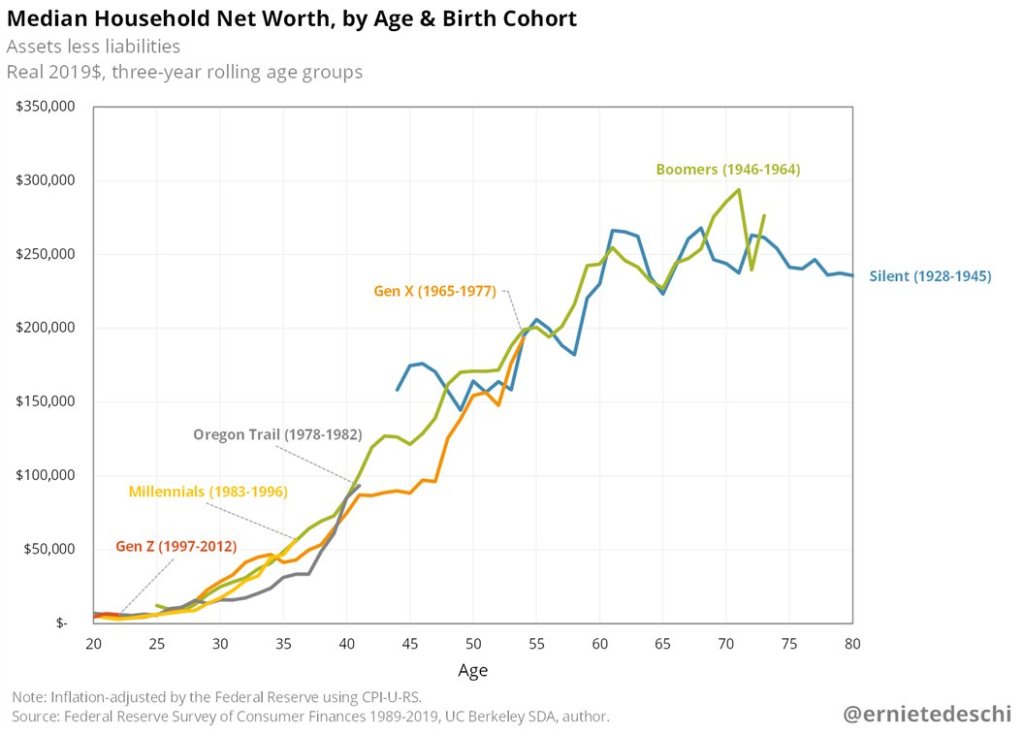

How do young people fare when it comes to household wealth? The recently released Survey of Consumer Finances from the Federal Reserve provides some insights. One major takeaway: the much-maligned Millennials are doing pretty good! Ernie Tedeschi created this informative chart on Twitter:

Looking at household net worth at roughly the same age, Millennials today have roughly the same household wealth as Boomers did in the past. And both of these generations beat the generation between them, Gen X, as well as the “microgeneration” creatively labeled Oregon Trail.

And it’s something of a running joke on Twitter, but I must add: Yes! It’s adjusted for inflation!

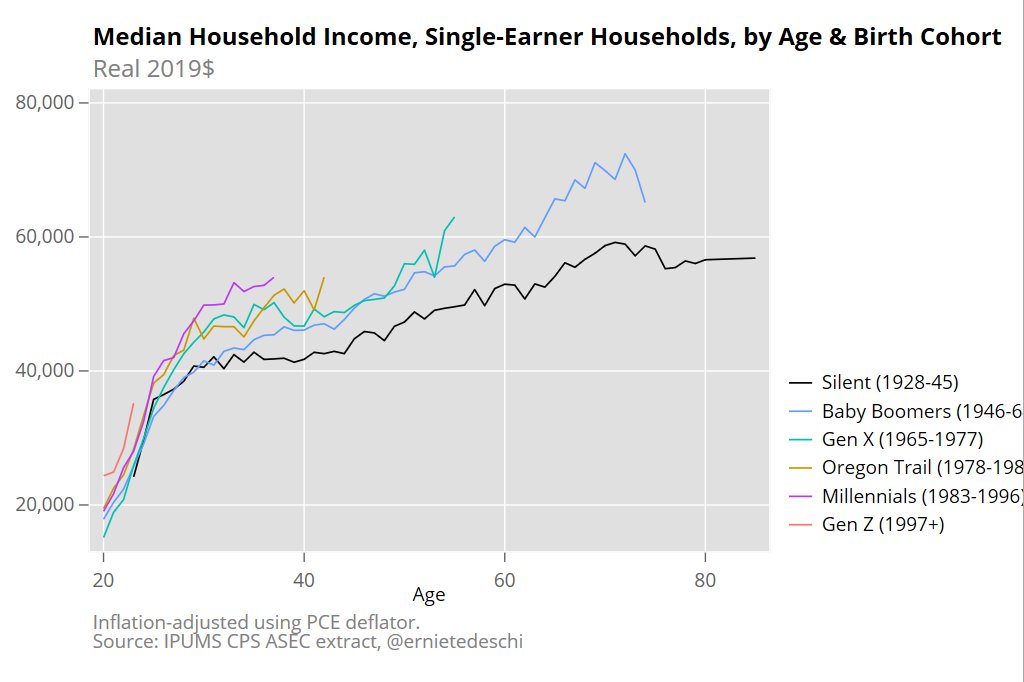

Part of this may be driven by the increase in dual-income households. Certainly that matters. While wealth data by number of earners is harder to track down, income data is more readily available. What if we look at single-income households? Millennials are still in the lead! (Once again, the chart comes from Ernie Tedeschi.)

And before you ask: Yes! It’s adjusted for inflation!

None of this means that Millennials don’t face challenges, including financial ones. This data is current through 2019, so 2020 will almost certainly make these numbers look worse, for a time. But all things considered and anecdotes aside, the kids today seem to be as well or better than past generations.

When contentious cultural and political issue arise in the USA, foreign intellectual elites invariably align themselves along partisan lines that try to mimick those of the cultural center of the world, the USA. The incomplete, and often contradictory overlap between foreign social reality, and that of the USA never fails to offer interesting paradoxes.

The intelectual battles, fought on foreign intellectual soil, are part of what I will call the proxy culture wars. The resulting paradoxes tend to stiffle local debate on local issues (I will use local as in local to a foreigner, i.e. not in the USA) by locking the participants into paradoxical positions. While the situation is amusing it causes real problems when trying to reach consensus on local solutions to local problems, communicating across the local partisan divide, or even thinking clearly about local issues.

For example, with the nomination of Amy Coney Barrett to the Supreme Court of the USA, legal twitter in Latin America has exploded in support or condemnation of her nomination. Those on the local/foreign right express their admiration for originalist interpretations, while those on the left local/foreign begin reciting Dworkin and praise interpretations of a living constitution. The ensuing battle would be relatively harmless if commentary on the goings-on in the USA was all that was at stake. But this is seldom the case as the parties bring out full battle regalia and engage in terms of the underlying merits of these positions as if they were general positions, applicable to local reality. In the fog of war, the local conditions and the contentious issues in the USA get mixed together.

The paradox arises when the debate turns local. For example consider Ecuador, where the constitution adopted in 2008 largely reflected the policy preferences of the self described twenty first century socialist president Rafael Correa (local left, now conviceted for corruption to 8 years of prison). Do those on the local right really admire originalism as a judicial doctrine? Do those on the Ecuadorean right really wish local judges would faithfully apply our constitution with its 99 constitutionally protected rights? Mind you, these rights include a right to universal access to information and communication technologies (Art. 16), recreation, the practice of sports and free time (Art. 24), and permanent and secure access to heathy and nutricious food, preferibly produced locally and in correspondence to the diverse identities and cultural traditions (Art. 13). Interesting side note: as documented by the Comptarative Constitutions Project, Ecuador ranks #1 in number of codified constitutional rights. But the nature of these rights and the problems they bring about are topics for future posts.

Does democracy require codified constitutional rights? Evidence from Latin America.

The most democratic countries in Latin America have few codified constitutional rights.

And the least democratic countries in Latin America have many codified constitutional rights. pic.twitter.com/fw2GZWusfV

Are those on the Ecuadorean left, oponents of originalism and supporters of a living constitution really arguing for a more expansive interpretations of these rights? For example when the fiscal reality of the Ecuadorean government makes it impossible for the government to guarantee one of the 99 rights codified in the constitution, do those on the left argue for an expansive interpretation? Do they really want an expansive interpretation so that the government is let off the hook when it fails to provide access to smart phone technology for all Ecuadoreans, because of unsustainable fiscal position?

Of course what is really going on is a great example of motivated reasoning. Conclusions are arrived at, and arguments follow to support those conclusions. The paradox arises as the arguments that support “things I would like in the USA” do not necesarily map well to “things I would like at home”. The lack of coherence between local reality and comentary on the affairs of the USA leads to paradoxical positions that muddy local debate, and lead to incoherence and sloppy thinking.

People have a lot of opinions about diet. For many, dietary opinion is individual – they don’t prescribe that anyone else adopt their beliefs and practices. Others have a more universal bent. Some people are dead-set against starches and others think that meat is taboo – for themselves and others. There are a lot of beliefs about diet.

The reasoning that people use for their dietary beliefs are just as diverse. Motivations range from religious beliefs, moral systems, social signaling, personal experimentation, anecdotal evidence, and so on.

Some people use the theory of evolution. They reason that we have canine teeth, like carnivores, so our ancestors had advantages in meat-eating. Others reason that we have relatively long small intestines, like herbivores, so our ancestors had advantages in plant-eating. Expert scientists from any one of a plethora of subjects are interviewed or write as authorities on the matter.

The problem, of course, is that using words like ‘meant’ or ‘designed’ implies one who ‘means’ or one who ‘designs’. For most religious people, there is no conflict. For an atheist, it’s strange turn of phrase. Why? Because evolution has two parts: 1) mutations that introduce variety and 2) natural selection. The former occurs prior to an animal’s birth. The latter occurs as a result of environmental reproductive pressure and opportunity.

In other words, to an atheist, there is no designer. So, what gives? I’ve settled on several plausible good-intentioned explanations that I order by increasing charity.

Poor Evolutionary Understanding: The atheist scientist’s understanding of evolution is flawed. Maybe their theory includes first-person or third-person intentionality. An example would be that giraffes stretched and intended that their necks would become longer over the generations. An alternative poor belief is that environmental pressures, including predators and vegetation, intended that giraffe necks would lengthen. Environmental pressures achieved their goal through reward of the long-necked and the punishment of the short-necked. I like to think that scientists have a better handle on their area of expertise rather than having beliefs such these.

Poor Grasp of English: The atheist scientist has a perfect grasp of evolution, but they are unpracticed at English in contexts of emergent order. Economists often have similar challenges and often refer to speaking allegorically as a crutch. Economists will say that prices ‘want’ to change or that a government desires social outcomes. Neither of which is true. Suppliers lower prices as their sales become lackluster. Policy outcomes are desired by someone within a governing process – though the social outcomes may be desirable by nobody. Similarly, predators desire to eat and unknowingly exert selective pressure for genetic traits. Or, a drought causes smaller lizards to survive and larger ones to dehydrate and die. English speakers have difficulty discussing biological processes without intention-denoting verbiage.

Implicit Theism: The atheist is really no atheist at all, but has belief in God that they cannot shake, despite their professions and logic otherwise. Using the past perfect tense in regard to the design of humans is case of parapraxis – a Freudian slip.

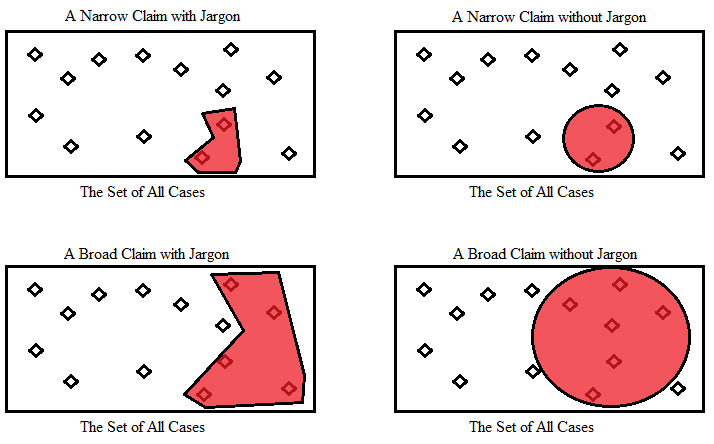

An Expertise Gap: Specialists in arts and sciences utilize highly specific jargon so that very specific concepts can be expressed concisely. But such jargon muddies communication with those who aren’t specialists in the field. The specialist grapples with this expertise gap. Although the struggle deserves sympathy, anthropomorphizing is far different from the expert’s idea of the truth.

The problem is that jargon has highly a specific meaning. So, when a specialist makes a claim with jargon, the claim is also specific. A narrower set of applicability has less room for credible challenges at the margins of a claim and ideas can be clearly communicated precisely – though, the applicable cases may not be interesting. As the breadth of a claim increases, jargon can help to ensure that the breadth is limited to appropriately specific cases.

When the listener is not an expert, the scientist is uncertain of the gap in knowledge. They attempt to make relatively broad and interesting claims, but without the aid of their case-narrowing jargon. The result is that the expert says something which is clearly false to another specialist, but may be mostly true – or true enough for the listener.

Again, these four interpretations of misspeaking and miscommunicating experts are ordered by charity. I especially sympathize with the last interpretation. Imagine trying to teach a student that inflation is always costly, but sometimes more beneficial than costly. And that the costs still exist when the benefits outweigh the costs. So, should we have a policy of inflation? The true answer is highly specific.

Does an atheist scientist understand that there is no designer of human bodies – much less one that had diet in mind? Very much. Does the same atheist scientist know how to communicate unintentional biological advantages to the non-specialist? They do not. What’s more is that they are not alone. Specialization introduces a knowledge gap and the unavailability of common jargon prevents adequately finessed broad claims.

Political polarization has been rising in the United States in recent years. There are two key reasons contributing to the polarization. First, we naturally hold different beliefs over objective matters. Furthermore, we trust different news sources. According to the 2020 Pew Research Survey around 75% conservative Republicans say they trust the information from Fox News, while 77% liberal Democrats say they distrust it.

Media outlets and politicians on the right and left sent divergent messages about the severity of the crisis during Coronavirus pandemic. A joint study by economists from NYU, Stanford and Harvard university find evidence for partisan differences in social distancing (Allcott et al. 2020). They combined a survey study with GPS location data, where GPS data record daily and weekly visits to the points of interest (POIs). The GPS data shows the strong partisan differences in social distancing behavior that emerged with the rise of COVID. The analysis carefully controlled for local policy, health, weather, and economic variables, the result remains statistically and economically significant. They also used a nationally representative survey to measure the individual behavior and belief differences about social distancing. Demographics, beliefs regarding the efficacy of social distancing, self-reported distancing, and predictions about future COVID cases. They find compare to Republicans, Democrats believe the pandemic is more severe and report a greater reduction in contact with others.

Reference:

Allcott, Hunt, Levi Boxell, Jacob Conway, Matthew Gentzkow, Michael Thaler, and David Y. Yang. “Polarization and public health: Partisan differences in social distancing during the Coronavirus pandemic.” NBER Working Paper (2020).

In my undergraduate training, I never came across the term “co-production” but after learning about it a few years back, I find I return to the concept frequently. Co-production is the idea that a consumer’s input is important to production. The term was coined by Nobel Laureate Elinor Ostrom. Examples include:

Police protection – We lock our doors, buy security systems, and engage in neighborhood watch groups.

Fire protection – We buy appliances with improved safety features and have fire extinguishers in our homes.

Education – Parents involve themselves in the education of their children through practice, ensuring the child does their homework and gets plenty of sleep.

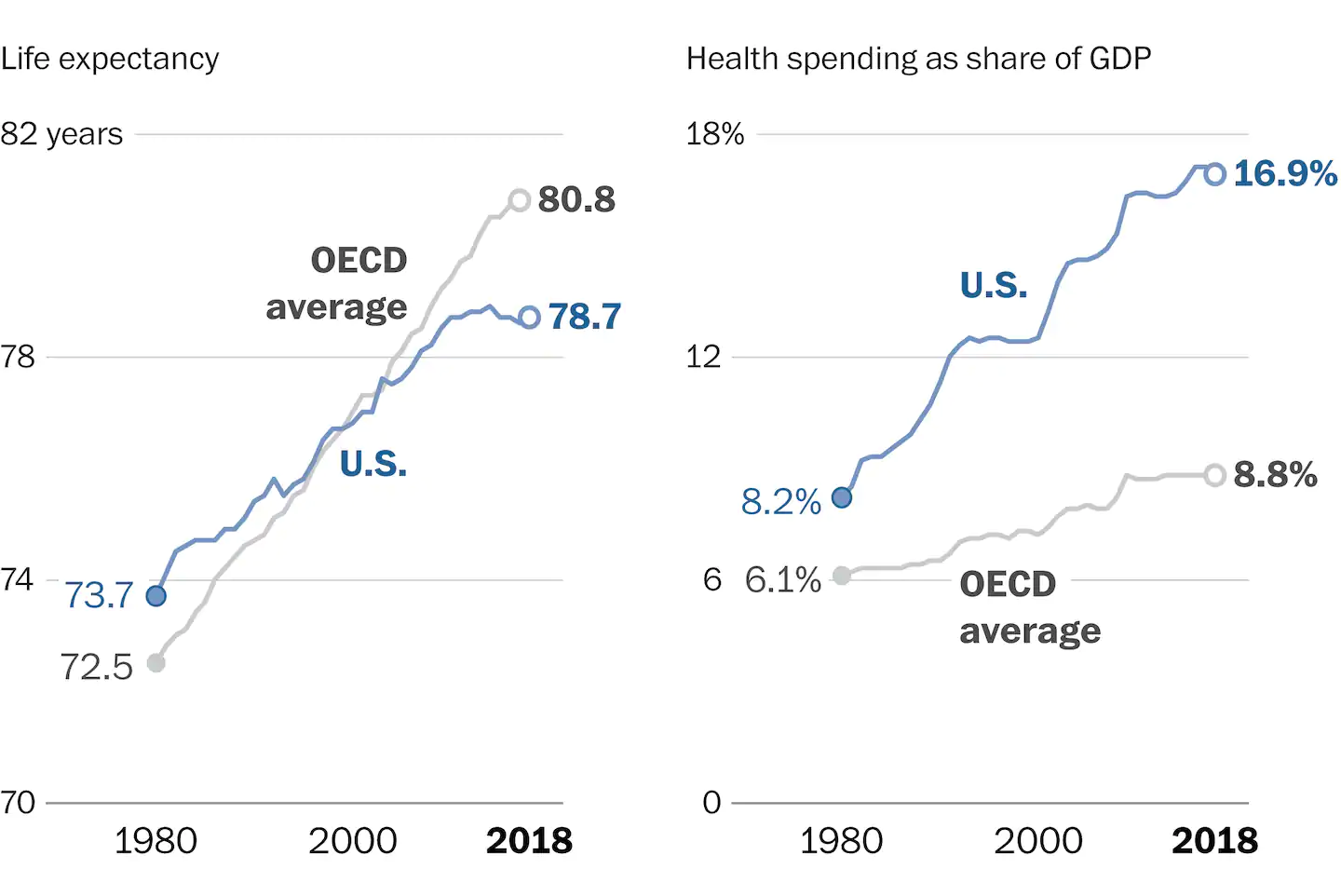

Once you start to think about co-production, you see it everywhere. For example, I am currently teaching health economics and it is not uncommon to come across graphs like this (see below) from The Washington Post. Some suggest these differences highlight how the U.S. needs a less market-oriented health system. But, when I see the graph, I think of all the ways in which the United States is different. Specifically, I question the extent to which we are good co-producers of our health.

In the United States, 36 percent of adults were considered obese in 2016. The most among OECD countries. You can present similar data on drug use disorders, alcoholism, mental health disease burden, and so forth. I do not mean to suggest we have equal control over all of these outcomes but we are often not powerless.

The debate about government v. market provision of health services is a discussion for another time and sure to feature in the upcoming presidential debates. But, I do think any intervention in the health sector that does not address co-production will oversell and underdeliver.

Preheat the oven to 440-450°F (230 °C). Position a rack on a lower-middle shelf. The top of the fully risen popovers should be about midway up the oven. You don’t want the tops of the popping popovers to be too close to the top of the oven, as they might burn.

Use 12 cup nonstick popover pan, e.g. Chicago Metallic. Lightly grease the cups (may not be necessary every time). It is possible to use a standard, i.e. non-popover 12-cup metal muffin tin, one whose cups are close to 2 1/2″ wide x 1 1/2″ deep, though results may not be quite as good unless you preheat the muffin tin in the over for five minutes. As noted above, reduce recipe size for 6-cup popover pan (where each cup is somewhat larger than with the 12-cup popover pans).

Use a wire whisk or beater on low speed to beat together the eggs, milk, and salt. Whisk till the egg and milk are well combined, with no streaks of yolk showing.

Add the flour all at once, and beat till frothy; there shouldn’t be any large lumps in the batter, but smaller lumps are OK.

Stir in the melted butter, combining quickly. Best to let batter then rest at least 10 minutes, e.g. while oven preheats.

Pour the batter into the popover cups, evenly; about 2/3 full. [For 12 standard muffin cups: fill them about 2/3 to 3/4 full. ]

Make absolutely certain your oven is heated, 440- 450°F.

Bake the popovers for 19-20 minutes without opening the oven door. Reduce the heat to 360 °F [180 °C] (again without opening the door), and bake for an additional 15-20 minutes, until they’re a deep, golden brown. [If using muffin tins, for second phase cook only 10-15 min at 350 F]. Preferable: pierce them about 2 minutes before removing from oven to release steam.

If the popovers seem to be browning too quickly, reduce temperature a little.

NOTES ON MAKING POPOVERS:

( A ) These are fairly healthy and easy to make, and taste delicious split open and served warm, with butter and jelly, for dessert or snack. Can also serve with things like chili or stew. Get creative and fill with pudding or whipped cream and fruit. Popovers taste almost like pastry, but without all the fat. The larger popovers from the 6-cup pans look more dramatic, and have big cavity inside them, especially when made with all white flour.

( B ) These are best cooked in special popover pans. These have typically six or twelve metal cups, joined by fairly thin metal rods, so heat can get quickly to the cups. It is possible to cook popovers in regular muffin tins.

( C ) The oven needs to be hot, and the oven door kept closed to keep moisture in, in order for the popovers to rise. They rise because steam gets trapped in sticky eggy dough.

( D ) You can make these with all white flour. Use a full 1.5 c white flour. (I cut back a little with the amount of whole wheat flour, since it absorbs more liquid than white flour). Using all white flour tends to make the popovers rise more, with thinner, drier walls. I like them a little thicker and chewier, hence the whole wheat.

( E ) Popovers are best when eaten within an hour or two of cooking. With time, the crispness of the outer wall gets softened by moisture from the inside. They can be re-crisped by heating in an oven or electric skillet or large covered frying pan at say 350 F for ten minutes or so. They can also be frozen, then gently thawed in microwave and then re-crisped.

( 2 ) TRADITIONAL IRISH SODA BREAD (NO YEAST)

INGREDIENTS

4 cups (580g) all-purpose flour

1½ teaspoons baking soda

1 teaspoon salt

Scant 2 cups (470ml) cold buttermilk

INSTRUCTIONS

( 1) If you don’t have buttermilk, first make it by adding 3.5 T vinegar or fresh lemon juice to measuring cup, and filling to two cups with whole or 2% milk (i.e. a scant 2 T vinegar per cup of milk). Stir and let sit for at least ten minutes for milk to sour. I used apple cider vinegar for a faint fruity aura.

(2) Preheat oven to 425 degrees F (218 degrees C) , or slightly hotter if your oven runs cool. Line a baking sheet with parchment paper or grease well; set aside. You can also use an 8″ cake pan or oven proof skillet.

(3) In a large bowl whisk together the flour, baking soda, and salt. Stir in the buttermilk just until combined and the dough starts to become too stiff to stir. Transfer to work surface and with floured hands lightly knead the dough 5-10 times or until all the flour is moistened and the dough comes together.

(4) Form dough into a 1 ½” (4 cm) high round, approximately 8” (20 cm) diameter. Place on prepared pan. With a serrated or very sharp knife cut a deep cross on the top from side to side, cutting about a third of the way deep into the dough. Bake for 30-35 minutes or until golden brown and it sounds hollow when tapped on the bottom. Alternatively, bake at 425-440 F for 20 min, then turn down to 400 F for last 15 or so minutes.

RECIPE NOTES FOR SODA BREAD

( A ) Note the dough for soda bread is NOT kneaded to the point of being smooth, but just enough to barely hold together, still looking “shaggy”. The reason is that with the baking soda, all the CO2 is released in a relatively short time as the dough heats up, so the dough has to be soft (not tough and cohesive) so it can quickly stretch. (This is the opposite from yeast bread, where you knead the dough long and hard to build gluten chains to strengthen the dough, so the CO2 produced slowly from the yeast during rising will not escape.)

( B ) The deep cross cut in the dough helps it expand, and helps heat to get to the center of the loaf.

( C ) This is authentic, basic Irish soda bread. The crust comes out pretty hard. It is great for dipping in stew or soup, or just spread with butter while warm and chew carefully. I like to have the crust a bit softer, so I brush the loaf with buttermilk or butter just before baking. When cooling the loaf, cooking on rack will make crust crispy, while being covered with tea towel will soften the crust.

( D ) As with most real bread, this goes stale very fast. I suggest cutting off whatever portion you will not eat that day, and freezing it. It is fine thawed. Bread that is not too stale can be partly, temporarily resuscitated by wetting the crust, and baking it for say 12 minutes at 350 F.

This is a slightly more complex recipe for Irish soda bread, including butter, egg, a little sugar, and currants or raisins. Gives softer, sweeter version, verging on scone, instead of plain soda bread with tough crust. Has nice short confidence-building video showing how to work the dough. And has good photos of what dough should look like at each stage.

I live in Florida and there is a lot of residential construction down here. It’s not typically people just deciding to build a house on some isolated plot of land. A large portion of construction is private or semi-private neighborhoods built by developers. They often include manicured common spaces and strict Home Owners Association (HOA) rules.

The typical procedure is that a developer purchases a large parcel of land, and then starts building. Before the first house is even sold, the HOA is established and the governing board is packed with developer representatives. Written into the HOA bylaws is that the developer maintains a preponderance of the HOA representation during construction. This makes sense. ‘Nice’ neighborhoods command higher property prices and the developer has often invested *very* large sums of money. Certainly more money than it’s willing to risk at the hands of a sloppy, owner-controlled HOA.

Best practice differs by developer.

Typically, the residents will have seats on the HOA board in some proportion of development project completeness. For example, if 75% of the total planned lots have been built and sold, then the developer may retain 2/3 or 3/5 control of an HOA board. The developer finally relinquishes all HOA control after 100% of the planned units are completed and sold.

Ignoring policies for beautification and such, a HOA boards under developer control act differently from those that are resident controlled. As I said, the developer has full discretion on HOA policy, practically speaking, because it maintains a majority of the voting members. But, HOA fees are *not paid* by the developer.[1] Only homeowners pay HOA fees.

For example: Not everyone wants cable TV. But the developer knows that home-buyers want the option for cable TV. Typically, one of the first HOA orders of business is to pay for monthly cable TV. Every single unit pays for cable TV through their HOA fees – whether they use it or not – in exchange for the cable company laying cable lines and providing access. Typically, these contracts are often a decade in duration, after which time the contract can be cancelled and owners can individually decide whether to pay for cable. It’s not obvious that an owner-controlled HOA would pay for cable and have lines laid in the first place (Satellite TV anyone?).

To be clear: The developer sets the HOA policy priorities and determines the HOA budget. Then, the owners pay the quarterly HOA fee. Can you say Principal-Agent problem? Early HOA activities include less resident engagement because residents don’t much affect outcomes. The developer also doesn’t mind higher HOA fees because it doesn’t bear the cost. Do you expect your HOA to put contracts up for bid, say, to do landscaping, pressure washing, etc.? If your HOA is developer-controlled, then you should expect no such thing. Putting contracts ‘up for bid’ is time consuming and reflects a concern for costs. Not to mention that the quality of the bid work may be variable. Developers want high property values and they want them dependably. HOA fiscal prudence, besides solvency, is not a priority.

Having said all this – it’s true that your neighborhood may be ‘nicer’ due to developer control of the HOA. Depending on you preferences, this might align nicely with your priorities. If that’s true, however, you can expect to be less happy in the long-run when your neighbors ultimately gain control of the HOA.

I’m on my HOA board and it’s now 100% privately owned. There are still principal-agent problems. But they are much easier to address now that everyone on the board pays HOA fees. Our problems and our opportunities are truly ours.

[1] Sometimes, the developer will provide a loan to the HOA to provide for initial management costs.

When you mention you teach economics, who among us hasn’t heard someone blurt out, “Oh, I hated that class!” or sigh, “I just never ‘got it’”? There are probably many reasons for this but I suspect their teacher did not have an appreciation for the “rhetorical triangle” or Aristotle’s modes of persuasion: Logos (logic), ethos (credibility), and pathos (emotion). Economists often act like logos and ethos are enough. They are not! When we construct arguments with only the two it’s like trying to create a stable two-legged stool. Good luck, something is missing.

Economists need pathos to create an argument that is memorable and doesn’t fall apart. In this short post, I want to explore the role of beauty to make that emotional appeal.

Christian author Donald Miller writes, “Sometimes you have to watch somebody love something before you can love it yourself. It is as if they are showing you the way.” How can we show students our love for economics and the beauty of the economic way of thinking? Through discussion of what excites us. From helping students to see economics “in the wild” of everyday life to helping students see the magic of markets. All of this improves their understanding of principles and economic concepts. First, let me discuss the mundane and then we can discuss the magic.

When I was an undergraduate, every Friday night I would head to Sonny’s BBQ with some buddies. On Friday nights they had the all-you-can-eat baby back ribs. Normally, the rib re-orders came promptly and the sweet tea refills flowed. But, on one particular Friday night the service was pretty bad and we talked over empty plates and cups.

Why? It wasn’t busier than normal. They didn’t seem understaffed. Our waitress was paying attention to other tables but not our table. Why? Well, our normal group was a party of four but we invited a couple more friends that week. For six person tables, automatic gratuity kicked-in and the waitress was paying attention to tables where her gratuity could still rise or fall with the quality of service. She had us locked in at 18 percent, and being poor college students, she likely didn’t expect us to tip more than 18% if she gave good service. Economics in the wild! The power to explain the mundane.

Share your own stories with your students (or on this blog!). When is the first time you saw economics in the wild? When is the first time you realized you were an economist? For inspiration on the mundane, check out Robert Frank Economics Naturalist and his conversations with Russ Roberts on that book as well as dinner table economics.

For a transition from the mundane to the magic consider having students read, “I, Pencil” by Leonard Reed. Though the video with Uncle Milt is wonderful too. The remarkable journey of a simple pencil!

Build on those ideas either before or after you have them read “I, Pencil” or watch Milton Friedman. Hand out chocolate chip cookies to students and ask them to describe in as much detail as possible how to make a chocolate chip cookie (no, not their grandma’s recipe). Then, help them to see something so simple like a cookie required vast networks of exchange coordinated through a price system that nobody controlled. Inconceivable!

Pencils and cookies are complicated? Really!? Inconceivable!

For another great magical treatment of economics, check out Russ Roberts’ poem, “It’s a Wonderful Loaf” (accompanying video on the same site). The emergence of order from seeming chaos is profound.

We rarely feel more human than when we are on a journey. Beauty has the power to place us on that path of inquiry that awakens a desire to know more. In that search for beauty, we shouldn’t discount the mundane. I tell students there are few things more exhilarating than seeing economics in the wild. You feel like you have a decoder ring to explain the puzzles of our social world. On the other hand, I have always found the magical explanations special and profound, to be appreciated like works of art. Yes, they increase understanding but they also evoke a sense of awe. Both the mundane and magical are beautiful and economists should look to beauty more. Our arguments will be better if we do.

It is not straightforward to define what “money” is in a modern national economy. Simply tallying the amount of coins and paper currency is inadequate. Most buying and selling is now done by shifting numbers between abstract bank accounts, not by pushing a bundle of bills across a table. Thus, these bank accounts serve the functions of money (medium of exchange and store of value). The question then arises as to which of these financial accounts to regard as money.

Among financial assets, there is a broad spectrum of liquidity. Typically you can write a check on your checking account which, when it clears, provides immediate and final settlement for a purchase. On the other hand, if you want to tap your brokerage account with its holdings of Apple stock to buy a television, you would typically have to sell (liquidate) your stock. A third party would have to be willing to give you something more money-like (e.g. credit your money market fund at your brokerage) in exchange for the stock at some negotiated price. Then you might have to transfer the funds from your brokerage fund into your bank checking account before you can actually buy that TV. Because of all these intermediate steps, and the fluctuating value of the stock before you complete the sale, the stock holding would not be counted as “money”, even though its value enabled you to ultimately make your purchase.

There are a number of measures of money in modern economies. In the U.S. some of these are:

M0: The total of all physical currency (coins and paper bills).

MB (“Monetary Base”): The total of all physical currency (coins and bill) plus Federal Reserve Deposits (special deposits that only banks can have at the Fed). This is money essentially created by the government plus the Federal Reserve, which does not necessarily enter the private economy to be spent.

M1: Physical currency circulating outside of the Fed and private banking system, plus the amount of demand deposits, travelers’ checks and other checkable deposits. This is highly “liquid” money, i.e. accepted and used for transactions in the private economy.

M2: M1 + most savings accounts, money market accounts, retail money market mutual funds, and small denomination time deposits (certificates of deposit of under $100,000). The funds in these additional savings and money market accounts can in general be easily transferred to checkable accounts, and thus could go towards making purchases if desired.

MZM: “Money Zero Maturity” is one of the most popular aggregates in use by the Fed because its velocity has historically been the most accurate predictor of inflation. It is M2 – time deposits + institutional money market funds.

Below is a chart showing the growth in the U.S. in the past fifteen years of M0 (total currency, labeled “currency in circulation), MB, M1, and M2. The grayed areas are recessions, i.e. 2008-2009 and the present. [1]

Various Measures of “Money” in the U.S.

The M1 money supply (green line) was about $1.4 trillion ( $1,400 billion on the chart) in 2005, was fairly steady for several years, then started a steady ramp up to $4 trillion by January, 2020. Due to the extraordinary events associated with the Covid-19 shutdown (government stimulus package plus Fed purchases of securities), M1 jumped up to $ 5.4 trillion by August of this year. M2 followed similar trends, though on a much larger scale, rising to$18.3 trillion this year. This compares to a current U. S. total GDP of about $21 trillion.

The lowest line on the chart is the physical currency (blue line), which has grown slowly but steadily. The “Total MB” (red) line, was essentially on top of the blue line up until the 2008-2009 recession. Since MB = physical currency plus reserves, this meant that the amount of money in the reserve balances at the Fed of the private banks was nearly zero before 2008. The reserves jumped up (difference between the red and blue lines) in 2009, with the onset of massive purchases of securities by the Fed (“quantitative easing”). The Fed buys these securities from the banks, and credits their reserve accounts. The Fed has tried to taper down its holdings in recent years (red line declining 2015-2019), but suddenly purchased trillions more this spring (red line jumping up in 2020). Most pundits hold that all this Fed money injected into the financial system has been the major cause of the enormous rise in stock prices in the past decade, especially in the past six months.

[1] Chart produced on the St. Louis Fed “FRED” site, https://fred.stlouisfed.org/categories/24 . This site has a wealth of economic data. Unfortunately, it is not easy to change units, so I was stuck with “billions” instead of “trillions” for the axis labels. Also, the M0 and MB numbers were only available in “millions”, so I had to divide those numbers by 1000 to get them to fit on the plot with M1 and M2. The grayed out spots on the graph labels is where I blotted out the “ /1000 ” which the plotting software put in. It would have been cleaner, in retrospect, to have exported the data to Excel and replotted it there.

I want to share a conversation about proportion Vs. probability.

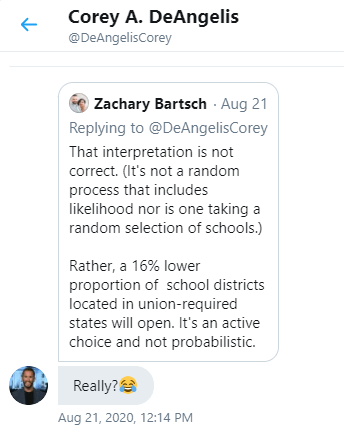

My friend, Corey DeAngelis, has a new research paper that measures the link between school district unionization and in-person re-opening in the time of Covid-19.

He promoted it on Twitter – but little did he know that a member of the statistics police was on patrol…

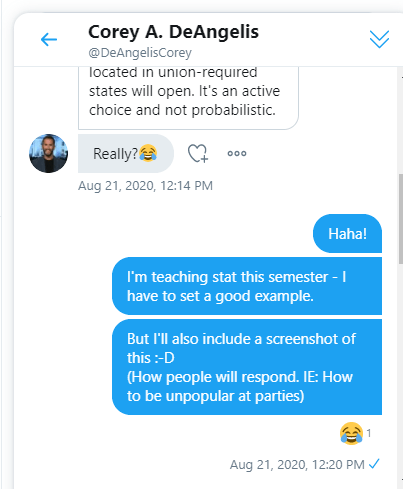

That interpretation is not correct. (It's not a random process that includes likelihood nor is one taking a random selection of schools.)

Rather, a 16% lower proportion of school districts located in union-required states will open. It's an active choice and not probabilistic.

Am I splitting hairs? Of course I am. Do most people know what he means? I think so. Is the distinction important? You betchya.

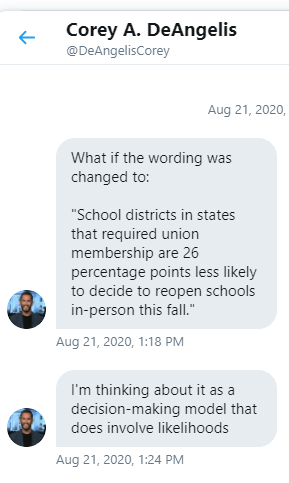

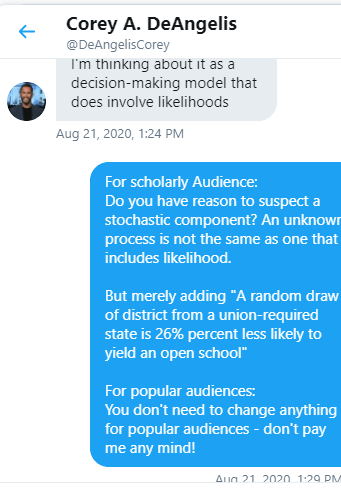

Corey, sent me a private message with the appropriate response:

Oh, yes – really. Speaking probabilistically when we don’t have all of the information is so very tempting. To us the observer, lots of things appear probabilistic to us that are deterministic in nature (Have you ever played the board game “Don’t Wake Daddy!”, “Hot Potato”, or “Musical Chairs”? There is a process that determines when daddy will awaken or when the music ends). Not knowing the underlying process makes the experience appear probabilistic. But appearances can be deceptive.

Often, people speak as if they are taking a random draw from a sample. That can be probabilistic. Given a draw of school districts, the likelihood of selecting an opening school from non-union districts is greater than choosing an opening school from a union district. This is entirely right. What is not right is saying that teacher-unionized districts are “more likely” to stay closed.

The decision to stay closed or to open is a product of collective choice – the decisions of several parties with diverse interests. Of course, we don’t know every single influence on the decision. But we do know that the outcome follows a pattern. A lower proportion of schools open in teacher-unionized districts than the proportion in non-union-districts.

Researchers often talk about their sample as if it is reality. A random draw from a sample has a probability. Nobody is randomly drawing an actual school district and expecting a probabilistic process to determine the policy outcome. Just ask yourself: “Does the sample proportion tell me an empirical probability?”

*Note: This is why we have different language when using a standard normal distribution.

“What proportion of area is to the left of z*=1.5?”

“Given a random draw from a standard normal distribution, what is the probability of selecting a value that is less than 1.5?”

One describes randomness. The other describes an already determined outcome.

Note: Yes, this kind of behavior does have implications for one’s popularity.