Inflation is on everyone’s mind. Everybody freaks out. You cannot do anything about it. As such, lets talk about something mildly related: how price indexes (those that we use to talk about inflation) deal with quality changes.

One big problem when we try to measure the cost of living is that the price information we collect does not reflect the same thing we consume. I know that sentence seems weird. After all, 1$ for a pound of bread is 1$ for a pound a bread. And if prices go up 10%, then the price per pound of bread is 1.10$!

If you think that, you’re wrong. Think about the following example from my native province of Quebec. In the 1990s, Quebec deregulated opening hours for grocery stores. The result was … higher prices at large superstores. Why? Before the reform, stores had shorter hours especially on sundays. This meant that stores were competing with each other on a smaller quality dimension which meant more price-based competition. With deregulation, some consumers were willing to pay slightly higher prices to shop at ungodly hours. What were these consumers consuming? Were they consuming only the breadloafs they bought or were they consuming those loafs and the flexible schedule of the grocery stores? The answer is the latter! Ergo, the change from 1$ per pound to 1.10$ per pound does not mean that the price of bread alone increased — it may have even fallen all else being equal!

So how do you adjust for that? There are many papers on how to do hedonic adjustments (hedonic is the fancy words we use to say “quality-adjusted”) and they are all a pain to read unless you are very familiar with real analysis, set theory and advanced calculus (and even there, its still a pain). Fortunately, I recently found a neat little application from an old econometrics graduate text from the 1960s (see image below) that allows me to teach this to my students (and now, you too!) in an easy-to-get format.

The book has a neat chapter by one of the most famous econometricians of the 20th century, Zvi Griliches, titled “Hedonic Price Indexes for Automobiles: An Econometric Analysis of Quality Change”. In the chapter, Griliches points out that from 1954 to 1960, car prices went up some 20% — well above the overall price index. From 1937 to 1950, prices for cars went up in line with inflation. Taken together, these two facts suggest that the real price of cars stayed constant from 1937 to 1950 and increased to 1960. But that suggestion is wrong Griliches points out because of our aforementioned quality issues. Up until 1960, there were considerable improvement in vehicle quality: better gears, better brakes, more horsepower, safer settings, automatic transmission, hardtops, switching to V-8 engines rather than 6 cylinders engines etc.

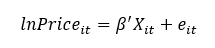

How do you account for these quality changes? Griliches simply went about consulting guide books for autobuyers. He collected price data for the cars as well the details regarding quality. And he used this very simple specification where the log of the nominal price is set as a dependent variable.

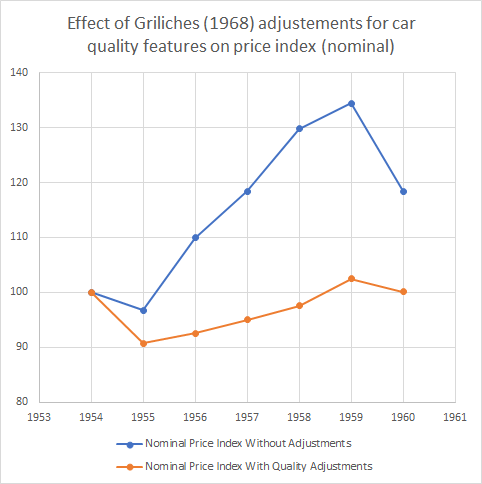

The vector X is all the quality dimensions he could find (horsepower, shipping weight, length, V-8 engine, hardtop, automatic transmission, power steering, power brakes, compact car). All of these dimensions were statistically significant determinants of the price of cars (with the exception of V-8 engines which was not significant). Then, Griliches assumed that all quality dimensions were “unchanged” from 1954 to 1960 in order to see how prices would have evolved without any changes in quality. The result is the figure below. The blue line depicts the actual prices he collected where you can see the 20% increase to 1960 (which is a 30%+ increase to 1959). The orange line depicts the price holding quality constant. That orange line is unambiguous: quality-constant car prices didn’t change much during the 1950s. Adjusting for inflation during the period suggests a drop in 10% in the real price of a quality-constant car.

Isn’t that a fascinating way to understand what we are actually measuring when we collect prices to talk about inflation? I find this to be an utterly fascinating example (and a useful teaching tool). Okay, I am done, you can go back to freaking out about inflation and how bad the Fed, Bank of Canada, ECB are.