I’m a big fan of Milton Friedman. I’m also a big fan of easy-to-remember phrases that impart great wisdom. It honestly made me wince the first time I said the following:

“Inflation is *not* everywhere and always a monetary phenomenon“.

The reasoning is as plain as day. Consider the quantity equation:

MV=PY

For the uninitiated, M is the money supply, V (velocity) is the average number of times dollars transacts during a period, P is the price level, and finally Y is real output during a period. This equation is often called the “equation of exchange” or “the quantity equation”. Strictly speaking, it is an identity. It is a truism that cannot be violated. All economists agree that the equation is true, though they may disagree on its usefulness.

Inflation is simply the percent change in price. We can rearrange the quantity equation, solving for price, in order to see the relationship between the price level and its determinants.

P= MV/Y

What does this mean? It means that more money results in more inflation, all else held constant. It means that higher velocity results in more inflation, all else held constant. It means that less output results in more inflation, all else held constant.

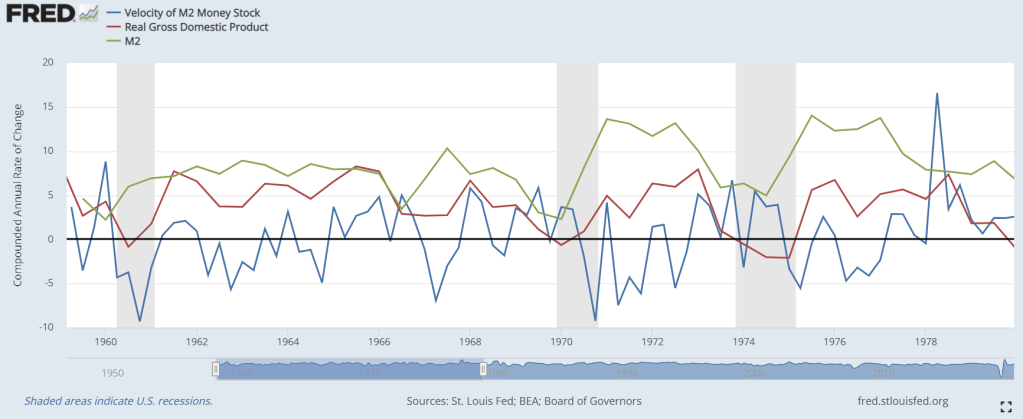

Why would Milton Friedman say that inflation is always caused by changes in the money supply if it is clear that there are two other causes of the price level? When Milton Friedman said his famous quote, output growth was relatively steady. Velocity growth was relatively steady. For his context, Milton Friedman was right. The majority of price and inflation volatility was found in changes in M. See below.

Strictly speaking however, Milton Friedman knew better and he knew that the statement was not strictly correct. Friedman was a public intellectual and he was a great simplifier. He taught many people many true things. At the time, people were blaming inflation on a great variety of things: taxes, fish catches, and unions, to name a few. Arguably, Friedman got them closer to the truth.

What does this mean? It means that higher NGDP results in more inflation, all else held constant. It means that less output results in more inflation, all else held constant.

But economists dismissing M in lieu of AD are committing the same oversimplification. Y can also change! Maybe economists figure that our recent history is full of relatively stable Y growth and that we ought not pay attention to it. And indeed, unsurprisingly, RGDP growth has been less than NGDP growth.

But what is driving the current bought of inflation?

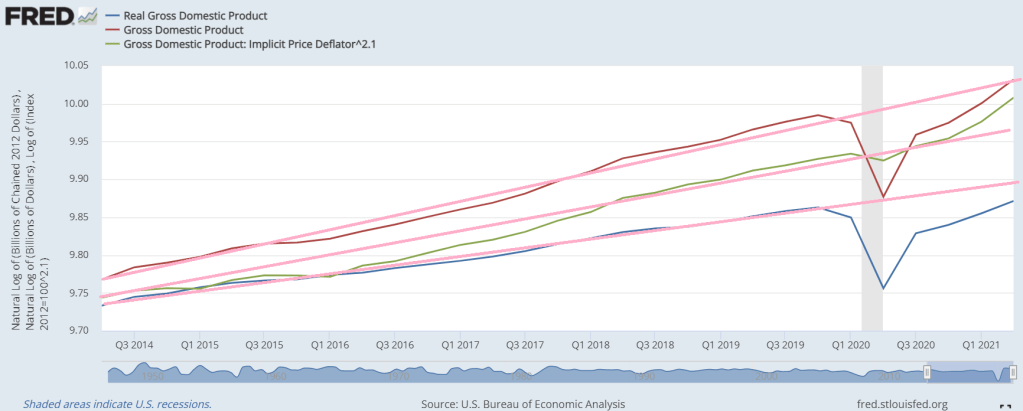

Pardon the crude image. The pink lines are eye-balled trend lines on natural logged data for AD, Y, and P. Prices are up. Is it because of exceptionally high NGDP? Nope. Total spending is back on pre-2020 trend. Does Y happen to be down? Yep, it sure is.

Right now, assuming the previous trend was anywhere close to potential output, inflation is not being driven by excess aggregate demand. It’s being driven by inadequate real output. The news tells the story. There have been supply-chain bottle-necks, difficulty employing, lockdowns, and fear of covid. Right now we have an output problem and higher prices are a symptom. We do not have an aggregate spending problem.

PS – In fact, it is my belief that the Fed successfully avoided a debt-deflation aggregate demand tumble that would have been catastrophic. Inflation is expected when supplies of goods decline.

Grade inflation in the US education system is a common observation, one that is, at least at the college level, largely undeniable. A couple recent interactions with students has brought it to the front of my mind again. When discussing their majors and what classes they were taking, there was considerable hesitation to take what were perceived as difficult classes. What I thought this called for, in the moment, was a bit of confidence building, for a professor such as myself to say “You can do it!”

It turns out confidence in their ability to learn the material was not the issue. What they were unsure of was their ability to get an A. No, to guaranteed get an A. It was the risk of a sub-A grade that concerned them (likely exacerbated by the fact that my university does not award + and – grades in undergraduate classes). So I went through my usual pitch:

You take 5 classes a semester for 8 semesters. That’s 40 classes. The cost of couple B’s or even a C will pale in comparison to the benefit acquiring more technical skills, which would pay out for a lifetime. A couple courses in computer science, econometrics and statistics, maybe real analysis for those thinking about a PhD in economics – these would all have huge payoffs. There was a problem with my logic, however, that quickly became apparent.

They weren’t sure what they wanted to do after their bachelors. They didn’t know what advanced degrees they might pursue, whether law or medical school was something they were interested in. What they did know, however, is that GPAs were really important. That students were applying to things they might be interested in, and doing so with 3.8 and 3.9’s. When they saw classes that regularly handed out C’s (not D’s or F’s mind you, just C’s), what they saw was pure downside risk. If they were great at something, no one would ever be able to tell. But if they weren’t, or if they had a bad day on a hard final exam, that it could close doors. What I inferred was that they were trying to maximize their expected outcomes, and in order to do so they had to minimize the number of hard classes in their portfolio. Each path had a handful of unavoidable hard classes, so to take a an additional hard class beyond the requirements of the path they chose was suboptimal.

I don’t know that they’re wrong.

I’ve told this story before. When I was considering getting a PhD in economics I planned on just going to my local school. I was visiting a friend on the opposite coast, though, and thought I’d stop in at a really good local school there. I met with the director of graduate studies in the economics department and was flatly informed that my application would not be read because my GPA (3.2, if you’re curious) was below their cutoff. I said thanks and left. It was some time later that it dawned on me that this was ludicrous. Did they simply never admit students from (the famously uninflated grades of) CalTech? Were they discriminating against math and engineering majors? Likely not. But this is deeper knowledge than that held by your typical undergraduate. All they know is the average admissions statistics and the implied (or in my case explicitly stated) cutoffs.

When we inflate grades and get rid of standardized tests, we put greater pressure on students to curate their education to expected grade outcomes and, more important, to minimize risk. There’s no upside to shining in a difficult class if the best 50% all get A’s. The signal value of success has been attenuated. The signal value of failure, however, has not just been left intact, it’s been heightened. There’s no positive variance to balance it out. There’s no way to be an excellent B+ student whose occasional C in risky classes are balanced out by some exemplary A’s. We’ve effectively raised the costs of taking challenging classes and in doing so discouraged students from acquiring the skills that are most rewarded in the marketplace.

The problem only becomes all the worse when we think about the cultural biases in the confidence we cultivate in different groups of students. If a deficiency in math and science has been low-key implied at every stage of your education, you’re that much less likely to incur the risk of “hard classes”. There’s much pearl-clutching over “everyone winning a trophy” and school being too easy from folks who walked to and from school through 12 months of snow, uphill both ways. Those arguments, which are often little more than a sort of grumpy money illusion, miss the real problem entirely. Undoing grade inflation to make school harder is like giving 7 points for every goal in soccer to make it more exciting.

The actual grades don’t matter. What matters is the the shape of the distribution of grades . If we bunch everyone in the A’s and then disproportionately select into institutions based on those grades, we’re incentivizing students to stay in the herd. To risk your GPA for the sake of hard classes is to risk being isolated. To risk being cutout by admissions committees trying to sort through 1000 applications, half of with have near-perfect GPA’s, and for whom the fastest way to make their workload manageable in an acceptable manner is cut out everyone with less than 3.7.

I’m not sure students are wrong in their grade-mongering. They got into college in many cases based on nothing but those GPAs. They’ll be able to go to grad school without taking the GRE. There will come a day, however, when the next step isn’t school, and after which no one will ever ask them their GPA again for the rest of their life. After which the only thing that will matter is what they know. And who will know more: the overconfident student of upper-middle class parents who graduated with a 2.8 BS in electrical engineering or the pragmatic student who curated courses to maximize their 3.7 GPA while preparing for the MCATS and medical school? I don’t know who will leave with more skills, but I also don’t worry about either. Who I worry about is the first-gen college student, the child of a working class household with a 4.0 BA and 4.0 MA in communications who, desperate to prove to others that they belonged in school, made sure to protect that perfect GPA at every turn. What have we done to ensure that they know enough when they enter the job market?

I sympathize with the sentiment of the meme. But friends of friends were quickly critical of it. Then I wasn’t sure what to believe. So, I crunched the numbers.

First of all, there is an inherent ambiguity in the meme’s claim, seeing as future tax rates, maximum taxable income, benefits, and plausible returns are unknown. But we can address the data so far. The meme is dated in 2019, but current data is even more charitable toward it.

What we know as of 2021:

The maximum annual benefit is currently $46,740. It was previously lower, but this is a charitable post.

We also know the historical tax rates and maximum taxable incomes. Currently, 12.4% and $142,800. YES, we’re about to assume that somebody met the maximum income criteria over their entire working life.

If someone worked for 40 years while making the maximum contribution each year, then they would have contributed $406,255.20. If we plainly calculate the rate of return on this amount, then we’d yield 11.5%, which is not too shabby ($46,740/$406,255.20). Of course, this is entirely unreasonable because the funds could have been earning interest in private hands during the contribution period. If the funds had been earning 5% throughout the entire period, then the 2021 value of the contributed funds would be $968,838.39. The annual benefit implies a return of 4.8% ($46,740/$968,838.39). Investing those funds in a private account that yielded 5% would have provided $48,441.92 per year, which is not a huge difference. In this light, social security appears not to be a terrible deal. Not as good as the private sector – but not far off.

Let’s be more charitable to the spirit of the meme. What about for 50 years of work? Then the total contribution would have been $423,905.38, yielding an implied return of 11%. Considering the time value of money changes the rate of return to 4.2%. Again, not terrible, but now noticeably less than 5%. If the funds had been invested at and paid out 5%, then the private annual benefit would be $55,846.56. In other words, the privately invested funds would have yielded an annual benefit that is 19.5% higher than what is currently paid. That is substantial. The social security investment is definitely not excellent.

How reasonable is the meme? Well, in order to get the $1.9M figure, interest rates would have to be 7.2% (assuming 50 years of work and that we don’t spend the principal). The concomitant annual retirement benefit would be $136,825.51 (Now that’s an exciting number). In order to get the $95k, we only need to assume 6.3% per year. The S&P 500 has yielded an annual return of 7.6% over the same period (not including dividends). The meme is reasonable. Not perfect. But not ridiculous.

One BIG caveat is that this entire analysis assumes that the employee could simply invest equivalent amounts if Social Security were abolished. This is very unreasonable. Currently, part of the contribution comes from employers. While employees would experience an increase in total pay if the taxes were abolished, the employer would also enjoy a lower cost of labor. Not all of the gains would go to the employee. One could also argue that abolishing Social Security would improve growth and real incomes generally, but that’s a counter-factual beyond the scope of this post.

And by cursory inspection of excerpts and reviews, it is chock full of all kinds of silly ideas that experienced what I can only imagine to be a frictionless path from the authors’ minds to publication. I don’t really care about this book or the specific ways in which it is is bad. And I don’t really care about the authors, who appear to be mediocre self-styled evolutionary scientists whose major claims to fame appear to be favoring ivermectin over vaccines and supporting themselves financially by levying a lawsuit against Evergreen State College.

What I care about is evolutionary biology and psychology as subfields. The core idea is that the evolutionary framework of persistent adoption and adaptation of traits under unrelenting selective pressures can be a useful modeling framework for generating theories of social, economic, biological, and psychological phenomena. Evolutionary selection is a good idea, one of the most powerful in intellectual history! But to me, an outsider economist with a long-ago acquired undergraduate degree in biology, the subfields seems to be suffocating under the weight of ad hoc theories generated in volume by marginal practitioners and non-scientists. Why? What’s wrong with evolutionary sciences? Here’s a couple thoughts.

1) There’s nothing wrong. Saying something is wrong with the subfields is like watching The Shining and thinking “There’s something wrong with axes”. This is just a bad book with bad ideas thought up by authors with minimal right to claim the mantle of evolutionary science.

That’s a totally reasonable response but I’m in no mood to leave well enough alone.

2) There’s a perverse selective pressure within evolutionary sciences where the worst ideas rise to the level of public dissemination. The culling forces of the popular press select along dimensions that are not merely orthogonal to good science, they are actively selecting against it. Put in the language of my own field, publishing bad ideas seems to be more profitable than publishing good ones.

That’s pretty big claim, and one for which I have no real proof, just tacit intuition and a small number of anecdotes. Sorting through the reviews of the Heying & Weinstein book, I thought of the brief phenomenon that was “Sex at Dawn” a decade ago. It, similarly, sold a breathless explanation of human behavior, specifically promiscuity. Emphasis on the world sold. “Sex at Dawn” proved that you could be scientifically hollow and still sell a boatload of copies. For those who are curious, here’s a review by an evolutionary psychologist that doesn’t hold nearly the grudge that I do. He politely sifts through the major claims, weaving through the silliness to find the handful of specific claims, and proceeds to debunk them. Other reviewers were considerably less kind (including those at Oxford Press, who rejected it for publication).

So why are these and similar books, so successful?

I’ve long suspected that there is a Gresham’s Law of Popular Science at work. Simply put, bad ideas are less costly to generate than good ones, so they are more plentiful. For the non-expert consumer of popular science, this raises the costs of search probability that a randomly encountered book is bunk. What I believe to be more problematic, though, is that bad ideas are often less costly to consume. Spoon-fed as common sense writ magnificent and powerful, pseudoscientific books get a foothold in our mind first through the scarcity of our time and attention only to then grow roots in our ego. Easily consumed during rare moments of relaxed reading, they then show us ideas that give us explanatory access to life, the universe, and everything. Why struggle through caveated niche explorations when someone else has distilled the complexity of a modern life well-lived to something that is as flexible in its flattery as a horoscope and often conveniently enumerated?

Does this happen within economics? Of course it does. It happens in every scientific field. But that is why scientific fields evolve intellectual immune systems, and often very aggressive ones at that. The entire field of “Statistics” essentially exists as the custodian of the scientific method. But there are little details that matter, too.

Take, for example, the core concept of “maximization” in economics. Sure, it gets abused, but at the end of the day it’s pretty tough to get very far with an ad hoc utility/profit/wealth maximizing model in economics that produces useful predictions. Why is that? Well, a big reason is that we’ve left out a very important word. Economists deal almost exclusively in constrained maximization. Absent constraints, nearly every maximizing model amounts to little more than a tautology. It’s requirement for maximization under constraints, both components transparently introduced, that gives a model it’s power. When I observe meritless pop evolutionary science books, mostly what I’m seeing is unconstrained just so stories that work backwards from a conclusion they believe there is a book-purchasing audience for. There are selective pressures, but where are the resource constraints? There are groups but where are the rivals they are competing with? There is this evolutionary path, but why not the other paths?

So what should evolutionary sciences do? Well, first of all, I don’t know. But if I had to guess, the answer is nothing. Nothing but do the thing a proper science always does. Do the work, push the good ideas, kill the bad ones, and trust that the custodians of the scientific method will do their jobs. And so will the editors. And the hiring committees. And the critics. Sure, a couple folks will pay a couple years mortgage, but a bit of financial and status injustice are a small price to pay while we keep the scientific mission moving forward. At least until we’re all crabs.

Hopefully by this time we all know about index funds. The idea is that by investing in a large, diversified portfolio, one can enjoy the average return across many assets and avoid their individual risk. Because assets are imperfectly correlated, they don’t always go up and down at the same time or in the same magnitude. The result is that one can avoid idiosyncratic risk – the risk that is specific to individual assets. It’s almost like a free lunch. A major caveat is that there is no way to diversify away the systemic risk – the risk that is common across all assets in the portfolio.

We can avoid the idiosyncratic risk among assets. But, we can also avoid idiosyncratic risk among times. Each moment has its own specific risks that are peculiar to it. Many people think of investing as a matter of timing the market. However, people who try to time the market are actively adopting the specific risks that are associated with the instant of their transaction. This idea seems obvious now that I’m writing it down. But I had a real-world investing experience that– though embarrassing in hindsight – taught me a heuristic for avoiding overconfidence and also drilled into my head the idea of diversifying across time.

I invested a lot into my preferred index fund this past year. I’d get a chunk of money, then I’d turn around and plow it into the fund. What with the Covid rebound, it was an exciting time. I started paying more attention to the fund’s performance, identifying patterns in variance and the magnitude of the irregularly timed and larger changes. In short, by paying attention and looking for patterns, I was fooling myself into believing that I understood the behavior of the fund price.

And it’s *so* embarrassing in hindsight. I’d see the value rise by $10 and then subsequently fall to a net increase of $5. I noticed it happening several times. I acted on it. I transferred funds to my broker, then waited for the seemingly regular decline. Cha-ching! Man, those premium returns felt good. Success!

Silly me. I thought that I understood something. I got another chunk of change that was destined for investing. I saw the $10 rise of my favorite fund and I placed a limit order, ensuring that I’d be ready when the $5 fall arrived. And I waited. A couple weeks passed. “NBD, cycles are irregular”, I told myself. A month passed. And like a guy waiting at the wrong bus stop, my bus never arrived. All the while, the fund price was ultimately going up. I was wrong about the behavior of the fund. Not only did I fail to enjoy the premium of the extra $5 per share. I also missed what turned out to be a $10 per share gain that I would have had if I had simply thrown in my money in the first place, inattentive to the fund’s performance.

Reevaluation

I hate making bad decisions. I can live with myself when I make the right decision and it doesn’t pan out. But if I set myself up for failure through my own discretion, then it hurts me at a deep level. What was my error? Overconfidence is the answer. But why did it hurt me?

Bo Burnham is a comedian and musician who, like so many of the artists I enjoy, produces art that I can only describe as extremely specific to him. His newest special on Netflix features a song, “Welcome to the Internet” (some NSFW lyrics), that I liked so much I thought it was worth writing as a formal model.

No, really. Hey, we all need a hobby.

The whole song is a meditation on the overwhelming nature of the internet and is, in my opinion, fantastic. I think if we zero in on two pieces of refrain in the lyrics, we can get some traction in what Burnham believes is the underlying problem, if not outright crisis, that resides within the internet and those that are “extremely online”:

First, the lure:

Could I interest you in everything? All of the time? A little bit of everything All of the time

This is the value-add of the internet and why we can never, and will never, leave it behind willingly. This is also the “cognitive overload” hypothesis of why the internet is bad. Sure, for the infovores of the world there hasn’t been a bigger technological shift since the printing press, but there certainly exists the possibility that most human minds (if any) aren’t built to handle the deluge of information they are drowning in. That’s one theory, but I think that’s the kind of problem that isn’t actually a problem. Some will consume more of the internet, some will consume less, c’est la vie.

It’s in the second half of the refrain, however, that we see the actual problem.

Apathy’s a tragedy And boredom is a crime Anything and everything All of the time

And therein lies the rub. You can’t opt out. But is that true? Well, that depends on who you are and how you live your best life i.e. how you optimize your utility function. So let’s do it. Let’s write down the utility function that lives inside the song. What we’re going to do is this- we’re going to lay out the simple components as natural language, then turn it into formal math, and then bring it back to natural language.

In our Burnhamian mode, people need two things: Private goods like food and shelter and Social Goods like friendship and camraderie. How much Utility you enjoy will always be increasing in both, but the optimal mix will depend on your constraints (wealth, time, accessible population) and the mathematical function determining how much Utility you get from a mix of Private and Social goods i.e. are they additive, multiplicative, or something else. Utility equal to zero is equivalent to death.

Let’s add one last layer of complexity. Let’s say that your Social goods are a function of two kinds of elements: Friends and Clubs. Friends are direct, one-to-one relationships. Clubs are large social groups. We will define and differentiate between the two as such: if you cease to be part of a friendship (whether between 2,3, or 5 people), then that friendship no longer exists in the same form. If you drop out of a club, on the other hand, that club will persist without you.

So what a person has to do is, within their constraints, try to optimize how much of their resources they invest in their Private goods, their Friends, and their Clubs.

The first line is our base model, the second is an expanded version with our two-input model of Social goods. The function we are using is called a Constant Elasticity of Substitution utility function. The key parameter, α, determines how Private and Social goods interact. If α=1, then they are what economists call perfect substitutes. All that matters is how much you have in total of the two inputs, and if you want you could specialize in just one of them. They are perfectly additive. If, on the other hand, α=-∞ (negative infinity), then they are perfect complements, like right and left shoes. There is no point in adding even one more unit of Private goods until you have another unit of Social goods to pair with it. In a sense, they are multiplicative, meaning if either value is zero, then your utility is zero. The value of α will tell us whether the best life requires more of a mix of Social and Private inputs (if they are more complementary), or simply the most of whatever is the easiest to come by (if they are good substitutes for each other).

We’ve nested in our Friends and Clubs production of Social goods as a CES function within the second equation, with a similar story, only here β will determine how much of a mix of Friends and Clubs we want, or whether we can specialize more in one over the other. In the third and last line of the model, we’ve reduced it down to the underlying questions that will tell our story represented by addition and multiplication signs:

Are Private and Social Goods complements (multiplicative) or substitutes (additive) when we internally produce utility? Are Friends and Clubs complements or substitutes when we internally produce our Social goods?

Assumption 1: α= -0.1 Private and Social goods are weak complements. What this means is that there are diminishing returns to Private and Social goods, you need some of both, but you can have less of one or the other and its fine. Let’s just assume wealthy people need other people in their lives to stay sane while, at the same time people with rich social lives and supportive communities still need food and shelter. You can specialize a bit more on one side, depending on what’s available, but you can’t live without at least some of both.

We’re all different in how we build our social lives and, in turn, how we internalize the internet in our lives. I think we can gain some insight into this process by working out the stories in this simple model through our second parameter, β. Let’s consider three broad types of people.

Person Type 1: Friends and Clubs are Strong Substitutes (high β)

These people are either relatively offline (e.g. they still use their phones as phones to make phone calls) or extremely online (e.g. they get a panic attack unless they have 80% battery and a charge pack on their person). These are the people who can become hyper-specialized in new clubs if they are extricated from prior social networks or club settings. This is why cults recruit people who move to new places where they don’t know anyone. This is how your diehard hippie socialist friend grew up to be a conservative evangelical after they moved to the Texas suburbs.

With regards to our original question, people who hyperspecialize in their club and club identity will be constantly contributing grist to the club’s identity: evidence of the necessity of the club and it’s mission, rage at non-members, disappointment in members who aren’t committed enough, and constant vigilance in the monitoring of everyone else’s commitment. They are in it, they are of it, and they are ready to purge.

Apathy’s a tragedy(You must care about everything the club cares about) And boredom is a crime(All of your time must be allocated to the club) Anything and everything All of the time

Type 2: Friends and Clubs are strong complements (low β)

These are the people that I think Burnham’s song is targeted at, for whom he has the most sympathy, and with whom I suspect he would count himself. These are people for whom the internet is the most taxing, the most exhausting to navigate.

Type 2 folks want to have personal friendships and friend groups while still feeling a part of something bigger, whether it’s a community, a political movement, or spiritual affiliation. Type 2 people will have preferences towards one or more social identities manifested as clusters on the internet, but they don’t want to purge people who don’t share those preferences from their circle of friends. Type 2 folks are interested in civil rights and social justice, but they want to diversify their emotional and material resources across their personal relationships and private wellbeing as well.

The deluge of the internet, with its stark images, focus on extreme outcomes, battle cries, and public reputation mauling, are constantly admonishing and shaming Type 2’s. Type 2 people are tired. Perhaps most importantly, the pandemic has been especially hard on Type 2’s. While Type 1 club-specialists have thrived by focusing the totality of their efforts to the online arena, their voices have been tearing the Type 2 social-portfolio diversifiers to shreds.

Type 3: Friends and Clubs are weak complements (middle β)

Type 3 people are a lot like Type 2’s, but it is easier for them to compartmentalize the production of their social goods. Type 3 people are often in clubs, but they are rarely ofclubs. They’re not joiners. Whether you’re looking at sacrifice-demanding religious cults or extremely-online political culture warriors, if the social associations of the world demand too much of Type 3 people, they are happy to half-ass their contribution or opt-out entirely. They might be on Twitter or Facebook, but they don’t need to reply to anyone. They might go to church on Sunday with the family, but if the minister tells them their sister is going to hell for their sexual preference, it’s just not that costly to stop going. For them clubs will always remain a luxury good, never a necessity.

To be clear this post is an exercise in building a toy model of something big and complex and important. It’s a gross abstraction and shouldn’t be taken too seriously. The process of formalizing your thinking on a social mechanism, however, is something that I think you should take very seriously. Formal models are useful because there is no hiding what your idea actually is. There’s no “sorry, you misread me” or reliance on obscure jargon. Formal models force you to clarify and reveal your thinking to everyone, including yourself. They can open up new avenues for explorations and even generate empirically testable predictions. Formal models have in many ways been the principal force behind economic imperialism in the social sciences. Not because the math is perfect or all encompassing or even correct. It’s because it’s all out there, ready to be judged and dissected and tested. That transparency makes it a useful.

I don’t know if my interpretation of Bo Burnham’s theory of the internet is correct or even necessarily what he intended it to be. But this is one way we can take it a step forward and see what we can actually learn from it. Which is pretty much all I want to do for the rest of my research life, on every topic, all of the time.

A disproportionate share of my influences have been, at least in track record if not in conscious intellectual identity, contrarian voices. Contrarians are to me those thinkers who have a persistent mistrust of conventional wisdom. They tends towards a certain amount of Burkean conservativism (i.e. the status quo is usually better than we give it credit for), though not necessarily economic or cultural conservatism. The last 5 years, specifically the Trump administration and the Covid-19 pandemic, have to my mind presented perhaps the single greatest challenge for contrarians in my lifetime for a host of (maybe) obvious and non-obvious reasons. To better understand why, I think it’s worth casually investigating the strengths and weakness of contrarian sensibilities.

Contrarians are an antidote to herding

The Banerjee model of herding behavior is a masterclass of parsimonious modeling that changes the way you see the world the moment you internalize it. To oversimplify and already simple model, it’s the classic business cliché of “Nobody gets fired for buying IBM” writ both much larger and much smaller. If you’re on Twitter, it means nobody gets cancelled reaffirming the shibboleths within your intellectual and political social network. Following the herd can insulate you from bespoke micro consequences (i.e. no one can punish you without punishing everyone), but it can’t protect you from macro consequences (i.e. if the herd runs off a cliff, you’re going over with them).

Contrarian’s are useful because they are seemingly less susceptible to such pressures to conform because their identity, and the product they sell in the intellectual marketplace is defined by their distance from modal positions. What’s interesting here is that whether they are right or wrong is almost beside the point – contrarians add value just by adding noise to the intellectual marketplace, jittering herding populations out of potentially suboptimal equilibria. This is a powerful consideration – contrarians can make the world a smarter place even if their actual intellectual goods are complete trash.

Contrarians maintain our intellectual hygiene

Similar to their ability to break herding equilibria, contrarians offer a custodial service for science. Through their constant devil’s advocation, contrarians serve up intermittent stress tests for old ideas that might otherwise survive simply based on past glories. Just because something is an old truth doesn’t mean it’s a good or useful truth. Contrarians force us to regularly consider our core models and assumptions. Is it annoying when someone asks whether or not NASA was actually successful? Of course, it’s always annoying to defend a position that is obviously true. But sometimes you get a Warren Nutter telling anyone who will listen that Paul Samuelson’s textbook is wrong and the Soviet Union is a shell of its industrial reputation. Sure, it probably wasn’t fun to get run out of academia <adopts the snarkiest Ivy-league-jerk-in-a-skit-voice>for being just so obviously wrong, but checking every now and then that we actually know the things we think we know is an underprovided public good. We need contrarians to tell use when fads and social shibboleths are masquerading as science.

There’s more wisdom than madness in crowds

Hygiene and herd-prevention are definitively good things, but it’s important to remember that most conventional wisdom is in fact wisdom. There’s a been a certain agony in watching my favorite contrarians tie themselves in knots trying to find the strategic genius to Donald Trump, the collective madness that must be behind Covid fears, the grand lie of that surrounds Joe Biden as he sells his secret Republicanism to Democrats. Sometimes things are obvious because they are obvious.

Most of the time, whether it’s guessing the number of jellybeans in a jar or finding the best pizza in town, the crowd gets it right. The reason that most politically informed people think Donald Trump is a wet-brained buffoon is that he’s a buffoon (I will forever hold to the believe that his buffoonery wasn’t a strategic choice, but rather an pre-existing attribute that the political marketplace generally, and the Republican Primary specifically, selected for in 2016 and may select for again. Politics, like any habitat, can be quite cruel in its amorality.) The reason most people are afraid of Covid is because Covid is a danger of sufficient magnitude that it warrants private and public action to mitigate it. The reason that Joe Biden seems like a mix of the modal Republican and Democrat is because that’s exactly what the median voter is. The mob is good any taking a million small clues and turning them into a big conventional wisdom.

Intellectual Serial Autocorrelation

We should all be careful of our own intellectual brands, doubly so for contrarians. Yes, I’ll admit that in the market for takes there is a strong incentive to differentiate, but most following the path of optimal differentiation end up being just a different flavor of one of the two or three dominant conventional positions. Contrarians are far more likely to stake out territory as lone(-ish) wolves, perhaps on the periphery of one or more of the major intellectual identity clusters.

For these thinkers and commentators, they can often find themselves repelled from the obvious. Cultivating too strong a revulsion to the wisdom of crowds is often foolish and sometimes dangerous. Don’t get me wrong,sometimes there is no spoon.Sometimes. But most of the time it’s just a spoon and you should move on to the next puzzle. Maybe your model of world of the world is telling you to keep plowing ahead, but if everyone in the car is telling you to stop, you should probably stop.

It’s a blog. I’ll write about 9/11, since it’s 20 years today. 9/11 was an attack on my family and I will always be sad on this day remembering the horror. 9/11 was more than the number of murders we can count.

The Twin Towers episode was more than an attack on American citizens. New York City is the place people from all over the country and all over the world dream of reaching. It is the great melting pot. It is the symbol of American ideals, even as it is paradoxically at odds sometimes with the conservative heartland. Anything is possible for anyone, in New York.

I was not a New Yorker as a kid. I grew up nearby, but my parents avoided the city. I think the fact that you had to pay for parking and fight traffic was their primary reason. We were transcendentalists, preferring to park for free by some hiking trail on weekends. Anyway, I want to be a New Yorker now, if they’ll have me. I will always share that dream of moving to New York and experiencing the version of freedom that was uniquely created there.

I follow a lot of smart people who want to fix all problems. By all means, fix problems. This day just hurts. No one is expected, for example, to cure cancer on the day their deceased husband’s birthday comes around. This day can be for remembering what was lost and listening to a favorite song and talking to a favorite person. I try to convert the survivor’s guilt into gratitude.

9/11 will haunt me all my life. I know this is becoming a topic for history textbooks. People will interpret this event as coldly as I do when I read about massacres in history books. My professor peers are getting the first wave of kids born after 9/11. “I can’t believe these kids were born after 9/11. Is that… Do I have a gray hair?” It is in fact true that everyone born after 9/11 was born after 9/11. Maybe we should be happy that it’s been so long. I don’t wish this memory on my children.

The kids-these-days lost their innocence to Covid (and watching adults fight about it). I can only imagine how the 9th graders felt who were sent home from school to watch from the windows while a parent-killing plague swept through their community. They will want to share their lockdown stories in the way that I want to share my “where were you on…” story.

I lived close enough to New York to feel the outer ripple of grieving families. A schoolmate’s uncle died. I had a flamboyant Sunday School teacher who told us that God told him to stay home that morning and make muffins, else he would have been in lower Manhattan at his job in the fashion industry.

Tomorrow, I will begin a series of post about “behavioral economics” and the rumor that it died.

Topps lost the the licensing rights to Major League Baseball which, prior to it actually happening, is a thing that your typical baseball fan would not have previously acknowledged as even possible. Topps makes baseball cards. Not the only baseball cards, but for most of the history of baseball cards, Topps were the baseball cards. How can baseball cards exist without Topps?

Major League Baseball (MLB), of course, simply sold the licensing rights to someone else: Fanatics. Now, to be perfectly clear, I don’t care abou, any of the corporate entities involved here, imaging rights, or even baseball cards. What I am interested in is the concept of a purposely designed collectible–not something that becomes collectible, an item designed solely to exist as a collectible.

The markets for baseball cards rise and fall, and there was one definitive bubble in the early 90s. Like any commodity, prices are an emergent outcome of supply and demand, and while in the short run price movements are associated with fad and event driven demand, in the long run a collectible item’s price ascent begins and ends with supply. For an item to exist as a collectible with investment-grade price growth potential, it’s supply must be short-term limited and long-term fixed.

Fanatics just paid a lot of money for the MLB imaging rights, more than Topps was willing to bring to the table as a 70-year producer and stake holder. Part of Fanatics reasoning in committing so many resources to the rights is their ambition to produce non-fungible tokens (NFTS), which they will no doubt restrict the supply of to a profit maximizing level. NFTs, I suspect, offer Fanatics the opportunity to pursue a parallel product distribution that will allow them a new channel for price discrimination. Specifically, I expect the physical cards to be relatively inexpensive, sold at a price comparable to recent historical prices in an effort to serve price sensitive kids and hobbyists. The NFTs, on the other hand, I expect to be greatly limited in supply, a promise to hardcore collectors that the assets in question will offer the investment-grade inelasticity of supply that collectors covet in their aspiration to hold collectible items that hold value as art-adjacent consumption value while also being long term lottery tickets.

Fanatics believe the key to unlocking this is the image rights to Major League Baseball. Their cards and NFTs are the real ones, the official ones.

But that begs the question: why does the market care that they are officially sanctioned? The value of the image rights was to be able to use the names and logos of Major League Baseball without getting sued. The only way to profit off baseball cards previously was to produce at scale – you couldn’t capture the future collectible value nearly as well as the present consumption value. And there was no way to produce at scale without the imaging rights – there’s no good way to secretly print and sell a million baseball cards with images you lack the rights for. A person or company can’t sell a million black market bootleg cards without getting caught.

But someone could sell three.

A person can sell three cards without getting caught. A person could sell an unlicensed NFT without getting caught. And so can it’s next owner, and the one after that, ad infinitum. In the crypto world of NFTs these transactions, especially in the long term, are feasibly untraceable. If anyone can sell three baseball cards and associated NFTs, then anyone can make them as well.

Remember zines? Actually, maybe you don’t. In the before-times, aficionados of musical, artistic, or even just aesthetic subcultures would print their own magazines at home, pay for a 100 copies at Kinko’s, and then distribute them independently on their own through the mail or at small local bookstores. Not dissimilarly, many artists have for years produced “Art Cards, Editions and Originals” (ACEOs). Essentially baseball cards, but with small collectible works of art instead.

An independent artist that tried to produce baseball ACEOs and sell them on eBay would probably fly below the radar. But in the unlikely event that their card did become the card that the market chose as the most sought after, then yes, MLB and Fanatics would likely pursue legal action. The thing about pursuing a copyright so vigorously is, like many consumer goods for which distribution is illegal, restricted supply only increases their value. And an NFT transaction is considerably harder to trace than a physical or even traditional software good. It’s called “crypto” for a reason.

Sure, Fanatics will be the only company that can sell the “official” baseball card, the “real” one. But who’s to say that they’ll be selling the best one? In a world without enforceable image rights, the market is likely to care a lot less about the what’s official, and a lot more what’s the, always ephemeral and hard to anticipate, best. When you’re talking about a commodity where limiting supply is the key to unlocking value, NFTs and crypto technologies change the entire landscape, because copyright and image rights are only only enforceable to limit production at scale, which means any effort to do so just creates great incentive for small scale independent production.

This isn’t just relevant to baseball cards, either. This is relevant to anyone designing a product with the intention of it becoming collectible, where some portion of its value today is it’s predictable scarcity tomorrow. Twenty years ago downloadable music changed the entire market for music. Musicians at the highest levels of popularity found themselves returned to a world where the bulk of their income came from live performance, which had of course been the norm for musicians for most of human history prior to the vinyl record. It would be interesting if baseball cards, and other portable pieces of functional art (such as Magic or Pokémon cards) found themselves on a similar path, where large scale production of collectibles becomes outflanked by anonymous independent artists.

You’ll probably never own a $5.2 million Mickey Mantle 1952 rookie card. But you maybe you’ll paint Shohei Ohtani as a half-man, half-Gundam neo-noir warrior prince pitching a no-hitter the same night he hit three grand-slams. And maybe the market will say that the official photo cards of Ohtani are nice, but your image, and your NFT, are the one true image that captured the moment he became the greatest baseball player ever. Maybe the market will select your card.

(What I’m saying is…maybe the market will say your card is….topps. Yeah, sorry, I’ll see myself out).

What happens when the world changes sufficiently that a subset of the institutions that laid the groundwork for the most successful nation of the last 200 years becomes becomes maladapted to their context? Well, thanks to a couple billion year of evolutionary biology, we know the possible outcomes. The classic evolutionary answer is that the species in question will either adapt, migrate, or die. Repurposed for the modern nation-state, the country in question will either:

Adapt it institutions

Change the context (i.e. whole nations can’t migrate)

Steadily decline into some combination of irrelevance or chaos

Omar Wasow put together a nice thread, where each individual tweet stands wholly on it’s own as an acute observation, on the current state of the Senate as an elected institution:

America is increasingly centripetal — cities keep growing and rural areas keep shrinking — but key institutions like the Senate and the electoral college ensure stark political inequality favoring low-population regions will only get more extreme. https://t.co/Xz7qgSiEggpic.twitter.com/9dBjjhStx8

— Omar Wasow | @owasow@bsky.social (@owasow) August 25, 2021

How long will a super-majority agree to the rule of a super-minority? “By 2040, ~70% of Americans are expected to live in the 15 largest states. They will have only 30 senators representing them, while the remaining 30% of Americans will have 70 senators.” https://t.co/JjMpkhScBc

— Omar Wasow | @owasow@bsky.social (@owasow) August 25, 2021

.@namalhotra points out his co-authored study on “Racial Representation and U.S. Senate Apportionment” found Africans Americans are projected to improve in representation but Hispanics and Asians are poised for big losses. https://t.co/O5EX1Q1Lgq

— Omar Wasow | @owasow@bsky.social (@owasow) August 25, 2021

So let’s think about our options here.

Decline into Irrelevance and Chaos

I mean, it’s a choice, but it’s not one I’m particularly excited about.

Adaptation

We could amend the constitution to change how the Senate is apportioned in some clever way that still maintains the mandated suffrage of every state. We could change/abolish the electoral college. I’ll be blunt: I don’t ever see a path forward for constitutional change that will entirely undermine the political power of the one of the major parties (good luck getting 2/3 of Senators to push through an Amendment that will undercut the careers of at least half of them). The resistance to it, at every level, will be extreme. The last time we tried to make an institutional change with that much impact on the balance of power, we had to fight a war to resolve it. There may be a path forward here, but not on a timescale that I’m interested in. I’m only interested in solutions that could be feasibly enacted in my lifetime.

Change the Circumstances

Unlike your typical seed-eating bird of the Galapagos Islands, we do have the means to change the map upon which the Senate is selected. In other words, more states. I don’t mean just granting statehood to Puerto Rico and DC (though it is mildly unconscionable that we haven’t done so already). And I don’t just mean (the very good and perfectly reasonable idea) of splitting California and Texas into 5 and 3 states. I meana lot more states.

Let’s think about the underlying problem for a second. The Senate biasing representation towards a small minority of voters is a symptom of a larger phenomenon: the continued movement of Americans to dense urban areas. People keep moving to cities, and often from states without a major urban center, and into states with multiple large cities. The rural areas that they are emptying out from maintain their pool of slots for elected Senators, while the cities gain none. So what’s the answer?

Welcome to the great state of Seattle! [state motto: “If it’s not caffeinated, send it back”]

The Vinegar-Tomato Sauce State of Raleigh! [state color: halfway between Duke blue and UNC blue]

The Beechwood Aged State of St. Louis![ state left fielder: Lou Brock]

The Always Hustling State of Atlanta [state anthem: written and performed by Outkast]

City-states. Remember city-states!? Yes, I know, when we speak historically of city-states we mean entities independent of any other nation state – classic Venice, current Singapore or Monaco, but that doesn’t mean we can’t piggyback on their awesomeness. Texans already joke about the “People’s Republic of Austin” – let’s make it official! We can set a size minimum as either an explicit population threshold (e.g. 500k) or a moving bar, such as the population of the smallest state in the previous census. It’s essentially adding another option for a city to apply for inclusion in the next tier of our federalist system.

This is more feasible than you might think and vastly more feasible than amending the constitution.

Consider:

These cities already have government infrastructures. The governor on day 1 is the current sitting mayor.

The citizens of most medium- and large-sized cities derive the bulk of their regional identity from their city, not their state. Most urbanites will be thrilled at the notion of elevating the political status of their city while losing the affiliation of their previous state.

New state coffers will be heavily subsidized with flag and swag sales the first few years (only mostly kidding)

The remaining rural states will have the far more manageable task of trying to serve rural citizens without having to serve an urban voter base with radically different needs and preferences. Public goods will be better matched with the citizens of rural states as well.

States will often look like Swiss cheese, which will be both hilarious and, slightly less importantly, will allow for constituents to even more easily vote with their feet when elected officials fall short in their duties.

Are there downsides? Sure.

The speed traps before you enter and as you exit city-states into their rural envelopers will be aggressively extractive. There will be rampant attempts at exporting taxes across borders.

Reconstituting water supplies as special districts supporting multiple states will be tricky.

Coordinating interstate public goods will, no doubt, at times become even more farcical than the status quo.

Decent chance this turns into a NealStephenson novel within 100 years.

But, in the medium and long run, I believe the benefits will greatly outweigh the costs. Throughout the pandemic there has been a constant tension, particularly in “red states”, between the public goods desired by the citizens in cities versus rural areas. While urbanites have been desperate for mask and vaccine mandates, rural citizens have been far more interested in consuming personal liberty and symbolic group-identity goods, at the expense of greater Covid cases and deaths for those in denser areas.

I’ve said it before and I’ll keep saying it tomorrow: there isn’t a red-blue divide, a religious divide, or a class divide. America is currently defined by an urban-rural divide. If we don’t adapt our institutions to reflect it and balance the equal political enfranchisement of people on both sides of that divide, it will continue to erode the integrity of our political infrastructure.

I imagine I don’t have to persuade many people that the integrity of the franchise is not something to be taken lightly. Regardless of the mathematical salience of an individual vote to any election, the fact remains that the less people believe their vote has at least the potential to be realized in the form of representation that serves them, the more they will look to alternative channels to the political process. And maybe, for the libertarian inside of you, the alternative you imagine might exist in the private marketplace for goods and services. But history informs us that the dominant alternatives to democracy are heritable lineage and bloodshed, and I don’t see any benevolent American scions laying in wait.