Thankfully for US consumers, grocery prices have leveled off. They haven’t fallen, of course, which will still lead to viral complaints about egg prices, etc. But over the past 4 years, wages have almost caught up with grocery prices.

Not so with fast food prices (“limited service meals”), which have definitely outpaced wages over the past 4 years, and continue to grow at an annual rate of about 5 percent (also more than wages).

Furthermore, if we go back to 2014, we see it’s not just a post-pandemic effect on fast food. Prices since 2014 are up 54 percent for fast food according to the BLS, more than the 31 percent overall CPI-U increase and more than average wages (46 percent).

An article from FinanceBuzz puts together some more specific data on a dozen fast-food chains in the US. Consumer favorites for a quick, cheap bite to eat like Taco Bell and McDonald’s have seen menu prices increase by 80 or even 100 percent!

Check out the article for even more specific food item data at each of these restaurants. For example, the most famous of fast-food sandwiches is the Big Mac, which is up from $3.99 in 2014 to $5.99 in 2024, a 50 percent increase. A Whopper meal at Burger King is up 79 percent. All the more reason to seek out deals in the apps, or just good-old in-store discounts, like the “buy one get one for $1” promo at most McDonald’s. This deal would get you two Big Macs for $7, or $3.50 each… less than in 2014! Or since today is Wednesday, you might want to head to Burger King, where Whoppers are $3 at most locations (regular price: around $6).

Price discrimination is alive and well at the drive-thru window, and if you are just ordering from the menu without any discounts, you are really going to feel the pain of inflation.

What’s the connection between social media use and mental health, especially among young people? You’ve probably heard a lot about this recently, in the media, by politicians, and among friends chatting about their kids. Lots of assertions are made, but there is also a bit of research on this topic. As someone who frequently uses social media myself, as well as a parent of young children, and a teacher that works every week with young college students, I am particularly interested in this topic.

Jonathan Haidt and various co-authors have been trying to catalog all the research on the topic and figure out if there is a connection between the decline in teenage mental health and the rise of social media use. Haidt also has a new book on this topic, as well as the decline of “free play” among kids, which I have not yet read but I’ve looked through his documents that contain all of the underlying and summaries of the research he is citing. I’ll read the book soon, as I’m certainly part of the intended audience (see the last sentence of the above paragraph). And while this research is very much outside of my area of expertise, my training as an economist has taught me how to read academic papers and to be convinced by evidence, so once again I’m very much the intended audience on this score as well.

Please read this post as my attempt to understand the evidence and start to form conclusions and/or critique what Haidt is saying. It’s a work in progress, and I’ll write more as I read and think more about it.

Christians across the world are observing the season of Lent right now, concluding this week. This important period of religious observance involves personal sacrifice of some sort, and for Western Christians a common form of sacrifice is abstaining from consuming meat on Fridays during Lent. But there is one exception: most Christians allow consumption of fish on Fridays, in lieu of other kinds of meat.

But abstaining from meat on Fridays was not always a practice reserved for Lent. Catholics used to abstain from meat for the entire year prior to a 1966 decree by Pope Paul VI. This decree relaxed the rules on fasting and decentralized them. In the US, Catholic Bishops chose to eliminate meatless Fridays, except during Lent.

No doubt this was an important religious change, but it was also an important economic change. And the first question an economist would ask is: how did this impact the price of fish? In our simple supply and demand framework, this should result in a decrease in demand, which would lower the price of fish. Did that happen?

In 1968, economist Frederick Bell asked just that question in an article published in the American Economic Review titled “The Pope and the Price of Fish.” The short answer is that yes, the price of fish did indeed decline!

Lately on Twitter this chart has been going around:

The chart comes from Bloomberg journalist Justin Fox, who always puts together interesting economic data. You can read his interpretation of the data at Bloomberg, but the folks posting it on Twitter all seem to have the same shock and awe: Detroit was the richest big city in 1949. And of course we all know that today it isn’t. Still, the Detroit MSA has done OK since 1949, even though it is no longer anywhere near the top.

How well has Detroit done? Despite industrial decline and many other major problems, median household income of the Detroit MSA was around $71,000 in 2022 according to the Census Bureau. How does this compare to the $3,627 median income in 1949? It’s about double in real terms: you can multiply it by about 10 using the Census’ preferred inflation adjustment for household incomes since 1949 (the C-CPI-U since 2000, and the R-CPI-U-RS before that).

Let me start by saying high rates of inflation, especially unexpected inflation, are bad. Still, it is useful to have some historical context. We’ve experienced the highest inflation rates in a generation lately, especially in 2022, but past generations experienced inflation too. How to compare?

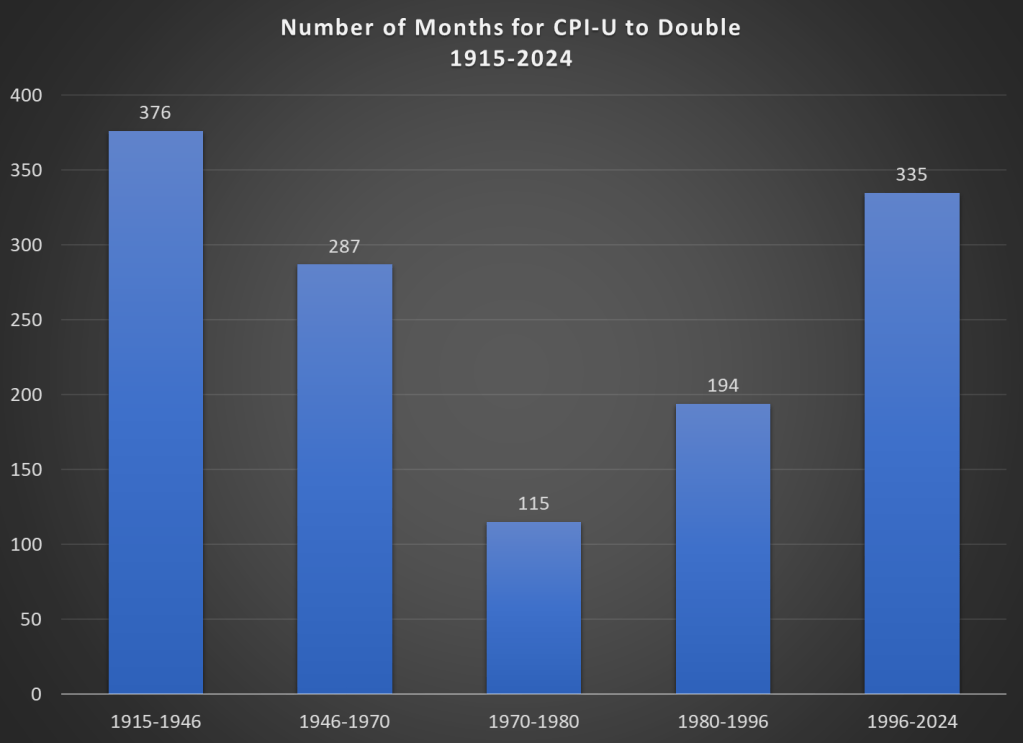

Here’s one approach. Using the latest CPI-U data, we can see that prices on average approximately doubled between March 1996 and February 2024. That’s 335 months to double, or just shy of 28 years. How long did it take prices to double if we keep moving backward in time from March 1996?

It only took 194 months for prices to double from January 1980 until March 1996, just a little over 16 years. Prior to January 1980, prices doubled even quicker, this time taking less than 10 years! Prior to that, it took 24 years for prices to double between WW2 and 1970, and before that you have to go back 31 years to 1915 for another doubling. Judged by this, our recent history doesn’t look so bad.

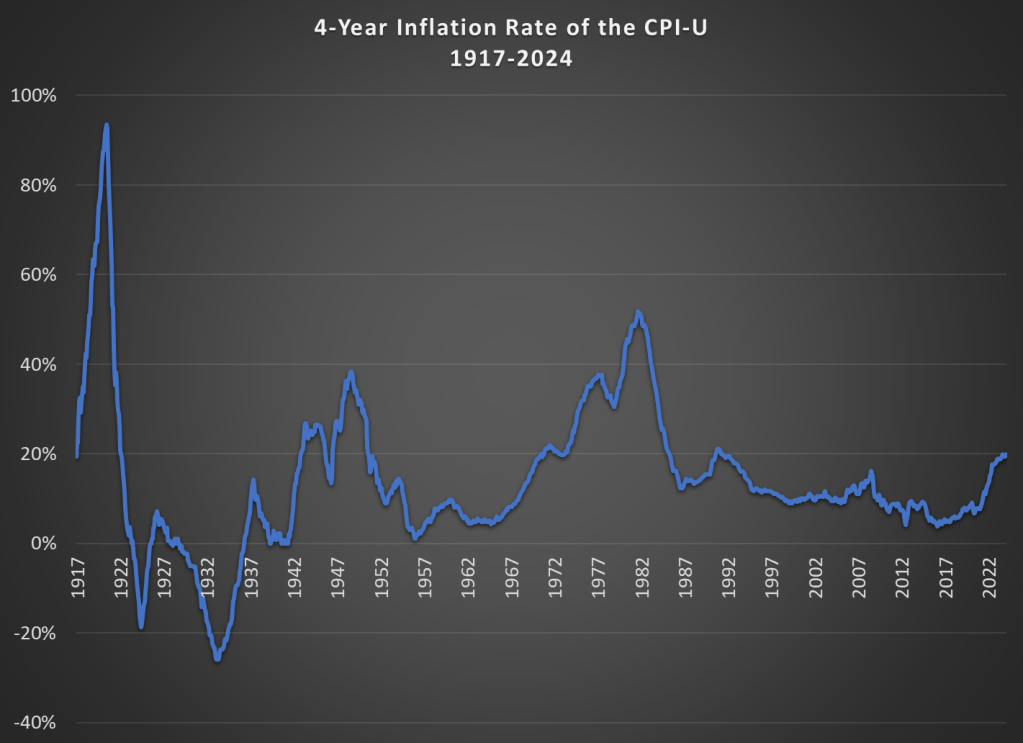

That doesn’t mean everything is OK. As I said above, unexpected inflation is the worst kind, since individuals and businesses aren’t planning for it. And we’ve had 20% inflation in the past 4 years — something not seen since 1991 over a 4-year time period. A 20%+ inflation rate is unusual to us today, but it certainly wasn’t in the past: basically all of the 1970s and 1980s had 20%+ inflation every 4 years, sometimes more than 40% or even 50%.

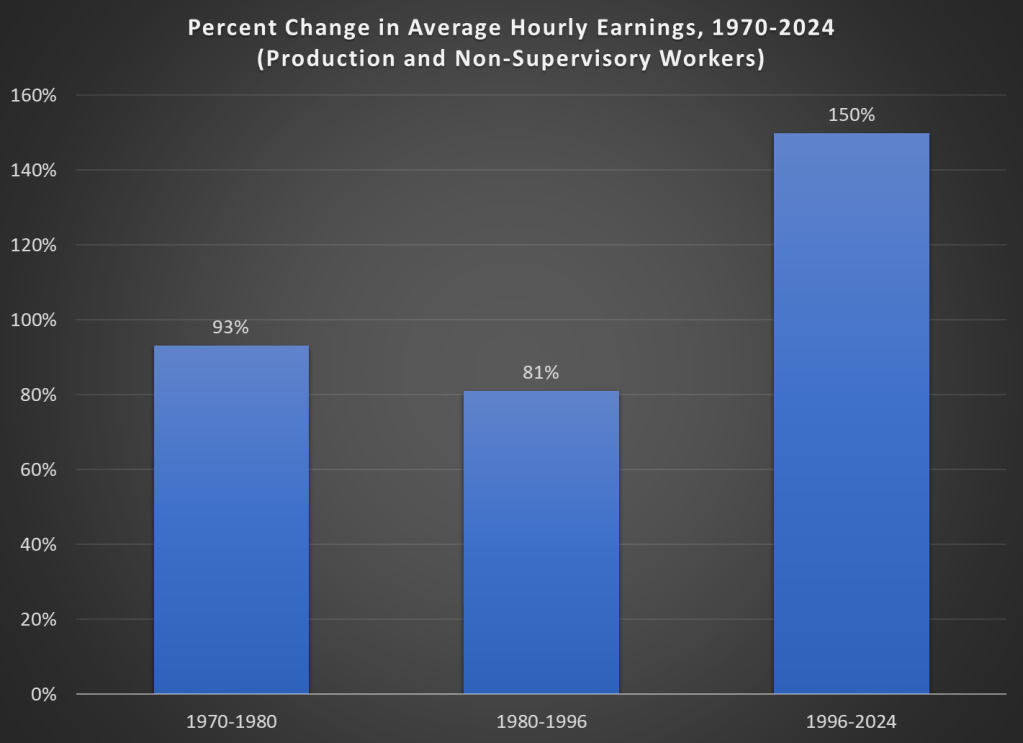

Finally, while unexpected inflation is bad, we also care about the relationship between wage increases and price increases. We can rightfully bemoan rapid, unexpected price inflation, but if wages are increasing faster than inflation, we are still better off (on average). The BLS average hourly wage series for production and non-supervisory workers only goes back to 1964, so we can’t do a full comparison with the CPI-U, but we can compare the three most recent doublings of prices.

Keep in mind with the chart above that prices (as measured by the CPI-U) increased by 100% for each of these time periods. So, for the 1970s and 1980-1996 periods, wages actually rose by less than rate of inflation — wage stagnation! If we used the PCE price index instead, those time periods still don’t look good: PCE prices increased by 88% for 1970-1980, 85% from 1980-1996, and 78% since 1996. With either price index, the 1996-2024 period is clearly the best of these three, and it’s not even really close.

Let me finish where I started: the recent inflation is bad. I don’t want to downplay that. But some historical perspective is also useful.

By now, hopefully we’ve all heard of shrinkflation. But if you haven’t, it’s when the unit price (e.g., the cost per pound) increases not because the price of the good went up, but because the product shrank in size.

Let’s be clear about a few things. First, this is nothing new. Here’s an Economist story from 2019 (pre-pandemic and pre-Bidenflation) talking about shrinkflation. You can find many such anecdotal stories back even further.

Second, the BLS is aware of this. They track it, and price it into the CPI. Take a look at the price data which underlies the CPI: it’s all stated in units. Price per pound, price per dozen, etc.

Moreover, the BLS also recently gave us some data on how frequently this happens. It’s pretty rare. Even among food items, which are a category the includes a fair amount of shrinkflation, only about 3 percent of products experienced any downsizing or upsizing from 2015-2021. That’s right, sometimes packages get larger, not smaller, which effectively lowers the unit price. “Shrinkdeflation” anyone?

Ignore the weird obsession with Biden’s ice cream habit. The Senator is concerned that NYC is not safe.

But what’s the reality? Here’s a map showing the homicide rate in each state, and its relative position to NYC (data is from the CDC for 2022, the most recent complete year available right now).

The light-colored states have a lower homicide rate than NYC (5.2 deaths per 100,000). There’s 18 of those states. But most states have higher homicide rates than NYC. Some are a lot higher, even triple NYC in a few states (colored purple). Alabama’s homicide rate of 13.9 deaths per 100,000 people is about 2.5 times as high as New York City.

But perhaps the homicide rates in these states are being driven by high homicide rates in cities in those states? Comparing a city to a state is perhaps a little strange to do, but I also often hear this retort: well, it’s those cities, especially “Democrat-controlled” cities, that are driving the high homicide rate in Alabama and elsewhere. And while this is true to a certain extent, comparing rural counties to New York City doesn’t make Alabama and the South look much better:

For this map I combined 2021 and 2022 data, because the CDC doesn’t report very small numbers (usually under 10 deaths), so grouping two years is needed to get more data. Even so, there are still a handful of states that don’t have enough homicides for CDC to report them over that two-year period, and they are shown in gray on the map (as well as states that have no rural counties: Delaware, Rhode Island, and New Jersey).

Notice that even focusing on just the rural counties, there are almost 20 states with higher murder rates than New York City. Again, some are double or even triple. Rural Alabama, at 11 deaths per 100,000 people, is exactly double NYC. Notably, the entirety of the rural South is higher than NYC.

If this is all true, why might New York City feel less safe? There are a number of possible explanations, but I’ll offer a few. First, homicide isn’t the only kind of crime. While it does correlate with other crimes, it’s not a 1:1 relationship, so it’s likely that some places with higher homicide rates than NYC have lower levels of assault, rape, or property crimes. These are even more challenging to compare across jurisdictions, but it’s a possible explanation. Related, NYC is a relatively safe big city! Other big cities wouldn’t compare as favorably to Alabama. But folks just seem to love NYC as a punching bag.

The other explanation is just the sheer number of people, and therefore homicides. According to the CDC, NYC had 434 homicides in 2022, that’s an average of more than one per day. You could literally turn on the news every single day and hear about a murder, and perhaps you had even been in the neighborhood where it happened recently. Contrast rural Alabama, which had 65 homicides in 2022. That’s only about one per week. And it might be happening in a completely different part of the state from you, so you either don’t hear about it or think “that’s somewhere else.”

But rural Alabama only has about 600,000 people. NYC has fourteen times as many people. So if we are trying to answer the question “What are the odds that a random person is murdered in a given year?”, we need to take population into account. That’s the logic of reporting homicide rates. Indeed it may feel like NYC is less safe, and that’s a natural human reaction. But that’s why the data is so important, to give us a sense of proportion.

Food prices are up a lot in the past few years. I’ve written about this several times in the past few months. In the US, we’ve seen grocery prices go up 20% on average in just 3 years. That’s much higher than we are used to: in the decade before the pandemic, the average 3-year increase was just 4%. In fact, the 3-year increase was negative for much of 2017 and 2018. To find increases this big, you have to go back to the late 1970s and early 1980s (when sometimes the 3-year grocery inflation rate was almost 50%).

But if it’s any consolation, this is not a problem that is unique to the US: food prices are up around the globe. That’s a relevant insight when we come to a recent viral video from Tucker Carlson’s visit to a Russian grocery store. Carlson says that the inflation and cost of groceries will “radicalize you against our leaders.”

So what has food price inflation looked like in Russia, the US, and the other G7 countries? (What used to be called the G8, until Russia invaded Crimea in 2014.) Here’s the chart:

Cumulatively since January 2021, when our current “leaders” came into power in the US, food prices are up 20% in the US, as I said above. But notice that this is on the low end for this group of countries. Japan, with consistently low inflation and occasionally deflation over the past few decades, has been the lowest over this timeframe (though even in Japan, food prices are up about 7 percent in the past year).

But notice who is the highest: Russia, where grocery prices are up 32% in the past 3 years. Certainly, their invasion of Ukraine and the resulting global sanctions plays a role in this, but even if we look at early 2022, the cumulative 15% food inflation was much higher than any G7 country.

So blaming our leaders for rampant inflation is probably not a good idea, especially if you are trying to portray Russia in a positive light.

Perhaps the more charitable interpretation of Tucker Carlson is that the nominal price of groceries is lower, rather than the rate of inflation (even though he does mention inflation in the video). The basket of food they purchase in the video comes out to the equivalent of about $100 at current exchange rates. Everyone on his crew guessed it would be around $400.

I can’t say whether their guess of $400 was accurate, but it would not be totally surprising if the prices of non-tradable goods were lower. This is what would expect in a country with lower wages. While we normally think of services as non-tradable, it’s also reasonable to assume that a lot of fresh food, such as produce, bread, and dairy, is also non-tradable (at least not without high transaction costs).

Carlson’s claim that people “literally can’t buy the groceries they want” is a much more apt statement of the state of affairs in Russia (and other poor countries) than it is in the US and Western Europe.

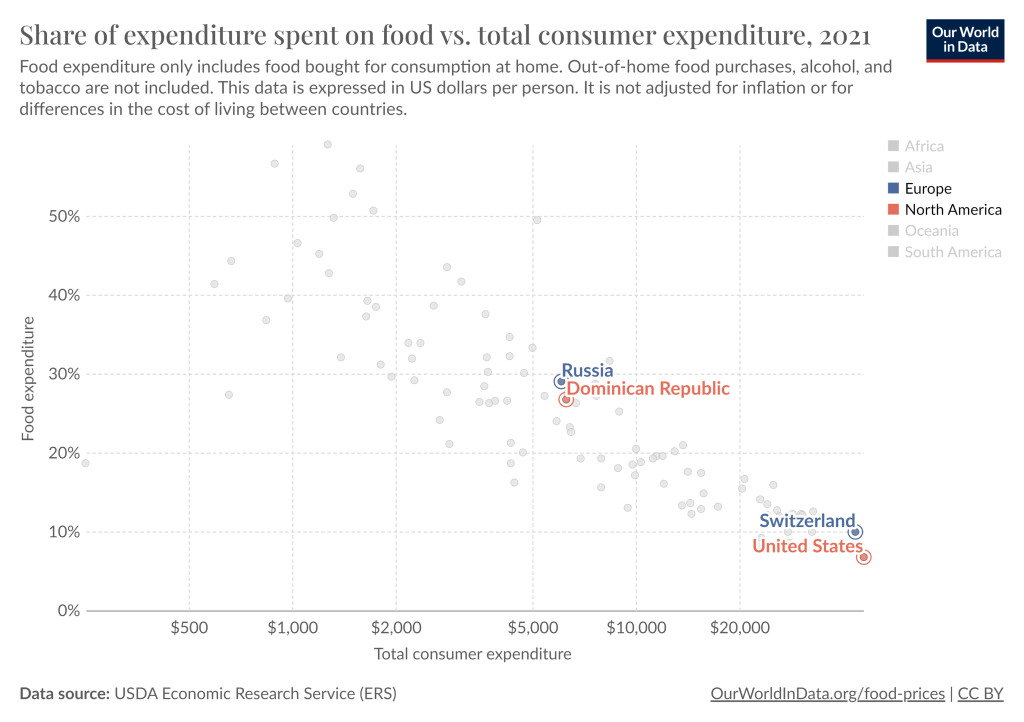

The average Russian allocates about 30% of their spending to groceries, similar to the Dominican Republic. And this data is from 2021, just before the massive spike in food prices in Russia. Meanwhile, the US is by far the lowest, at just under 7%. The UK, Canada, and Switzerland are the closest to the US, but they are in the 9-10% range. Food in the US is cheap.

The food inflation we’ve experienced in the US has been bad, the worst in a generation. But it’s not exactly clear that our “leaders” are to blame. And it’s also pretty clear that it’s much worse in the rest of the world, especially in Russia.

In a post from July 2021, I discussed housing affordability and “zoning taxes” — in other words, how land use restrictions such as zoning were driving up the cost of housing in some US cities. San Francisco, Los Angeles, Seattle, and New York stood out as the clear outliers, with “zoning taxes” adding several multiples of median household income to housing costs.

The paper I was summarizing used data from 2013-2018, and it’s a very well done paper. But so much has changed in the US housing market since that time. In my post, I pointed to a map from 2017 showing that a large swatch of the interior country still had affordable housing — loosely defined as median home prices being no more than 3 times median income.

To see how much has changed so quickly, consider these two maps for 2017 and 2022 generated from this interactive tool from the Joint Center for Housing Studies.

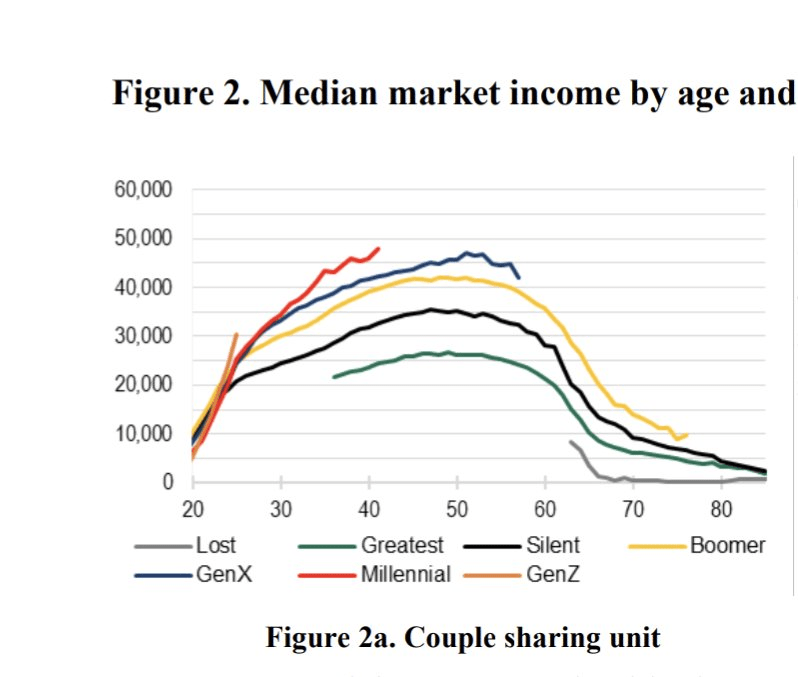

Regular readers know that I’ve written numerous times about the wealth levels of younger generations, such as this post from last month. Judged by average (and usually median too) wealth, younger generations are doing as well and often better than past generations. This is not too surprising, if you generally think that subsequent generations are better off than their parents, but many people today seem to think that progress has stopped. The data suggest it hasn’t stopped!

Now there’s a great new paper by Kevin Corinth and Jeff Larrimore which looks at not wealth but income levels by generation. The look at income in a variety of different ways, including both market income and post-tax/transfer income. But the result is pretty consistent: each generation has higher incomes (inflation adjusted) than the previous generation. Here’s a typical chart from the paper: