Who’s your favorite artist? Warhol? Picasso? Van Gogh? Maybe someone much earlier, such as Michelangelo or Titian? Of course, there is something about the style or subjects that you enjoy. But something about the artist’s personal life might also matter to you. Personally, I’m a fan of Hieronymus Bosch, about whom we know little, and William Blake, who had some social and political opinions that would still be considered liberal even today.

Picasso, Dalle, and Warhol were all eccentric. Picasso had multiple girlfriends who didn’t get along, Dalle enjoyed exemplifying surrealism in his dress and behavior, and Warhol was a reclusive hoarder. Their eccentricity increases their allure and fosters an aura of mystique that they are privy to some unknown truths.

Li Yining, Chinese reformer, helped re-establish the Chinese stock market

Padma Desai, Indian reformer and scholar of planning

Rebecca Blank, labor economist, UW chancellor, acting US Secretary of Commerce

Harry Markowitz, won Nobel for “pioneering work in the theory of financial economics” (finding the risk-return optimal frontier for a portfolio)

Not all the biggest names, but all important enough that I knew of them despite not working in their subfields and, unfortunately, not having met them personally.

Let me know if I’m currently missing anyone, though let’s hope the list doesn’t get much longer by the end of 2023.

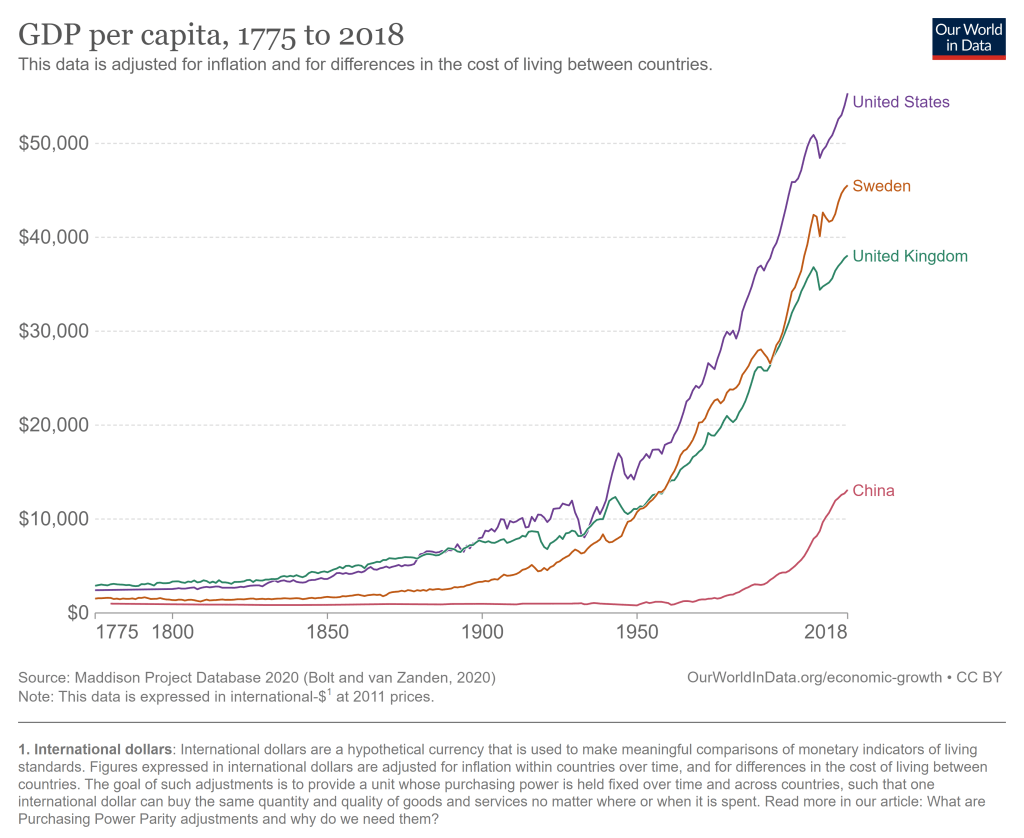

The United States has problems and always had. But the historical record of the United States as an economic powerhouse is unrivaled. The US had a bit of a head start on economic growth, being a direct descendant of the country that really kicked of the Industrial Revolution. But we took that head start and really ran with it, now being by far the highest income large country, and the highest income country that does not derive a significant part of its GDP from fossil fuels or being a tax haven.

The average American has, as best as we are able to measure it, a standard of living that is at least 20 times greater than Americans when this country began.

There is a narrative about US history that goes like this: “Historical racism was really bad and limited opportunities for blacks. Blacks were not allowed to participate in a set of occupations and other civic life. The absence of blacks from typically higher income occupations reduced the number of competitors in those sectors. Not only did blacks have fewereconomic opportunities, the whites who were insulated from competition earned monopoly rents. Therefore, if blacks were excluded, the whites who were in exclusive sectors earned profits at the expense of blacks.”

The logic is neat. Are there any holes in it?Let’s see.

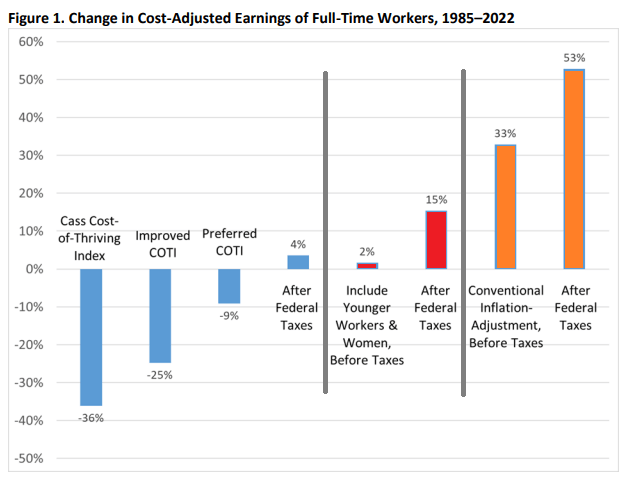

Last week my post was about a new article I have with Scott Winship on the “cost of thriving” today versus 1985. That paper has gotten quite a bit of coverage, including in the Wall Street Journal, which is great but also means you are going to get some pushback. Much of it comes in the form of “it just doesn’t feel like the numbers are right” (see Alex Tabarrok on this point), and that was the conclusion to the WSJ piece too.

Here’s a response of that nature from Mish Talk: “There’s no way a single person is better off today, especially a single parent with two kids based on child tax credits that will not come close to meeting daycare needs.”

He mentions daycare costs, but never comes back to it in the post (it’s mostly about housing costs). Daycare costs are undoubtedly an important cost for families with young children (though since Cass’ COTI is about married couples with one earner, they may not be as relevant). And in the CPI-U, daycare and preschool costs only getting a weight of 0.5%. Surely that’s not reality for the families that actually do pay daycare costs! If only there was an index that applied to the costs of raising children.

In fact, there already is. Since 1960, the USDA has been keeping track of the cost of raising a child. Daycare costs are definitely given much more weight: 16% of the expenditures on children got to child care and education. And much of that USDA index (recently updated by Brookings) looks similar to what COTI includes: housing, food, transportation, health care, education, but also clothing and daycare. I wrote about it in a post last year and compared that cost to various measures of income (including single-earner families and median weekly earnings). But what if we compared it to Oren Cass’ preferred measure of income, males 25 and older working full-time? Here’s the chart.

62 weeks. That’s how long the median male worker would need to work in a year to support a family in 2022, according to the calculations of Oren Cass for the American Compass Cost-of-Thriving Index released this year. Not only is 62 weeks longer than the baseline year of 1985 (when it took about 40 weeks, according to COTI), but there is a big problem: there aren’t 62 weeks in year. It is, by this calculation, impossible for a single male earner to support a family.

Is this true? In our new AEI paper, Scott Winship and I strongly disagree. First, we challenge the 62-week figure. With a few reasonable corrections to Cass’ COTI, we show that it is indeed possible for a median male earner to support a family. It takes 42 weeks, not 62 as reported in COTI.

But wait, there’s more. Much more. In our paper, we provide a range of reasonable estimates for how the cost of thriving has changed since 1985. In the COTI calculation, the standard of living for a single-earner family has fallen by 36 percent since 1985. In our most optimistic estimate, the standard of living has risen by 53 percent. The chart below summarizes our various alternative versions of COTI. How do we get such radically different results? Is this all a numbers game?

On summer vacation, I recently visited Mount Rushmore. It’s amazing structure, and the story of its construction is as impressive as the monument itself. Much of the story you learn when visiting is the story of its creation. As an economist, of course seeing the following display with wage data got me very excited:

While the sign says that laborers made 30 cents per hour, searching online it appears that 50 cents was more common. More skilled workers, such as assistant sculptors, made $1.50 per hour. These were, as the sign says, “good wages” for that time. In the economy generally, production workers made around 50 cents per hour our as well around that time period, and most of the construction of Rushmore was during the Depression (some of the workers were WPA funded), so having any job, much less one that paid pre-Depression wages, was certainly a good one.

How does this compare to wages today? This is always a tricky question, as I have documented on this blog several times before, but the most straight forward approach (and good first approximation) is a simple CPI inflation adjustment. Using 1929 as the baseline year, when construction was in full swing, 30 cents an hour is roughly $5 today, 50 cents per hour is close to $9, and $1.50 would be about $26.50. That doesn’t sound too bad!

The best comparison I like to use is BLS’s average hourly earnings for private production and non-supervisory workers. Averages aren’t perfect, but this measure excludes management occupations that will be distorting the average. In May 2023, that wage was $28.75 per hour. So the average worker today earns 3-6 times as much per hour as these “good paying jobs” in the late 1920s and the Depression. And, as the Rushmore signage notes, these jobs were seasonal. Their off-season jobs probably paid even less.

The wage of the assistant sculptor does compare well with average wages today, but that pay was unusual for the time and was likely a highly skilled worker. The only record I can find of anyone making that much at Rushmore was Lincoln Borglum, the son of the main sculptor Gutzon Borglum. Lincoln oversaw the completion of the project after Gutzon’s death, and it was only in later years on the project that his pay was increased to $1.50 per hour.

For the typical laborer on Rushmore, having a good job was indeed good to have, but the wages pale in comparison to a typical worker today.

In November 1738, clothier Henry Coulthurst informed weavers that he was cutting their piecework rates and would henceforth pay them in goods rather than cash. Needless to say, they were upset. Food prices were rising, and lower wages meant hunger and want.

Over three days in December, the weavers rioted. They smashed Coulthurst’s mill, wrecked his home, and “drank, carried out, and spilt, all the Beer, Wine and Brandy in the cellars.” They returned the following day to demolish Coulthurst’s house…

Wow. Our paper on cutting nominal wages is called “If Wages Fell During a Recession” We ran an experiment in which workers could retaliate if they experienced a nominal wage cut. They did! They couldn’t smash their employer’s house, but some of the slighted workers dropped their effort level down to the minimum level which meant that their employer made no more money in the experiment.

In my talk at IUE (show notes here and YouTube video), I connect the wage cut paper to another experiment on beliefs. One wonders, considering how serious the consequences turned out to be for Henry Coulthurst, why he was not able to anticipate the backlash against wage cuts. Being wrong was costly for him.

People are not always good at appreciating how strongly others have become attached to their own reference points. That’s why the paper on beliefs is called “My Reference Point, Not Yours“

Getting long-run historical PE ratios of US stocks by industry seems like the kind of thing that should be easy, but is not. At least, I searched for an hour on Google, ChatGPT, and Bing AI to no avail.

I eventually got monthly median PEs for the Fama French 49 industries back to 1970 from a proprietary database. I share two key stats here: the average of median monthly industry PE 1970-2022, and the most recent data point from late 2022.

Industry

Long Run Mean

End 2022

AERO

12.14

19.49

AGRIC

10.75

9.64

AUTOS

9.65

17.52

BANKS

10.38

10.46

BEER

15.23

35.70

BLDMT

12.00

15.41

BOOKS

12.95

17.60

BOXES

12.18

10.69

BUSSV

12.07

13.03

CHEMS

12.40

19.26

CHIPS

10.48

17.47

CLTHS

11.45

10.94

CNSTR

8.98

4.58

COAL

8.04

2.92

DRUGS

1.14

8.01

ELCEQ

10.78

17.85

FABPR

10.28

19.40

FIN

11.16

12.97

FOOD

14.30

25.03

FUN

9.10

21.06

GOLD

3.18

-5.95

GUNS

11.50

5.05

HARDW

7.96

19.16

HLTH

11.91

6.09

HSHLD

12.60

20.15

INSUR

10.95

16.33

LABEQ

13.46

25.18

MACH

12.51

20.27

MEALS

13.83

19.19

MEDEQ

6.81

27.64

MINES

8.06

16.27

OIL

6.96

9.00

OTHER

12.20

27.68

PAPER

12.50

16.69

PERSV

12.86

-0.65

RLEST

8.13

-0.30

RTAIL

12.26

8.58

RUBBR

12.11

12.81

SHIPS

9.79

17.42

SMOKE

11.74

17.79

SODA

12.38

32.09

SOFTW

8.21

-2.85

STEEL

8.18

4.30

TELCM

6.75

9.58

TOYS

9.18

-1.32

TRANS

11.25

13.11

TXTLS

9.43

-49.00

UTIL

12.34

17.41

WHLSL

11.08

13.13

Mean Industry Median

10.52

12.73

One obvious idea for what to do with this is to invest in industries that are well below their historical price, and avoid industries that are above it (not investment advice). Looking just at current PEs is ok, but a stock with a PE of 8 isn’t necessarily a good value if its in an industry that typically has PEs of 6.

By this metric, what looks overvalued? Money-losing industries (negative current earnings): Gold, Personal Services, Real Estate, Software, Toys, and Textiles. Making money but valuations 19+ above historical average: Medical Equipment, Beer, Soda. Most undervalued relative to history: Guns, Health, Coal, Construction, Steel, Retail (all 3+ below the historical average).

Of course, I don’t recommend blindly investing in these “undervalued” industries- not just for legal reasons, but because sometimes the market prices them low for a reason- that earnings are expected to fall. The industry may be in secular decline due to new types of competition (coal, steel, retail). Or investors may expect it to get hit with a big cyclical decline in an upcoming recession or rotation from the Covid goods/manufacturing economy back to services (guns, construction, steel, retail). Health services (as opposed to drugs and medical equipment) stands out here as the sector where I don’t see what is driving it to trade at barely half of its usual PE.

I’d still like to get data on long run market-cap weighted mean PE by industry, as opposed to the medians I show here. The best public page I found is Aswath Damodaran’s data page, which has a wide variety of statistics back to about 1999. Some of the current PEs he calculates are quite different from those in my source, another reason to tread carefully here. I’m not sure how much of this is mean vs median and how much is driven by different classification of which stocks fit in which industry category.

This gets at a big question for anyone trying to actually trade on this- do you buy single stocks, or industry ETFs? Industry ETFs make sense in principle (since we’re talking about industry level PEs overall) and also add built-in diversification. But the PE for the ETF’s basket of stocks likely differs from that of the industry as a whole. It would make more sense to compare the ETF’s current PE to its own historical PE, but most industry ETFs have very short track records (nothing close to the 53 years I show here). PE is also far from the only valuation metric worth considering.

All this gets complex fast but I hope the historical PE ratio by industry makes for a helpful start.

In the tapestry of human progress studies, two authors, Adam Smith and Virginia Postrel, have left their mark on the story of productivity and innovation. Their books, written centuries apart, both explore the power of specialization and the division of labor.

Part of the reason this came out this week is that I’m reading The Fabric of Civilization. So good! It had come highly recommended before, but I finally have an excuse to read it because I’m working on an article about fashion.