Incentives matter. I’ve taught at both public and private universities, and students have given me both great course evaluations and less great student evaluations. The private university cared a lot more about them. Obviously, some parts of student evaluations of their instructors are beyond the instructor’s control. The instructor can’t control inalienables and may not be able to change their charisma. But what about the things that instructors can control? Regardless of your current evals, here are 5 policies that are guaranteed to improve your course evaluations.

1: Very Clear Expectations/Schedule

Have all deadlines determined by the time that the semester starts. Students are busy people and they appreciate the ability to optimally plan their time. Relatedly, students desire respect from their instructor. Having clear rubrics and deadlines helps students know your expectations and how to meet them – or at least understand how they failed to meet them. Students want to feel like they were told the rules of the game ahead of time. This means no arbitrary deductions or deadlines. The syllabus is a contract if you treat it like one.

2: Mid-Semester Evaluations

One of the absolute best ways to improve your evaluation is to ask your evaluators for a performance update. Make a copy of your end-of-semester course evaluation and issue it about halfway through the semester. Then, summarize the feedback and review it with your class. This achieves three goals. (1) It is an opportunity to clarify policy if there are misplaced complaints. You may also wish to explain why policy is what it is. Knowing a good reason makes students more amenable to policies that they otherwise don’t prefer. (2) It provides voice to students who have things to say. Often, students want to be heard and acknowledged. It’s better that a student vents during the informal mid-semester survey than on the important one at the conclusion of the course. (3) If there are widespread issues with your course, then make changes. If you’re on the fence about something, then take a poll. And if you decide to make changes, then be graciously upfront about it. Unexplained or covert changes violate policy #1.

Lot’s of economists use FRED – that’s Federal Reserve Economic Data for the uninitiated. It’s super easy to use for basic queries, data transformations, graphs, and even maps. Downloading a single data series or even the same series for multiple geographic locations is also easy. But downloading distinct data series can be a hassle.

I’ve written previously about how the Excel add-on makes getting data more convenient. One of the problems with the Excel add-on is that locating the appropriate series can be difficult – I recommend using the FRED website to query data and then use the Excel add-on to obtain it. One major flaw is how the data is formatted in excel. A separate column of dates is downloaded for each series and the same dates aren’t aligned with one another. Further, re-downloading the data with small changes is almost impossible.

Only recently have I realized that there is an alternative that is better still! Stata has access to the FRED API and can import data sets directly in to its memory. There are no redundant date variables and the observations are all aligned by date.

At a Chinese restaurant, I got a fortune that said, “Success is in starting a new project at work.” It struck me as very funny, and it resonates with other people on Twitter.

Starting a new project at work does not translate to success in academia. The danger is usually in starting too many projects and finishing too few.

Starting a new research project, whether alone or with coauthors, is exciting. You fall in love with a new idea.

The hard part is sticking with that idea until the very end of the publication process. This is more comparable to staying married. The project will see you at your worst, and you will discover that the project is not as wonderful as it seemed initially. You might end up re-writing the manuscript several times, years after the initial infatuation has worn off.

Academics do need to start projects. It is important to start the right projects. A reason to not start too many projects is to preserve time for the best work. A downside to being overloaded is that you might have to say no to a new project when an actual good opportunity comes along.

In my post on the Beatles documentary Get Back, I observed the way that the bandmates start new songs together. It reminded me of coauthors convincing each other to start a new project.

Their creative process resembles co-authoring a research paper. When Paul is working out a song and humming through places he hasn’t worked the lyrics out yet, that reminds me of the early drafts of a paper. You don’t have to have the whole Introduction written. The hook of a song is a bit like the main result of a research paper. Persuading yourself and your coauthor that you have a project worth finishing is the first step. Coauthors have unspoken agreements on how the project is going to proceed. The tacit knowledge of the collaborative process is one of the most important things you can learn in graduate school.

This quote from Rules of Thumb was surprising: “None of this is part of a grand plan. At any moment, I work on whatever then interests me most. Coming up with ideas is the hardest and least controllable part of the research process. It is somewhat easier if you have broad interests.” He goes on to say: “I sometimes fear that because I work in so many different areas, each line of work is more superficial than it otherwise would be. Careful choice of co-authors can solve this problem to some extent, but not completely.”

He really refutes my fortune cookie with this line, “Deciding which research projects to pursue is the most difficult problem I face in allocating my time.” Success is about starting the right projects and no others.

I just found out I’ll be receiving a Course Buyout Grant from the Institute for Humane Studies. It will allow me to teach less next year in order to focus on my research on how Certificate of Need laws affect health care workers.

I’m happy about this because I think this research is valuable and time is my main constraint on doing it (especially doing it quickly enough to inform ongoing policy debates in several states). But I’m also happy because I finally got what I consider to be a “true” grant after many rejections.

I’ve received research funding many times before (e.g. Center for Open Science funding for replications), but it was always relatively small amounts that went directly to me. True grants tend to be larger and to be paid directly to the university. That’s the case with the course buyout grant, which essentially pays the university enough that they can hire someone else to teach my class.

I may have lost count but I’m pretty sure this was the 13th “true grant” I have applied for, and the 1st I will actually receive. Academics have to get used to rejection, since we need to publish and decent journals tend to reject 80%+ of the articles they receive. But for some reason I’ve found grants much harder even than that. From some combination of skill, luck, and targeting lower-tier journals than perhaps I could/should, my acceptance rate for journal articles is probably nearing 50%. I expected this to translate over to grants but it absolutely did not, they seem to be a much different ballgame, one I’m still figuring out.

I’d like to share some of those past misses, both to let junior people see the bumpy road behind success (like a CV of failures), and to try to extract lessons from an admittedly small sample. These proposals were not funded, and probably weren’t even close:

Peterson Foundation US 2050

MacArthur Foundation 100 & Change

RI INBRE (2x)

National Institute for Health Care Management (1x, waiting to hear but probably about to be 2x)

What did these failures of mine all have in common? Me, of course. This is not just a truism; in most of these cases I was applying for major grants solo as an assistant professor without previous funding. The usual advice is to work your way up with smaller grants or, preferably, as the collaborator of a senior professor with lots of previous funding who knows how things work. I knew that would be smart but I’ve tended to be at institutions without senior people in similar fields; almost all my research has either been solo or coauthored with students or assistant professors. Even my PhD advisor was a brand-new assistant professor when we started working together. I had good reasons for ignoring the usual advice to work with well-known seniors, and it has mostly served me well, but grants seem to be the exception.

Twice, I think I did come close on grant proposals, and both times it involved help from seniors at other institutions who had lots of previous funding. At one foundation that funds a lot of social science, my senior coauthor and I got glowing external reviews, but the internal committee rejected us on the grounds that we could do the project without their funding. They were right in the sense that we did do project anyway with no funding; it got published and even won a best paper award. But with their funding we would have done it faster and better and they would have gotten credit for it.

I do think it is smart for funders to consider whether the research would happen anyway without them, or whether their funding really improves things. But I think it is rare for funders to actually do this, and taking this rejection as advice probably led me to more rejections. I tried to propose bigger, more ambitious projects that needed expensive data so it was clear that I really needed the funding; but for most funders this probably made things worse. I have since heard several times that people who get lots of funding from major funders like NIH tend to submit proposals for research they have essentially already finished; that is why their proposals can look so thorough, credible, and polished. They then use the funding to work on their next project (and next proposal) instead of what they said it was for. That seems sketchy to me, but it’s certainly ethical to turn the proposal dial back somewhat toward “obviously achievable for me” from “ambitious and expensive”, and that’s what I’ve done more recently.

The other time I came close was with an R03 proposal to the Agency for Healthcare Research and Quality. First I got a not-close rejection, as I mentioned in the big list, where my proposal was “not discussed”. But AHRQ allows resubmission. At the prompting of my (excellent) grants office, I got feedback on the proposal from two kind seniors at other schools who get lots of funding. I rewrote the proposal based on their comments plus the rejection comments (which were actually quite detailed despite it being “not discussed”) and resubmitted it. This went way better- the resubmission got discussed with an impact score of 30 and a percentile of 17. Lower scores are better for AHRQ/NIH so this was pretty good, good enough that it might have been funded in a normal year, but 2019 was a bad year for government funding (though through some weird quirk I never actually got rejected; 4 years later their system still says “pending council review”). Again, the key to getting close was getting detailed feedback from people who know what they are talking about.

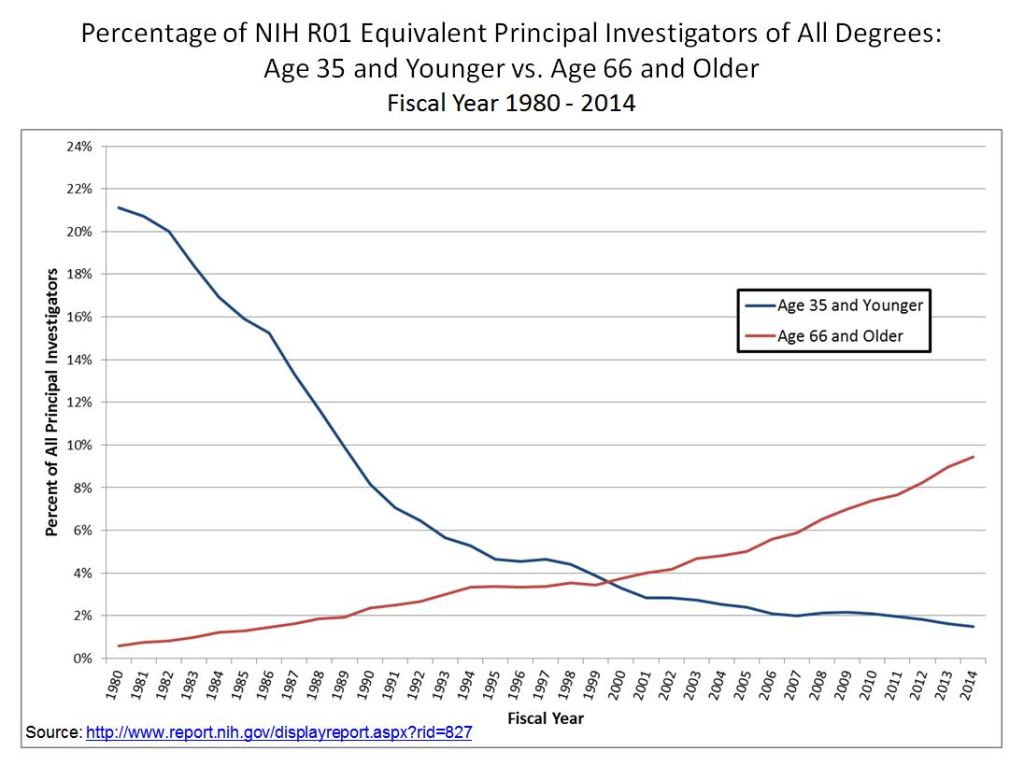

Of course, it also helps to get to know people at the funders and to become more senior yourself. It’s not surprising that my first major grant is coming from IHS given that I’ve been involved with them in all sorts of ways since going to a Liberty & Society seminar way back in 2009. Most funding goes to more senior people who have more connections, knowledge, and proven experience. This is extreme at perhaps the largest funder of research, the National Institutes of Health, where less than 2% of funded principal researchers are under age 36.

This may be the real secret for winning grants- just get older. My 12 rejections all came when I was younger than 36, while my first acceptance came less than a month after my 36th birthday.

In all seriousness, thanks to the Institute for Humane Studies, and I hope that a year from now I’ll be writing here about the great work that came out of this. For everyone with a growing pile of rejections, maybe the 13th time will be the charm for you too.

Economists overwhelmingly favor looser immigration controls. Allowing people to immigrate would improve the allocation of scarce labor and capital and it is a far cheaper way to aid poorer families than sending direct payments or trying to develop an entire country. Let’s cover some static analysis basics for migrating workers and their dependents.

Workers, Labor Markets, & Output Markets

There are two markets to consider: The new home country and the old home country. If workers leave the old country in search of the higher wages in the new country, then world employment remains unchanged. Employment obviously rises in the new country and falls in the old country. With identical laborers (a terrible assumption that’s the least charitable to immigration), wages in the new country fall and wages in the old country rise. This logic illustrates the cheap aid of which economists are fond.

One of the oldest theories in economics is the idea of compensating differentials. A job represents not just a certain amount of money per hour, but a whole package of positive and negative things. Jobs have more or less stability, flexibility, fun, room to grow, danger… and non-cash benefits like health insurance. The idea of compensating differentials is that, all else equal, jobs that are good on these other margins can pay lower cash wages and still attract workers (thus, the danger of doing what you love). On the other hand, jobs that are bad on these other margins need high wages if they want to hire anyone (thus, the deadliest catch)

I think this theory makes perfect sense, and we see evidence for it in many places. But when it comes to health insurance, everything looks backwards. A job that offers employer-provided health insurance is better to most employees than one that doesn’t, so by compensating differentials it should be able to offer lower wages. There’s just one problem: US data shows that jobs offering health insurance also offer significantly higher wages. The 2018 Current Population Survey shows that workers with employer-provided health insurance had average wages of $33/hr, compared to $24/hr for those without employer insurance.

All the economists are thinking now: that’s not a problem, compensating differentials is an “all else equal” claim, but not all else is equal here. The jobs with health insurance pay higher wages because they are trying to attract higher-skilled workers than the jobs that don’t offer insurance.

That’s what I thought too. It is true that jobs with insurance hire quite different workers on average:

The problem is, once we control for all the observable ways that insured workers differ, we still find that their wages are significantly higher than workers who don’t get employer-provided insurance. Like, 10-20% higher. That’s after controlling for: year, sex, education, age, race, marital status, state of residence, health, union membership, firm size, whether the firm offers a pension, whether the employee is paid hourly, and usual hours worked. I’ve thrown in every possibly-relevant control variable I can think of and employer-provided health insurance always still predicts significantly higher wages. Of course, there are limits to what we get to observe about people using surveys; I don’t get any direct measures of worker productivity. Possibly the workers who get insurance are more skilled in ways I don’t observe.

We can try to account for these unobserved differences by following the same person from one job to another. When someone switches jobs, they could have health insurance in both jobs, neither, only the new, or only the old. What happens to the wages of people in each of these situations? It turns out that gaining health insurance in a new job on average brings the biggest increase in wages:

What could be going on here? One possibility is that health insurance makes people healthier, which improves their productivity, which improves their wages. But we control for health status and still find this effect. The real mystery is that papers that study mandatory expansions of health insurance (like the ACA employer mandate and prior state-level mandates) tend to find that they lower wages. Why would employer-provided health insurance lower wages when it is broadly mandated, but raise wages for individuals who choose to switch to a job that offers it?

My current theory is that “efficiency benefits” are offered alongside “efficiency wages”. The idea of efficiency wages is that some firms pay above-market wages as a way of reducing turnover. Workers won’t want to leave if they know their current job pays above-market, and so the company saves money on hiring and training. But this only works if other firms aren’t doing it. The positive correlation of wages and insurance could be because the same firms that pay “efficiency wages” are more likely to pay “efficiency benefits”- offering unusually good benefits as a way to hold on to employees.

I still feel like these results are puzzling and that I haven’t fully solved the puzzle. This post summarizes a currently-unpublished paper that Anna Chorniy and I have been working on for a long time and that I’ll be presenting at WVU tomorrow. We welcome comments that could help solve this puzzle either on the empirical side (“just control for X”) or the theoretical side (“compensating differentials are being overwhelmed here by X”).

I recently bought a used desktop computer for what seemed like next to nothing. $240 for a machine more powerful than my much-more-expensive 2019 MacBook Pro, most notably due to its 32GB of RAM. Desktops have always been cheaper than equivalently powerful laptops, Windows computers cheaper than Macs, and used computers cheaper than new, so this isn’t totally shocking. But the extent of the difference still surprised me. For instance, buying a new desktop from Dell with similar specs to the used one I just got would cost $1399.

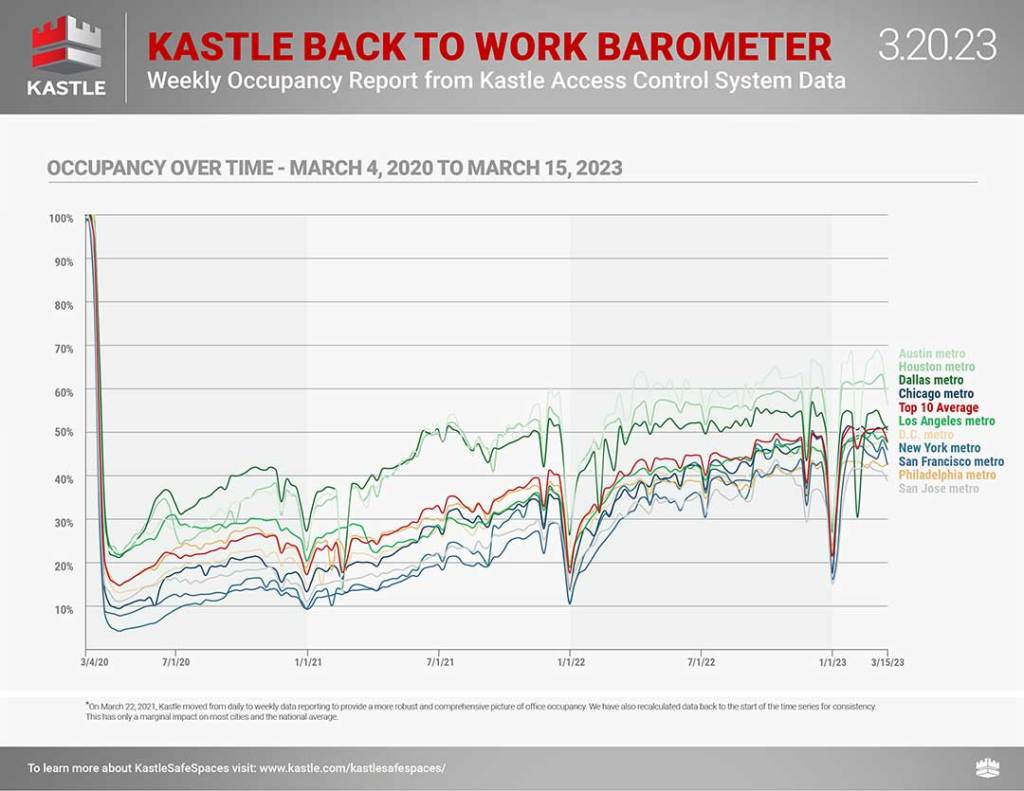

So why is the used discount so big right now? My guess is that its one more knock-on effect of work-from-home. Remote work has been the most persistent change from Covid, and there’s been a huge decline in the demand for office space, with occupancy rates still half of pre-Covid levels.

This means that offices are on sale relative to their pre-Covid prices. Office REITs are down 37% over the past year even after the Covid-induced drop of the previous two years. So it makes sense that all sorts of office equipment is on sale too. Offices tend to be full of employer-owned desktop computers, but when employees work from home they typically use their own machine or a company laptop. That means less demand for office desktops going forward, and a big overhang of existing office desktops that are being under-used. Employers realizing this may just sell them off cheap. Several things about the refurbished desktop I bought, such as its Windows Pro software, indicate that it used to be in an office.

Currently, we have software that can write software. What about physical machines that can produce physical machines? Indeed, what about machines that can produce other machines without human direction?

First of all, machines-building machines (MBM) still require resources: energy, transportation, time, and other inputs. A well-programmed machine that self-replicates quickly can grow in number exponentially. But where would the machines get the resources that enable self-replication? They’d have to purchase them (or conquer the world sci-fi style). Where would a machine get the resources to make purchases of necessary inputs? The same place that everyone else gets them.

I keep reading about how inflation has peaked (even peaked many months ago) and so any minute now the Fed will relent on raising interest rates, and will in fact start reducing them. Every data point that seems to support an early Fed pivot and a gentle “soft landing” for the economy is greeted with optimistic verbiage and a rip higher in stocks.

Except – – other meaningful data points regularly appear which show that inflation (especially core inflation) is remaining stubbornly high. The Personal Consumption Expenditures (PCE) Index is the Fed’s preferred way to track core inflation. It did peak in early 2022, and is falling, but very slowly and fitfully. Just when it seems like it is about to cascade downward, along comes another uptick. The latest report for 02/24/23 showed the PCE index (excluding the volatile categories of food and energy) increasing 0.6 percent during the month of January, which translated to a 4.7 percent year-on-year gain. That was considerably higher than the 0.4 percent monthly gain (4.3 percent year-on-year) that economists expected.

The chart below illustrates the chronic tendency of the economists at the Fed to lowball the estimates of future inflation. Each of the ten bars depicts quarterly projections of what inflation would be for 2023, starting back in September 2020 (first, green bar). No one in the craziness of 2020 could be held particularly responsible back then for accurately projecting 2023 conditions. But the Fed embarrassed themselves badly into late 2021 by airily dismissing inflation as “transitory”, due mainly to supply chain constraints that would quickly pass. (See towards the middle of the chart, yellow Sept 2021 and blue Dec 2021 bars projecting a mere 2.2% inflation for 2023.)

Only as of December 2022 did estimates of inflation jump up to 3.1% for 2023, and that estimate will surely get revised upward even further.

Many factors probably went into this systematic failure on the part of the Fed economists. There are probably political reasons for erring on the rosy optimistic side, which I will not speculate on here.

One factor in particular was mentioned in the Minutes of the Jan 31/Feb 1 Fed meeting that I thought was significant:

A few participants remarked that some business contacts appeared keen to retain workers even in the face of slowing demand for output because of their recent experiences of labor shortages and hiring challenges.

Jeremy LaKosh notes regarding this feature, “If true across the economy, the idea of keeping employees for fear of facing the labor force shortage would represent a fundamental shift in the employment market. This shift would make it harder for wage increases to mitigate towards historical norms and keep upward pressure on prices.”

This all rings true to my anecdotal observations. In bygone days, when business slowed down, factories would lay off or furlough workers, with the expectation on all sides that they would call the workers back (and the workers would come back) when conditions improved. However, employers have had to struggle so hard this past year to find willing/able workers, that employers are loath to let them go, lest they never get them back. I have read that even though homebuilders are not sure they can sell the houses they are building, they are so worried about losing workers that they are keeping them on the payroll, building away.

Other inflation data points show big decreases in prices for goods (and energy), but not for services. Wages, of course, are the big driver for service costs.

So the inflation story in 2023 seems to come down largely to a labor shortage. This is a large topic cannot be fully addressed here. I will mention one factor for which I have anecdotal support, that the enormous benefits (stimulus money plus enhanced unemployment) paid out during 2020-2021 set up a large number of baby boomers to leave the workforce early and permanently. Studies show that this is a major factor in the drop in workforce participation rate post-Covid. Maybe some of those folks had not planned ahead of time for such early retirement, but they got a taste of the good life (NOT getting up and going to work every day) in 2020-2021 along with the extra cash to pad their savings, and so they decided to just not return to work. That exodus of trained and presumably productive workers has left a hole in the labor force which now manifests as a labor shortage, which drives up wages and therefore inflation and therefore interest rates, which will eventually crater the economy enough that struggling firms will finally lay off enough workers to mitigate wage gains.

I wonder if this unhappy scenario could be staved off with increased legal migration of targeted skilled workers from other countries to alleviate the labor shortage. Dunno, just a thought.