I have done various maintenance and repairs on my cars over the decades. Usually, they turn out to be harder and more time-consuming than I thought. Changing the engine oil and oil filter has become genuinely harder since the oil filters have migrated deep up under the engine, where it is hard to access them without putting the car on a lift, and disposing of a milk jug of used oil has gotten more difficult. I used to be able to easily change out a light bulb in the headlight, but the last car where that needed doing required you to take apart much of the front end of the car to get at the headlight. However, I recently found that changing the cabin air filters in my two vehicles (van and sedan) is so easy, I wish I had started doing it years ago.

Why Change the Cabin Air Filter?

The cabin air filter filters the air coming into the passenger section of the car. It knocks out road dust and pollen, and other bits of whatever that might get sucked into your air system as you are going down the road. So, it protects your and your family’s lungs as well as the components of the air handling system. Typical recommendations are to change out the filter about once a year or every 15,000-20,000 miles.

The photo below shows the cabin air filter I just pulled out of my van after maybe 2 years and 25,000 miles, next to a relatively clean filter. Obviously, I let this one go a bit too long: it is grey with dust/dirt, and partly blocked with plant debris.

I have not been quick to change out these filters because garages or dealers often charge something like $80-$100 for this. And until recently, I never considered doing it myself, because for some reason I thought it was a hard job. I had read of people having to contort in unnatural positions with heads inserted under dashboards as they disassemble layers of car to get at the filter.

It Is (Often) Super Easy to Change a Cabin Air Filter

It all depends on where the filter is located. For most models of cars, you can find guidelines on line, including YouTube videos. There are some models where you indeed may have to unscrew a cover plate somewhere below the dashboard to expose the filter. But in most cars, you remove the glove box to expose the filter. That may involve undoing come screws or a snap or strut, and squeezing the edge of the glove box inward. For my Hondas, all I had to do was empty the glovebox, (authoritatively) squeeze in the edges, and the glove box pivoted down, and behold, there was the filter in its little holder. Then slide out the holder, pull out the old filter and put in the new filter (purchased at AutoZone for $20 each), slide the holder back in place, and finally tilt the glovebox back up until it snapped in place.

Ten minutes max, easy-peasy. Obviously, this saved money, but it also felt empowering. I highly recommend trying it.

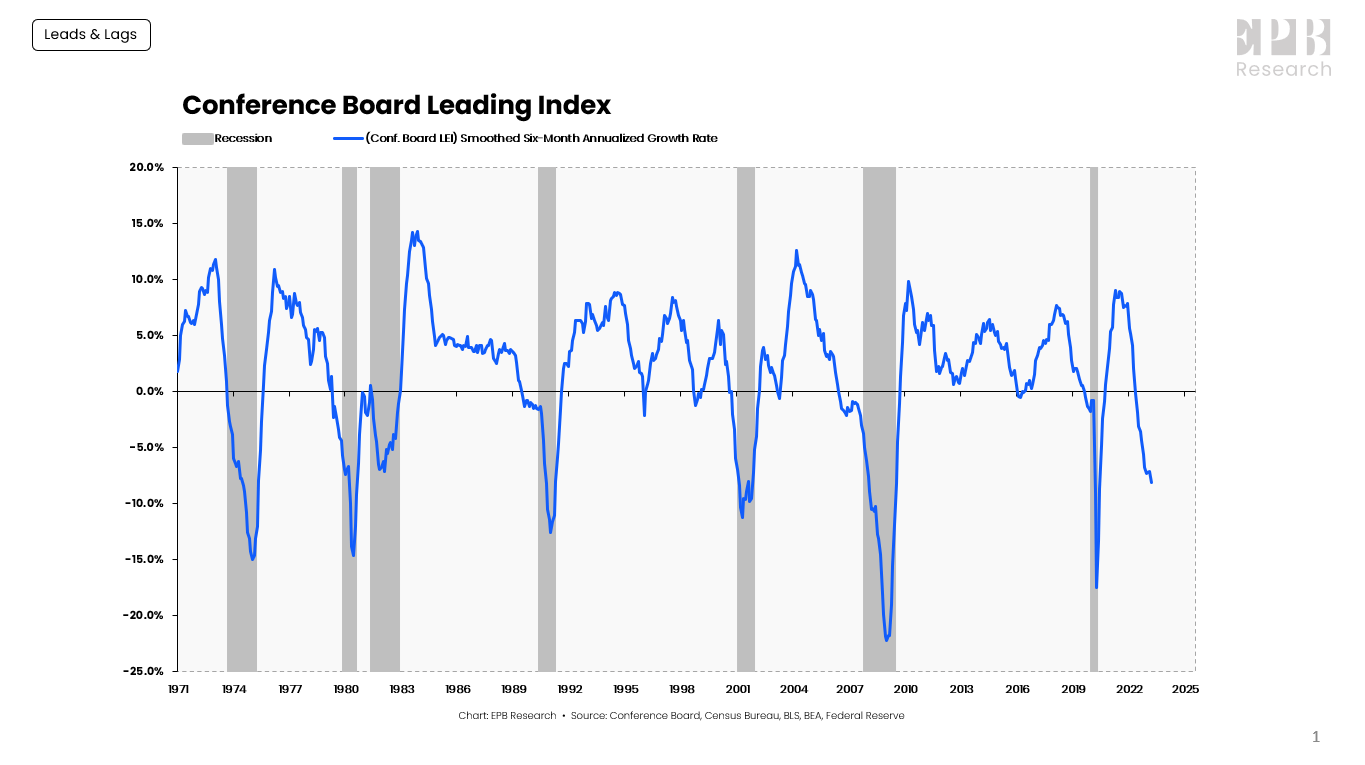

Here I will draw on a recent article Leads And Lags: Timing A Recession by Seeking Alpha author Eric Basmajian. His overall points are (1) that some indicators are associated with leading segments of the economy (which have historically turned down well before the rest), while others are more lagging, and (2) the leading indicators are strongly flashing recession. Direct quotes from his article are in italics.

Leading Economy, Cyclical Economy & Total Economy

When economic data is released, the information should be contextualized based on where the data point falls in the economic cycle sequence.

We can separate the economy into three buckets: the Leading Economy, the Cyclical Economy, and the Total Economy.

The Leading Economy is defined by the Conference Board Leading Index, which is a basket of ten leading economic variables such as building permits, new orders, and stock prices.

The Leading Index has turned negative before every recession, without exception.

Conference Board, Census Bureau, BLS, BEA, Federal Reserve

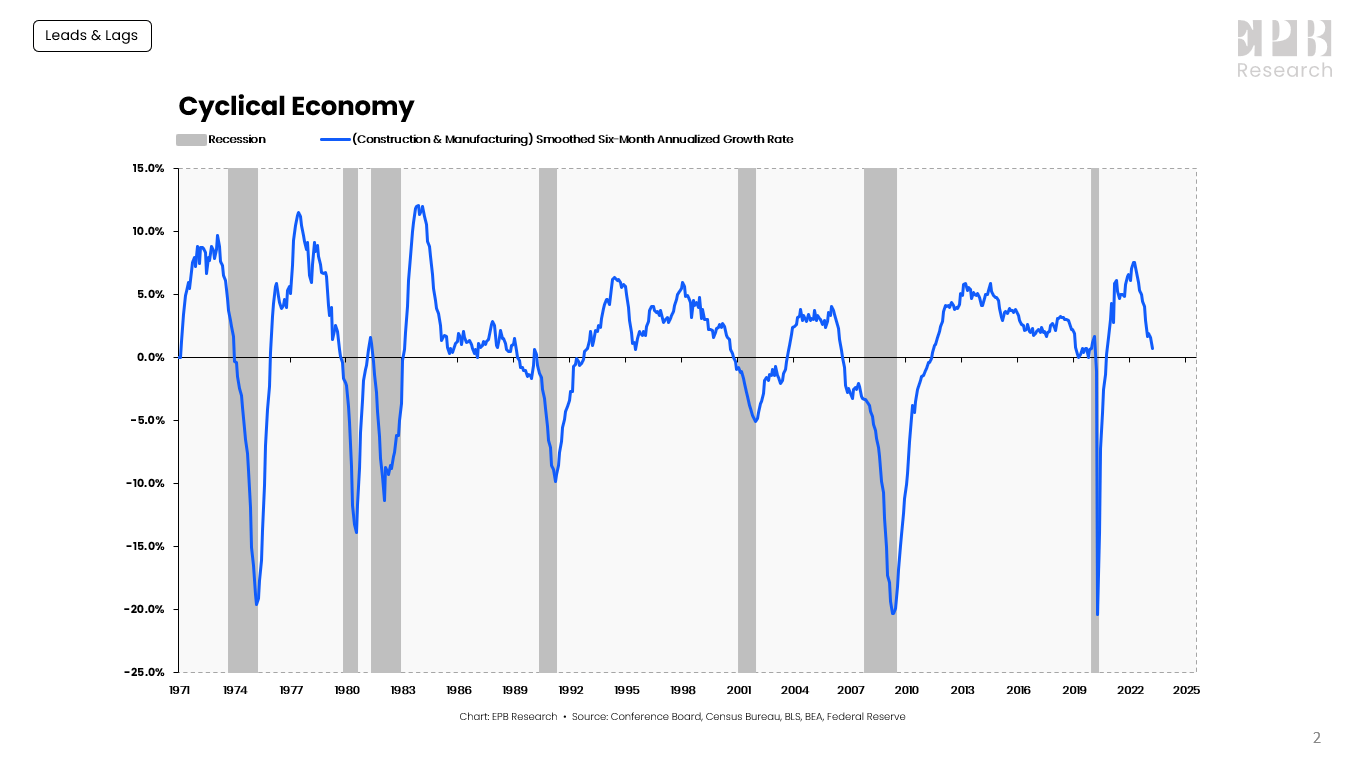

The Cyclical Economy represents the construction and manufacturing sectors. The Cyclical Economy is the driving force behind recessions, always turning negative before the Total Economy, and never giving a false signal; when the Cyclical Economy turns negative, the Total Economy turns negative several months later.

Conference Board, Census Bureau, BLS, BEA, Federal Reserve

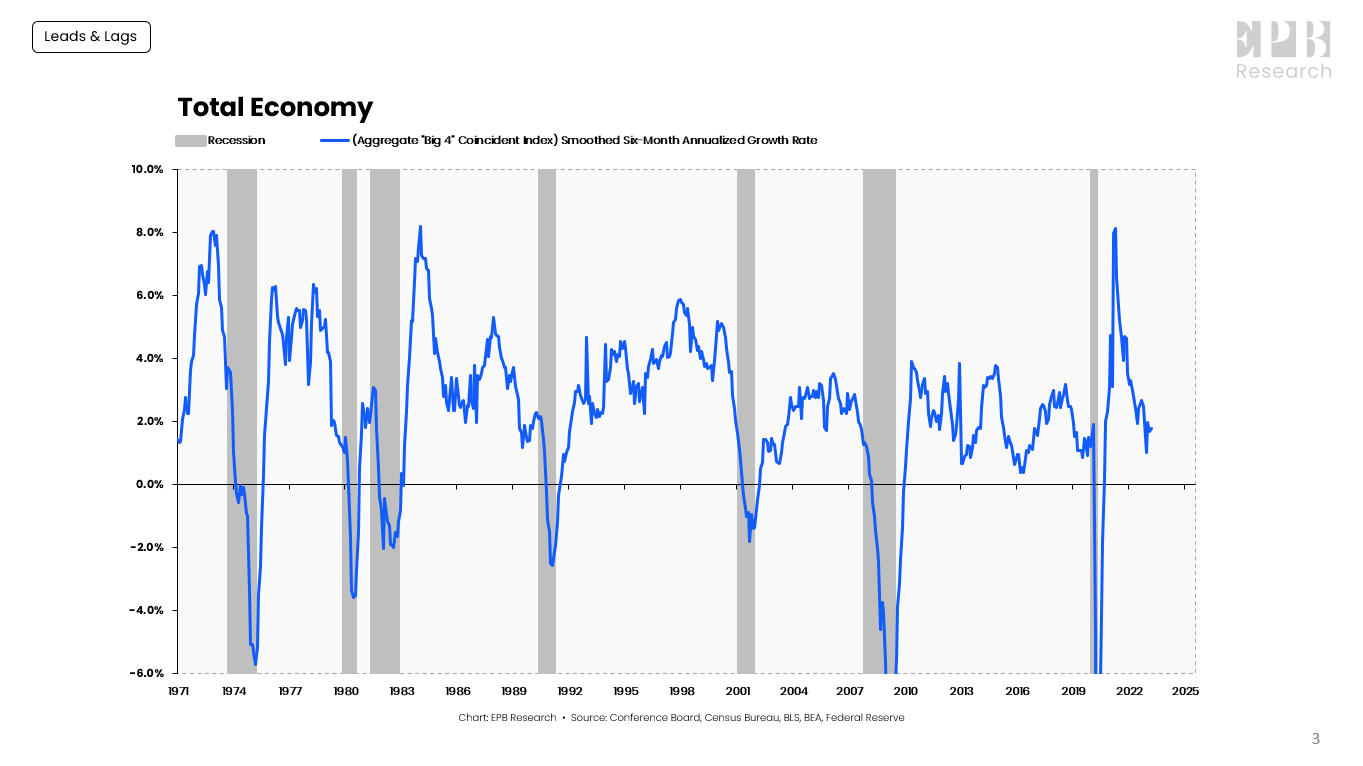

The Total Economy is defined by the “Big-4” Coincident Indicators of economic activity. Nonfarm payrolls, real personal income less transfer payments, real personal consumption, and industrial production are four major economic indicators that the NBER uses as the core of their recession dating procedure.

Conference Board, Census Bureau, BLS, BEA, Federal Reserve

A sustained contraction in the “Big-4” Coincident Indicators is the definition of a recession.

The Total Economy starts showing contracting growth rates about four months into the recession.

Could This Time Be Different?

If we do finally get a recession, it will be probably the most long-expected recession ever. Pundits have been warning for over a year that the Fed’s well-telegraphed program of rate hikes will crater the economy, as the only way to tame inflation.

According to Basmajian, When the Leading Economy and Cyclical Economy are both lower than -1%, a recession, as dated by the NBER, occurred an average of 5 months later, with a range of a 4-month lag to a 14-month lead.

His Leading indicator went negative about 11 months ago (June, 2022). However, it looks like the economy is still humming along and employment remains robust. His Cyclic Economy is on track to go negative right about now, but that has an unusually long lag between Leading and Cyclical:

The Cyclical Economy will likely turn negative with April data and potentially below -1% by May data should the current downward slope remain.

That would push the lag between the Leading Economy and the Cyclical Economy to 11 months, the longest on record.

And the lag before we finally get a bona fide recession in the Total Economy may keep dragging out longer yet. There is even a possible Soft Landing scenario where the rate hikes manage to cool the economy down without causing a severe recession at all.

It seems to me that we collectively are still spending down our excess pandemic benefits, and no recession will come till we finish running through those monies.

Apart from some possible geopolitical upset (and theater with the debt ceiling), the Big Issue for the larger economy, and for investing decisions, remains how fast inflation will decline – since that governs how soon the Fed can relent on keeping interest rates high. Those high interest rates are having all kinds of knock-on effects, including bank failures and suppressed home sales.

The investing market seems to be pricing in expectations of significant Fed rate cuts before the end of 2023, which in turn presupposes that inflation will have ratcheted downwards far enough by then to allow the Fed to declare victory. Goods inflation (= mainly stuff made in China) has declined nicely, but services (which comprise the majority of household spending) remains high. It is coming down, but too slowly to realistically hit the Fed’s 2% target this year.

In an article in the Seeking Alpha site title Services Inflation Is Stuck, the investment firm Blackrock notes some technical factors that will likely keep services inflation high for at least the remainder of this year. I will paste in their text in italics:

Core Services ex-Shelter inflation is a bit of a hodgepodge that includes things like medical care services, video and audio services, tuition, and insurance. It comprises roughly a quarter of the CPI basket and, importantly for the Fed, is very domestically oriented.

A key insight from this article is that nearly two-thirds of this key “Core Services ex-Shelter” component consists of:

(1) Service prices that are regulated (especially insurance), and

(2) Services with infrequent price resets (such as tuition and especially medical services):

There are technical factors that make it likely that these particular items will see ongoing, sticky inflation:

Impact of Regulated Prices

Regulated prices tend to be more discrete and more lagged in their changes due to bureaucratic delays and their negotiated nature. Some types of regulated prices, like postage or water and sewage fees, are easily recognizable as subject to government regulation. Somewhat less intuitive is the degree to which insurance in the United States is a regulated price. Insurance comprises the largest share of Core Services ex-Shelter basket and state-level insurance commissioners play important roles in negotiating auto, property, and casualty insurance price changes.

The underwriting costs of insurance have been surging globally – a combination of higher reinsurance premiums, inflated asset values, and more natural disasters. These rising costs have only just begun to flow through into consumer prices; auto insurance costs were an upside surprise within March’s CPI report.

Jumps in Medical and Education Prices Will Appear Later

Though the market has been fixated on the painstaking details of the month-over-month inflation prints, many of the sub-components of the CPI do not update monthly. Two of the more important items within the core services basket – medical care services and tuition – only update their prices annually. Coincidentally, updates for both of these categories take place in the autumn, and both are set to rise strongly.

Medical care services are the largest component (28%) of Core Services ex-Shelter, but have a complex and lagged computation and update only once a year in October. Medical services inflation has been negative since last October as a consequence of excess consumer demand for post-pandemic doctors’ visits, however, we expect this mechanical effect will abate later this year and thereafter lift core services inflation.

Tuition is another example of a service with intermittent price resets, given prices are set on the basis of the academic year. We expect the broad-based upward wage pressure in education to be passed through to higher education consumer prices later this year when students return to school.

And so…I expect “higher for longer” inflation and interest rates.

Rare earths are a set of 17 metals with properties which make them essential to a swathe of high-tech products. These products include lasers, LEDs, catalysts, batteries, medical devices, sensors, and above all, magnets. Rare earth magnets are used in electric motors and generators and vibrators, making them essential to electric cars, wind turbine generators, cell phones/tablets/computers, airplanes, phones, and all sorts of military devices.

China happens to have large amounts of rare earth oxide ores for mining, relatively lax environmental standards, and a large, compliant workforce. The Chinese government has harnessed these resources to make the nation by far the largest producer of rare earths. Their massive, relatively low-cost production has suppressed production in other countries. This has been a conscious policy, to achieve global control over a vital raw material.

The first time China used this effective monopoly as a political weapon was in a maritime dispute with Japan in 2010. China cut off exports of rare earth metals to Japan for two years, crimping the Japanese electronics industry. Other nations took note of this threat, and since then have been a number of half-hearted (in my opinion) efforts in various Western nations to develop some domestic capacity and to redesign motors to reduce dependence on rare earth materials.

China’s share of rare earth ore mined is down to 60%, but they totally dominate processing the ore to metals, and subsequent fabrication of magnets from the metal. Nearly all of the ore mined in the U.S. is shipped over to China for processing, mainly because of environmental regulations here.

The PRC still dominates the entire vertical industry and can flood global markets with cheap material, as it has done before with steel and with solar panels. In 2022, it mined 58% of all rare earths elements, refined 89% of all raw ore, and manufactured 92% of rare earths-based components worldwide.

There is no other global industry so concentrated in the hands of the Chinese Communist Party, nor with such asymmetric downstream impact, as rare earths.

It seems the only way for the West to blunt the Chinese monopoly in rare earths is with large, long-term subsidies (since the Chinese can always undersell the rest of the world on a free market basis) and probably some pushing past environmental objections.

Alarmed by the rapid buildup of Chinese military forces (towards a possible invasion of Taiwan), the U.S. and its allies have begun restricting exports of the highest-power silicon chips to China. In retaliation, China has reportedly made plans to restrict exports of rare earths, starting in 2023. If they follow through, that move would crush fabrication of magnets and of magnet-dependent devices like motors and generators in other countries; the rest of the world would have to come crawling to China for all these items.

This move would in turn cause the rest of the world to accelerate its plans to produce rare earths outside China, but there would be several years of great disruption, and Chinese-made final devices like motors and generators would always have a huge price advantage, due to their cheaper raw material inputs.

I suspect there may be a high-stakes game of brinksmanship going on behind the scenes. The Chinese leadership presumably knows that they can only play this rare earth export ban card once, and the West does not really want to plow a lot of resources into producing large amounts of rare earths much more expensively than they can be bought from China. So maybe we will see some relaxation in chip export controls for China in exchange for them not pulling the final trigger on a rare earth export ban.

In the past year, one cryptocurrency firm after another has gone bust, culminating in the grand implosion of the FTX exchange. The crypto vortex also contributed to some of the recent banking failures.

The prices of cryptocurrencies shot up in 2021, probably fueled by pandemic stimulus money sloshing around in the bank accounts of restless 20- and 30-somethings. All this came crashing back to earth in 2022, giving ample scope for skeptics to say, “I told you this was all foolishness.” Last rites were said, and crypto was left for dead.

But wait… in 2023, when no one was looking, the lid of the crypto coffin started to rattle, a bony hand reached out, and…crypto is back!!

Well, sort of. Here is a five-year chart of Bitcoin from Seeking Alpha, in U.S. dollars:

And here is the past six months:

We can see that Bitcoin took its final big leg down in November, 2022, with the FTX collapse. Its price stayed fairly plateaued down there (with heavy trading volume) until January. Since then, it has nearly doubled.

What has triggered this rise in 2023? Observers such as Michael Grothaus at Fast Company suggests some four factors:

( a ) A shift to “risk-on” with the prospect of the Fed easing off with interest rate hikes this year.

( b ) A flight to alternative assets in the wake of the turbulence in the banking sector. Also, since the total amount of bitcoin is programmed to never increase over a certain number, Bitcoin should be a hedge against inflation. (Many observers believe that the Fed will live with 3-4 % inflation indefinitely, to help inflate away the gigantic debt that the federal government incurred with pandemic relief).

( c ) Buying of Bitcoin by traders who were short, and now need to cover their positions.

( d ) The usual rise in Bitcoin values as a bitcoin “halving” event is on the horizon. (About every four years, with the next time scheduled for May 2024, the rewards for mining new bitcoins drops by 50%).

Will the rise in Bitcoin prices continue? Is this truly a resurrection from the dead, or just a “dead cat bounce”? [1] Nobody knows. But this latest, sustained rally seems to have helped it recover some luster of legitimacy as an asset class. Here is a list of some popular crypto exchanges that are still in operation.

My personal take: I hold a sliver of the Bitcoin fund GBTC, just to have some skin in the game. I have been too lazy to learn about and activate an actual crypto wallet. I think Bitcoin in particular is an intriguing entity. Many other cryptos at some level depend on some centralized administration, but Bitcoin embodies the ideal of a decentralized, power-to-the-people form of something like money.

[1] From Wikipedia: In finance, a dead cat bounce is a small, brief recovery in the price of a declining stock. Derived from the idea that “even a dead cat will bounce if it falls from a great height”, the phrase is also popularly applied to any case where a subject experiences a brief resurgence during or following a severe decline. This may also be known as a “sucker rally”.

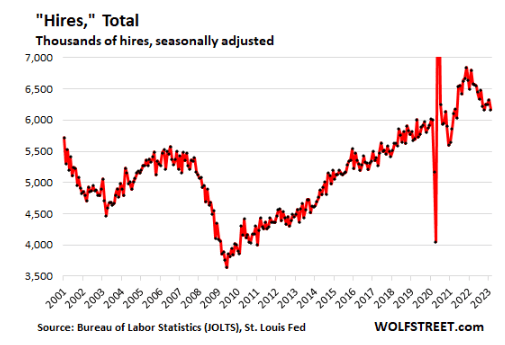

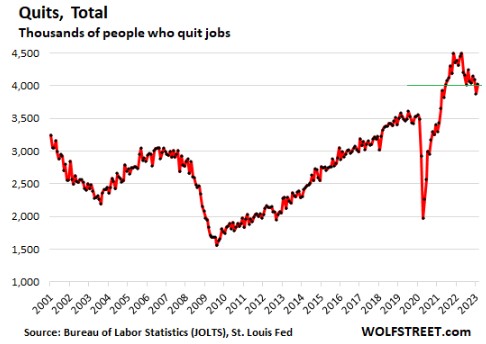

As noted earlier, the main driver in inflation since 2021 has not been supply chain issues, but ongoing wage increases in (mainly) the service industry, fueled by a tight labor market. Some headlines note recent decreases in job openings, etc., suggesting that the end of inflation is near. The point of this post is that measures of labor market tightness remain at very high levels, and so it will be a while yet before the Fed can claim victory over inflation and start meaningfully reducing interest rates.

Below I will post a set of charts (courtesy of Seeking Alpha article by Wolf Richter) which make the following point: most measure of labor tightness remain at least as high as they were in late 2019, just before the pandemic hit. It is true that things have loosened up in the past few months, but that just means the labor market has gone from white-hot to merely red-hot. Let the data speak:

We hold that the current tightness of the labor market is largely a result of pandemic policies which incentivized a whole tranche of experienced workers to take early retirement and also put lots of cash in our pockets which we are spending generously on services . Those workers are not coming back, but at some point in the next 1-2 years the excess Covid cash will run out and we may finally get the long-expected recession. But if the government rushes in with enhanced unemployment benefits to ease the recession pain, we would expect inflation to remain well above the nominal 2% target

As you drive through cities and many suburbs near cities, you see lot and lots and lots of office buildings. Employees by the tens of millions used to get dressed and fight their way through traffic to get to these building every weekday, park, and go up to their desks to do their white-collar jobs.

The demand for new office space seemed endless, and so developers borrowed money to build more office buildings, and firms like real estate investment trusts (REITs) also borrowed money to buy such buildings in order to rent them out.

Covid changed all that. Suddenly, in early/mid 2020, nearly all office buildings went dark, and people started working from home. With affordable computers and internet access, and with Zoom and other conferencing tools, it was found that workers could get their jobs done remotely. Even after vaccines rolled out in early/mid 2021, concerns over contagious Covid variants kept offices closed. 2022 was when things started opening up again big time, and by end 2022/early 2023 there were stories in the news about companies ordering employees back to their desks.

By January, 2023 Bloomberg could report “More than half of workers in major US cities went to the office last week, the first time that return-to-office rates crossed 50% of their pre-pandemic levels.” However, that movement seems to have stalled, and has even reversed in some cases, as workers have pushed back strongly against being forced back to the cubes. Notably, Elon Musk initially banned remote work at Twitter after taking it over in November, but after rethinking the costs of maintaining offices, has shut down Twitter’s offices in Seattle and Singapore, telling employees to work from home

Per the Morning Consult, “The pandemic lockdown triggered one of the swiftest, most significant behavior changes in human history. People’s habits changed overnight, and through the successive lockdowns, shutdowns and new standards, these new habits became ingrained. The experience triggered new, positive associations with working from home, working out with virtual trainers, cooking, gardening and more. A vast web of neural pathways formed to hold these new associations – and that web runs deep.”

And thus, many office buildings remain largely empty, which in turn is resulting in rising defaults on the loans for these buildings. A number of high profile corporate owners in recent months have deliberately (in their own pecuniary interest) defaulted on their loans, forfeited their equity interest in a building , and handed the keys back to the mortgage lenders, who are now stuck with big losses on their loans and with holding a building that nobody much wants.

There are many ramifications of these trends. The one I will focus on is how this extended underutilization of offices affects the parties that lent money to build or buy these buildings. In many cases, those lenders were smaller (regional) banks. They have much greater exposure to commercial real estate loans than the larger banks, which may cause serious problems in the coming months.

Eric Basmajian calls out some key differences between large and small banks in the U.S.:

At large US banks, loans make up 51% of total assets. Small banks have 65% loans as a percentage of total assets. So small banks have a lot of loans, and large banks have a lot of cash, Treasury bonds, and MBS.

…At small US banks, loans make up 65% of assets. Of that loan portfolio, real estate is 65%, meaning a lot of real estate exposure….Within that real estate loan portfolio, almost 70% was commercial real estate lending. So small banks have a high concentration of commercial real estate loans…. Within the commercial real estate category, the highest concentration is “non-residential property,” which can include office buildings, retail stores, and data centers.

….So small banks have a potentially large problem. Deposits are starting to leave after the SVB crisis in search of more safety, but also in search of higher yields on safe assets like Treasury bills. Deposit outflows will make it hard for small banks to grow lending and may cause a deleveraging. If deposit outflows are severe, deleveraging will cause banks to sell securities or loans.

Securities can be pledged at the Fed for a relatively high-interest rate. This keeps a bank solvent but at a material hit to earnings. The loan portfolio is a much bigger problem because the value of these potentially permanently impaired assets will be called into question.

Basmajian summarizes:

There are major differences between large and small US banks.

Large banks hold a lot of reserves, Treasuries, MBS, and residential real estate loans. The asset mix at large banks is very conservative.

Small banks have most of their assets in loans, with commercial real estate holding the highest weight. Small banks appear to have outsized exposure to highly impaired office buildings which could generate significant losses.

It will be critical to monitor lending standards and availability at small banks because, in the post-2008 cycle, small banks are the lifeblood of credit to the private economy.

It has been a tumultuous several weeks in the world of finance. Just when “soft landing” (i.e., the notion that Fed rate hikes would tame inflation without causing a nasty recession) was the meme, a string of banks went belly-up. We summarized the history and status of this dismal parade of corpses a week ago.

On Friday, Germany’s Deutsche Bank (DB) was added to the list of endangered financial species. Its share price plunged as the cost of insuring its credit swaps soared, a sign of lack of confidence in DB among other financial parties. As best I can discern, however, DB is a relatively poorly-managed bank, but not one teetering on insolvency like Credit Suisse or the smaller American banks that have collapsed.

Silicon Valley Bank Getting Sold Off, Finally

On this side of the pond, the big news is that Silicon Valley Bank (SVB), whose spectacular implosion was really what brought “crisis” to banking, will be taken over by another regional bank, First Citizens Bank of North Carolina. The first attempt to auction off SVB was a fizzle, so the feds tried again. They really, really wanted to get this kind of full takeover deal done (rather than breaking up SVB and selling off bits piecemeal), so First Citizens was able to drive a juicy bargain. First Citizens was a fairly modest-sized bank, about half the size of SVB at the end of last year. First Citizens will get SVB assets of $110 billion, deposits of $56 billion and loans of $72 billion, and will start operating the SVB branch offices again. They will pay only $55 billion for the nominal $72 billion in loans that SVB had made, a 29% mark-down. The cost to the FDIC for this deal is about $20 billion. (I don’t know how First Citizens is paying for this acquisition). First Citizens stock skyrocketed on this news, so the market sees this as a sweet deal for First Citizens.

Going forward, the FIDC has pledged to share any losses (or gains) on those loans in the future, which offers further protection to First Citizens. FDIC gets shares of First Citizens valued up to $500 million. First Citizens decided not to take an additional $90 billion in securities that the FDIC will now have to sell on its own. These are likely the long-term bonds which sunk SVB when their value cratered with rising interest rates this past year. I’m not sure how much further losses the FDIC will bear on these bonds.

Anyway, so far, so good, kind of; it is sobering to note that this $20 billion cost to the FDIC just chewed up 1/6 of its total $128 billion kitty for backstopping all qualifying deposits at all banks in America. So we can’t readily afford too many more meltdowns of this magnitude.

Bank Deposits Continue to Flee, But Slower

A worrisome trend in the past month or so has been for depositors to pull their funds from bank checking/savings accounts, and stash their money instead in higher yielding money market funds or CDs or Treasury bills. Banks have borrowed records amounts from the Fed in recent weeks, in order to have lots of cash on hand if they have to pay off departing clients. And within the banking system, about half a trillion dollars has been moved from smaller regional banks to large banks.

I can’t find the reference now, but in the past two days I read an article stating that rate of deposit withdrawals is slowing down, and will likely not of itself destabilize the system. I’m going with that narrative, for now.

An indirect fallout from all this bank turmoil is the reduced inclination of banks to extend loans to businesses. This will make for a slowdown in economic activity, which should cool off inflation – -which is exactly what Jay Powell was hoping would be the outcome of the Fed rate hikes.

So much has been happening in the banking world it is a little hard to keep track of it. See recent articles here by fellow bloggers Mike Makowsky, Jeremy Horpedahl, and Joy Buchanan. Here is a quick guide to all the drama.

Credit Suisse Takeover by UBS

Perhaps the biggest, newest news is a shotgun wedding between the two biggest Swiss banks announced over the weekend. Credit Suisse is a huge, globally significant bank that has suffered from just awful management over the last decade. Its missteps are a tale in itself. Its collapse would be an enormous hit to the Swiss financial mystique, and would tend to destabilize the larger western financial system. So the Swiss government strong-armed a takeover of Credit Suisse by the other Swiss bank behemoth, UBS, in an all-stock transaction. The government is providing some funding, and some guarantees against losses and liability. An unusual aspect of this deal is that Credit Suisse shareholders will get some value for their stock, but a whole class of Credit Suisse bonds Is being written down to zero. Usually bond holders have strong priority over stockholders, so this may make it more difficult for banks to sell unsecured bonds hereafter.

Silicon Valley Bank Collapse: Depositors Protected

The Silicon Valley Bank (SVB) collapse is old news by now. The mismanagement there is another cautionary tale: despite having a flighty tech/venture capital deposit base, management greedily reached for an extra 0.5% or so yield by putting assets into longer-term bonds that were vulnerable to a rise in interest rates instead of into stable short-term securities.

A key step back from the brink here was the feds coming to the rescue of depositors, brushing aside the existing $250,000 limit on FDIC guarantees. That was an important step, otherwise large depositors would stampede out of all the regional banks and take their funds to the few large banks that are in the too-big-to-fail category. It is true that this new level of guarantee encourages more moral hazard, since depositors can now be more careless, but the alternative to guaranteeing these deposits (i.e. the collapse of regional banks) was just too awful. Bank shareholders and most bondholders were wiped out. Presumably that will send a message to the investing community of the importance of risk management at banks.

The actual disposition of the business parts of SVB are still being worked out. The feds originally tapped the big, well capitalized banks to see if one of them would take over SVB as a going concern. That would have been a nice, clean, thorough resolution. But the big banks all declined. I suspect the actual responses in private were unprintable. Here’s why: in the 2008 banking crisis, the Obama-Biden administration went to the big banks and encouraged them to take over failing institutions like Countrywide Mortgage, who among other things had made arguably predatory loans to subprime borrowers who had poor prospects to keep up with the mortgage payments. The Obama administration’s Department of Justice promptly turned around and very aggressively prosecuted these big banks for the sins of the prior institutions. J. P. Morgan ended up paying something like 13 billion and Bank of America paid 17 billion. So when today’s Biden administration reached out to these big banks this month to see about taking over SVB, they got no takers.

Now the assets of SVB (renamed Silicon Valley Bridge Bank) are getting auctioned off, perhaps piecemeal, but how exactly that happens does not seem so critical.

Signature Bank: Shut Down, But Sold Off Intact

Crypto-friendly Signature Bank was shuttered by New York State officials on Sunday, March 12, making this the third largest (SVB was the second largest) bank failure in U.S. history. Forbes gives the whole story. At the end of last year, Signature had over $110 billion in assets and $88 billion in deposits. Spooked by Signature’s similarities to failed banks SVB and Silvergate, customers rushed to withdraw deposits, which the bank could not honor without selling securities at huge losses. As with SVB, the feds had the FDIC insure all deposits of all sizes at Signature.

Unlike SVB, Signature has received a bid for the whole business, from New York Community Bancorp’s subsidiary Flagstar Bank. Flagstar will take over most deposits and loans and other assets, and operate Signature Bank’s 40 branches.

First Republic: Teetering on The Brink, Propped Up by Banking Consortium

First Republic is in a somewhat different class than these other troubled institutions. Its overall practices seem reasonable, in terms of equity and assets. However, it caters to a wealthy clientele in the Bay Area, with a lot of accounts over the $250,000 threshold. In the absence of a rapid and decisive move by Congress to extend FDIC protection to all deposits at all banks, somehow (I haven’t tracked what started the stampede) depositors got to withdrawing huge amounts (like $70 billion) last week. This was a classic “run on the bank.” That would stress any bank, despite decent risk management. Once confidence is lost, it’s game over, since there are always alternative places to park one’s money. Ratings agencies downgraded First Republic to junk status, and the stock has cratered.

It is in the interest of the broader banking industry to forestall yet another collapse. If folks start to generally mistrust banks and withdraw deposits en masse, our whole financial system will be in deep trouble. In the case of First Republic, the private sector is trying to prop up it up, without a government takeover. So far this has mainly taken the form of depositing some $30 billion into First Republic, as deposits (not loans or equity), by a consortium of eleven large U.S. banks led by J. P. Morgan. This is was a quick and fairly unheroic intervention, since in the event of liquidation, depositors (including this consortium) have the highest claim on assets. This intervention will probably prove insufficient. Two potential outcomes would be a big issuance of stock to raise capital (which would dilute existing shareholders), or some large bank buying First Republic. The stock rose today on reports that Morgan’s Jamie Dimon was talking with other big banks about taking an equity stake in First Republic, possibly by converting some of the $30 billion deposit into equity.

Old News: Silvergate Bank Liquidation

Overshadowed by recent, bigger collapses, the orderly shutdown of the crypto-focused Silvergate Bank is old news. It was two weeks ago (March 8) that Silvergate announced it would shut down and self-liquidate. The meltdown of the crypto financing world led to excessive loss of deposits at Silvergate. Unlike SVB and Signature, it held a lot of its assets in more liquid, short-term securities, so its losses have not been as devastating – – all depositors will be made whole, though shareholders are toast (stock is down from $150 a year ago to $1.68 at Monday’s close).

Warren Buffett To the Rescue?

Banks generally operate on the model of borrow short/lend long: they “borrow” from depositors and buy longer-term securities. Normally, short-term rates are lower than long-term rates, so banks can pay out much lower interest on their deposits than they receive on their bond/loan investments. With the Fed’s rapid increases in short-term rates this past year, however, the rate curve is heavily inverted, which is disastrous for borrow short/lend long. Fortunately for banks, many depositors are too lazy to do what I have done, which is to move most of my immediate-need money out of bank accounts (paying maybe 1%) and into T-bills and money market funds paying 4-5%.

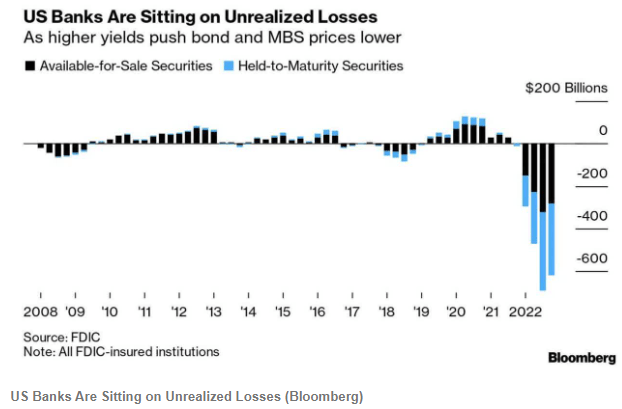

All this churn goes to highlight an inherent fragility of banks: there is typically a maturity mismatch between a bank’s deposits/liabilities (which are short-term and can be withdrawn at any time) and its assets (longer-term bonds it purchases, and loans that it makes which can be difficult to quickly liquidate). Runs on banks, where if you were late to panic you lost all your deposited money, used to be a real feature of life, as dramatized in classic films Mary Poppins and It’s a Wonderful Life. Eliminating this danger was a key reason for setting up the Federal Reserve system, and in general that has worked pretty well in the past hundred years. Banks in general (see chart above) are now carrying enormous amounts of unrealized losses on their portfolios of bonds and mortgage-backed securities (MBS) due to the increase in market rates. In addition to the existing “discount window” at which banks can borrow, the Fed has set up a new lending facility to help tide banks over if they (as in the case of SVB and Signature) get stressed by having to sell marked-down securities to cover withdrawal of deposits. Also, new measures reminiscent of 2008 were announced to extend dollar liquidity to central banks of other nations.

But when Gotham really has a problem, the Commissioner calls in the Caped Crusader. Warren Buffett has been in touch with administration officials about the banking situation. We wrote two weeks ago about Warren Buffett’s gigantic cash hoard from the float of his Berkshire Hathaway insurance businesses which allows him to quickly make deals that most other institutions cannot. Buffett rode to the rescue of large banks like Bank of America and Goldman Sachs in the 2008-2009 financial crisis. A lot of corporate jets have been noted flying into Omaha from airports near the headquarters of various regional banks. Buffett’s typical playbook in these cases is to have the troubled institution issue a special class of high yielding (with today’s regional banks, think: 9%) preferred stock that he buys, perhaps with privileges to convert into the common stock. That stock would count as much needed equity in the banks’ books.

On the Positivity Blog are no less than “67 Don’t Look Back Quotes to Help You Move on and Live Your Best Life”. Some of these sayings from notable folks include:

“Never look back unless you are planning to go that way.” – Henry David Thoreau

“If you want to live your life in a creative way, as an artist, you have to not look back too much. You have to be willing to take whatever you’ve done and whoever you were and throw them away.” – Steve Jobs

“There are far, far better things ahead than any we leave behind.” – C.S. Lewis

“Don’t cry because it’s over, smile because it happened”

– attributed to Dr. Seuss, though that attribution is heavily disputed

The Random Vibez offers another “60 Don’t Look Back Quotes To Inspire You To Move Forward”’ including “Don’t look back. You’ll miss what’s in front of you” and “I tend not to look back. It’s confusing”. The Bible would add sayings such as, “Let your eyes look straight ahead; fix your gaze directly before you” (Proverbs 4:25); Paul wrote to the Philippians, “One thing I do: Forgetting what is behind and straining toward what is ahead, I press on toward the goal to win the prize for which God has called me”.

The Landy-Bannister Statue

What put me in mind of this whole theme of not looking back was seeing a bronze statue involving Roger Bannister. Sports buffs, and most educated people who are over 60, will know that he was the first man to break the four-minute mile. During many previous decades of trying, no human had been able to run that fast that long: that is a velocity of 15 miles per hour, sustained for a full four minutes. That is like a full sprint for most people, or a moderate bicycling speed.

Bannister found that he was naturally a fast runner, and he employed scientific principles in his training. (He was a medical student at the time, and went on to become a noted research neurologist). On May 6, 1954 Bannister finally cracked the four-minute mile, with a 3:59.4 time. As may be imagined, the crowd went wild.

Records, however, are made to be broken, and just 46 days later a rival runner, John Landy, ran the mile in just 3:57.9 to become the world’s fastest man. A few months after that Bannister and Landy ran head-to-head in the August, 1954 Commonwealth games in Vancouver. Landy was in the lead nearly the whole way, with a ten-yard lead by the end of the third lap. Bannister then started his signature kick and managed to catch up with Landy on the final bend. Landy must have heard footsteps, and at the end of the race glanced over his left shoulder to gauge Bannister’s position. That distraction slowed him just enough to allow Bannister to power past him on his right side. Landy’s time was still a respectable 3:59.6, but Bannister won with 3:58.8. Both runners later agreed that Landy would have won if he had not looked back. More on that race, including link to video of it, here.

This finish of this “Miracle Mile” race was immortalized by a larger-than-life bronze statue by Vancouver sculptor Jack Harman. Landy later quipped, “”While Lot’s wife was turned into a pillar of salt for looking back, I am probably the only one ever turned into bronze for looking back.”

{kind=link}

{kind=link}

{kind=link}

{kind=link}