Wall Street analysts love to get out ahead and tout The Next Big Thing. Earlier this year it was Generative AI that was going to Change Everything. I am old enough to remember a surge of enthusiasm when fractal number sets were going to Change Everything (“How did we manage to get along without fractals?” was a question that was really asked), so I tend to underreact to these breathless hot takes.

Well, The Next Big Thing as of last week seemed to be the new generation of weight loss drugs. With names like Ozemic and Wegovy and Mounjaro (who thinks up these names, anyway?), these are mainly GLP-1 blockers which up till now have been mainly used in treating Type 2 diabetes.

From the august Mayo Clinic:

These drugs mimic the action of a hormone called glucagon-like peptide 1. When blood sugar levels start to rise after someone eats, these drugs stimulate the body to produce more insulin. The extra insulin helps lower blood sugar levels.

Lower blood sugar levels are helpful for controlling type 2 diabetes. But it’s not clear how the GLP-1 drugs lead to weight loss. Doctors do know that GLP-1s appear to help curb hunger. These drugs also slow the movement of food from the stomach into the small intestine. As a result, you may feel full faster and longer, so you eat less.

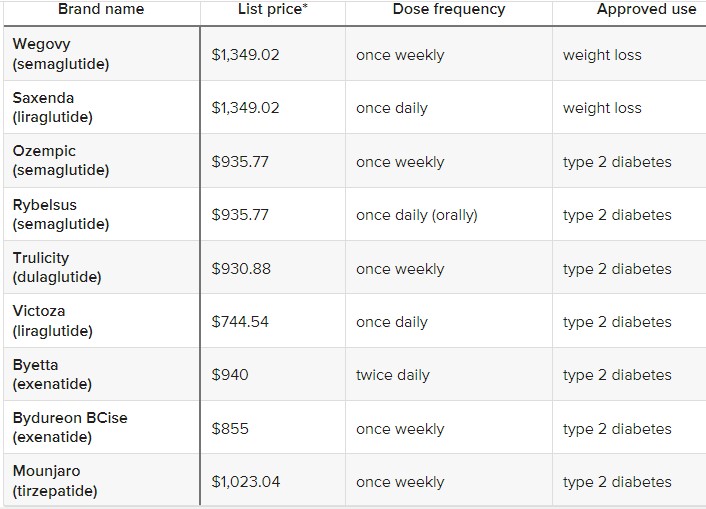

I’ll append a table at the end with a bunch of these drug names, for reference. At this point, most of them are only FDA approved for diabetes treatment, but are being prescribed off-label for weight control. It is no secret that obesity is rampant in America, and is spreading in other regions. The knock-on health problems of obesity are also well-known. So, these treatments might be very helpful, if they pan out.

What does Wall Street think of all this? Well, there is first the potential profit to accrue to the makers of these wonder drugs. You typically take them via daily or weekly skin injections, similar to insulin shots. A month’s worth of these meds may cost a cool $1000. Cha-ching right there, for makers like Novo Nordisk and Eli Lilly.

But wait, there’s more – Jonathan Block at Seeking Alpha calls out a number of possible financial angles for these drugs:

While at first glance the impact of these medications — known as GLP-1 agonists — might just impact food and beverages, the reality is that they could influence many other consumer industries.

Apparel retailers, casino/gaming names, and even airlines are just some of the industries that could see an impact from the growing popularity of weight loss drugs.

The thinking is that folks who lose 15 pounds will go out and buy a whole new wardrobe, which is good for clothing makers and retailers. On the other hand, gambling is highly correlated with obesity, so maybe casino business will fall off. There are claims that kidney health is so improved with these drugs that purveyors of dialysis equipment may be under threat.

Fuel represents some 25% of airlines’ expenses, so somebody with a sharp pencil at Jefferies sat down and calculated that for one airline (United) the cost savings would be $80 million per year if the average passenger shed 10 pounds. And who know, if people get really thinner, maybe the airlines can pack in an extra row of seats…

A concern over declining food sales has cut into the prices of companies like Walmart:

Analysts estimate that nearly 7% of the U.S. population could be on weight loss drugs by 2035, which could lead to a 30% cut in daily calorie intake due to the consumption changes for the targeted group. There is also some conjecture that the increased attention to dieting and weight loss in general could have a downstream impact on the consumption of snacks and sweets.

Real World Efficacy of Weight Loss Drugs May Fall Short of Clinical Trials

Throwing buckets of cold water on these scenarios of slenderized Americans is a study by RBC Capital Markets suggesting that the actual impact of these meds may be much less than indicated by clinical trials:

“Unlike clinical studies, insights from real-world use of these drugs imply weight loss can be limited or short-lived as a result, making it difficult for some users to justify the treatment’s lofty price tag,” RBC analyst Nik Modi said. “Recent insurance claims data on 4k+ patients who started taking GLP-1s in 2021 indicate only 32% remained on therapy and just 27% adhered to treatment after 1 year, citing an increase in healthcare costs.” He mentioned one study on 3.3k subjects that found after a year on the drugs, patients saw an average of just 4.4% weight loss. That is significantly less than declines cited by Novo Nordisk (NVO) and Eli Lilly (LLY) in their studies.

Also, he said IQVIA data found that the growth in GLP-1s is due mostly to new prescriptions, not refills, “making us question its sustainability.” Given this information, “we believe GLP-1s have genuine hurdles to prolonged use that have the potential to limit their long-term societal/economic impact.” To back up his argument, Modi provided several real-life examples of drugs or products where hype that it would shake up a consumer segment ended up falling flat.

The clinical trials for the GLP-1 blockers were paid for by the manufacturers, so they tend to be skewed to the positive. It is not clear whether these flattish real-world results are due to the drugs themselves not being so effective, or to other factors. These factors include side effects, unpleasantness of self-injection, and the huge out-of-pocket cost (~ $12,000/year). Weight loss drugs are often not covered by insurance, since obesity is considered a behavioral outcome, not a disease.

My guess is the final outcome will fall somewhere between mass weight loss and nothing. We hope that progress continues to be made in this area, since so many other health conditions are worsened by being overweight. For instance, fellow blogger Joy Buchanan recently linked to an article by Matt Iglesia in which he described significant and long-lasting weight loss from bariatric surgery.

And as promised, that list of diabetes/weight-loss meds: