In our era of increasingly sophisticated artificial intelligence, what can an 18th-century Scottish philosopher teach us about its fundamental limitations? David Hume‘s analysis of how we acquire knowledge through experience, rather than through pure reason, offers an interesting parallel to how modern AI systems learn from data rather than explicit rules.

In his groundbreaking work A Treatise of Human Nature, Hume asserted that “All knowledge degenerates into probability.” …

Furthermore, I explain why this could have implications for the limits of AGI, if LLMs learn from experience and are limited in the number of datapoints they can observe. It is also a follow-up to my summer post: Is the Universe Legible to Intelligence?

Economists are pretty united against tariffs. There are lots of complicated arguments. Keeping things simple, one reason is that they are bad for welfare. President-elect Trump seems to imply that tariffs can raise a lot of government revenue. But in lieu of what? The Tax Foundation estimates that there is absolutely no way that tariffs can replace all revenue from income taxes. The primary reason that they cite is that imports compose a tiny portion of the potential tax base. There are plenty of goods and services produced domestically that wouldn’t be subject to the tariffs. Any time we add a tax exemption, we’re adding complication, higher compliance costs, and distorting consumption patterns, etc.

For this post I singularly focus on the tax revenue. In fact, let’s demonstrate what *maximizing* tax revenue looks like under three cases: 1) Closed economy with a tax, 2) Open economy with a tax, & 3) Open economy with a tariff. I’ll use some simple math to demonstrate my point. None of the particulars affect the logic. You’ll reach the same general results with different intercepts, slopes, etc. Let’s start with a domestic demand and domestic supply.

Closed Economy with a Tax

Whenever tax revenue is raised, there is a difference between the price paid by demanders and the price received by suppliers. In a closed economy a tax might be imposed on all goods. In these examples, I treat the tax as some dollar per-unit of output tax. But it’s a short jump to percent of spending taxes, and then another short jump to percent of income taxes. With this in mind, demanders pay more than the suppliers receive by the amount of the tax. Tax revenue is the tax rate times the number of units of output that are subject to the tax. That’s the thing we want to maximize.

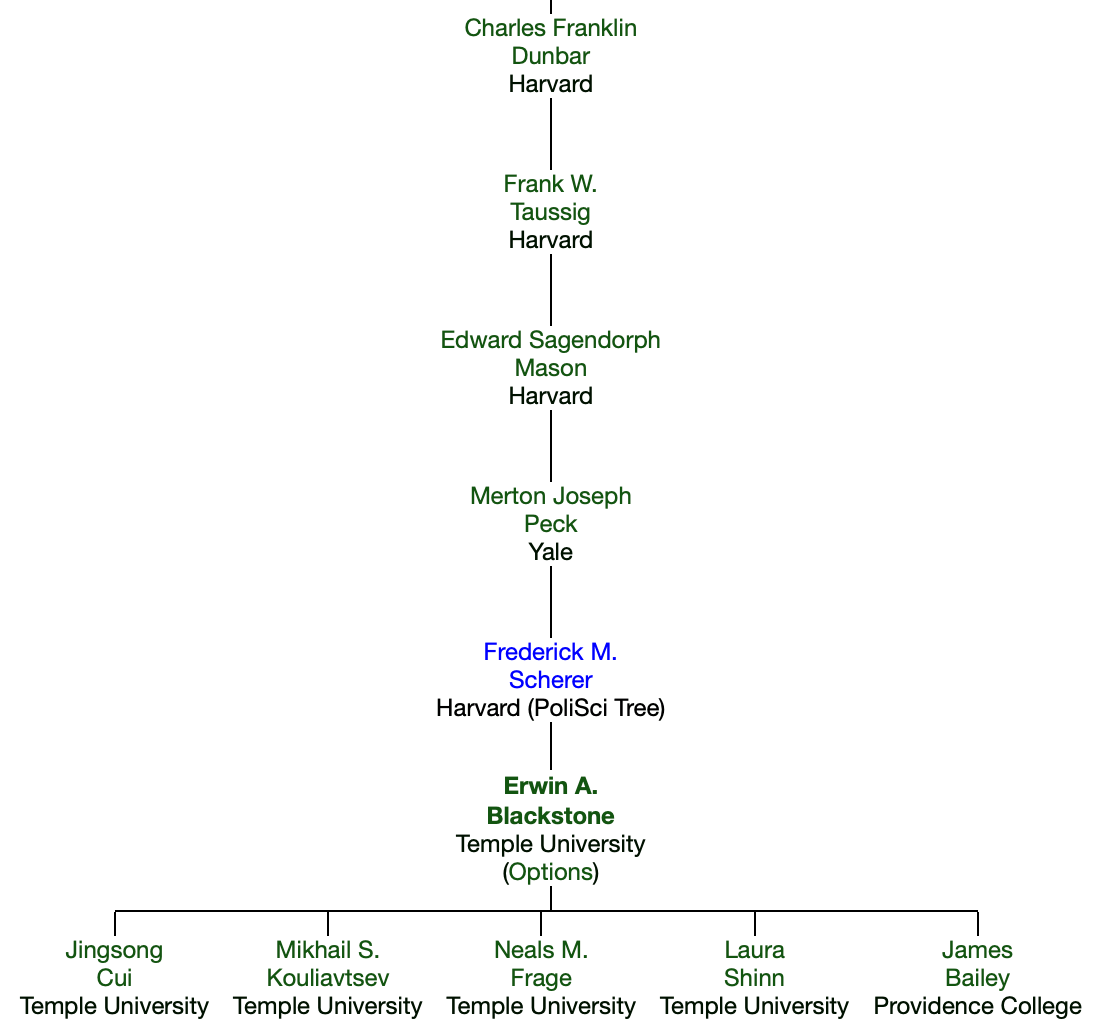

I’m told that Professor Erwin Blackstone died earlier this year, but I haven’t been able to find anything like an obituary online; consider this a personal memorial.

I knew Dr. Blackstone first as the professor of my Industrial Organization class at Temple University, where he taught since 1976. He was a model of how to take students seriously and treat them respectfully; he always called on us as “Mr./Ms. Last Name” and thought carefully about our questions.

Of course I learned all sorts of particular things about IO, especially US antitrust law and history- from Judge Learned Hand and baseball’s antitrust exemption to current merger guidelines and cases. I would later ask Dr. Blackstone to join my thesis committee, where he would heavily mark up my papers with comments and critiques.

He was a key part of how I was able to become a health economist despite the fact that Temple lacked a true health economist on the tenure-track economics faculty while I was there (as opposed to IO or labor economists who did some health). Blackstone’s coauthor Joseph Fuhr– a true health economist who also had Blackstone on the committee of his 1980 dissertation- came part-time to teach graduate health economics. Blackstone and Fuhr worked together to write the health economics field exam I took.

Finally, I learned from Blackstone by reading his papers. While he wrote many on health economics, my personal favorite was his work with Andrew Buck and Simon Hakim on foster care and adoption. It convincingly demonstrated the problems of having one fixed price in an area that most people don’t think about as a “price” at all- adoption fees. Having one fairly high fee for all children means the few seen as most desirable by adopting parents (typically younger, whiter, healthier) get adopted quickly, while those seen as less desirable by would-be adoptive parents linger in foster care for years. Like much of his work, it pairs a simple economic insight with a rich explanation of the relevant institutional details.

Academics hope to live on through our work- through our writing and the people we taught. Having taught many thousands of students at Cornell, Dartmouth, and Temple over 55 years, served on dozens of dissertation committees, and published over 50 papers and several books, I expect that it will be a long, long time before Erwin Blackstone is forgotten.

Source: Academic Tree. Charles Franklin Dunbar founded the Quarterly Journal of Economics in 1886.

For decades one of the most popular Christmas gifts for kids (and often adults) has been video game systems. And Nintendo has long been a dominant player in this market: the original NES arguably launched the modern gaming market in 1986 (even though it wasn’t the first, it was the first blockbuster) and Nintendo’s latest offering, the Switch, is now the best-selling console ever in the US.

As we often ask on this blog: has it become more or less affordable for an average worker to buy this iconic Christmas gift (or even buy one for yourself)?

When it comes to the consoles themselves, the Switch and NES are, perhaps surprisingly, equally affordable. The original NES cost $90 in 1986, while the Switch costs $300 today. Average wages in late 1986 were $9/hour and they are about $30/hour today. So in both years, it took about 10 hours of work to buy the console (alternatively, it’s about 25% of median weekly earnings in both years).

But as any serious gamer will tell you, the individual game cartridges can cost as much or more than the console if you want to play a lot of games. For example, the games available in the 1986 Sears catalog ranged from $25-$30. To buy just the 10 games in that catalog would cost $275 — over 30 hours of labor at the average wage, or about 3 hours of labor per game.

Today there is a wider range of prices for games, but the most expensive Switch games are around $60, or just 2 hours of labor at the average wage. There are also plenty of games around $30, or just 1 hour of labor.

The challenge with the comparison is that video games today are much higher quality, challenging, and advanced in so many ways. Is there any way to make a more direct comparison?

Yes. Nintendo offers an annual subscription for $20 to Nintendo Switch Online. Included in the subscription is access to nearly every NES game, plus Super Nintendo and Gameboy games. Not only do you get the 10 games from the 1986 Sears catalog, but many dozens more. All for less than $1 hour of labor at the average wage.

In other words, for 30 hours of labor today (the time to purchase those 10 original NES games), you could buy about 46 years worth of subscriptions to Nintendo online. That’s almost a lifetime of video game play, with many more advanced games.

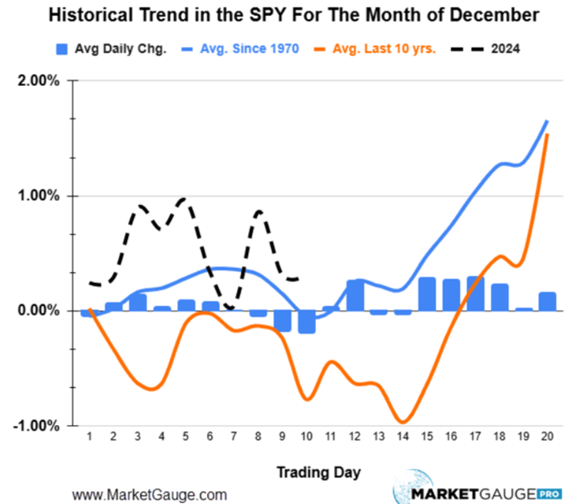

There tends to be a significant rise in broad stock indices the last two weeks of the old year and into the first two trading days of the new year. This is termed the “Santa Claus” rally. Sometimes it is focused on the last five trading days of the old and the first two days of the new.

Here is a chart showing average changes in S&P 500 prices for the month of December for 1970-2023 (blue line), and more recent data (last ten years, orange line).

Tax-loss harvesting: Investors may sell stocks at the end of a year to claim capital losses, to offset capital gains. They may then repurchase these stocks at the start of the new year.

Low trading volume: Larger institutional investors often go on holiday in this timeframe, leaving the market more to individual retail investors, who may be more optimistic.

Herd mentality: If most investors believe stocks will go up, then probably stocks will go up.

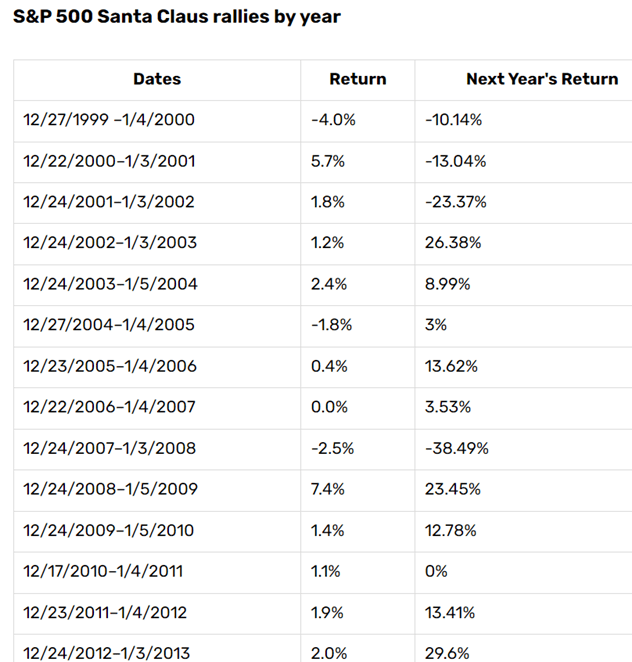

Santa Predicts the Future

Perhaps even more significant is the power of the Santa Claus rally to predict stock returns in the coming year. The following table lists returns for the last five trading days of the old year plus the first two days of the new year, and also the returns for the whole new year:

The table above was published in 2023, so the full year 2023 stock returns at that point were “TBD”. We now know the 2023 returns were hugely positive (approx. 23%). So, for 1999-2023, Santa came to town 19 out of 24 times for a year-end rally. Also, since 1999, the market rose 19 times during the Santa Claus rally; the following year, the S&P posted gains 15 times. Out of the 5 times the market lost ground during same period, the market fell in 3 of the following years. So the market performance in this transitional timeframe correlates well with the stock gains for the whole new year.

Will stocks soar again this holiday season? I have no idea. We are off to a shaky start, with the S&P 500 down about 1.5% in the past five days , through 12/22. This after the market hated the Fed’s more hawkish stance last week, being now likely slower to reduce interest rates than previously assumed.

As usual, nothing here should be considered advice to buy or sell any security.

Did you really think I was going to write a post this week? Sorry, this week is for far flung family and nutritionally disastrous cookies.

If you simply must have an economic observation, here you go: if you don’t gain weight during the holidays you’re probably too debt averse. Consume now, pay later. It’s worth the vig.

In August, I listed the Top EWED Posts of 2024. Here are a few more highlights. This list is roughly based on web traffic, starting with the highest number of views for 2024, since the August list.

Mike Makowsky has the top post since August with Bad service is a sign of a better world. “What if service in restaurants, hospitality, etc is, in fact, lower in quality than it was one or two decades ago? I would like to suggest that this is a good sign of improving times.” Thoughtful. Recommended. Bosses will not be requiring “15 pieces of flair” anymore. I have noticed that restaurant servers these days seem to wear whatever they want. It was previously noted by Mike that Kitchen staff were canaries in the coal mine.

3. You know it’s good when a post with such a cryptic title goes viral. Mike wrote about the topic people were thinking about, in the moment: At the moment (updated 10/22/24) Sometimes we write about the economics community and what began as a critical mass of people that used to call itself #EconTwitter. Some of those people have moved to Bluesky. You can find Mike there at @mikemakowsky.bsky.social, and most of us have accounts there. Getting social media just right is tricky. If you follow the right people and don’t waste too much time on it, then social media can be part of How to Keep Up With Economics (James).

9. Post-Pandemic Lumber Market Zachary Bartsch writes, “People used to talk about higher gasoline prices all the time, but never discussed with the same enthusiasm when prices fell. The same is true for lumber.” Good for teaching about supply and demand.

10. I Give Up, Standard & Poor’s Wins James lets us learn from his journey- “my stock picks underperformed the incredible 26% return the S&P has posted so far this year.” This is something most people would rather not admit, and yet for most of us it’s true.

12. Why Podcasts Succeeded in Gaining Influence Where MOOCs Failed attracted some attention. If you are being honest, would you have predicted a priori that Joe Rogan talking in a closed room FOR HOURS would outdo Ivy League professor lectures? In retrospect, it might seem obvious, but I probably would have gotten the prediction wrong. MOOCs and podcasts both launched around the same time because the internet lowered the cost of broadcasting. They both had some success. In terms of shaping culture or voting behavior, I think it’s clear that podcasts win. Until a product is launched on the market, we just don’t know what will become popular, which is a topic that came up in the podcast I recorded recently: Joy on The Inductive Economy podcast

Speaking of what I don’t predict, EWED is starting to get web traffic from LLMs like chatgpt.com. Right now, it’s very small compared to Google search. For a while, I wondered if LLMs would simply plagiarize us without giving us any credit. Maybe that’s our raison d’être. Here’s me being dramatic about it in 2022 – “Because of when I was born, I believe that something I have published will make it into the training data for these models. Will that turn out to be more significant than any human readers we can attract?”

However, writers of the world, LLMs might start giving you credit. There is some demand from users for sources and citations. (My paper on made up sources).

While we are settling scores and doing web traffic round-ups, there is one thing I’d like to put on the record. I made one resolution last year, publicly on January 3, 2024. I have made good on this promise. The people who run the AdamSmithWorks website have informed me that I wrote their top post of the year, Would Adam Smith Tell Taylor Swift to Attend the Super Bowl?

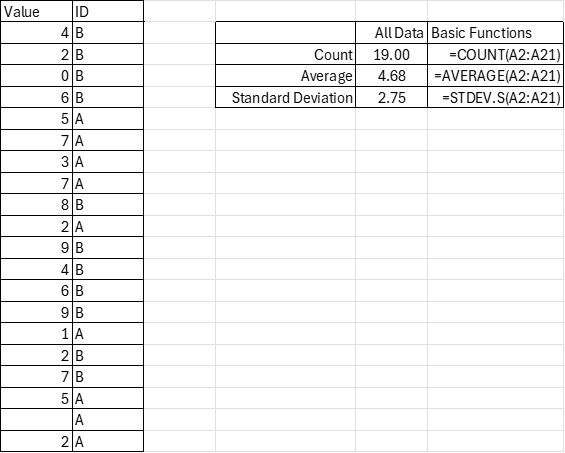

Excel is an attractive tool for those who consider themselves ‘not a math person’. In particular, it visually organizes information and has many built-in functions that can make your life easier. You can use math if you want, but there are functions that can help even the non-math folks

If you are a moderate Excel user, then you likely already know about the AVERAGE and COUNT functions. If you’re a little but statistically inclined, then you might also know about the STDEV.S function (STDEV is deprecated). All of these functions are super easy and only have one argument. You just enter the cells (array) that you want to describe, and you’re done. Below is an example with the ‘code’ for convenience.

=COUNT(A2:A21)

=AVERAGE(A2:A21)

=STDEV.S(A2:A21)

If you do some slightly more sophisticated data analysis, then you may know about the “IF” function. It’s relatively simple; if a proposition is true (such as a cell value condition), then it returns a value. If the proposition is false, then it returns another value. You can even create nested “IF”s in which a condition being satisfied results in another tested proposition. Back when excel had more limited functions, we had to think creatively because there was a limit to the number of nested “IF” functions that were permitted in a single cell. Prior to 2007, a maximum of seven “IF” functions were permitted. Now the maximum is 64 nested “IF”s. If you’re using that many “IF”s, then you might have bigger problems than the “IF” limitations.

Another improvement that Excel introduced in 2019 was easier array arguments. In prior versions of Excel, there was some mild complication in how array functions must be entered (curly brackets: {}). But now, Excel is usually smart enough to handle the arrays without special instructions. Subsequently, Excel has introduced functions that combine the array features with the “IF” functions to save people keystrokes and brainpower.

Looking at the example data we see that there is an identifier that marks the values as “A” or “B”. Say that you want to describe these subgroups. Historically, if you weren’t already a sophisticated user, then you’d need to sort the data and then calculate the functions for each subgroup’s array. That’s no big deal for small sets of data and two possible ID values, but it’s a more time-consuming task for many possible ID values and multiple ID categories.

The early “IF” statements allowed users to analyze certain values of the data, such as those that were greater than, less than, or equal to a particular value. But, what if you want to describe the data according to criteria in another column (such as ID)? That’s where Excel has some more sophisticated functions for convenience. However, as a general matter of user interface, it will be clear why these are somewhat… awkward.

I normally like the Wall Street Journal; it is the only news page I check directly on a regular basis, rather than just following links from social media. But their “Biggest News Stories of 2024” roundup makes me wonder if they are overly parochial. When I try to zoom out and think of the very biggest stories of the past five to ten years, three of the absolute top would be the rapid rise of China and India, together with the astonishing growth in artificial intelligence capabilities.

All three of those major stories continued to play out this year, along with allsorts of otherthings happening in the two most populous countries in the world, and all the ways existing AI capabilities are beginning to be integrated into our businesses, research, and lives. But the Wall Street Journal thinks that none of this is important enough to be mentioned in their 100+ “Biggest Stories”.

To be fair, China and AI do show up indirectly. AI is driving the 4 (!) stories on NVIDIA’s soaring stock price, and China shows up in stories about spying on the US, hacking the US, and the US potentially forcing a sale of TikTok. But there are zero stories regarding anything that happened within the borders of China, and zero that let you know that AI is good for anything besides NVIDIA’s stock price.

Plus of course, zero stories that let you know that India- now the world’s most populous country, where over one out of every six people alive resides- even exists.

AI’s take on India’s Prime Minister using AI

This isn’t just an America-centric bias on WSJ’s part, since there is lots of foreign coverage in their roundup; indeed the Middle East probably gets more than its fair share thanks to “if it bleeds, it leads”. For some reason they just missed the biggest countries. They also seem to have a blind spot for science and technology; they don’t mention a single scientific discovery, and only had two technology stories, on SpaceX catching a rocket and doing the first private spacewalk.

The SpaceX stories at least are genuinely important- the sort of thing that might show up in a history book in 50+ years, along with some of the stories on U.S. politics and the Russia-Ukraine war, but unlike most of the trivialities reported.

I welcome your pointers to better takes on what was important in 2024, or on what you consider to be the best news source today.

Really, our richest in the 1890s? Can this be true? Are the anonymous socialist Twitter accounts correct? Let’s look at the data. But the answer probably won’t surprise you: your intuition is correct, we are much better off today than the 1890s, in almost every way of looking at it economically.