Vice President Vance’s recent trip to Hungary to stump for Viktor Orban was interesting for a number of reasons, but is not totally surprising. In many ways Orban’s “illiberal democracy” (his self-applied term) has many overlaps with MAGA Republican policy. Johan Norberg recently wrote a very good critique of Orban’s policies, and why the US should not follow further down the path or Orbanism.

I agree completely with Norberg’s analysis completely, though his focus is mostly on the decline in democracy, the rule of law, and personal freedoms in Hungary under Orban. Norberg does have several criticisms of Orban’s economic policies, but on the whole economic policy under Orban has been relatively unchanged: in the Human Freedom Index report Norberg cites, the “personal freedom” portion of the index declined 1.5 points on a 10-point scale under Orban, while the “economic freedom” portion only declined by 0.3 points.

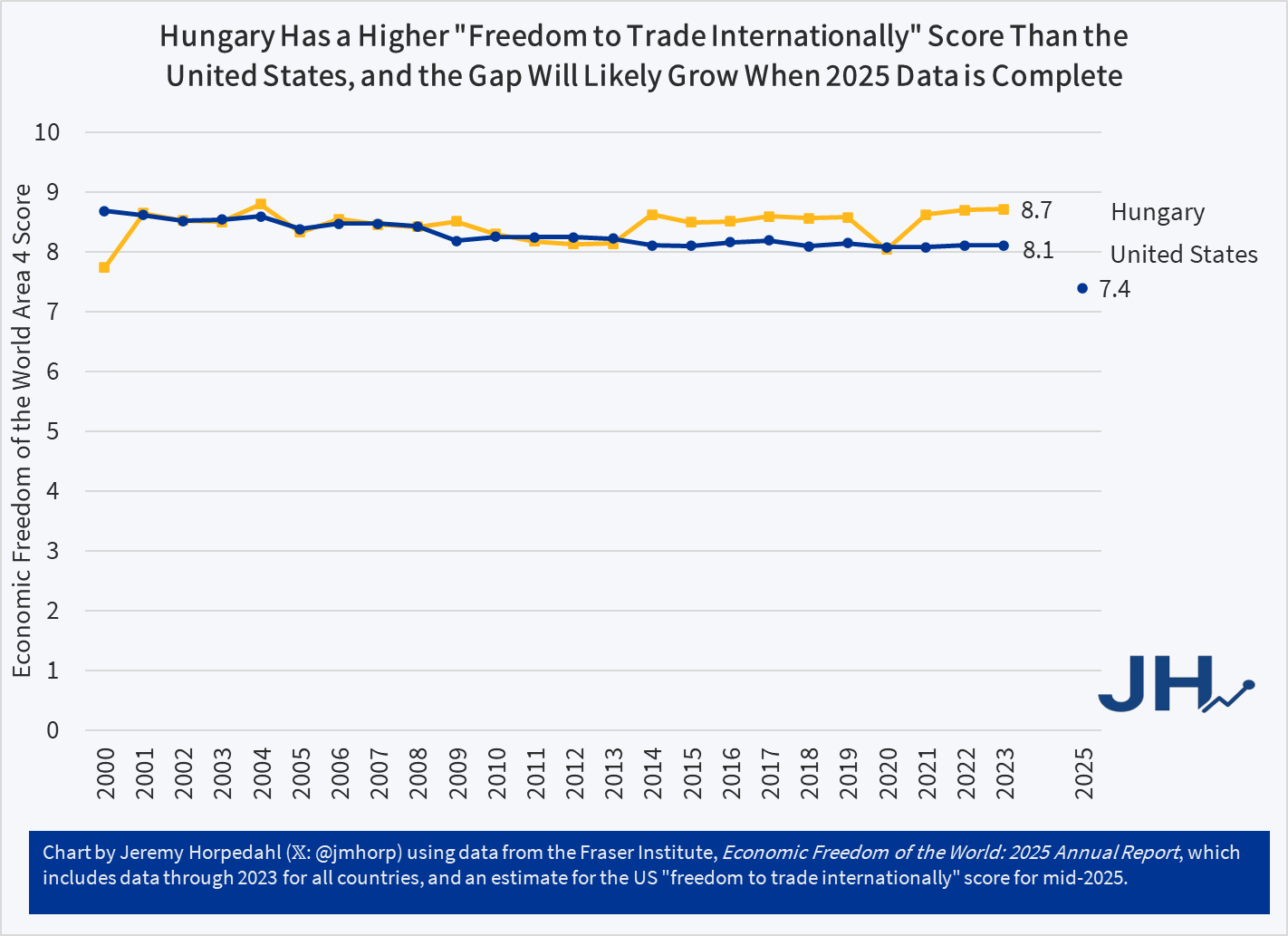

What’s really interesting is that within the Economic Freedom of the World Index, Hungary’s highest scoring area of the five areas is “freedom to trade internationally,” where they ranked the 25th best country in the world in 2023. While MAGA Republicans might like the US to copy many of Hungary’s policies, they clearly do not in this case, as trade restrictions one of the signature economic policies of Trump (possibly his most important economic policy).

To be clear, the high ranking on free trade in Hungary is not due to any conscious policy choice of Orban’s administration. Instead, it is because Hungary is a member of the European Union, and therefore is part of the single market (meaning they have free trade with most of their trading partners) and part of the customs union (meaning they can’t set their own external trade policy). Indeed, it appears if Orban had his way, they would have much less free trade, as he is trying to hold up the EU-Mercosur trade agreement. Nonetheless, Orban’s hands are largely tied on trade policy.

Not only was Hungary ranked quite high on free trade in 2023, they were ranked higher than the US, as they have been for most of the past decade:

While the EFW data is generally only available with a significant lag, and therefore only through 2023 in the chart above, they did provide a special update for the US in mid-2025, given the radical changes in trade policies by the second Trump administration. That’s the blue dot you see floating down below with a score of 7.4. While that isn’t the final ranking for 2025 (they still don’t have the scores for 2024!), it gives an indication of roughly where the US will land in 2025, making it much less free trading than Hungary.

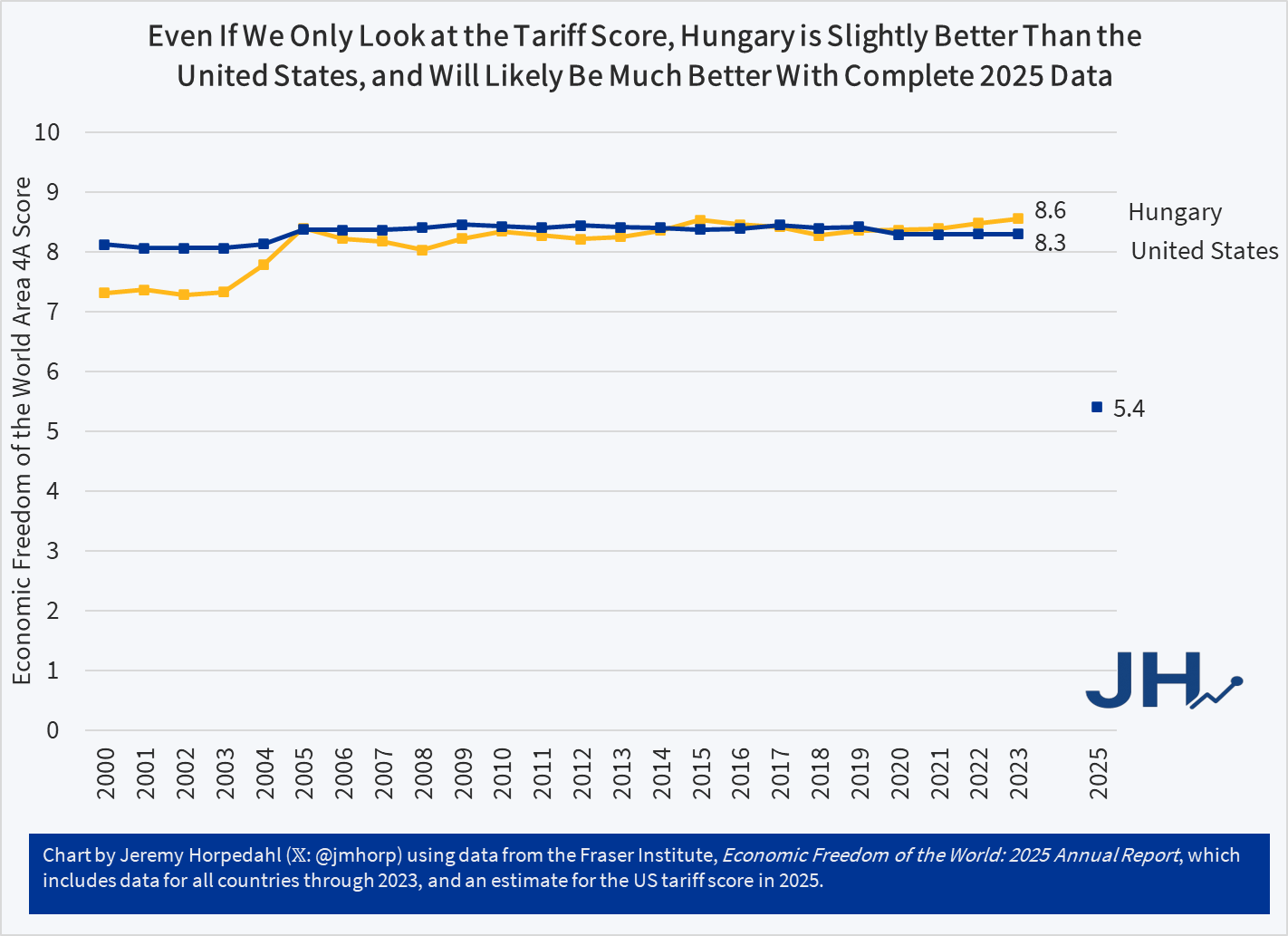

The EFW Area 4 score includes not just tariff rates, but also non-tariff barriers to trade, as well as capital controls and labor movement. What if we only focus on the tariff sub-score, since this is the part of trade policy Trump has altered the most?

On tariff policy alone, there wasn’t much difference between the US and Hungary in 2023 (indeed, if we look solely at tariff rates, the US was slightly better, with an average rate of 3.3% compared with 5.0% in Hungary). But with the radical change in rates in 2025, Fraser estimates that the US will drop significantly, giving it one of the highest average tariff rates in the world. This would be a massive difference between Hungary and the US on trade policy. We’ll have to wait for the complete data before making a final judgement, and indeed given that average tariff rates have changed more than 50 times under the second Trump administration already, it’s not even clear what our score will be for 2025. But it will almost certainly be worse than Hungary.