent state regulatory reforms. For instance, Broughel, Baugus, and Bose (2022) released a dataset that could be used to evaluate state regulatory reforms, but it has only been cited 3 times. This is why I’m adding this to my ideas page as a good subject for future academic research. Do state REINS or Red Tape Reduction Acts actually reduce either the stock or flow of regulation? If so, which types of regulations are affected, and does this have any effect on downstream measures like economic growth or new business formation?

Any research along these lines could help inform policy debates in the states, as well as for a new Presidential administration coming in with hopes of boosting economic growth through deregulation.

I offer a cleaned version of the state-level NSDUH in Stata .dta and Excel .xlsx formats here.

The NSDUH is mostly quite good as government datasets go- they share individual-level data in many formats and with the option to get most years together in a single file. But due to privacy concerns, the individual-level data doesn’t tell you what state people live in, which means it can’t be used to study things like state policy. SAMHSA does offer a state-level version of their data, but it is messy and only available in SAS format. So I offer the 1999-2019 state-level NSDUH Small Area Estimation Dataset in Stata .dta and Excel .xlsx formats here.

If you have Stata I recommend using that version, since the variables are labelled, making it much easier to understand what they represent.

This is the latest addition to my data page, where you can find cleaned/improved versions of other government datasets.

I thought this was going to be another election post, but it didn’t turn out that way.

My plan was to do another annual portfolio review, with a focus on changes I’ll make to my portfolio as a result of how the election impacts various market themes, and how my take on the election differs from the market’s take. But as I looked at my portfolio, what struck me wasn’t how the election changes things, but instead how severely my stock picks underperformed the incredible 26% return the S&P has posted so far this year.

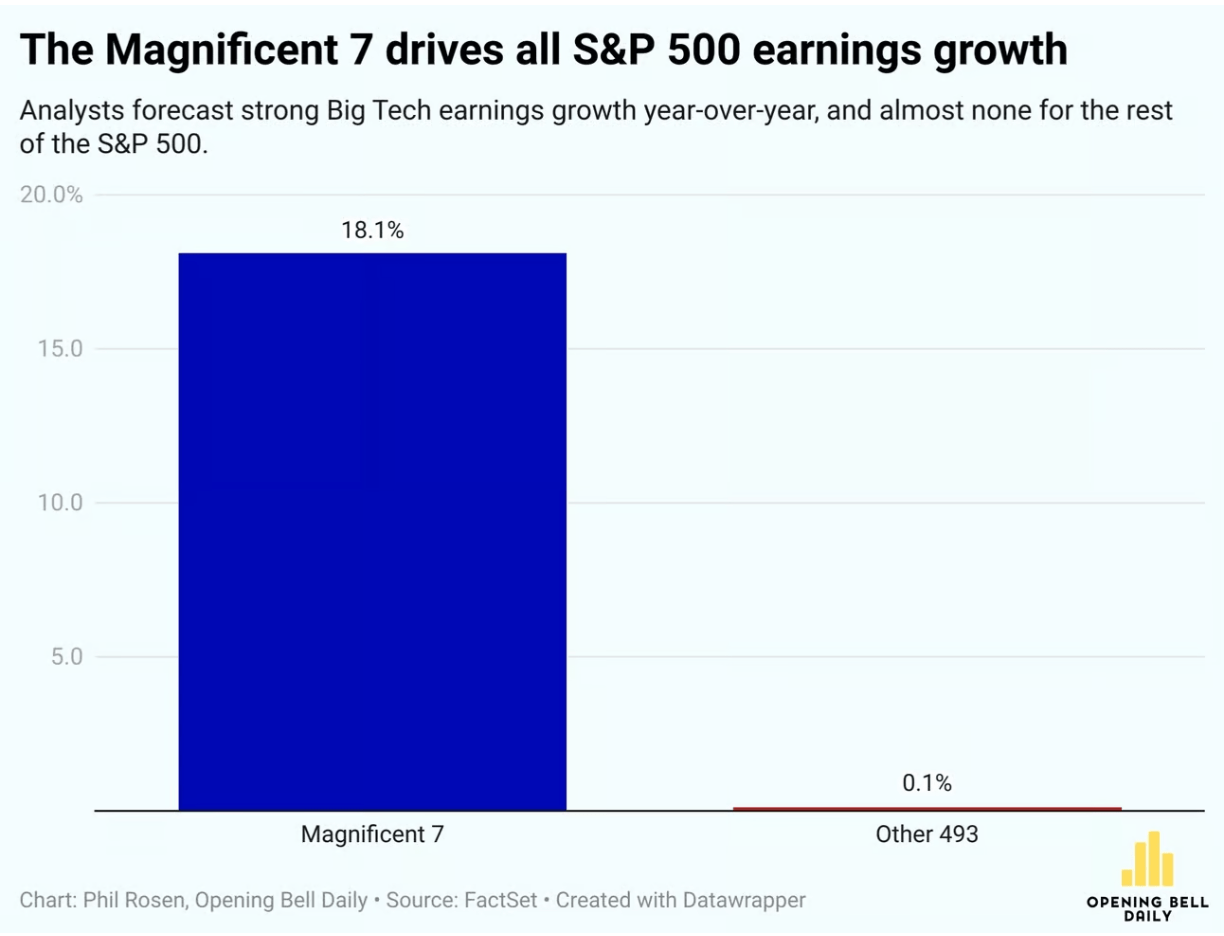

My first couple years of stock picking tended to match the S&P, roughly what you’d expect if markets are efficient and I’m just throwing darts. But more recently so much of the overall return of the market has been driven by just 7 mega-cap stocks, the “Magnificent 7”, that if you don’t own them you are probably underperforming big time.

Of course buying a broad index, especially a market-cap-weighted one like the S&P, is a way to ensure you own at least a piece of the big winners, which is one reason economists usually recommend buying the broad index. And I did this with 80% of my portfolio, to match my 80% belief in the efficient markets hypothesis. But I’m now back up to 90% belief in efficient markets, at least for stocks.

This efficiency seems to change a lot over time. Probably fewer than 10% of US stocks have obvious mis-pricings right now; really none stand out as super mispriced to a casual observer like me. Instead, it seems like every 10 years or so a broad swathe of the market is driven crazy by a bubble or a crash, and you get lots of mispricing- like tech in 2000, forced/panic selling at the bottom in 2009, or meme stocks in 2021. The rest of the time, the stock market is quite efficient. So, in typical times, just be boring and buy and hold a broad index fund.

Of course, you might think that AI is a bubble now. I certainly don’t love the 68 P/E on NVIDIA, but this doesn’t strike me as a true bubble driven by irrational hope- peoples’ hopes have proven well justified so far, with AI performing miracles and the Mag 7 delivering huge profits. So like Scott, I’m finally giving up on being overweight value stocks. Perhaps our capitulation is the sign that growth’s decade-plus run is finally about to reverse; but if so, I’ll try not to regret it. After all, the S&P has plenty of value stocks too.

Last week I laid out my own expectations for what economic policy would look like in a Trump or Harris presidency. Now after yesterday’s market reaction, we can infer what market participants as a whole expect by roughly doubling the size of yesterday’s market moves. Prediction markets had a 50-60% change of Trump winning as of Tuesday morning’s market close, which moved to a 99+% chance by Wednesday morning. Look at how other markets moved over the same time, multiply it by 2-2.5x, and you get the expected effect of a Trump presidency relative to a Harris presidency. So what do we see?

Stocks Up Overall: S&P 500 up 2%, Dow up 3%, Russell 2000 (small caps) up 6%. My guess this is mostly about avoiding tax increases- the odds that most of the Tax Cuts and Jobs Act gets renewed when it expires in 2025 just went way up. Lower corporate taxes boost corporate earnings directly, while lower taxes on households mean that they have more money to spend on their stocks and their products. Lower regulation and looser antitrust rules are also likely to boost corporate earnings.

Bond Prices Down (Yields Up): 10yr Treasury yields rose from 4.29% to 4.4%. This is the flip side of the tax cuts- they need to be paid for, and markets expect they will be paid for through deficits rather than cutting spending. The government will issue more bonds to borrow the money, lowering the value of existing bonds.

Dollar Up: The US dollar is up 2% against a basket of foreign currencies. I think this is mostly about the expected tariffs. People like the sound of the phrase “strong dollar” but it isn’t necessarily a good thing; it makes it cheaper to vacation abroad, but makes it harder to export, even before we consider potential retaliatory tariffs.

Crypto Way Up: Bitcoin went up 7% overnight, Ethereum is now 15% up since Tuesday. Crypto exchange Coinbase was up 31%. Markets anticipate friendlier regulation of crypto, along with a potential ‘strategic Bitcoin reserve’.

Single Stock Moves: Private prison stocks are up 30%+. Tesla is up 15%, mostly due to Elon Musk’s ties to Trump, but also due to tariffs. Foreign car companies were way down on the expectation of tariffs- Mercedes-Benz down 8%, BMW down 10%, Honda down 8%.

Sector Moves: Steel stocks are up on the expectation of tariffs, while solar stocks (which can’t catch a break, doing poorly under Biden despite big subsidies and big revenue increases) were down 12% in the expectation of falling subsidies. Bank stocks did especially well, with one bank ETF up 12%. This gives us one hint on what to me is now the biggest question about the second Trump administration- who will staff it? I could see Trump appointing free-market types, or wall-streeters in the mold of Steve Mnuchin, or dirigiste nationalist conservatives in the JD Vance / Heritage Foundation mold, or an eclectic mix of political backers like Elon Musk and RFK Jr, or a combination of all of the above. The fact that bank stocks are way up tells me that markets expect the free-marketers and/or the Wall-Street types to mostly win out.

Just Ask Prediction Markets: If you want to know what markets expect from a Presidency, you can do what I just did, look at moves the big traditional markets like stocks and bonds and try to guess what is driving them. But increasingly you can skip this step and just ask prediction markets directly- the same markets that just had a very goodelection night. Kalshi now has markets on both who Trump will nominate to cabinet posts, as well as the fate of specific policies like ‘no tax on tips‘

I doubt anyone has been waiting for my take on the Trump and Harris economic plans to decide their vote. More than that, it is entirely reasonable to vote based on things other than their economic plans entirely- like foreign policy, character, or preservingdemocracy. But either Trump or Harris will soon be President, and thinking through their economic plans can help us understand how the next 4 years are likely to go.

The bad news is that both campaigns keep proposing terrible ideas. The good news is that, thanks to our system of checks and balances, most of them are unlikely to become policy. The other good news is that our economy can handle a bit of bad policy- as Adam Smith said, there’s a lot of ruin in a nation. After all, the last Trump admin and the Biden-Harris admin did all sorts of bad economic policies, but overall economic performance in both administrations was pretty good; to the extent it wasn’t (bad unemployment at the end of the Trump admin, bad inflation at the beginning of Biden-Harris), Covid was the main culprit.

Note that this post will just be my quick reactions; the Penn Wharton Budget Model has done a more in-depth analysis. They find that Harris’ plan is bad:

We estimate that the Harris Campaign tax and spending proposals would increase primary deficits by $1.2 trillion over the next 10 years on a conventional basis and by $2.0 trillion on a dynamic basis that includes a reduction in economic activity. Lower and middle-income households generally benefit from increased transfers and credits on a conventional basis, while higher-income households are worse off.

We estimate that the Trump Campaign tax and spending proposals would increase primary deficits by $5.8 trillion over the next 10 years on a conventional basis and by $4.1 trillion on a dynamic basis that includes economic feedback effects. Households across all income groups benefit on a conventional basis.

We are already running way too big a deficit; candidates should be competing to shrink it, not make it worse. This isn’t just me being a free-market economist; Keynes himself would be saying to run a surplus in good economic times so that you have room to run a deficit in the next recession.

Now for my lightning round of quick reactions:

No tax on tips: both campaigns are now proposing this; it is a silly idea, there is no reason to treat tips differently from other income. The good news is that this almost certainly won’t make it through Congress.

Taxes: Trump’s Tax Cuts and Jobs Act of 2017 is set to expire in 2025. He says he wants to renew it and add more tax cuts, though he will need a friendly Congress to do so. Harris wants to let most of it expire, but renew and expand the Child Tax Credit while raising taxes on the wealthy and corporations. There’s a good chance we end up with divided government, in which case probably only the most popular parts of TCJA (increased standard deduction and child tax credit) get renewed and no big new changes happen.

Price controls: both campaigns, especially Harris‘, have talked about fighting ‘price gouging’, leading economists to worry about the price controls (any intro micro class explains why these are a bad idea). My guess is that no real bill gets passed, President Harris gets the FTC to make a show of going after grocery stores but nothing major changes.

Tariffs: Harris would probably leave them where they are; Trump is promising to raise them 10-20% across the board and 60% on China. This would lead to higher prices for US consumers and invite retaliation from abroad; we saw the same things when Trump raised tarriffs in his first term, but he is promising bigger increases now. This is worrisome because the President has a lot of power to change tariffs unilaterally; it would take a bill getting through Congress to stop this, and I don’t see that happening.

Regulation / One in two out: The total amount of Federal regulation stayed fairly flat during the Trump administration thanks to his one in two out rule, while regulation increased during the Biden-Harris administration. I expect that a second Trump admin would behave like the first here, while a Harris admin would continue the Biden-Harris trend.

Antitrust: FTC and DOJ have been aggressive during the Biden-Harris administration, blocking reasonable mergers and losing a lot in court. But Trump’s VP candidate JD Vance thinks FTC Chair Lina Khan is “doing a pretty good job”, so we could see this poor policy continue either way. More generally, voters should consider what a Vance presidency would look like, because making him Vice President makes it much more likely (Trump is 78 and people keep trying to shoot him; plus VPs get elected President at high rates).

Immigration: Immigration rates have been high under the Biden-Harris admin, while Trump’s top two planks in his platform are “seal the border” and “carry out the largest deportation operation in American history”. Economically, this would lead to a reduction in both supply and demand in many sectors, with the relative balance (so whether prices go up or down) depending on the sector. The exclusion of Mexican farmworkers in the 1960’s led to a huge increase in mechanization, to the point that domestic farmworkers saw no increase in their wages; presumably this also limited the potential harm to the food supply.

Crypto: The Biden admin has been fairly negative on crypto; both Harris and Trump are making pro-crypto statements in their campaigns, particularly Trump.

Marijuana: The Biden admin is in the process of rescheduling marijuana to no longer be in the most restricted category of drugs. I think Trump would probably see the process through, while Harris definitely would.

Elon Musk / Civil Service: Elon Musk has thrown his support hard behind Trump, spending lots of money, tweeting continuously, and attending rallies. It’s hard to know how much of this is genuine support for a range of Trump’s policies, how much is to get the Federal government to stop suing his companies so much, and how much is to get himself a direct role in government. In any case, it is a safe bet that more Federal civil servants get fired in a Trump admin than in a Harris admin. What’s much harder to say is how many get fired, and what proportion of firings come from a genuine attempt to improve efficiency vs a purge of those Trump sees as disloyal. Personally I think government could stand to treat its employees a bit more like the private sector, making it easier to fire people for genuine poor performance (not political views), but also allowing for more flexibility on improved pay, benefits, and the ability to focus on achieving goals more than following the way things have always been done. But I doubt that’s on the table either way.

CFTC/ Prediction Markets: The Biden CFTC has tried to crack down on prediction markets, though they have mostly failed in the courts, and the growth of Kalshi and Polymarket mean that prediction markets are now bigger than ever. Most of the anti-prediction-market decisions have been 3-2 votes of the democrats vs the republicans, so a new republican appointee could lock in the legal gains prediction markets have made, though this is far from guaranteed (not all Rs support this).

Final Thoughts: So much of how things turn out will depend not just on who wins the Presidency, but on whether their party wins full control of Congress. Because the Democrats have a lot more Senate seats up for grabs this year, Harris is much more likely to be part of a divided government (especially once you consider the Supreme Court).

Because of this, and because of the ability of the President to raise tariffs unilaterally, I see Trump as the bigger risk when it comes to economic prosperity, as well as non-economic issues. Harris with a Republican Senate is the best chance of maintaining something like the status quo, whereas a Trump victory is likely to see bigger changes, many of them bad.

That said, predicting the future is hard, and this applies doubly to Presidential terms. I’m struck by how often in my lifetime the most important decisions a President had to make had nothing to do with what the campaign was fought over. Who knew in 1988 that the President’s biggest task would be managing the breakup of the Soviet Union? In 2000, that it would be responding to 9/11? Bush specifically tried to distinguish himself from Gore as being the candidate more against “nation-building”, then went on to try just that in Afghanistan and Iraq. In 2004, who knew that the biggest issue of the term would be not Social Security or foreign policy, but a domestic financial crisis and recession? In 2016, who knew that they were voting on the President that would respond to the Covid pandemic? In 2020, who knew that they were voting on who would respond to Russia’s invasion of Ukraine?

The most important issue for the next President could easily be how they address China or AI, because those are clearly huge deals. I won’t vote based on this, because I don’t know who has the better plan for them, because I have no idea what a good plan looks like. Or the most important issue could be something that comes completely out of left field, like Covid did. Not even the very wise can see all ends.

What I do know is that, while much of the Libertarian Party has recently gone from its usual “goofy-crazy” to “mean-crazy“, Chase Oliver is so far the only candidate pandering to me personally. But it’s not too late for other politicians at all levels to try the same.

See you all again next Thursday, by which time the election will, I hope, be over.

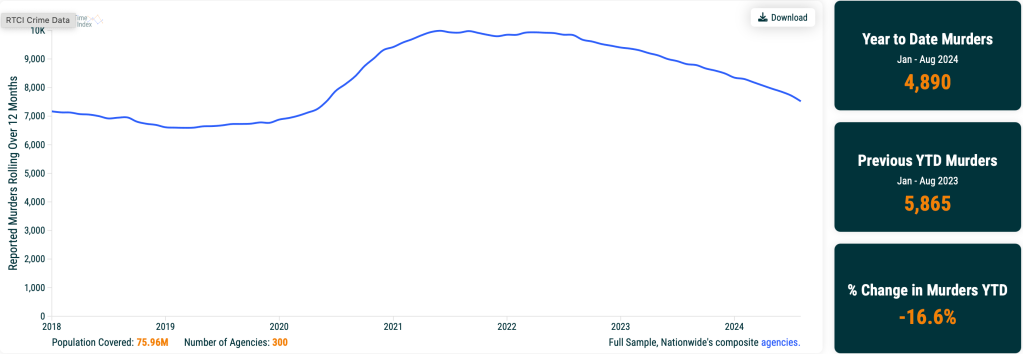

If you want to know how many pigs were killed in the United States yesterday, the USDA has the answer. But if you want to know how many humans were killed in the US this month, the FBI is going to need a year or two to figure it out. The new Real Time Crime Index, though, can tell you much sooner, by putting together the faster local agency reports:

Trends currently look good, though murders still aren’t quite back to pre-2020 levels.

In addition to graphing top-line state and national trends, the Real Time Crime Index also offers the option to download a CSV with city-level data going back to 2018. This seems like a great resource for researchers, worthy of adding to my page of most-improved datasets.

Kalshi just announced that they will begin paying interest on money that customers keep with them, including money bet on prediction market contracts (though attentive readers here knew was in the works). I think this is a big deal.

First, and most obviously, it makes prediction markets better for bettors. This was previously a big drawback:

The big problem with prediction markets as investments is that they are zero sum (or negative sum once fees are factored in). You can’t make money except by taking it from the person on the other side of the bet. This is different from stocks and bonds, where you can win just by buying and holding a diversified portfolio. Buy a bunch of random stocks, and on average you will earn about 7% per year. Buy into a bunch of random prediction markets, and on average you will earn 0% at best (less if there are fees or slippage).

This big problem just went away, at least for election markets (soon to be all markets) on Kalshi. But the biggest benefit could be how this improves the accuracy of certain markets. Before this, there was little incentive to improve accuracy in very long-run markets. Suppose you knew for sure that the market share of electric vehicles in 2030 would over 20%. It still wouldn’t make sense to bet in this market on that exact question. Each 89 cents you bet on “above 20%” turns into 1 dollar in 2030; but each 89 cents invested in 5-year US bonds (currently paying 4%) would turn into more than $1.08 by 2030, so betting on this market (especially if you bid up the odds to the 99-100% we are assuming is accurate) makes no financial sense. And that’s in the case where we assume you know the outcome for sure; throwing in real-world uncertainty, you would have to think a long-run market like this is extremely mis-priced before it made sense to bet.

But now if you can get the same 4% interest by making the bet, plus the chance to win the bet, contributing your knowledge by betting in this market suddenly makes sense.

This matters not just for long-run markets like the EV example. I think we’ll also see improved accuracy in long-shot odds on medium-run markets. I’ve often noticed early on in election markets, candidates with zero chance (like RFK Jr or Hillary Clinton in 2024) can be bid up to 4 or 5 cents because betting against them will at best pay 4-5% over a year, and you could make a similar payoff more safely with bonds or a high-yield savings account. Page and Clemen documented this bias more formally in a 2012 Economic Journal paper:

We show that the time dimension can play an important role in the calibration of the market price. When traders who have time discounting preferences receive no interest on the funds committed to a prediction-market contract, a cost is induced, with the result that traders with beliefs near the market price abstain from participation in the market. This abstention is more pronounced for the favourite because the higher price of a favourite contract requires a larger money commitment from the trader and hence a larger cost due to the trader’s preference for the present. Under general conditions on the distribution of beliefs on the market, this produces a bias of the price towards 50%, similar to the so-called favourite/longshot bias.

We confirm this prediction using a data set of actual prediction markets prices from 1,787 market representing a total of more than 500,000 transactions.

Hopefully the introduction of interest will correct this, other markets like PredictIt and Polymarket will feel competitive pressure to follow suit, and we’ll all have more accurate forecasts to consult.

Other than being the smallest state, of course. In other places I’ve lived, it was more obvious what made them stand out. Boston has the most high-quality universities, including the oldest one (though it is expensive and traffic-ridden). New Orleans has the best food, live music, and festivals (though terrible crime and roads). I’ve lived in Rhode Island since 2020 and I’ve enjoyed how it seems to have no big negatives the way many other places do- it’s been pretty nice all around. But it has been harder to see anything where Rhode Island really stands out.

What should a tourist see or do here that they couldn’t do elsewhere? The Italian food is great, but that’s true of several other cities. You can find Portuguese food here in a way you can’t in most of the US. Probably the Cliff Walk in Newport is our best entry: a 3-mile trail along cliffs where you can see the Atlantic on one side, and Gilded-age mansions on the other.

For those living here, what stands out is the compactness. This makes sense for the smallest state, but it is even more true than you would expect, because even within Rhode Island most people are clustered within the small portion of the state that is within 5 miles of Providence.

Because of this, I almost never feel the need to drive more than 10 miles or 20 minutes; this wasn’t so true any of the other ~dozen places I’ve lived. I can easily walk to the Bay, the Zoo, and my kids’ school; then its a 20 minute drive or less to work, several good hospitals and universities, sailing, several beaches, forest hikes, the state capital, the excellent airport, Amtrak, every good grocery store, leaving the state, et c. Most other places either lack some of those things entirely or involve longer drives to get to them, though probably there’s somewhere else like this I don’t know about.

Or perhaps the best thing about Rhode Island is our people:

What do you think I missed about Rhode Island? Or if you haven’t been here, what do you think is most special about where you live?