One of my specializations in graduate school at George Mason University was monetary theory. It included two classes taught by Larry White who specializes in free-banking, Austrian macroeconomics, and monetary regimes. Separately, my dad was a libertarian and I’ve attended multiple Students for Liberty events. Right now, I’m writing from my hotel room at a Catholic/Crypto conference, where I learned that the deepest trench in Dante’s Inferno includes money debasers.

Everything about my pedigree suggests that I should have a disdain for the Federal Reserve and cast a wistful gaze toward the perpetually falling value of the US dollar. But I don’t. I certainly do have opinions about what the Fed should be doing and how our monetary system could work. But I’m not excited by the long-run depreciation of the dollar.

Let me tell you why.

Learning a little bit of theory is a dangerous thing. Monetary theory is especially hard because we examine the non-good side of the transaction: the medium of exchange. In frantic excitement, enthusiasts often point out that the value of the dollar has lost very much of its value in the past 100 years. They describe that loss by describing the lower quantity of something that a dollar can purchase now versus what it could have purchased historically. That information is incapsulated in the price of a good. The price of a good is the number of dollars that one must exchange in order to purchase the good. Similarly, the price of a dollar is the number of goods that one must give up in order to purchase the dollar.

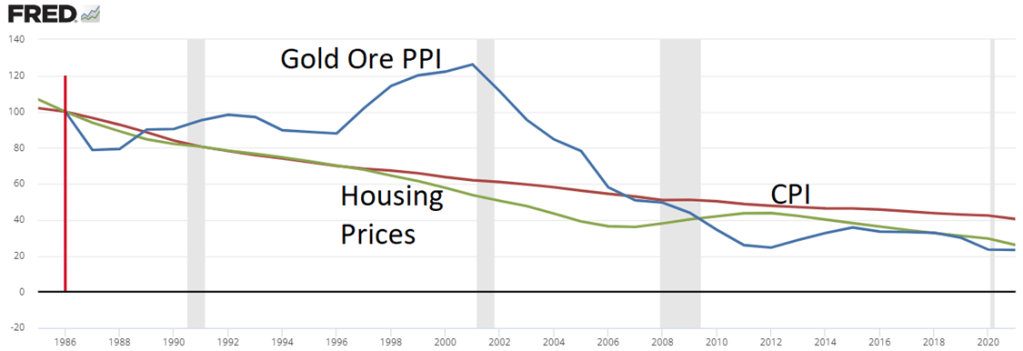

We can consider a variety of goods. Below is a graph that describes the quantity price of the dollar where the quantities are CPI basket units, gold, and housing. In the 35 years following 1986, a single dollar purchases 60% less of the consumer basket, 74% fewer houses (not quality adjusted), and 76% less gold.

This is where all of the anti-fed people get excited. They say that our savings are being decimated and that our wealth is being taxed away by inflation – the falling value of the dollar. There is a glaring problem with this reasoning. Namely, that most people do not hold their savings in in the form of dollars. Indeed, most people hold a variety of financial assets, business interests, and real estate. If you invested $1 into the typical American home in 1986, then it would be worth, on average, 284% more dollars. If you invested instead in the S&P 500, then you’d have 1,695% more dollars.

It’s not that the dollar nay-sayers have misunderstood the math. It’s that they conflate holding a dollar-denominated assets with holding actual dollars. Microeconomic theory says that there is a marginal rate of transformation between all goods. That is, any good can be converted via trade into any other good. There is no role for money. Indeed, if inflation affects the price of all items equally then the rate of transformation among the physical goods remains unchanged. Of course, different assets have different productivities, and their prices reflect that dynamic determinant of their value.

Major Point: The relative value of goods to one another is independent of the value of the US dollar.

Our savings are not being eaten away by inflation. The value of our savings is unaffected by the value of the dollar when we care about the final goods and services that we can obtain by trading away some of our savings. Of course, the major caveat is that this holds for non-dollar assets. Of course, if you are holding dollars as your major form of wealth, then the value of your savings is being eaten away. This just doesn’t apply to most people.

All of the above logic applies to the value of assets, which are a stock of resources. What about flows? People who already own assets may be insulated from the harmful effects of inflation, but what about people who earn incomes now? Aren’t the dollars that we earn worth less? Well yes, in a sense. I’m not going to try to argue against the phenomenon of currency devaluation. However, the price of labor is flexible. If the quantity of goods that one can purchase with dollars decreases, then people begin to require more dollars in compensation for their time (Paging Dr. Horpedahl). We’re accustomed to thinking about nominal median weekly earnings for wage and salary earners. But what about the labor price of money? The graph below illustrates the changing quantity of labor that the US dollar can afford. Since 1986, a dollar can purchase 64% less of the median person’s time.

So, a single US dollar can be purchased with less of most goods. Fewer labor hours, less of the consumer basket, a smaller fraction of a house, and less gold is necessary to get ahold of one dollar. But what is the net effect on people? What is the net effect of the dollar being able to afford 64.02% less labor and 59.52% less consumption? The answer is 12.5%=(1-0.5952)/(1-0.6402). Specifically, a unit of median labor can now afford 12.5% more consumption.

Do you find the above calculation confusing? Indeed, it is! There is a reason that we try not to express money in terms of the goods that can be purchased with it. Do you know what we do instead? We express the money-price of goods in inflation adjusted terms – in real terms. Do you know by how much real median wages have risen since 1986?

12.6%

That’s darn near the same number. It’s a rounding error’s worth of difference. You know what would have ben easier? Just dividing the nominal wage by CPI, which is par for the course for economists.

Major Point: The relative value of goods, labor, and output are not affected by the changing value of currency in the long run.

The devaluation of the US dollar doesn’t matter for the real value of most assets (stocks) and doesn’t matter for the purchasing power of labor (flows). That’s why I don’t get excited about the falling value of the dollar. It doesn’t matter in micro theory and the data matches the theory.

What about the impact of inflation on the taxation of capital gains?

LikeLike

I ignore the Fed response function that creates the expectation of higher FFR.

I think he concern here is that zero real returns still result in a tax bill due to the positive nominal returns. Investors care about real returns. Taxes are backed in to nominal prices. A firm with zero real return will have a nominal return that is greater than inflation because the after tax real return will be bid to zero. The result is a positive tax bill, zero real return *after taxes*.

LikeLike

If that were true then what even is the Fed dickering about for.

What about fixed pensions (without COLAs), long term mortgages, anything that fixes price (like the threshold between grand and petty theft)?

LikeLike

First, moderate inflation is part of the Fed’s mandate, regardless of whether moderate inflation is desirable (Selgin says it’s not desirable).

Second, If markets are great, then isn’t the probability distribution for the possible inflations already built in to the asset prices and contract details?

Further, on one side of a fixed payments contract is someone who bears the cost of unexpected inflation and on the other side is someone who doesn’t. He who doesn’t pays compensation for shedding that risk in the form of a higher interest rate. In this case, the unexpected inflation or deflation is a pure transfer and appropriate given the details of the contract.

As I said in the post, I’m not saying that inflation doesn’t exist. I’m saying that there is not great reason to be worried about the type of inflation that we’ve had in the US.

LikeLike

“…the deepest trench in Dante’s Inferno includes money debasers.” 🙂

LikeLike