- Networking remains underrated, even though people talk about it. I think it’s underrated because when people do a good job with it they don’t notice that they are doing it. Whereas, you don’t, for example, teach a class and not notice that you did it.

- I’m reading Hillbilly Elegy in paperback. With the new edition in hand, what I noticed first was the pages of breathless reviews from every outlet you could ever want praise from (NYT, WSJ, Vox, Rolling Stone, etc.). How did he do it? Did “they” come to him? Did he go to them? What on earth happened? See above point #1. Halfway in, I agree with the blurb from The Atlantic that it is a “beautiful memoir.” Although I’m sorry not to be supporting independent bookstores more, my strategy these days is to buy used paperbacks through Amazon. The books themselves are nearly free and shipping still costs less than Kindle. (This is how AI can help us reduce trash – get the stuff we have already manufactured to the people who want it.)

- “Fewer students are benefiting from doing their homework: an eleven-year study” Via LinkedIn post by Ethan Mollick. Students might even learn less from homework if they use ChatGPT. Relatedly, SAT standards might be declining even if scores are not.

- Shruti Rajagopalan discusses talent in India

- “The rise of cultural Christianity” (The New Statesman) via Sam Enright

Month: August 2024

More Immigrants, More Safety

The headlines often read with the criminal threats that illegal/undocumented immigrants pose to the US native population. The story usually includes a heart wrenching and tragic story about a native minor who was harmed by an immigrant and a politician to help propose a solution. There’s also usually a number cited for how many such crimes happened in the most recent year with data. Stories like this are designed to provoke feelings – not to provoke thinkings.

First, the tragic story is probably not representative. Even if it is, the citation of a raw count of crimes is not communicative in a helpful way. Sometimes politicians will say something like “one victim of a crime by an illegal immigrant is too many”. But that seems like a silly argument to make *if* immigrants reduce the probability of being a victim of a crime.

I argue that (1) immigrants who commit crimes at a lower probability than the native population cause the native population to be safer and, counterintuitively, (2) immigrants who commit crimes at a *higher* probability than the native population cause the native population to be safer.

Continue readingLeave Me Alone and I’ll Make You Rich

That is the title of a 2020 book by Dierdre McCloskey and Art Carden. It attempts to sum up McCloskey’s trilogy of huge books on the “Bourgeois Virtues” in one short, relatively easy to read book. I haven’t read the full trilogy, so I can’t say how good the new book is as a distillation, but I found that it was easy to read and at least makes me think I understand McCloskey’s basic thesis for why the world got rich. I share some highlights here.

Part 1 of the book aims to establish that the world did in fact get richer over recent centuries, plus give a basic explanation of liberal political thought. If you already know this you could skip this part and cut down an easy 189 page read to a very easy 106 page read (part 1 is for some reason written in a way that assumes you disagree with the authors, which grates when you don’t, or perhaps also if you do).

Part 2 gets to what I at least came for- digging into the history to solve the puzzle of why the Industrial Revolution / Great Enrichment took off when and where it did. Which means first, explaining why many things people think made 18th century England special were actually common elsewhere, like markets:

Continue readingGrocery Inflation Since 2019: BLS Data is Probably About Right

Grocery prices are definitely up a lot in the past few years. I’ve wrote about this several times before. But lately there has been a trend on social media to “post your receipts” and show how much your grocery prices have gone up. Unfortunately, very few people actually post the full receipts, often just showing the total, which leads to wild claims like prices being up 250% in just the past 2 years! That’s a huge contrast to BLS “food at home” category of the CPI, which shows an increase of 4.7% from July 2022 to July 2024 (it’s also unclear in the video what the exact date of the receipt is, he just says “2 years”). Depending on the exact base month, you’re going to be in the 20-25% compared with pre-pandemic or early pandemic using BLS data.

What if we actually looked at receipts? I tried such an exercise in November 2023, when there was another round of social media videos claiming prices had doubled in just a single year. My own personal receipt matched the corresponding BLS data pretty closely, but that was just one receipt with only eight items from Sam’s Club (which might not match grocery stores, for various reasons). At the time, I couldn’t find any good receipts from 2019 or 2020 (Kroger and Walmart drop old receipts in your account after about 2 years), but after scouring an old email account, I discovered two more receipts to compare. These are both from Walmart, in 2019 and 2020, and they contain a larger number of items than my Sam’s Club receipt (each with about a dozen and half items that are fairly typical grocery purchases, and I was able to find matching products today).

I present… the receipts!

Continue readingFunds Paying “Return of Capital” Give You (Sort of) Tax-Free Income

The stock of an individual company like AT&T, or a stock fund, often pays a dividend or distribution. Typically, these dividends are taxed as income. If you buy shares of a fund like MUNI that hold municipal bonds from U.S. states and cities, the dividends from that are not taxed by the feds (they are taxed on state income taxes). That’s nice, but the yield from a muni fund MUNI is only 3.3%, and the share price of MUNI drifts around with bond prices; it does not grow like the S&P500 stocks do.

What if there was a way to get highish dividends that are not taxed, at least not in the short term? There is. Funds classify their distributions or dividends in various categories. Net investment income or short-term capital gains are taxed like interest or ordinary income (highest rates). Qualified dividends or long-term capital gain returns are taxed at a lower rate. But “Return of Capital” (ROC) distributions are not taxed at all, when you receive them. (The accounting fiction is that ROC is simply your own investment money being handed back to you, rather than you getting interest or profit, which is why it is not taxed).

ROC only catches up with you when you sell your shares. Every dollar you pocket in ROC goes to lower the formal cost basis of your shares, so that increases the capital gains tax you pay when you sell. Still, it can mean you defer paying taxes for many years, and when you do sell after many years, you will pay mainly long-term capital gains. Long-term capital gains have relatively low tax rates, and sometimes can be offset with capital losses elsewhere. So, this is a pretty good deal overall. All this only benefits you if you are holding these stocks in a taxable account, not in an IRA.

And, there are ways to not sell your shares, and hence never pay an inflated capital gains tax from all that ROC. One way not to sell your shares is to die (!). Your heirs inherit the funds at the current market value i (stepped-up basis”), without having to pay capital gains. So older folks do deliberately lard up their portfolios with ROC-paying funds or stocks, to leave to their heirs.

Another tactic is to donate the shares to charity. As I understand it, the donation gets valued at current market price, regardless of your cost basis. So, for instance, you might buy shares of XYZ fund at $100/share, collect say $50 in untaxed ROC over the next five years, and then donate the shares for a tax deduction at say $100/share (if their market price had not changed in five years). Obviously, this is only attractive if you wanted to make a charitable donation anyway.

OK, what are some funds or stocks that pay out ROC? There are number of funds which hold stocks, and write (sell) call options on them to generate income. (See here on selling options). Some (not all) of these funds pay out as mainly ROC, and are discussed here. SPYI and ETV are plain vanilla funds holding a basket of S&P500 type stocks, usually with a skew towards tech, and selling call options on them. (Or usually, selling options on an index like SPX or QQQ). SPYI is currently paying about 11.5% yield, and ETV about 9%, both mainly ROC. ETV happens to be a closed-end fund, which can be good or bad, depending on whether you buy in when the share price is at a discount or premium to the asset value. Right now, ETV is at about a 5% discount, so it is a relatively good time to buy.

It is essential to note with these high yielding funds, the raw yield is practically meaningless. You have to look at total return, which factors in stock price over time as well as cash payout. The reason is that some funds “cheat” by paying huge yields, which sucks in investors, but those yields are not really earned by the fund, so those big payouts gradually deplete the fund’s assets.

FEPI holds an equally-weighted basket of fifteen tech stocks, and sell options on them. By selling options on individual stocks, the options income is huge; FEPI pays about 20% yield. The share price bounces around heavily, being so narrowly concentrated. If tech has a bad/good day, FEPI goes way down/up. QDTE also pays about 20%. It has a more novel strategy, selling “zero-day” options, which I won’t try to explain here. It has only been running about 6 months, but is doing OK.

A problem with all these option-selling funds is that their asset value goes down 10% if the underlying stocks go down 10%, but if stocks recover fast, the value of the funds typically do not recover as much. So, the share price of these funds keeps slipping below the price of a plain stock fund like SPY or QQQ. Now, if stocks go up (which they do most years), the price of an options fund can also go up, just not as much. The lag of these options fund is significant enough that on a total return basis (i.e. with dividends and stock price included), they usually lag behind just holding the stocks. Thus, the only reason to hold these funds is to harvest the tax-free ROC, or if you have a reason to want to generate steady income without selling off stocks.

Some 1-year total returns:

SPY 26.7% Plain S&P 500 stock fund

SPYI 8.5% Option fund

ETV 8.8% Option fund

FEPI 20.2% Option fund

QDPL 25.9% Quadruple stock divi fund

(Note, it is a little random that FEPI looked so good and SPYI and ETV looked poor in the past 12 months; that is not always the case. In the past 6 months, FEPI fared much worse than SPYI and ETV, which only lagged SPY by 1-2%). Some other newish option funds that pay mainly ROC are ISPY (8% yield, sells daily options, very little return lag) and three more with fairly low return drag: XDTE and QDTE (~20% yields, daily options on S&P500 and on NASDAQ 100); QYLG (6% yield; monthly options on half of NASDAQ 100).

Another fund I became aware of recently that pays mainly ROC is QDPL. It does not sell options, so it does not suffer the return lag the other funds do. It uses a futures strategy to take about 15% of the fund assets to garner roughly 4X the normal stock dividends of the S&P500 stocks. It only yields about 5.5%, but its total return keeps up pretty well with SPY. I like this one, and am including it in my portfolio with some of the options funds discussed above.

A whole other class of stocks that pay out mainly ROC is limited partnerships. These are common, e.g., among oil and gas pipeline companies like ET and EPD. These pay 7-8% and also are having strong share price appreciation. But they issue K-1 tax forms, which most mortals don’t want to deal with (I don’t).

As usual, this discussion does not constitute advice to buy or sell any security.

Why was the Democratic Convention so patriotic?

Election season tends to spoil watching sports that have ad breaks, but one positive (for me at least) is that there is constant pedagogical fodder for my public choice & political economy class, particularly with regards to the median voter thereom. The biggest gripe with the MVT that people just insist on bringing up is the minor detail that it is obviously always wrong, which just misses the point entirely. Politics is neither fast nor slow. It’s more geological in that is slow to change until it isn’t. It can be painfully slow to watch coalitions 1. Coalesce 2. Cooperate 3. Fall apart 4. Return to 1. But politics is also opportunistic, which means responses to context can sometimes manifest relatively quickly. I would argue that nothing can provoke a more stark change in a political coalition than when their opposition abandons a position or brand that appeals to the median voter.

I tend to view Trumpology the same way I view Sovietology: it’s interesting to consume out of curiosity but we probably won’t have a deep understanding and know who was right until 20 years after the fact. Warren Nutter was right about the Soviet Union being an industrial ruse, but in his time he was mostly dismissed. My mental model of Trump and his team is that he’s a bad-faith business person who leverages transaction costs to the hilt and whose narcissism makes him effective at assembling imcompetent yes men. But, and I can’t emphasize this enough, we don’t really know what’s happening internally, there’s just too much noise in the information stream. What we can effectively observe, however, is the policy bundle and platform messaging on which he is compaigning.

That bundle is overwhelmingly negative. Beyond traditional scapegoating, the picture being painted of the current United States is bleak. Pessimistic, dystopian imagery appeals to plenty of people from the left and right extremes, but I struggle to think of a time in US history where the median American did not believe in America as both a good idea and a good place to live. A lot of people when discussing the MVT focus on the prediction that both parties will, in a vaccuum, arrive at identical platforms, an idea that seems false on it’s face. This is not unlike the prediction of physics that a feather and a bowling ball will fall at the same velocity in a vacuum – to demostrate that they don’t from the top of your apartment building is to both miss the point and place the people around you in intellectual (if not mortal) danger.

The most important insight in the MVT is the gravity of the median. Or, in the case of the current election, the speed with which one party will reclaim any branding opportunities around said median when the opposition abandons them. I have no doubt there are some veteran leaders within the RNC that are fuming over the long term costs of letting the Democratic party claim the mantle of the more patriotic and optimistic party. These are the kind of brands that are hard to take from the opposition- you pretty much have to wait for them, in a moment of foolishness or chaotic happenstance, to release their grip. Which I suspect the Republicans have.

I have no doubt the Democrats will find a way to do makes similar mistakes with this or other positions in the future. Politics is chaos and the median voter is far easier to find on an abstract two-dimensional curve than in reality. But that doesn’t mean we can pretend the median voter isn’t out there and that they don’t matter. It’s a simple model that may always be wrong, but it will never lead you astray.

Top EWED Posts of 2024

The following are notable posts from 2024, in descending order by the number of views this year.

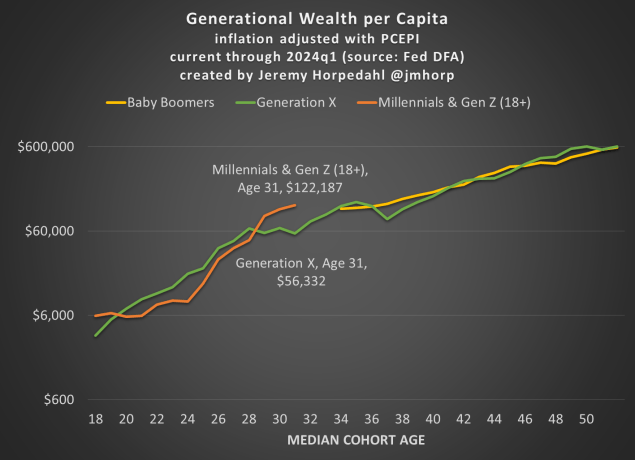

- Young People Have a Lot More Wealth Than We Thought Jeremy Horpedahl was first to this scene. American Millennials, on average, have money. Perhaps this is becoming common knowledge now among folks that read The Economist. The US is getting gradually richer, and the average young adult is benefiting. You can see more from Jeremy by following him on Twitter/X.

- Civil War as radical literalism Mike Makowsky writes, “There’s a million war movies, most of which have arcs and metaphors strewn throughout. The problem with making a moving about a hypothetical civil war in the modern United States is that the audience will spend so much time looking for the heroes, villains, and associated opportunities to feel morally superior that it seems almost impossible to deliver an effective portrayal of what it might actually feel like to wake up to a US civil war…”

- Is “Rich Dad Poor Dad” a Fraud? Scott explores whether a popular finance book is based on a false premise.

- Is the Universe Legible to Intelligence? I (Joy) do philosophy. It also has practical implications. Can machines outsmart us, for better or worse? How smart can anything physical be. Maybe, as @sama says, “intelligence is an emergent property of matter…” However, maybe “intelligence” only goes so far. We have many posts on artificial intelligence this year.

- How To Drive a Turbocharged Car, Such as a Honda CR-V This is one of those pieces by Scott that people find through search engines when they are looking for help.

- Grocery Price Nostalgia: 1980 Edition You can use our search function to find everything from this year about the topic of inflation.

- The US Housing Market Is Very Quickly Becoming Unaffordable

- Predicting College Closures James reflects on closing universities and what indicators might help stakeholders like parents and faculty anticipate the next event.

- Counting Jobs (Revisited) Jeremy did something that might have sounded boring at the time. Yet, soon afterwards there was serious interest in the question of : Did 818,000 jobs vanish?

- Why Avocado on Toast? As an avocado toast person, I loved this. I’m glad many other people found Zachary’s post interesting.

- Recovering My Frozen Assets at BlockFi, Part1. How Sam Bankman-Fried’s Fraud Cost Me.

- Why Don’t Full Daycares Raise Prices? The cost of childcare is an important issue. James wrote this from personal experience, and I pointed out something similar before.

- This post only got medium traffic in terms of the number of views this summer. Now that we know who the candidate will be, it’s interesting to look back and see a vindication of betting markets. Who Will Be the Democratic Presidential Candidate? Follow the Money (Betting Markets)

- Honorable mention to Mike’s post from 2022 that continues to get many search hits: Why Agent-Based Modeling Never Happened in Economics

At this point, the EWED authors have each written enough words to constitute a book. Watching this blog grow and flux with the rest of the internet has been fascinating.

You can subscribe to our WordPress site to get posts sent to your email. The widget for putting your email in should be on the right side of your screen on a computer, or you can find it by scrolling to the bottom of the home page on a mobile device. WordPress will let you customize your preferences so that you get emails batched once a week if you prefer that to Every Day.

Persistent Beliefs

The things that happen between people’s ears are difficult to study. Similarly, the actions that we take and the symbolic gestures that we communicate to the people around us are also difficult to study. We often and easily perceive the social signals of otherwise mundane activities, but they are nearly impossible to quantify systematically beyond 1st person accounts. And that’s me being generous. Part of the reason that these things are hard to study is that communication requires both a transmitter and a receiver. One person transmits a message and another person receives it. Sometimes, they’re on slightly or very different wavelengths and the message gets garbled or sent inadvertently and then conflict ensues.

Having common beliefs and understandings about the world help us to communicate more effectively. Those beliefs also tend to be relevant about the material world too. A small example is sunscreen. Because a parent rightly believes that sunscreen will protect their child from short-run pain and long-run sickness, they might lather it on. But, due to their belief, they also signal their love, compassion, and stewardship for their child. A spouse or another adult failing to apply sunscreen to a child signals the lack thereof and conflict can ensue even when the long-term impact of one-time and brief sun exposure is almost zero.

People cry both sad and happy tears because of how they interpret the actions of others – often apart from the other external effects. Therefore, beliefs imbue with costs and benefits even the behaviors that have seemingly immaterial consequences otherwise. We can argue all day about beliefs. And while beliefs might change with temporary changes in the technology, society, and the environment, core beliefs need to be durable over time. Therefore, if this economist were to recommend beliefs, then I would focus on the prerequisite of persistence before even trying to find a locally optimal set.

Here are three inexhaustive criteria for a durable beliefs:

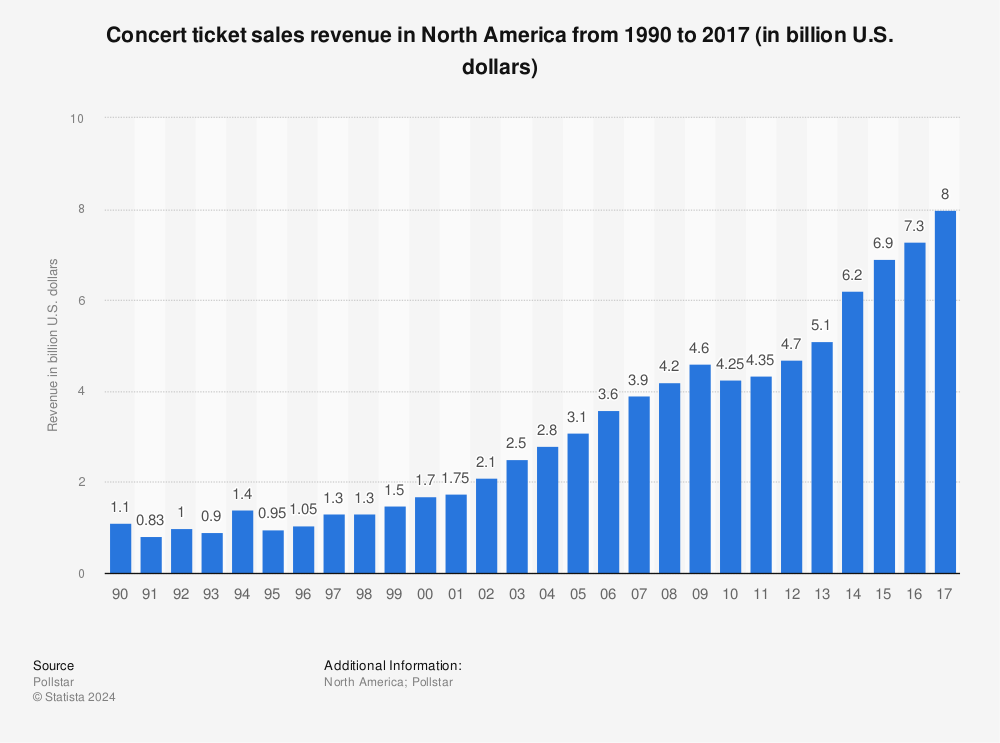

Continue readingPeople Are Paying for Music Again

Recorded music sales peaked in 1999- then came Napster and other ways to listen to the exact music you want for free. Recorded music sales still haven’t fully recovered, but with the rapid growth of paid streaming since 2014, they have been increasing again:

Meanwhile, live music sales have exploded since the ’90s:

The latest report from Pollstar on the top live tours is positively glowing:

2023 was a colossus, the likes of which the live industry has never before seen. If 2022 was a historic record-setting year, which it was, then this year completely blew it out of the water— by double digits. Total grosses for the 2023 Worldwide Top 100 Tours were up 46% to $9.17 billion

When you combine live and recorded sales, total spending on music has now passed the 1999 peak; this is the biggest the market for music has ever been. Of course, this doesn’t mean its an easy time to be a musician; touring is hard work and, as always, record labels and others are taking a big share of the money before it gets to artists. And opinions differ about whether today’s environment is good for creating good new music.

There are dozens of songs about how the road is hard, and the more time you spend on the road, the less they sound like cliches than like a simple and sometimes stark description of your life. Sooner or later everybody spots the exit that has their name on it –John Darnielle

The BLS data is noisy but suggests that the number of musicians in the US has been fairly flat and is projected to stay that way. A lot will depend on whether live music continues to grow, how much of that is captured by a few superstars, and whether the current streaming paradigm continues, or goes in a more or less artist-friendly direction. But now that consumers are willing to pay for music again, artists at least have a fighting chance.

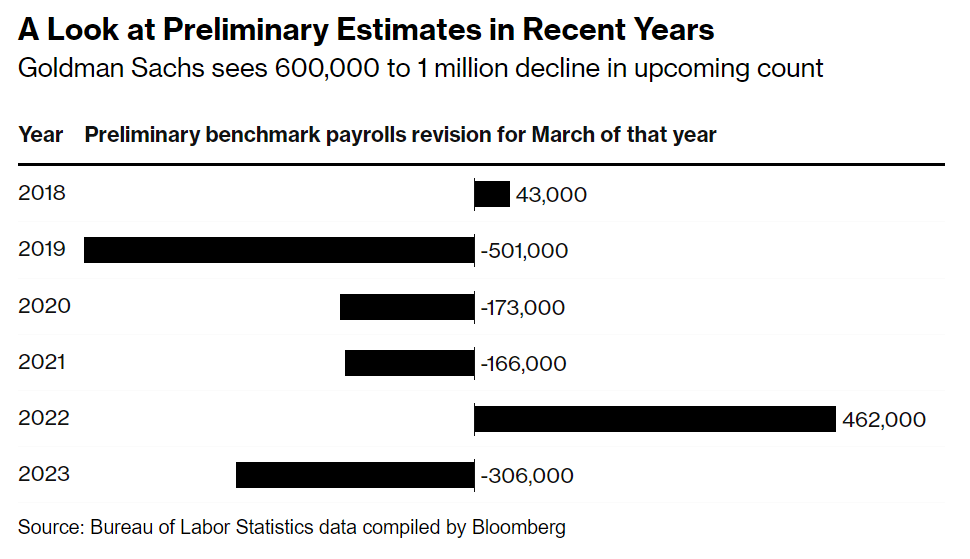

Did 818,000 jobs vanish?

This morning the Bureau of Labor Statistics released the latest quarterly data for their Quarterly Census of Employment and Wages for the first quarter of 2024. Along with this release is the announcement of their preliminary “benchmark estimate” for March 2024, which will eventually (next year) be used to revise employment data for the Current Employment Statistics program. To keep all of the alphabet soup of programs clear in year head, CES is the more familiar “nonfarm jobs” data that is released each month, usually with some media fanfare.

Benchmarking is an important part of the process for many data releases, because the monthly CES data is based on a survey of employers, a subset of the total. But the QCEW data is the universe of employees — at least the universe of the those covered by Unemployment Insurance law, which is something like 97-98% of workers in the US. So the numbers will never match exactly (CES is supposed to be measuring all workers, not just the 97-98% covered by UI), but they should be pretty close. The media reports the CES monthly data more prominently, because it is more timely and usually pretty close to correct — but benchmarking is the process to see just how correct those initial surveys were.

That brings us to the release today, which is the preliminary estimate of the benchmark adjustment for March 2024 (it will be finalized early in 2025). And that preliminary estimate was a big number, with a downward revision projected of 818,000 jobs. To put this in perspective, the current CES data shows 2.9 million jobs were added between March 2023 and March 2024, so this estimate suggest that the job growth was overstated by perhaps 40 percent. That’s a big revision, though large revisions are not unheard of: the same figure for March 2022 was an estimated 468,000 jobs higher, while March 2019 was 501,000 jobs lower. But this year is a big one (largest absolute number since 2009). Here’s a chart summarizing recent years revisions from Bloomberg:

I’ve covered this topic before, such as an April 2024 post where I noted that as of September 2023, there was an 880,000 gap in job growth between the CES and QCEW over the prior year. So this was not unexpected, and in the days leading up to the report, close followers of the data were forecasting that the revision could be up to 1 million jobs.

Continue reading