The share prices of many semiconductor chip companies have gone nearly vertical in the past month. Here are five-year charts for Micron (MU) and AMD, as of the close Monday:

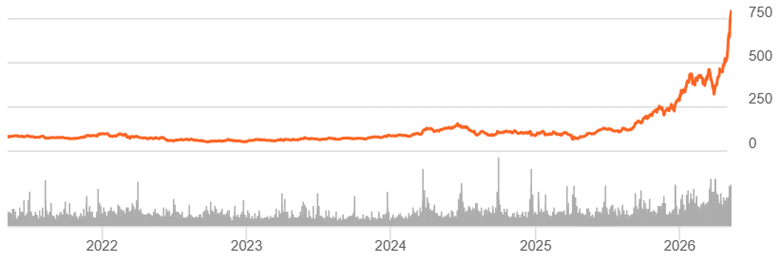

Micron (MU) 5-Year Stock Chart

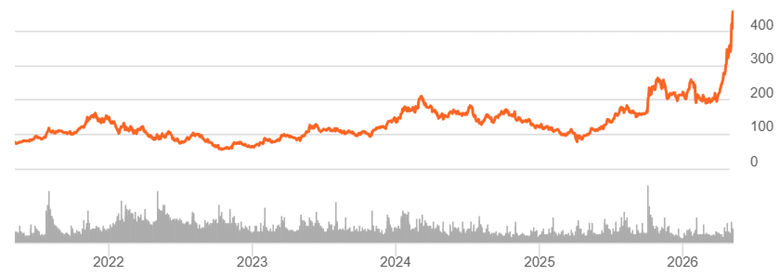

Advanced Micro Devices (AMD) 5-Year Stock Chart

Many analysts have been taken by surprise by the magnitude of the recent surge and prices. There has been no sudden, truly new news to drive this shift. It has been known for over a year that there is a huge shortage of memory chips, allowing Micron to charge high prices for its products. But apparently the official quarterly announcement of earnings and projections substantiated that narrative. The bears have been claiming that memory chips are a cyclic business, where chip shortages are followed by building more manufacturing capacity, which inevitably leads to overcapacity and a crash in memory chip prices. It has happened repeatedly, and therefore the current Micron stock party would end in tears after a couple of years. But the bears have been beaten back to their caves for now. Micron was up another full 7% yesterday.

AMD, which specializes in central processing units (CPUs), also released good earnings and strong projections. But the real share price driver there seems to be the new narrative that the shift from the shift to agentic AI will require a higher ratio of CPUs to GPUs. GPUs (graphic processing units) are the engines that do the core large language model (LLM) AI calculations. But apparently an increasing number of CPUs will be required to coordinate the activities of the GPUs:

AI agents—or the Agentic Era, as called by analysts—need more CPUs per GPU because they are responsible for the orchestration of AI workloads and the required data processing in order for the agent to accomplish its task, or, more simply, CPUs organize the steps of the workflow for the agent. Traditional LLM models—not agents—required a CPU:GPU ratio of 1:4 to 1:8, but analysts anticipate this ratio to shift toward 1:2 or even 1:1 in the coming years.

All that to say demand for AMD‘s chips is projected to increase.

So far, so good. But apparently being swept up in the whirlwind of exhilaration is the share price for lowly Intel (INTC). Intel was the leading manufacturer of processor chips back in the day, but it missed the boat on GPUs and just cannot seem to execute at global standards. In recent years, Intel has mainly been famous for ever-slipping deadlines on producing high performing chips. Its earnings have been approximately zero for some time. The good news is it now has a foundry business. The bad news is that the foundry business loses around $2 billion a year. The foundry has pulled in a few large customers, and after their experience there, they all run screaming for the exits. But wait, there’s been an announcement that Apple may contract with Intel to produce some low-end chips. Whoopee!

Intel (INTC) Five-year stock chart

Folks who look at technical behavior of stocks rather than the fundamentals of the business seem somewhat skeptical about the current surge. Terms like overbought are thrown around. I read an article claiming that hedging activities in the options market is creating an artificial, temporary demand for these high-flying stocks:

It is also fairly clear what has been driving these overbought conditions at the index level: aggressive call buying is creating a gamma squeeze across several stocks, such as Micron (MU). This occurs when aggressive call buying forces dealer hedging flows, resulting in purchases of the underlying stock. The more the stock rises, the more call buying tends to increase, and the cycle builds on itself.

My take on this spectacle

I can get the fundamental bull case in general for Micron stock. I bought into it about six months ago. Even that far back, it was clear that the demand for memory chips far outstripped the supply, so Micron could not help minting money for the next year or two. It was one of my fairly rare successes in stock picking. Sadly, I only bought a little bit, because I was influenced by many negative articles claiming that memory chips are a cyclic business, so this boom would end like all the previous Micron booms, with a glut and a crash.

There seems to be a solid bull case for AMD as well. For pitiful Intel, however, I see its price chart as a sign of market FOMO.

Where these stock prices go from here, I have no idea. My observation over the years is that this level of enthusiasm is usually followed eventually by, “What was I thinking?”, and a return to earth. However, in the meantime, tech stock prices often run up longer and further than I would have thought possible.

Usual disclaimer: Nothing here should be taken as advice to buy or sell any security.

#/media/File:Tesla-optimus-bot-gen-2-scaled_(cropped).jpg){kind=link}