Abstract: We study how transparent information about effort impacts the allocation of earnings in a dictator game experiment. We manipulate information about the respective contributions to a joint endowment that a dictator can keep or share with a counterpart…

Employees within an organization are sensitive to whether they are being treated fairly. Greater organizational fairness is shown to improve job satisfaction, reduce employee turnover, and boost the organization’s reputation. To study how transparent information impacts fairness perceptions, we conduct a dictator game with a jointly earned endowment.

The endowment is earned by completing a real effort task in the experiment, an analog to the labor employees contribute to employers. First, two players work independently to create a pool of money. Then, the subject assigned the role of the “dictator” allocates the final earnings between them.

In the transparent treatment, both dictators and recipients have access to complete information about their own effort levels and contributions, as well as those of their counterparts. In the non-transparent treatment, dictators have full information about the relative contributions of both players, but recipients do not know how much each person contributed to the endowment. The two treatments allow us to compare the behaviors of dictators who know they could be judged and held to reciprocity norms with dictators who do not face the same level of scrutiny.

*drumroll* results:

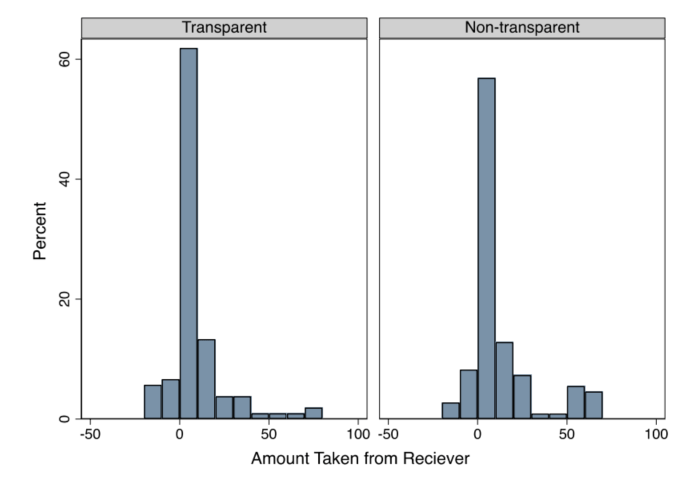

This graph shows the amount of money the dictators take from the recipient contribution, in cents. There are two ways to look at this. Notice the spike next to zero. Most dictators do not take much from what their counterpart earned. They are *dictators*, meaning they could take everything. Most take almost nothing, regardless of the treatment. We interpret this to mean that they are acting out of a sense of fairness, and we apply a humanomics framework to explain this in the paper.

Also, there is significantly more taken in non-transparency. When the worker does not have good information on the meritocratic outcome, then some dictators feel like they can get away with taking more. Some of this happens through what we call “shading down” of the amount sent by the dictator under the cover of non-transparency.

There is more in the paper, but the last thing I’ll point out here is that the “worker” subjects (recipients) anticipate that this will happen. The recipients forecast that the dictator would take more under non-transparency. In our conclusion, we mention that, even though the dictator seems to be at an advantage in a non-transparent environment, the dictator still might choose a transparency policy if it affects which workers select into the team.

View and download your article* This hyperlink is good for a limited number of free downloads of my paper with Demiral and Saglam, says Springer the publisher. Please don’t waste it, but if you want the article I might as well put it out there. I posted this on 11/2/2024, so there is no guarantee that the link will work for you.

Parkinson’s Law, the principle that “work expands to fill the time available for its completion,” was originally intended as a satirical observation on bureaucratic inefficiencies. However, it has broader applications, especially in academic life. When preparing to teach an intermediate microeconomics class, for example, I often find that Parkinson’s Law applies: no matter how much time I dedicate, there’s always more content, illustrative examples, and analysis that could be included. The time invested in preparation creates a tradeoff between covering the broad spectrum of microeconomic theories versus delving deeply into a few core concepts. Either approach can be effective, but Parkinson’s Law reminds me that more preparation doesn’t always imply improvement.

Teaching intermediate microeconomics presents a natural tradeoff between breadth and depth. The course covers foundational concepts like consumer and producer theory, market structures, and welfare economics, and each of these areas is rich with intricate details, special cases, and real-world applications. A broader approach would expose students to more topics, providing a more comprehensive view of microeconomics. Exploring fewer topics fosters more critical thinking and analytical skills. Too much preparation on one topic can detract from time that could be spent introducing other essential concepts… Or other classes for that matter.

Let’s say I have a few hours to prepare for a Monday lecture on consumer theory. I might fall into a spiral of over-preparation: digging into endless variations of consumer surplus or finding additional applications that illustrate price elasticity. This is precisely what Parkinson’s Law warns against; if I pour time into my preparation, then the lecture becomes denser beyond the ideal for my students’ comprehension.

The extra hours may result in a more detailed presentation, but this doesn’t necessarily mean better learning outcomes. A concise, well-planned lecture is often just as effective—if not more so—than one crammed with detail. Overwhelming students with information that won’t stick is bad pedagogy.

I doubt anyone has been waiting for my take on the Trump and Harris economic plans to decide their vote. More than that, it is entirely reasonable to vote based on things other than their economic plans entirely- like foreign policy, character, or preservingdemocracy. But either Trump or Harris will soon be President, and thinking through their economic plans can help us understand how the next 4 years are likely to go.

The bad news is that both campaigns keep proposing terrible ideas. The good news is that, thanks to our system of checks and balances, most of them are unlikely to become policy. The other good news is that our economy can handle a bit of bad policy- as Adam Smith said, there’s a lot of ruin in a nation. After all, the last Trump admin and the Biden-Harris admin did all sorts of bad economic policies, but overall economic performance in both administrations was pretty good; to the extent it wasn’t (bad unemployment at the end of the Trump admin, bad inflation at the beginning of Biden-Harris), Covid was the main culprit.

Note that this post will just be my quick reactions; the Penn Wharton Budget Model has done a more in-depth analysis. They find that Harris’ plan is bad:

We estimate that the Harris Campaign tax and spending proposals would increase primary deficits by $1.2 trillion over the next 10 years on a conventional basis and by $2.0 trillion on a dynamic basis that includes a reduction in economic activity. Lower and middle-income households generally benefit from increased transfers and credits on a conventional basis, while higher-income households are worse off.

We estimate that the Trump Campaign tax and spending proposals would increase primary deficits by $5.8 trillion over the next 10 years on a conventional basis and by $4.1 trillion on a dynamic basis that includes economic feedback effects. Households across all income groups benefit on a conventional basis.

We are already running way too big a deficit; candidates should be competing to shrink it, not make it worse. This isn’t just me being a free-market economist; Keynes himself would be saying to run a surplus in good economic times so that you have room to run a deficit in the next recession.

Now for my lightning round of quick reactions:

No tax on tips: both campaigns are now proposing this; it is a silly idea, there is no reason to treat tips differently from other income. The good news is that this almost certainly won’t make it through Congress.

Taxes: Trump’s Tax Cuts and Jobs Act of 2017 is set to expire in 2025. He says he wants to renew it and add more tax cuts, though he will need a friendly Congress to do so. Harris wants to let most of it expire, but renew and expand the Child Tax Credit while raising taxes on the wealthy and corporations. There’s a good chance we end up with divided government, in which case probably only the most popular parts of TCJA (increased standard deduction and child tax credit) get renewed and no big new changes happen.

Price controls: both campaigns, especially Harris‘, have talked about fighting ‘price gouging’, leading economists to worry about the price controls (any intro micro class explains why these are a bad idea). My guess is that no real bill gets passed, President Harris gets the FTC to make a show of going after grocery stores but nothing major changes.

Tariffs: Harris would probably leave them where they are; Trump is promising to raise them 10-20% across the board and 60% on China. This would lead to higher prices for US consumers and invite retaliation from abroad; we saw the same things when Trump raised tarriffs in his first term, but he is promising bigger increases now. This is worrisome because the President has a lot of power to change tariffs unilaterally; it would take a bill getting through Congress to stop this, and I don’t see that happening.

Regulation / One in two out: The total amount of Federal regulation stayed fairly flat during the Trump administration thanks to his one in two out rule, while regulation increased during the Biden-Harris administration. I expect that a second Trump admin would behave like the first here, while a Harris admin would continue the Biden-Harris trend.

Antitrust: FTC and DOJ have been aggressive during the Biden-Harris administration, blocking reasonable mergers and losing a lot in court. But Trump’s VP candidate JD Vance thinks FTC Chair Lina Khan is “doing a pretty good job”, so we could see this poor policy continue either way. More generally, voters should consider what a Vance presidency would look like, because making him Vice President makes it much more likely (Trump is 78 and people keep trying to shoot him; plus VPs get elected President at high rates).

Immigration: Immigration rates have been high under the Biden-Harris admin, while Trump’s top two planks in his platform are “seal the border” and “carry out the largest deportation operation in American history”. Economically, this would lead to a reduction in both supply and demand in many sectors, with the relative balance (so whether prices go up or down) depending on the sector. The exclusion of Mexican farmworkers in the 1960’s led to a huge increase in mechanization, to the point that domestic farmworkers saw no increase in their wages; presumably this also limited the potential harm to the food supply.

Crypto: The Biden admin has been fairly negative on crypto; both Harris and Trump are making pro-crypto statements in their campaigns, particularly Trump.

Marijuana: The Biden admin is in the process of rescheduling marijuana to no longer be in the most restricted category of drugs. I think Trump would probably see the process through, while Harris definitely would.

Elon Musk / Civil Service: Elon Musk has thrown his support hard behind Trump, spending lots of money, tweeting continuously, and attending rallies. It’s hard to know how much of this is genuine support for a range of Trump’s policies, how much is to get the Federal government to stop suing his companies so much, and how much is to get himself a direct role in government. In any case, it is a safe bet that more Federal civil servants get fired in a Trump admin than in a Harris admin. What’s much harder to say is how many get fired, and what proportion of firings come from a genuine attempt to improve efficiency vs a purge of those Trump sees as disloyal. Personally I think government could stand to treat its employees a bit more like the private sector, making it easier to fire people for genuine poor performance (not political views), but also allowing for more flexibility on improved pay, benefits, and the ability to focus on achieving goals more than following the way things have always been done. But I doubt that’s on the table either way.

CFTC/ Prediction Markets: The Biden CFTC has tried to crack down on prediction markets, though they have mostly failed in the courts, and the growth of Kalshi and Polymarket mean that prediction markets are now bigger than ever. Most of the anti-prediction-market decisions have been 3-2 votes of the democrats vs the republicans, so a new republican appointee could lock in the legal gains prediction markets have made, though this is far from guaranteed (not all Rs support this).

Final Thoughts: So much of how things turn out will depend not just on who wins the Presidency, but on whether their party wins full control of Congress. Because the Democrats have a lot more Senate seats up for grabs this year, Harris is much more likely to be part of a divided government (especially once you consider the Supreme Court).

Because of this, and because of the ability of the President to raise tariffs unilaterally, I see Trump as the bigger risk when it comes to economic prosperity, as well as non-economic issues. Harris with a Republican Senate is the best chance of maintaining something like the status quo, whereas a Trump victory is likely to see bigger changes, many of them bad.

That said, predicting the future is hard, and this applies doubly to Presidential terms. I’m struck by how often in my lifetime the most important decisions a President had to make had nothing to do with what the campaign was fought over. Who knew in 1988 that the President’s biggest task would be managing the breakup of the Soviet Union? In 2000, that it would be responding to 9/11? Bush specifically tried to distinguish himself from Gore as being the candidate more against “nation-building”, then went on to try just that in Afghanistan and Iraq. In 2004, who knew that the biggest issue of the term would be not Social Security or foreign policy, but a domestic financial crisis and recession? In 2016, who knew that they were voting on the President that would respond to the Covid pandemic? In 2020, who knew that they were voting on who would respond to Russia’s invasion of Ukraine?

The most important issue for the next President could easily be how they address China or AI, because those are clearly huge deals. I won’t vote based on this, because I don’t know who has the better plan for them, because I have no idea what a good plan looks like. Or the most important issue could be something that comes completely out of left field, like Covid did. Not even the very wise can see all ends.

What I do know is that, while much of the Libertarian Party has recently gone from its usual “goofy-crazy” to “mean-crazy“, Chase Oliver is so far the only candidate pandering to me personally. But it’s not too late for other politicians at all levels to try the same.

See you all again next Thursday, by which time the election will, I hope, be over.

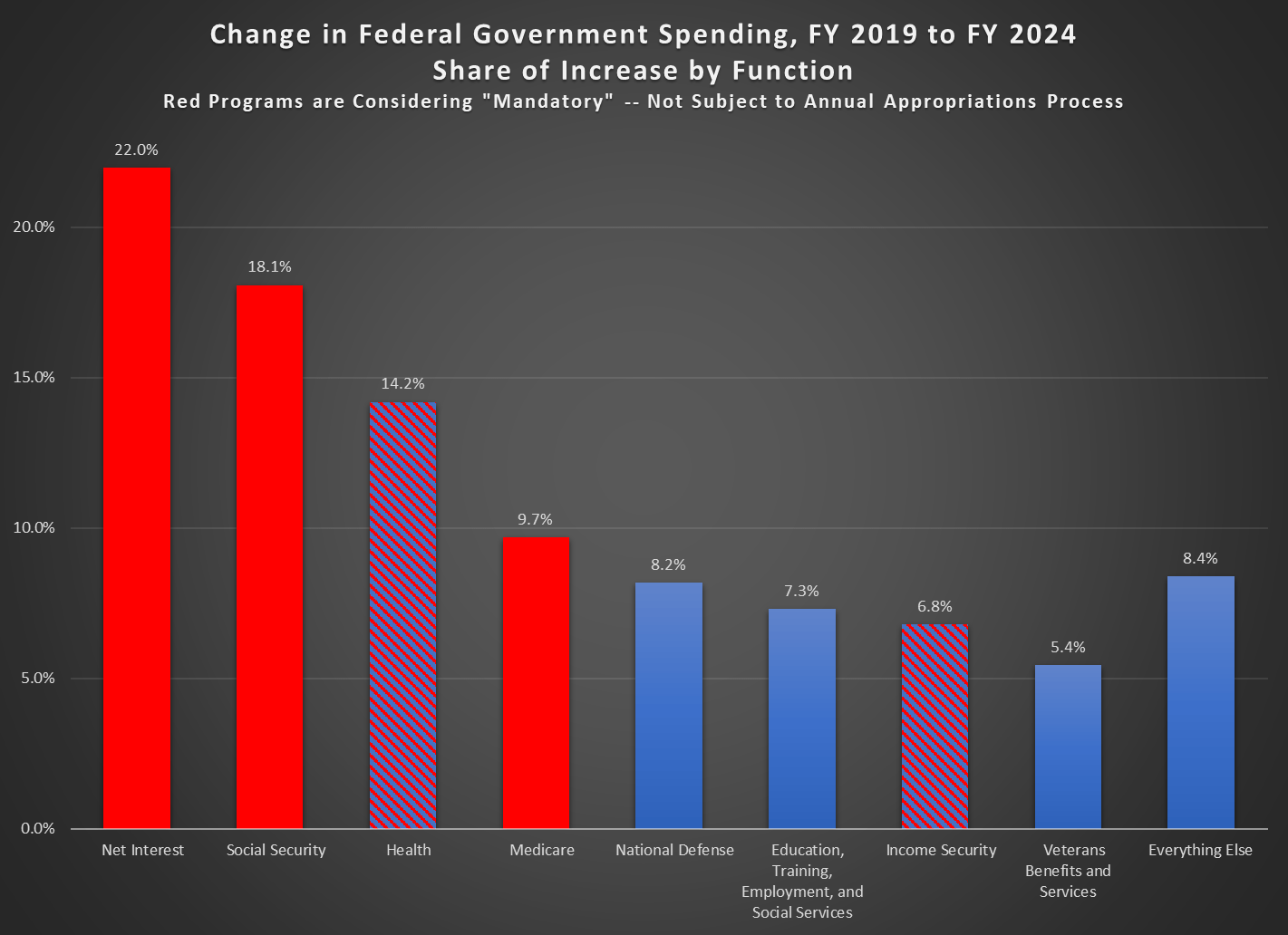

In Fiscal Year 2019, the US federal government spent $4.45 trillion dollars. In Fiscal Year 2024, spending was $6.75 trillion, or an increase of $2.3 trillion dollars. If you adjusted the 2019 number for inflation with the CPI, it would only be about $1 trillion more. Where did that additional $2.3 trillion go?

It will probably not surprise you that most of the increase in spending went to the largest categories of spending. Historically these have been health, Social Security, and defense, but now we must also include interest spending (roughly equal in size to defense and Medicaid in 2024). Indeed, with these areas of spending, 72 percent of the increase is accounted for. Add in the next three functions, and we’ve already accounted for over 90 percent of the increase.

Importantly, most of these categories are outside of the annual federal budget process, meaning that Congress does not need to approve new spending each year (Congress could change them, just as it could change any law, but it’s not part of the annual budgeting process). The “mandatory” categories, as they are called in federal law, are shaded red. I’ve striped with red and blue the health and income security functions, because some of this is subject to the annual budget process, but most of it is not. For example, Medicaid is not subject to the budget process (biggest part of the “health” function) and SNAP is not subject to the budget process (a big part of income security — it is set by the Farm Bill, usually on a five-year cycle).

So, when we talk about the $2 trillion increase since 2019, or the roughly $2 trillion cuts that would be needed to balance the budget, keep in mind that most of this is not subject to the annual budget process. It would require Congress to consider them specifically to enact cuts — though some big categories, such as Social Security, would be automatically cut under current law once their trust funds are exhausted (coming up on about a decade for the Social Security Old-Age Trust Fund).

For many people nowadays, investing in “stocks” means buying a fund like SPY or VOO which tracks the large cap S&P 500 index, or maybe QQQ or QQQM which track the tech-heavy NASDAQ 100 index. These types of funds are exchange-traded funds (ETFs), which very low annual fees (around 0.2% or so). These are so-called passive funds, which mechanically buy and sell stocks such that their holdings match what is in their respective indices. No extra judgment on stock picking is required.

An alternative is to pick stocks yourself, or to buy into a fund with active management, where humans (and their algorithms) try to buy stocks which will beat the passive indices, and try to avoid losing stocks. The active versus passive debate has been going on for decades. There will always be some active funds that outperform in any given year. These successes help keep the allure of active management alive. On average, though, the performance of active funds (before fees) is generally not much different than the passive funds. Thus, with their added fees, the active funds are net losers.

However, there are always cheerful fund managers with a story on how they have a plan to kill it this year, and there are investors willing to buy those stories. Sometimes these fund managers take financial advisors out for expensive lunches, and, behold, said advisors then recommend these actively managed funds to their clients. And so, there are plenty of active funds that still exist. New ones are minted every year, even as some older ones go out of business.

A problem with benchmarking against a cap-weighted fund like SPY or QQQ is that these passive indices are actually very effective. These work as closet momentum-rewarding funds: as the share price of, say, Microsoft goes up and up (presumably because of accelerating earnings), its representation among the biggest 500 companies (by stock capitalization) goes up. Thus, the better, growing companies automatically keep making bigger contributions to the indices, while fading companies sink to lower and lower per cent weighting. That works well to relentlessly home in on the relatively few stocks that account for the gains of the entire market, and to weed down all those other firms, most of which are net losers on stock price over time. This algorithm governing the cap weighted funds is tough for active management to beat.

Having stated these challenges, I’d like to compare performance of some actively-managed funds that have shown enhanced performance in recent years. The problem is, of course, we cannot know if this outperformance will continue. But hopefully looking at performance and discussing the underlying strategies of the funds may help investors decide if they would like to participate in any of them.

Two broad categories of stock funds are growth and value. Growth looks at how fast a firm is increasing revenues, earnings, etc. Most tech stocks command high share prices because of their growth prospects, rather than current earnings (although many of the current big tech leaders generate gobs of cash). Value looks at measures such as price/earnings and price/sales and price/book value, hoping to find undervalued firms whose price does not yet reflect the underlying value. Tech funds are generally under-represented in the value category.

Here we will look at five good actively-managed ETFs, and compare total returns (with dividends reinvested) to the S&P 500 fund SPY. They all claim to incorporate both growth and value into their stock picking. These five funds are:

SPGP – This is a supposed “growth at a reasonable price” fund, which seems to weight value more than growth. In top ten holdings, there is only one tech stock, a 2.7% weighting of Nvidia. There are four petroleum companies, and diverse smattering of other types of firms.

GARP – Another “growth at a reasonable price” (note “G.A.R.P.”) fund. This tilts heavily toward growth: seven of the top ten holdings are tech, with 5.43% Nvidia.

PVAL – As indicated in the name (Putnam Focused Large Cap Value), this is a value fund, but with some growth considerations – – The top ten are: Walmart (retail), Exxon Mobil (petro), Thermo Fisher Scientific, Citigroup, Bank of America (finance), Oracle (tech), UnitedHealth Group (healthcare), Coca-Cola, NXP Semiconductors, and PulteGroup (homebuilder).

MOAT – – “VanEck Morningstar Wide Moat” – This fund seeks to replicate the performance of the Morningstar® Wide Moat Focus Index, which in turn tries to identify a diverse group of U.S. large companies with wide “moats”, that give them sustainable advantages over competitors. Four measures are used to determine a corporation’s dominance: Intangible Assets (brands, patents, proprietary technologies); Switching Costs (inconvenient for the customer to find an alternative); Network Effect (when customers use one service, they adopt additional company services); Cost Advantage.

FFLC – This fund uses “fundamental analysis” and looks for companies that can take advantage of trends in “technological advances, product innovation, economic plans, demographics, social attitudes, and other factors”. An analysis of the fund’s holdings (heavy in big tech; 6% Nvidia) shows a strong focus on growth and momentum, with a moderate value weighting.

All these funds have plausible rationales for choosing the stocks they do. A big question is always: how much of a company’s promise is already reflected in its stock price? If everyone else has already figured out that, say, Microsoft will have high sustained earnings growth, then maybe the current share price is so high that it will not go up any faster than the broad market.

Now for the charts. I will discuss 1-year, 3-year, and 5-year charts, so we can see how the fund strategies worked in different market regimes. The one-year chart covers the raging bull market of the past twelve months, especially in AI-related tech/growth stocks. The 3-year chart encompasses a lengthy bear episode that occupied most of 2022, in reaction to the raising of interest rates to tamp down inflation. The 5-year chart includes the brief but sharp pandemic panic March-April 2020, sandwiched in a huge rise in internet-related big tech stocks 2019-2021.

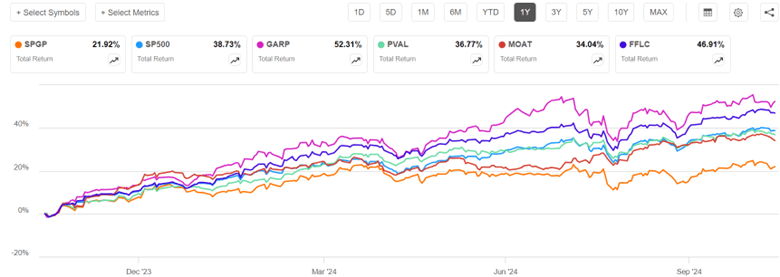

One-Year Chart

Over the past one year, GARP (52% return) soared way above S&P 500 (blue line, 39%), but with high volatility, consistent with its heavy growth/tech exposure. FFLC steadily pulled ahead of SP500 over the past twelve months, racking up a 47% return. PVAL and MOAT finished close to SP500, while tech-poor SPGP flat-lined in the most recent six months and so got left far behind.

Three-Year Chart (End Oct 2021-end Oct 2024)

The defining features of the past three years were a roughly 21% bear market decline in S&P 500 during Jan-Oct 2022, followed by a strong recovery, which was interrupted by a moderate slump July-Oct 2023. FFLC and PVAL performed nearly identically for the first third of this time period (through early March, 2023). They dropped much less than SP500 in 2022, and so by early March, 2023 they were some 15% ahead of SP500. PVAL’s lead over SP500 shrank a bit over the next twelve months, and then widened March-July 2024, to give PVAL (43%) a 16% advantage over SP500 (27%) at the end of three years. FFLC just kept steadily widening its lead over SP500, ending with a 58% return over this three-year time period. MOAT and SPGP also fell less than SP500 in 2022, but fell more than PVAL and FFLC, and they did not keep pace with the tech-led surge in 2023-2024. In the end, MOAT finished essentially even with SPY, and SPGP finished lower (18%). Tech-heavy GARP crashed harder than SP500 in 2022, but more than made up for it with the 2024 tech-fest, finishing well above SP500 and tied with PVAL at 43%.

I won’t show the full five-year chart, since some of the funds did not start prior to that period. But I will make a few semi-quantitative comments. The five-year time period is a little kinder to SPGP – this fund showed a fairly consistent lead over SP500 in 2021 as well as 2022, and so got rave reviews then in the investing literature. It was only in the past six months that it performed so poorly.

FFLC got off to a rocky start, falling about 10% behind SP500 in 2020-2021, although its winning ways since then gave it the overall best 5-year performance. GARP and MOAT pretty much kept pace with SP500 Oct 2019-Oct 2021, so their five-year performance vs SP500 is about the same as for three-year (GARP soundly beat SP500, MOAT roughly tied).

One more chart (below), a five-year comparison of SP500 to FFLC (overall winner among the active funds discussed above) and GARP (tech-heavy) to QQQ (passive, tech-heavy, tracks NASDAQ 100 stocks) and SSO (its stock price moves up and down 2X the daily price movement of S&P500). GARP didn’t start operation till early 2020 (marked by red arrow on chart), to its curve should be shifted up to make a fair comparison with the others; with this correction, it would end up roughly tied with FFLC, with both these funds beating SP500 by about 33% (135% return vs 92%). But even these stellar active funds were soundly beaten by QQQ and even more by the passive 2X fund SSO. Holders of SSO, however, would have suffered heart-stopping drawdowns along the way (e.g. over 50% loss in market value in early 2020).

Readers can draw their own conclusions from this flyover of results. Just like you can fool people some of the time, any active fund may beat “the market” (e.g., S&P 500) some of the time. Some active funds seem to beat the market most of the time. But it is most unlikely that any given fund will beat it all of the time. The S&P 500 algorithm is actually pretty effective. It may behoove the investor to make their own judgement as to what market regime we are in or are about to be in, and to choose active funds which are more likely to thrive in that regime.

I am motivated to include some FFLC (for overall consistent good performance) and PVAL (for a bit of crash protection) in my holdings. But I recognize that their performance could deteriorate in the future, if their investing style no longer works in some new market regime. SPGP is a cautionary example, going from rock star in 2021-2022 to awful in 2024. Even FFLC had an unfavorable first year of operation. The tech giants that dominate QQQ continue to also dominate earnings growth, so QQQ may continue to outpace SP500.

As far as SSO, I earlier wrote on strategies for 2X returns using 2X funds or call options. If you think stocks are going to keep going up, it can make sense to hold these 2X funds. Many advisors, though, recommend against just buy and hold because of the enormous possible losses in a crash; too many investors panic and sell at a low price in that situation. I hold some QLD, which is a 2X QQQ fund, but only as a minor component of my portfolio. Also, if I can overcome fear in the moment, I plan to swap out of plain vanilla stock funds and into a 2X fund like SSO after the next big dip in the market, and then swap back out of SSO after the market recovers.

Disclaimer: Nothing here should be considered advice to buy or sell any security.

It’s spooky season and I just received perhaps the spookiest of student emails. We all know that students never read the syllabus, only want to know what’s on the exam, and can’t be bothered to pay attention. But, and hear me out…what if they are listening?

I got this email yesterday. It might be my favorite student email ever, even if it is direct evidence that my stream of consciousness while lecturing, from the students’ perspectives, must border on surreal at times. I don’t know that much of it is actually funny, but it’s interesting to see what actually sticks in a student’s mind. Notes in curly brackets { } are edits and additions from me, with a few small redactions to ensure the anonymity of the student:

From: {NAME REDACTED}

Halloween is the time to celebrate the spooky things in life, and what is scarier than being perceived? I have taken it upon myself to write down some of the silly things you say in class throughout the month of October to celebrate the scariest time of the year. I have compiled them all here and I think you should be proud of your wit. I think they are funnier without context, so in the spirit of politics, I will be leaving it out.

“I’m just a decomposing corpse here on stage.”

“The good thing about a recession is it’s not a vibes-based measure.”

“[Imagine] You’re wearing a suit, mens or pant….”

“We’re not making assumptions about shapes… yet.”

“Can you imagine the ad campaigns for the eight year old vote?!”

“[In reference to Jesse Ventura, one might even imagine little hearts scribbled in the margins] He’s perfect” {Note: This was not said in admiration of his politics, but rather his existence as Jesse Ventura}

“{Irrelevant 3rd party candidate} is the antichrist, that’s all I know. They kicked my dog and I want to throw them into the 4th layer of hell.”

(with the most deadpan tone and expression) “Yippee, we’re fine, we’re free, we’re great.”

“There’s crooks, and then there’s crooks”

“What I’m saying is, we’re all becoming monsters.” (very on theme to be honest)

“I cannot tell the difference between parody and reality.” (uh oh)

“White gets 1, grey gets 0, and professor Makowsky goes into a quiet rage.”

“Get an amish pretzel with amish butter on it, ya know. Love yourself.”

“Stay away from the swamps, there’s luggage there that wants to eat you.”

The experimental economics world is currently still doing data collection in traditional physical labs with human subjects who show up in person. This is still the gold standard, but it is expensive per observation. Many researchers, including myself, also do projects with subjects that are recruited online because the cost per observation is much lower.

As I remember it, the first platform that got widely used was Mechanical Turk. Prior to 2022, the attitude toward MTurk changed. It became known in the behavioral research community that MTurk had too many bots and bad actors. MTurk had not been designed for researchers, so maybe it’s not surprising that it did not serve our purposes.

The Prolific platform has had a good reputation for a few years. You have to pay to use Prolific but the cost per observation is still much lower than what it costs to use a traditional physical laboratory or to pay Americans to show up for an appointment. Prolific is especially attractive if the experiment is short and does not require a long span of attention from human subjects.

This week at my university the Economics Department Co-hosted an event titled “Interest Rates and Student Loans” with the Office of Financial Aid. I discussed interest rates for a broad audience of young adults. Below is my talk on interest rates.

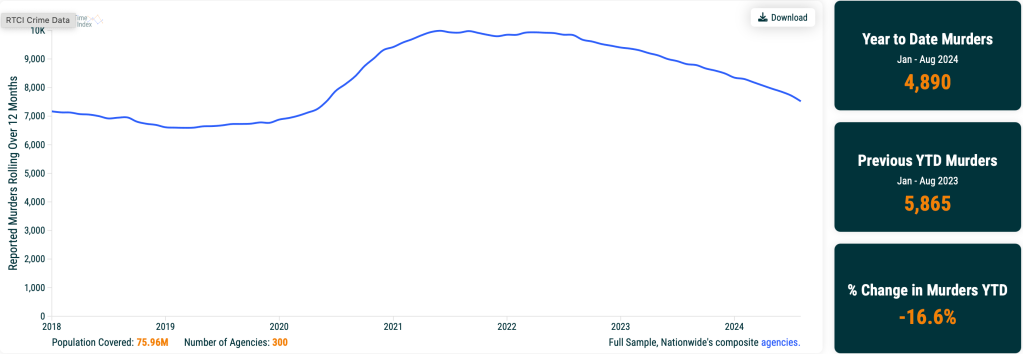

If you want to know how many pigs were killed in the United States yesterday, the USDA has the answer. But if you want to know how many humans were killed in the US this month, the FBI is going to need a year or two to figure it out. The new Real Time Crime Index, though, can tell you much sooner, by putting together the faster local agency reports:

Trends currently look good, though murders still aren’t quite back to pre-2020 levels.

In addition to graphing top-line state and national trends, the Real Time Crime Index also offers the option to download a CSV with city-level data going back to 2018. This seems like a great resource for researchers, worthy of adding to my page of most-improved datasets.

As the presidential race finishes out the last two weeks, it’s clearly a close race. In the past I have recommended prediction markets, and right now these are giving Trump about 60% odds. There have been lately a few big bettors coming into the markets and primarily betting on Trump, so there has been speculation of manipulation, but even at 60-40 the race is pretty close to a toss-up.

Another tool many use to follow the election are prediction models, which usually incorporate polling data plus other information (such as economic conditions or even prediction markets themselves). One of the more well-known prediction models is from Nate Silver, who right now has the race pretty close to 50-50 (Trump is slightly ahead and has been rising recently).

But Silver’s model, and many like it, is likely very complicated and we don’t know what’s actually going into it (mostly polls, and he does tell us the relative importance of each, but the exact model is his trade secret). I think those models are useful and interesting to watch, but I actually prefer a much simpler model: Ray Fair’s President and House Vote-Share Models.

The model is simple and totally transparent. It uses just three variables, all of which come from the BEA GDP report, and focuses on economic growth and inflation (there are some dummy variables for things like incumbency advantage). Ray Fair even gives you a version of the model online, which you can play with yourself. Because the model uses data from the GDP report, we still have one more quarter of data (releasing next week), and there may be revisions to the data. So you can play with it (and one of the variables uses the 3 most recent quarters of growth), but mostly these numbers won’t change very much.