UPDATE: Michael Green has written a follow-up post which essentially agrees that $140,000 is not a good national poverty line, but he still has concerns. I have written a new response to his post.

A recent essay by Michael W. Green makes a very bold claim that the poverty line should not be where it is currently set — about $31,200 for a family of four — but should be much higher. He suggests somewhere around $140,000. The essay was originally posted on his Substack, but has now gone somewhat viral and has been reposted at the Free Press. (Note: that actual poverty threshold for a family of four with two kids is $31,812 — a minor difference from Mr. Green’s figure, so not worth dwelling on much, but this is a constant frustration in his essay: he rarely tells us where his numbers come from.)

I think there are at least three major errors Mr. Green makes in the essay:

He drastically underestimates how much income American families have.

He drastically overstates how much spending is necessary to support a family, because he uses average spending figures and treats them as minimum amounts.

He obsesses over the Official Poverty Measure, since it was originally based on the cost of food in the 1960s, and ignores that Census already has a new poverty measure which takes into account food, shelter, clothing, and utility costs: the Supplement Poverty Measure.

I won’t go into great detail about the Official Poverty Measure, as I would recommend you read Scott Winship on this topic. Needless to say, today the OPM (or some multiple of it) is primarily used today for anti-poverty program qualification, not to actually measure how well families are doing today. If we really bumped the Poverty Line about to $140,000, tons of Americans would now qualify for things like Medicaid, SNAP, and federal housing assistance. Does Mr. Green really want 2/3 of Americans to qualify for these programs? I doubt it. Instead, he seems to be interested in measuring how well-off American families are today. So am I.

Tomorrow, the Bureau of Labor Statistics is set to release the first major report of economic data that was delayed by the federal government shutdown: the September 2025 employment situation report. It’s good that we will get that information, but notice that we’re now in the middle of November and we’re just now learning what the unemployment rate was in the middle of September — 2 months ago (you can see their evolving updated release calendar at this link). This is less than ideal for many reasons, including that the Federal Reserve is trying to make policy decisions with a limited amount of the normal data.

What about the October 2025 unemployment rate? Early indications from the White House are that we just will never know that number. Why? Because the data likely wasn’t collected, due to the federal government shutdown. There was some confusion about this recently, with many people asking why they don’t just release it. Well, that’s because they can’t release what they don’t collect: the unemployment rate comes from the Current Population Survey, a joint effort of the BLS and Census where they interview 60,000 households every month. The survey was not done in October. It would not be impossible to do this retroactively, but the data would be of lower quality and, again, quite delayed. That gap in a series that goes back to 1948 wouldn’t be the end of the world, but it is symbolic of the disfunction of our current political moment.

What about GDP? We are now over half way through the 4th quarter of the year, and… we still don’t know what happened with GDP in the third quarter of 2025. BEA is in the process of revised their release calendar too, but they haven’t yet told us when 3rd quarter GDP will be released. In this case, the data was likely collected, but there is a certain amount of processing that needs to be done. Sure, we have estimates from places like the Atlanta Fed’s GDPNow model, but the trouble is… many of the inputs it uses are government data which haven’t been released yet for the last month of the quarter.

Eventually, all will mostly be well and back to normal, even if there are a few monthly gaps in some data series. The temporary data darkness may be coming to an end soon, but I fear it will not be the last time this happens.

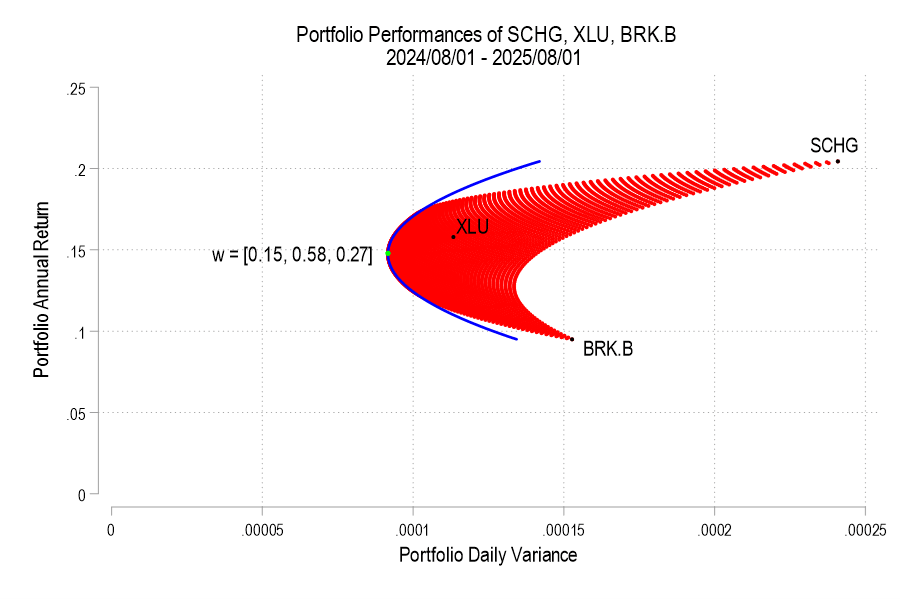

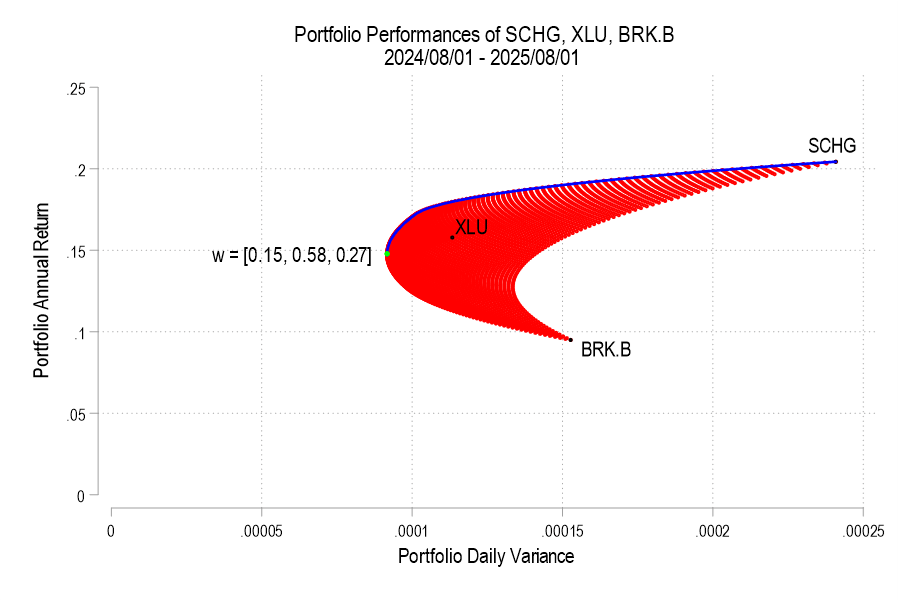

Previously, I plotted the possible portfolio variances and returns that can result from different asset weights. I also plotted the efficient frontier, which is the set of possible portfolios that minimize the variance for each portfolio return.* In this post, I elaborate more on the efficient frontier (EF).

To begin, recall from the previous post the possible portfolio returns and variances.

From the above the definitions we can see that the portfolio return depends on the asset weights linearly and that the variance depends on the asset weights quadratically because the two w terms are multiplied. Since the portfolio return can be expressed as a function of the weights, this implies that the variance is also a quadratic function of returns. Therefore, every possible portfolio return-variance pair lies on a parabola. So, it follows that every pair along the efficient frontier also lies on a parabola. Not every pair lies on the same parabola, however – the efficient frontier can be composed on multiple parabolas!

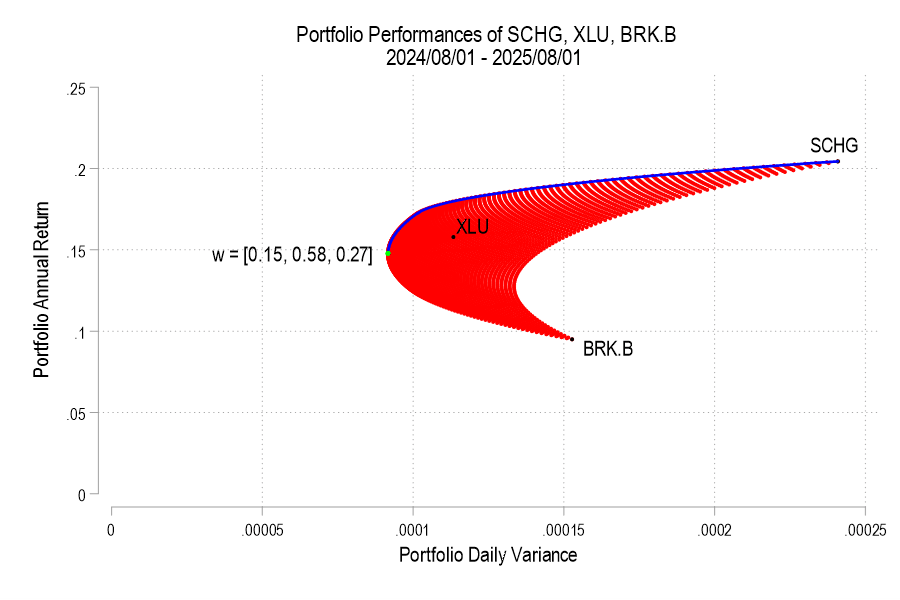

I’ll use the same 3 possible assets from the previous post, below is the image denoting the possible pairs, the EF set, and the variance-minimizing point.

One way to find the EF is to calculate every possible portfolio variance-return pair and then note the greatest return at each variance. That’s a discrete iterative process and it definitely works. One drawback is that as the number of assets can increase the number of possible weight combinations to an intractable number that makes iterative calculations too time consuming. So, we can instead just calculate the frontier parabolas directly. Below is the equation for a frontier parabola and the corresponding graph.

Notice that the above efficient frontier doesn’t appear quite right. First, most obviously, the portion below the variance-minimizing return is inapplicable – I’ve left it to better illustrate the parabola. Near the variance-minimizing point, the frontier fits very nicely. But once the return increases beyond a certain level, the frontier departs from the set of possible portfolio pairs. What gives? The answer is that the parabola is unconstrained by the weights summing to zero. After all, a parabola exists at the entire domain, not just the ones that are feasible for a portfolio. The implication is that the blue curve that extends beyond the possible set includes negative weights for one or more of the assets. What to do?

As we deduced earlier, each pair corresponds to a parabola. So, we just need to find the other parabolas on the frontier. The parabola that we found above includes the covariance matrix of all three assets, even when their weights are negative. The remaining possible parabolas include the covariance matrices of each pair of assets, exhausting the non-singular asset portfolios. The result is a total of four parabolas, pictured below.

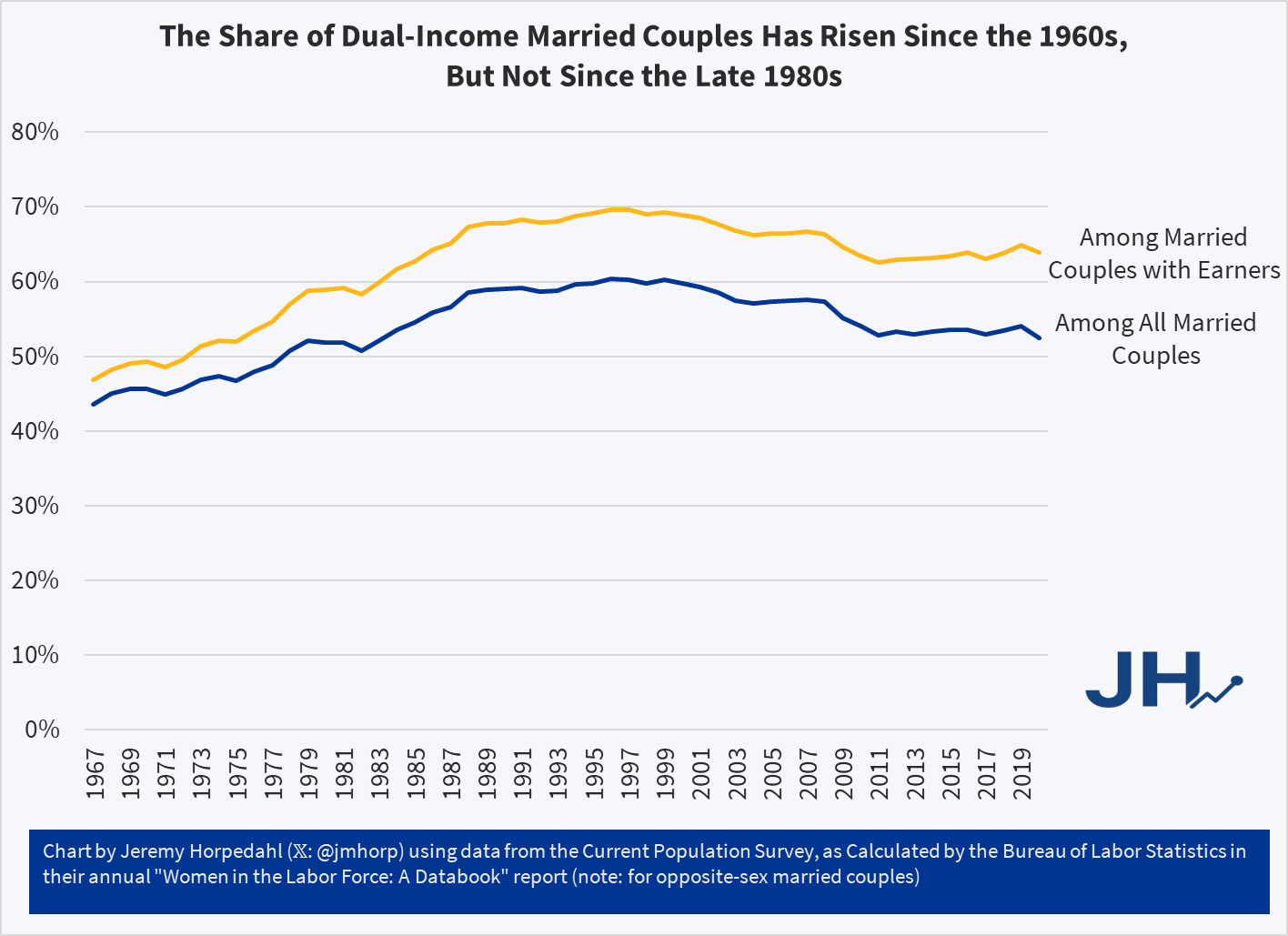

In addition to questions about inflation adjustments and general disbelief, one of the more common questions about this data is how much of it is driven by rising dual-income families, where both the husband and wife work (for purposes of this post, I will look only at opposite-sex couples, since going back to the 1960s this is the only way we can really make consistent comparisons).

In short: most of the growth of high-income families can not be explained by the rise of dual-income families. The basic reason is that the growth in dual-income families had mostly already occurred by the 1980s or 1990s (depending on the measure). So the tremendous growth since about 1990, when just about 15 percent of families were above $150,000 (in 2024 dollars), is better explained by rising prosperity, not a trick of more earners.

You can see this in a number of ways. First, here is the share of married couples where both spouses are working. I have presented the data including all married couples (blue line), as well as only married couples with some earners (gold line), since the aging of the population is biasing the blue-line downwards over time.

All of us have assets. Together, they experience some average rate of return and the value of our assets changes over time. Maybe you have an idea of what assets you want to hold. But how much of your portfolio should be composed of each? As a matter of finance, we know that not only do the asset returns and volatilities differ, but that diversification can allow us to choose from a menu of risk & reward combinations. This post exemplifies the point.

1) Describe the Assets

I analyze 3 stocks from August 1, 2024 through August 1, 2025: SCHG (Schwab Growth ETF), XLU (Utility ETF), and BRK.B (Berkshire Hathaway). Over this period, each asset has an average return, a variance, and co-variances of daily returns. The returns can be listed in their own matrix. The covariances are in a matrix with the variances on the diagonal.

The return of the portfolio that is composed of these three stocks is merely the weighted average of the returns. In particular, each return is weighted by the proportion of value that it initially composes in the portfolio. Since daily returns are somewhat correlated, the variance of the daily portfolio returns is not merely equal to the average weighted variances. Stock prices sometimes increase and decrease together, rather than independently.

Since the covariance matrix of returns and the covariance matrix are given, it’s just our job to determine the optimal weights. What does “optimal” mean? This is where financiers fall back onto the language of risk appetite. That’s hard to express in a vacuum. It’s easier, however, if we have a menu of options. Humans are pretty bad at identifying objective details about things. But we are really good at identifying differences between things. So, if we can create a menu of risk-reward combinations, then we’re better able to see how much a bit of reward costs us.

2) Create the Menu

In our simple example of three assets, we have three weights to determine. The weights must sum to one and we’ll limit ourselves to 1% increments. It turns out that this is a finite list. If our portfolio includes 0% SCHG, then the remaining two weights sum to 100%. There are 101 possible pairs that achieve that: (0%, 100%), (1%,99%), (2%,98%), etc. Then, we can increase the weight on SCHG to 1% for which there are 100 possible pairs of the remaining weights: (0%,99%), (1%, 98%), (2%, 97%), etc. We can iterate this process until the SCHG weight reaches 100%. The total number of weight combinations is 5,151. That means that there are 5,151 different possible portfolio returns and variances. The below figure plots each resulting variance-return pair in red.

In September we covered the release of the Fraser Institute’s 2025 Economic Freedom of the World report. I said then:

The authors are doing great work and releasing it for free, so no complaints, but two additional things I’d like to see from them are a graphic showing which countries had the biggest changes in economic freedom since last year, and links to the underlying program used to create the above graphs so that readers could hover over each dot to identify the country

Well, now Matthew Mitchell of the Fraser Institute has done that:

I can only post a screenshot of a scatterplot here, but if you click through to the Fraser report you can hover over any dot to see which country it represents:

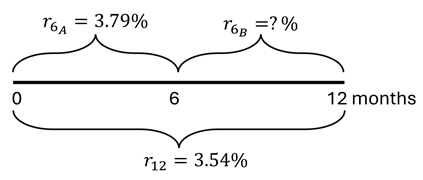

Jerome Powell’s term as Fed Chair ends in late May 2026. President Trump has said that he will nominate a new chair and the US senate will confirm them. It may take multiple nominations, but that’s the process. The new chair doesn’t govern monetary and interest rate policy all by their lonesome, however. They have to get most of the FOMC on board in order to make interest rate decisions. We all know that the president wants lower interest rates and there is uncertainty about the political independence of the next chair. What will actually happen once Jerome is out and his replacement is in?

The treasury markets can give us a hint. The yields on government debt tend to follow the federal funds rate closely (see below). So, we can use some simple logic to forecast the currently expected rates during the new Fed Chair’s first several months.

Here’s the logic. As of October 16, the yield on the 6-month treasury was 3.79% and the yield on the 1-year treasury was 3.54%. If the market expectations are accurate, then holding the 1-year treasury to maturity should yield the same as the 6-month treasury purchased today and then another one purchased six months from now. The below diagram and equation provide the intuition and math.

Since the federal funds rate and US treasury yields closely track one another, we can deduce that the interest rates are expected to fall after 6 months. Specifically, rates will fall by the difference in the 6-month rates, or about 49.9 basis points (0.499%). This cut is an expected value of course. Given that the cut is between a half and a zero percent, we can back out the market expectation of for a 0.5% vs 0.0% cut where α is the probability of the half-point cut.* Formally:

One of the likely effects of the federal government shutdown is that recipients of SNAP benefits (what used to be officially called “food stamps,” a term still used by the general public, especially those that dislike the program) may lose their benefits next month. This would obviously be a hardship for those that depend on this program, but it has also led to bad claims being made about the program, from both supporters and opponents of the program.

Let’s start from the political right: Matt Walsh makes the claim that by subsidizing food consumption “obviously drives up the cost” of groceries.

The number one thing that artificially inflates the price of groceries is the food stamp program. The federal government is subsidizing groceries for 40 million people which obviously drives up the cost. That's why the increase in the cost of groceries tracks exactly with the…

As with all bad claims, there is a nugget of truth baked into them. If the government subsidizes anything, we would expect demand to increase, and thus unless supply is perfectly elastic, there will be some effect on prices. However, we need to think more carefully about the nature of the subsidy.

The way SNAP works is that beneficiaries receive an electronic voucher to spend at the grocery store, which is about $300 per month on average for a household. That $300 must be spent on groceries. However, if that household had already planned to spend $300 or more on groceries, it is unlikely they will spend all of the additional $300 on food. In the limit, it’s entirely possible they will spend no additional money on groceries, merely reducing their out-of-pocket spending on groceries by $300. They will then effectively have $300 more to spend on other goods. More likely is that they will spend some of the additional $300 on groceries, and some of it on other goods.

Many studies have tried to look at the extent to which SNAP benefits affect household spending, but these were mostly observational studies. There was no treatment and control group. But a 2009 paper titled “Consumption Responses to In-Kind Transfers: Evidence from the Introduction of the Food Stamp Program” has a better approach to studying the question. Since the original Food Stamp program was slowly rolled out across the country over more than a decade, you can compare counties that entered the program first to counties that entered it later. By doing so, Hilary Hoynes and Diane Schanzenbach find out some first interesting things about the causal effects of SNAP benefits.

For the claim by Walsh in his Tweet, the most relevant result from the paper is that food stamps impact household spending similarly to a cash transfer. Yes, the program increases household spending on groceries, but it also increases spending on other goods and services. And it does so almost identically to how cash transfers impact household spending. In other words, while pitching the program as assistance for buying groceries may make it more politically palatable, SNAP benefits are no different from a similarly-sized cash transfer for the average recipient. If they do cause any inflation, they do so in the same way as a cash transfer would, and thus there is no specific impact on food inflation.

A second bad claim about SNAP comes from the political left, in this case Minnesota Governor Tim Walz:

Talk to some economists and they’ll tell you that exchange rates aren’t economically important. They say that exchange rates between countries are a reflection of supply and demand for one another’s stuff. So, at the macro, it’s a result and not a determinant of transnational economic activity.

For individual firms at the micro level, it’s the opposite. They don’t affect the exchange rate by their lonesome and are instead affected by it. If you have operations in a foreign country, then sudden changes to the exchange rate can cause your costs to be much higher or lower than you had anticipated. The same is true when you sell in a foreign country, but for revenues. This type of risk is called ‘exchange rate risk’ since it’s possible that none of the prices in either country changed and yet your investment returns change merely because of an appreciated currency.

Supply & Demand

Exchange rates are determined by supply and demand for currencies. Demand is driven by what people can do with a currency. If a country’s goods become more attractive, then demand for those goods rise and demand for the currency rises. After all, most retailers and wholesalers in the US require that you pay using US dollars. Importantly, it’s not just manufacturing goods that drive demand for currency. Demand for services, real estate, and financial assets can also affect the supply and demand for currency. In fact, many foreigners are specifically interested in stocks, bonds, US treasuries, and other investments. The more attractive all of those things are, the more demand there is for them.

Of course, the market for currency also includes suppliers. Who does that? Answer: Anyone who holds dollars and might buy something. Indeed, all buyers of goods or financial products are suppliers of their medium of exchange. In the US, we pay in dollars. Especially since 1972, suppliers have also included other central banks and governments. They treat the US currency as if it’s a reserve of value, such as gold, that can be depended upon if they need a valuable asset (hence the name, “Federal Reserve”). This is where the term ‘reserve currency’ comes from – not from the dollar-denominated prices of some internationally traded commodities. Though, that’s come to be an adopted meaning.

Another major supplier of currency is the US central bank. It has the advantage of being able to print US dollars. But it doesn’t have an exchange rate policy. So, it’s not targeting a particular price of the US dollar versus any other currency. The Fed does engage in some international reserve lending, but it’s not for the purpose of supplying currency to foreign exchange markets.

The US Exchange Rate in 2025

One of the reasons that the US has such popular financial assets is that we have highly developed financial markets and the rule of law. People trust that, regardless of the individual performance of an asset, the rules of the game are mostly known and evenly applied. For example, we have a process to follow when bond issuers default. So, our popularity is not merely because our assets have higher returns. Rather, US investment returns have dependably avoided political risk – relative to other countries anyway.

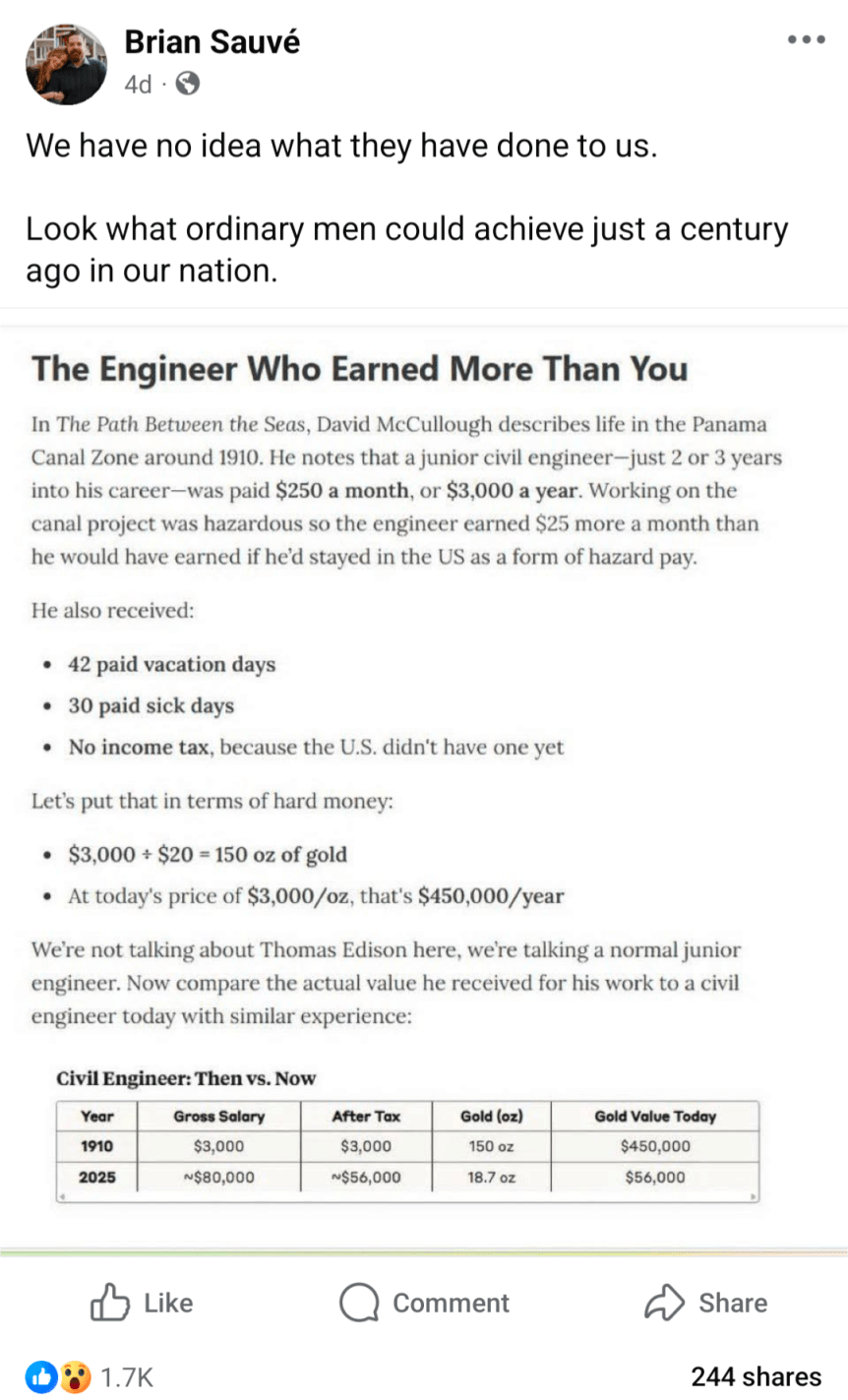

Inflation adjusting income and prices from the past is a common theme in my blog posts, including fact checking of other attempts to do these adjustments. But here is a really novel one, in a viral post from Facebook (which comes from this essay), which claims that a civil engineer earned the equivalent of $450,000 in today’s terms:

Can this be correct? If so, it would represent massive stagnation in incomes over time. Thankfully, there are two major errors, or at least misleading aspects to the calculation.

The listed salary was not one of an “ordinary man” — far from it.

Using gold prices to inflation adjust the incomes is very misleading.

First, the salary: $3,000 per year was definitely not what ordinary men earned. The average wage, for example, for a production worker in manufacturing was 18 cents per hour. You would need to work almost 17,000 hours to earn $3,000 at that wage, which of course is not possible. In reality, the average worker put in 57 hours per week — which means they earned about $500 if they were able to work 50 weeks per year (most probably didn’t). So already we see that the civil engineer working on the Panama Canal is making about 6 times as much as an “ordinary man.” Agricultural workers, the other main industry of 1910, earned about $28 per month ($22 if they also received board) — even less than manufacturing, and only about 1/10 of the engineer

Second, the gold price adjustment is misleading. Yes, in 1910, gold was how we defined currency in the US. But you can’t eat gold, and most people only keep a little gold on hand that can be described as providing services for them (such as jewelry). What people really wanted were real goods and services, and mostly goods. Around 1910, the average American household spent about 40% of their income on food, 23% on housing, and 15% on clothing. Comparing standards of living over time requires us to look at what people spend their money on, not what the currency is denominated in. And that’s what a good consumer price index does: it compares the prices of all consumer spending at different points in time, not just one thing like gold, allowing us to make rough comparisons of income over time.

Using the Measuring Worth historical CPI (which extends the BLS CPI back before 1913), we see that the index was 9.21 in 1910, and it stands at 323.364 in August 2025. So the 18-cent manufacturing wage from 1910 is roughly equivalent to $6.32 in current dollars. The average manufacturing wage today? Around $29. And of course, workers today have a whole range of fringe benefits, worth roughly another $13.58 for private sector workers. This means that an “ordinary man” today working in manufacturing can buy 5-7 times as many real goods and services as his 1910 counterpart for each hour he works. And the work is, of course, much safer today: BLS reports 23,000 industrial deaths in 1913 (61 deaths per 100,000 workers), but only 391 manufacturing deaths in 2023 (0.003 deaths per 100,000 workers).

But what about that extraordinary man in 1910, the civil engineer? How was he doing compared with today? Using the same historical CPI, we can see that $3,000 in 1910 is roughly equivalent to $105,000 today. Not bad! That’s almost exactly the median pay for civil engineers today. But keep in mind the civil engineer working in Panama was an unusually highly paid position. A 1913 report from the American Society of Civil Engineers suggests that most early career civil engineers were making closer to $1,500 per year — half of the Panama engineer. Engineers were also a highly skilled, very rare profession in 1910. And don’t forget that about 10% of the American workers on the Canal died in the construction, mostly from disease so the engineers were probably just as susceptible to death as the laborers.

Finally, we might ask a different question: what if you had held onto gold since 1910? Let’s say your great-great grandfather was a civil engineer, and managed over the course of a few years to save one year’s salary in gold. He even managed to hide it during the 1930s-1970s, when private holding of gold was generally illegal in the US.

How much would that 150 ounces of gold be worth today? That answer is simple: about $615,000 today (gold has gone up a bit just since that calculation was done in May!). But was that a good investment? Not really. A $3,000 investment in the stock market from 1910 to 2024 would be worth about… $120 million (it’s actually a bit more than that, since the market continued to rise after January 2024). Of course, that would have required a bit of active management, since index funds don’t come along until much later. But your great-great grandfather would have been much wiser to set up a trust for you and have it actively managed to approximate the entire US stock market, rather than to bury 150 ounces of gold in his backyard.

Even assuming you lost half the value to management fees, the stock portfolio today would be worth at least 100 times as much as the gold.