When I first started reading of “Lender-on-Lender Violence” this year, images of bankers in three-piece suits brawling in the streets of Lower Manhattan came to mind. It turns out that this is a staid legal term for a practice which has been around for some time, but is becoming more common and consequential.

Consider a case where say three lenders (e.g. banks or more likely venture capital funds) have lent money to some startup or struggling company XYZ. Let’s call these lenders A, B, and C. Now XYZ needs even more funding, perhaps because they need to build another factory, or perhaps because things are not working out as they hoped and they cannot pay off the original loans and still stay in business.

Now Lenders A and B get together and cook up a scheme. They will lend some more money to company XYZ to largely replace the original loan, but they contrive to get legal terms for that new loan that give it a higher priority for payment than the original loan. This is called “up-tiering” the new loan. This has the effect of reducing the market value of the original loan.

Lender C is now hosed. It faces murky prospects for repayment on that original loan. Lenders A and B offer to buy them out of the original loan for 40 cents on the dollar. Lender C proceeds to sue Lenders A and B.

Will Lender C prevail? Probably not, if the course of recent cases is any guide. Unless there is very specific language in the legal “covenant” regarding the first loan forbidding this practice, it seems to be legal.

A similar maneuver would be for a new Lender D to offer a replacement loan to Company XYZ, with legal language giving it priority over the original loan. This is called “priming.”

Yet another tactic by the aggressive lenders includes working with Company XYZ to move its more valuable assets into a subsidiary or shell company, and to get the new loan to hold that as collateral. This again hoses the “victim” lenders, since again the assurance that they will be repaid has gone down.

My Personal Experience with Lender-on-Lender Violence

Some years ago, I bought the bonds of a company called SeaDrill. I bought the bonds instead of the common or preferred stock, for an additional margin of safety. Unlike the stock, the bonds must be repaid in full, right? Both the bonds and the preferreds were paying about 9%, back when general interest rates were much lower than that are now. So, I was a lender to the company.

Silly me. Times got tough in the oil patch, and the company would have had difficulty paying off its bonds AND paying its management their high salaries. So, they went for Chapter 11 bankruptcy. I had not realized the difference between Chapter 7 bankruptcy, where the company shuts down and liquidates and pays off its creditors in pecking order, and Chapter 11, which is largely a chance for the company to put the losses on its creditors and to keep on operating.

As with the example above, some big institution offered to refinance things with new secured bonds that had priority ahead of the old bonds (which I held). In the end I got about 44 cents on the dollar for my bonds. I was not happy about that, but I did make out better than the hapless preferred stockholders, who got just a tiny crumb to make them go away. It was a learning experience. I did feel, well, violated.

Implications for the Burgeoning Private Credit Market

I will be writing more on the booming “private credit” market. Many of the loans in this space are “covenant-lite.” Back before say 2008, a large fraction of loans to business were through banks, who would insist on strong legal protection for their money. But in recent years, private equity funds have competed for this lending, allowing the borrowers to borrow on terms that give much less protection to the lenders. Cov-lite is now the norm.

Traditionally, loans (as distinct from bonds) to businesses have enjoyed decent recoveries (e.g., around 70%) in case of defaults, thanks to strong collateral backing the loans. But if we face any sort of prolonged recession and elevated defaults, the recoveries on all these loans will be far less than in the past. These are uncharted waters.

Morgan Housel’s Psychology of Money is not much like other personal finance books. Rather than making recommendations about exactly what to do and how to do it, Housel tells stories about how people’s different attitudes toward money serve them well or poorly. His stance is that most people already know what they should do, so he doesn’t need to explain that, but instead needs to explain why people so often don’t do what they know they should (e.g. save more). The book is not only pleasant to read, but at least for me exerts a calming effect I definitely do not normally associate with the finance genre, as if the subtext of “just be chill, be patient, follow the plan and everything will be alright” is continually seeping into my brain. Some highlights:

The idea of retirement is fairly new. Labor force participation for men over 65 is only about 20% today, but was well over 50% prior to the introduction of Social Security. Even once it started, Social Security paid in real terms about a quarter of what it does today. Plus pensions weren’t as common as people think; as of 1975 only a quarter of those over 65 had pensions, and most of those didn’t pay much. The 401k didn’t exist until 1978; the Roth IRA until 1998. “It should surprise no one that many of us are bad at saving and investing for retirement. We’re not crazy. We’re all just newbies.”

If you are disappointed whenever the price of your stocks goes down, you are in for a bad time, though you will do well if you can just ignore it:

“Netflix stock returned more than 35,000% from 2002 to 2018, but traded below its previous all-time high on 94% of days. Monster Beverage returned 319,000% from 1995 to 2018- among the highest returns in history- but traded below its previous high 95% of the time during that period…. this is the price of market returns.”

Housel isn’t very prescriptive because he recognizes how much people differ: “I can’t tell you what to do with your money, because I don’t know you. I don’t know what you want. I don’t know when you want it. I don’t know why you want it.”

At the end explains what he does with his own money: “Effectively all of our net worth is a house, a checking account, and some Vanguard index funds.” He convincingly argues that his way isn’t for everyone; he paid off his house early but “I don’t try to defend this decision to those pointing out its flaws, or to those who would never do the same. On paper it’s defenseless. But it works for us. We like it. That’s what matters.”

The closest he gets to specific recommendation is “for most investors, dollar-cost averaging into a low-cost index fund will provide the highest odds of long-term success.” There are lots of more general recommendations about good mindsets to take, for instance:

The few people who know the details of our finances ask, ‘What are you saving for? A house? A boat? A new car?’ No, none of those. I’m saving for a world where curveballs are more common than we expect.

Overall this is an easy book to recommend- it is both pleasant and easy to read, and gives good advice. My main complaint is that it is short on the nuts and bolts of how you actually do this stuff; for someone who doesn’t already know, it would pair well with a book that is stronger on that front, like I Will Teach You to Be Rich.

Economics as a discipline really likes to boil things down to their essentials. There are plenty of examples. How many goods can one consume? Just two, bread and not bread. How can you spend your time? You can labor or leisure. How do you spend your money? Consume or save. It’s this last one that I want to emphasize here.

First, all income ultimately ends up being spent on consumption. Saving today is just the decision to consume in the future. And if not by you, then by your heirs. One determinant of inter-temporal consumption decisions is the real rate of return. That is, how many apples can you eat in the future by forgoing an apple eaten today? The bigger that number is, the more attractive the decision to save.

Further, since most saving is not in the form of cash and is instead invested in productive assets, we can also characterize the intertemporal consumption problem as the current budget allocation decision to consume or invest. The more attractive capital becomes, the more one is willing to invest rather than consume. The relative attractiveness between consumption and investment informs the consumption decision.

How attractive is investment? I’ll illustrate in two graphs. First, if the price of investment goods falls relative to consumption goods, then individuals will invest more. The graph below charts the price ratio of investment goods to consumption goods. Relative to consumption, the price of investment has fallen since 1980. Saving for the future has never been cheaper!

Of course, as in a price taker story, I am assuming that individuals don’t affect this price ratio. Truly, prices are endogenous to consumption/investment decisions. For all we know, it may be that the prices of investment goods are falling because demand for investment goods has fallen. But that doesn’t appear to be the case.

I’m back from Manifest, a conference on prediction markets, forecasting, and the future. It was an incredible chance to hear from many of my favorite writers on the internet, along with the CEOs of most major prediction markets; in Steve Hsu’s words, Woodstock for Nerds. Some highlights:

Robin Hanson took over my session on academic research on prediction markets (in a good way; once he was there everyone just wanted to ask him questions). He thinks the biggest current question for the field is to figure out why is the demand for prediction markets so low. What are the different types of demand, and which is most likely to scale? In a different talk, Robin says that we need to either turn the ship of world culture, or get off in lifeboats, before falling fertility in a global monoculture wrecks it.

Play-money prediction markets were surprisingly effective relative to real-money ones in the 2022 midterms. Stephen Grugett, co-founder of Manifold (the play-money prediction market that put on the conference), admitted that success in one election could simply be a coincidence. He himself was surprised by how well they did in the 2022 midterms, and said he lost a bunch of mana on bets assuming that Polymarket was more accurate.

Substack CEO Chris Best: No one wants to pay money for internet writing in the abstract, but everyone wants to pay their favorite writer. For me, that was Scott Alexander. We are trying to copy Twitter a bit. Wants to move into improving scientific publishing. I asked about the prospects of ending the feud with Elon; Best says Substack links aren’t treated much worse than any other links on X anymore.

Razib Khan explained the strings he had to pull for his son to be the first to get a whole genome sequence in utero back in 2014- ask the hospital to do a regular genetic test, ask them for the sample, get a journalist to tweet at them when they say no, get his PI’s lab to run the sample. He thinks crispr companies could be at the nadir of the hype cycle (good time to invest?).

Kalshi cofounder Luana Lopes Lara says they are considering paying interest on long term markets, and offering margin. There is enough money in it now that their top 10 or so traders are full time (earning enough that they don’t need a job). The CFTC has approved everything we send them except for once (elections). We don’t think their current rule banning contest markets will go through, but if it does we would have to take down Oscar and Grammy markets. When we get tired of the CFTC, we joke that we should self certify shallot futures markets (toeing the line of the forbidden onion futures). Planning to expand to Europe via brokerages. Added bounty program to find rules problems. Launching 30-50 markets per week now (seems like a good opportunity, these can’t all be efficient right?).

There was lots else of interest, but to keep things short I’ll just say it was way more fun and informative doing yet another academic conference, where I’ve hit diminishing returns. More highlights from Theo Jaffee here; I also loved economist Scott Sumner’s take on a similar conference at the same venue in Berkeley:

If you spend a fair bit of time surrounded by people in this sector, you begin to think that San Francisco is the only city that matters; everywhere else is just a backwater. There’s a sense that the world we live in today will soon come to an end, replaced by either a better world or human extinction. It’s the Bay Area’s world, we just live in it.

Financial markets have sustained themselves for nearly two years now on the hope that within 1-2 quarters, the Fed will finally relent and start lowering interest rates. This hope gets dashed again and again by data showing stubbornly persistent high employment, high GDP growth, and high inflation, but the hope refuses to die.

Long-term interest rates had been falling nicely for the last month, based on expectations of rate cuts in the fall. Then came Friday’s jobs report, and, blam, up went 10-year rates again. The Bureau of Labor Statistics (BLS) published its “Establishment” survey of data gleaned from employers. Non-farm payrolls rose by US 272k. This was appreciably higher than the 180k consensus expectation.

The plot below indicates that this number fits into a trend of essentially steady, fairly high employment gains (suggesting ongoing inflationary pressures):

There are fundamental reasons to take the BLS Establishment figures with a grain of salt. They have a history of significant revisions some months after first publication. Also, BLS uses a “birth/death” model for small businesses, which can account for some 50% (!) of the job gains they report. [1]

Another factor is that all of the net “jobs” created in recent quarters are reported to be part-time. According to Bret Jensen at Seeking Alpha, “Part-time jobs rose 286,000 during the quarter, while full-time jobs fell by just over 600,000. This is a continuation of a concerning trend where over the past year, roughly 1.5 million part-time positions were created while approximately one million full-time jobs were lost. This difference is that the BLS survey does not account for people working two or three jobs, which are now at a record as many Americans have struggled to maintain their standard of living during the inflationary environment of the past couple of years.”

It seems, then, that this week’s huge “jobs added” figure is not to be taken as indicating that the economy is overheated. However, it is still warm enough that rate cuts will be postponed yet again. A different BLS survey (“Household”) showed unemployment creeping up from 4.0% to 4.1%, which again suggests a more or less steady and fairly robust employment picture.

As far as drivers of inflation, I would look especially at wage growth. That is fitfully slowing, but not nearly enough to get us to the Fed’s 2% annual inflation target. My sense is that ongoing enormous federal deficit spending will keep pumping money into the economy fast enough to keep inflation high. High inflation will prevent significant interest rate cuts, assuming the Fed remains responsible. The interest payments on the federal debt will balloon due to the high rates, leading to even more deficit spending. If we actually get an economic downturn, leading to job insecurity and a willingness of workers to accept slower wage growth in the private sector, the federal spending floodgates will open even wider.

This makes hard assets like gold look attractive, to hedge against inflating U.S. dollars. This is one reason China has been quietly selling off its dollar hoard, and buying gold instead.

[1] For more in-depth treatments of employment statistics, see posts by fellow blogger Jeremy Horpedahl, e.g. here.

You know how perfect diversification means that one bears no idiosyncratic risk? That means that one is willing to pay more for some given return, driving up the price of assets included in such a diversified portfolio. That means that, without an informational advantage, index funds should place upward pressure on the price of assets that compose them. Anyone who invests in individual stocks, again without an informational advantage, would be priced out of the market because they bear idiosyncratic risk and would need to enjoy a risk premium that lowers the maximum price that they are willing to pay.

The Red lobster restaurant chain has historically positioned itself in what was hopefully a sweet spot between slow, expensive, full-service restaurants, and cheaper fast-food establishments. With its economies of scale, the Red Lobster franchise could engage in national advertising and improved supply contracts, giving it an advantage over small family-owned local restaurants.

The firm has been struggling for a number of years, caught between the quasi-upscaling of many fast-food chains, and the rise of fast-casual competitors like Chipotle. Also, seafood is more expensive to procure compared to chicken and beef, and the pandemic made a long-lasting dent in their revenues. That said, Red Lobster has been viable business for decades.

However, the firm has been adversely affected by financial engineering by outside companies. General Mills spun off Red Lobster to a company called Darden Restaurants in 1995. In 2014 Darden sold Red Lobster to a private equity firm called Golden Gate Capital for $2.5 billion. Golden Gate promptly plundered Red Lobster by selling its real estate out from under it. Instead of owning their own land and buildings, now the restaurants had to pay rent to landlords. This put a permanent hurt on the restaurant chain’s profits. After this bit of financial engineering, the private equity firm in 2019 sold a 49% stake to a company called Thai Union. Thai Union bought out the rest of Red Lobster ownership from Golden Gate in 2020.

The Iron Fist from Outside

Thai Union is a huge seafood producer, which operates massive shrimp farms in Southeast Asia and sells a lot of shrimp to Red Lobster. Although Thai Union initially said they would not interfere in the operations of Red Lobster, that’s not how it panned out.

An article by CNN author Nathaniel Meyersohn details how Thai Union took effective control of red lobster management decisions by 2022. Given the restaurant chain’s poor financial performance, it’s understandable that Thai Union would want to shake things up, but unfortunately the hatchet men they brought in appeared to have done more harm than good. Numerous off the record conversations agreed that the outside CEO was unnecessarily rude as well as incompetent. Knowledgeable Red Lobster veterans were driven out, and morale plummeted. Per Meyersohn:

Thai Union’s damaging decisions drove the pioneering chain’s fall, according to 13 former Red Lobster executives and senior leaders in various areas of the business as well as analysts. All but two of the former Red Lobster employees spoke to CNN under the condition of anonymity because of either non-disclosure agreements with Thai Union; fear that speaking out would harm their careers; or because they don’t want to jeopardize deferred compensation from Red Lobster…

Former Red Lobster employees say that while the pandemic, inflation and rent costs impacted Red Lobster, Thai Union’s ineptitude was the pivotal factor in Red Lobster’s decline.

“It was miserable working there for the last year and a half I was there,” said Les Foreman, a West Coast division vice president who worked at Red Lobster for 20 years and was fired in 2022. “They didn’t have any idea about running a restaurant company in the United States.”

At Red Lobster headquarters, employees prided themselves on a fiercely loyal culture and low turnover. Some employees had been with the chain for 30 and 40 years. But as Thai Union installed executives at the chain, dozens of veteran Red Lobster leaders with deep knowledge of the brand and restaurant industry were fired or resigned in rapid succession. Red Lobster ended up having five CEOs in five years…

Former Red Lobster employees describe a toxic and demoralizing environment as Thai Union-appointed executives descended on headquarters and interim CEO Paul Kenny eventually took over the chain in 2022. Kenny, an Australian-born former CEO of Minor Food, one of Asia’s largest casual dining and quick-service restaurants, was part of the Thai Union-led investor group that acquired Red Lobster.

Kenny criticized Red Lobster employees at meetings and made derogatory comments about them, according to former Red Lobster leaders who worked closely with Kenny…

At the direction of Thai Union, Kenny became interim CEO, according to Red Lobster’s bankruptcy filing.

In the months after Kenny took over, Valade’s leadership team and other veteran leaders left. In July of 2022, the chief operations officer and six vice presidents of operations overseeing restaurants were abruptly fired shortly before Red Lobster’s annual general manager conference.

Kenny appointed a Thai Union frozen seafood manager, Trin Tapanya, as Red Lobster’s chief operations officer overseeing restaurants. Tapanya had no experience running restaurants. He did not respond to CNN’s requests for comment.

Other Thai Union representatives also became more closely involved across Red Lobster’s supply chain, finance, operations and strategy teams…Thai Union took a larger role in Red Lobster’s supply chain decisions, despite pledges in 2020 that it would not interfere.

Red Lobster had spent decades developing a wide array of suppliers to buy at competitive prices and mitigate the risks of becoming too reliant on any single supplier.

Thai Union blew that up.

Red Lobster employees say they were pressured by Thai Union representatives to buy more seafood from Thai Union. Thai Union representatives also began sitting in on meetings between Red Lobster and seafood suppliers, said one of the former Red Lobster employees who witnessed these conversations. Thai Union was the direct competitor of these other seafood suppliers, and suddenly had intimate access to their products, prices and strategy. “Our suppliers were really upset that [Thai Union representatives] were in those meetings with them,” this person said.

Red Lobster now claims that Thai Union pushed out other shrimp suppliers, “leaving Thai Union with an exclusive deal that led to higher costs to Red Lobster”.

The “Endless Shrimp” Disaster The final blow to Red Lobster was offering an every-day special of all the shrimp you can eat. The firm had historically offered occasional all you can eat specials, to draw in first-time customers. But they had learned from a disastrous extended all you can eat crab special back in 2003, that if you are not very careful, you can lose a ton of money letting people eat all they want of an expensive food item.

Apparently, Thai Union pressured Red Lobster into offering an every-day “Endless Shrimp” special starting in June, 2023. Old guard Red Lobster management tried to push back, but were overruled. For Thai Union, this was of course a chance to sell more shrimp. But it led to huge losses on the part of Red Lobster. Internet personalities boosted their viewings by wolfing down plate after plate after plate of expensive shrimp:

The deal quickly went viral on social media. People started posting videos on Tik Tok showing how many shrimp they could eat. It became something of a challenge where people would try to eat as many shrimp as possible to gain social media clout. For example, a YouTuber called The Notorious Bob ate 31 plates of shrimp. Each plate has six shrimp so he ate 186 shrimp in total … another YouTuber called Sir Yacht stayed at Red Lobster for 10 hours and ate 200 shrimps throughout the day.

Red Lobster has now filed for Chapter 11 bankruptcy protection from its creditors, while it further downsizes to try to stay afloat. Thai Union has written down its investment in Red Lobster to the tune of $540 million, and its creditors now own the company.

The various actors in our current financial system played their usual roles here: General Mills spun off a non-core business; a private equity firm plundered its acquisition and then dumped it, presumably making gobs of money in the process for its partners; a supplier acquired a downstream company to develop a more integrated business line; a venerable American brand simply lost ground (think: Sears) in the competitive market place as tastes and competition changed over time, with vicious cost-cutting unable to save it.

This story is somewhat tragic, but I’m not sure there are any real villains, apart from the obnoxious outside CEO. Thai Union is a powerhouse seafood supplier, but they simply did not understand the American restaurant business and could not come up with a viable plan to fix Red Lobster. The now-unemployed restaurant workers may be victims, but the cooks and wait staff and store managers who worked extra hard, short-handed to keep serving their customers well despite horrible upper management – – to me, those are the heroes here.

Supporters of prediction markets tend to emphasize how they are great tools for aggregating information to produce accurate forecasts. If you want to know e.g. who is likely to win the next election, you can watch every poll and listen to pundits for hours, or you can take ten seconds to check the odds. This is great for people who want information- but how do prediction markets fare as investments for their actual participants?

Zero Sum

The big problem with prediction markets as investments is that they are zero sum (or negative sum once fees are factored in). You can’t make money except by taking it from the person on the other side of the bet. This is different from stocks and bonds, where you can win just by buying and holding a diversified portfolio. Buy a bunch of random stocks, and on average you will earn about 7% per year. Buy into a bunch of random prediction markets, and on average you will earn 0% at best (less if there are fees or slippage).

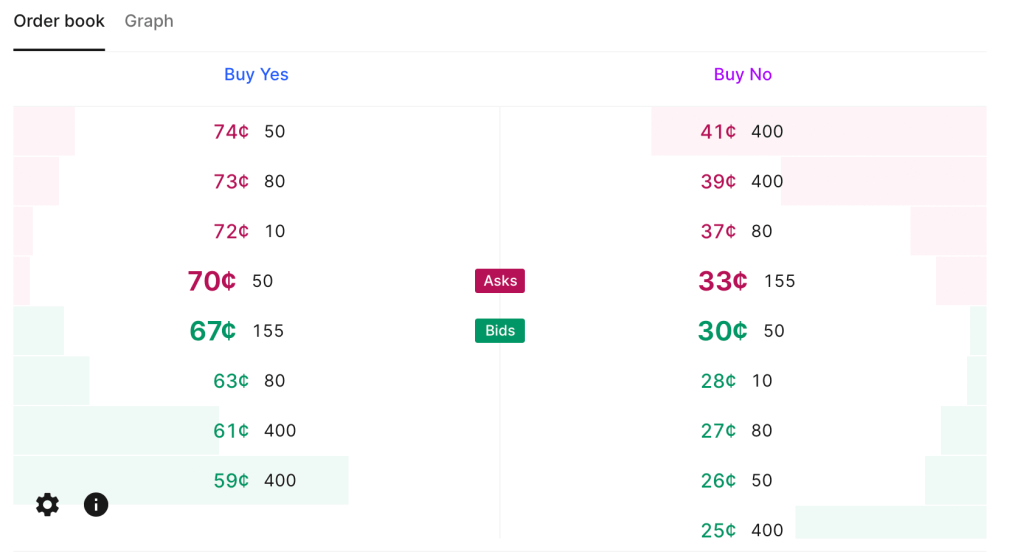

Low Liquidity

Current Kalshi order book for “Will June 2024 be the hottest June ever“. Betting $200 on either outcome could move the price by 5 cents (so move the estimated probability by 5pp).

This zero sum problem is close to inevitable based on how prediction markets work. They currently have one other big problem, though it is not inevitable, and is getting better as they grow: liquidity. There are some stocks and bonds where big institutions can buy or sell millions of dollars worth without moving the price. But in markets like Kalshi or PredictIt, I personally move prices often by betting just hundreds, or sometimes even just tens, of dollars. Buying at scale means getting worse prices, if you can even buy at all. PredictIt has a bet limit of $850 per contract for regulatory reasons. This definitely excludes institutional investors, but even for individuals it can mean many markets aren’t worthwhile. Say an outcome is already priced at 90 cents, the most you can make by betting it happens is about $94. That’s not nothing but its also not enough to incentivize lots of in-depth research, especially given the risk of losing the $850 if you are wrong and the opportunity cost of investing the money in stocks or bonds. Kalshi in theory allows bets up to $25k, but most of their markets haven’t had the liquidity to absorb a bet anywhere near that (though this could be changing).

Easy Alpha

Given these negatives, why would anyone want to participate in prediction markets, except to gamble or to generously donate their time to create information for everyone else? Probably because they think they can beat the market. Compared to the stock market, this is a fairly realistic goal. Perhaps because the low liquidity keeps out institutional investors, it isn’t that hard for a smart and informed investor to find mispricings or even pure arbitrages in prediction markets. This seems to be especially true with political prediction markets, where people often make bets because they personally like or dislike a candidate, rather than based on their actual chances of winning; that is exactly the kind of counterparty I want to be trading with.

I’ve been on PredictIt since 2018 and earned a 16% total return after fees; this was on hundreds of separate trades so I think it is mostly skill, not luck. Of course, even with this alpha, 16% total (not annual) return over 6 years is not great compared to stocks. On the other hand, I tended to put money in right before big elections and take it out after, so the money is mostly not tied up in PredictIt the whole time; the actual IRR is significantly better, though harder to calculate. On the other other hand, the actual dollar amount I made is probably not great compared to the time I put in. On yet another hand, the time isn’t a big deal if you are already following the subject (e.g the election) anyway.

Uncorrelated Alpha

The other big positive about prediction markets is that there is no reason to expect your returns there are correlated with your returns in traditional markets. Institutional investors are often looking for investments that can do well when stocks are down, and are willing to sacrifice some expected returns to get it. In fact, there may be ways to get a negative correlation between your prediction market returns and your other returns, hedging by betting on outcomes that would otherwise harm you. For instance, you can hedge against inflation by betting it will rise, or hedge against a recession by betting one happens. If you are right, you make some money by winning the bet; if you are wrong, you lose money on the bet but your other investments are probably doing well in the low-inflation no-recession environment.

Going Forward

Prediction markets have long been in a regulatory grey area in the US, but with the emergence of Kalshi and the current CFTC, everything may soon be black and white. Kalshi has won full approval from the CFTC for a variety of markets, but the CFTC is moving to completely ban betting on elections (you can comment on their proposal here until July 9th).

One great place to discuss the future of prediction markets will be Manifest, a conference hosted by play-money market Manifold in Berkeley, CA June 7-9th. It features the founders of most major US predictions markets and many of the bestwriters on prediction markets. I’ll be there, and as I write tickets are still available.

I ran across an article by Lyn Schwartzer on seeking Alpha last week, which I thought was insightful regarding investments. Here is my summary.

The article is Most Investments Are Bad. Here’s Why, And What To Do About It. The article’s first bullet point is “Historical data shows that the majority of investments, including bonds, stocks, and real estate, perform poorly.” Unpacking this, looking at various investment classes:

Bonds and Stocks

Investment-grade bonds typically pay interest rates just a little above inflation, so it’s not surprising that they have been mediocre investments over the long-term. The prices of long bonds (10 years or more maturity) tended to rise between about 1985 and 2020, as interest rates came steadily down, but that tailwind is pretty much over.

It has been known for years, e.g. from a study by Hendrik Bessembinder, that only a tiny fraction of stocks makes up the vast majority of returns in equity markets. I wrote about this a couple of years ago on this blog.:

The rise of the S&P is entirely due to huge gains by a tiny subset of stocks. The average stock actually loses money over both short and long time periods. … half of the U.S. stock market wealth creation [1926-2015] had come from a mere 0.33% of the listed companies… Out of some 26,000 listed companies, 86 of them (0.33%) provided 50% of the aggregate wealth creation, and the top 983 companies (4%) accounted for the full 100%. That means the other 25,000 companies netted out to zero return. Some gave positive returns, while most were net losers.

As investors, we of course want to know how to lock in on those few stocks that will perform well. I see two approaches here, not mentioned in the article. One is to be very good at analyzing the finances and market environments of companies, to be able to pick individual firms which will be able to grow their profits. Being lucky here probably helps, as well. An easier and very effective method is to simply invest in the S&P 500 index funds like SPY or VOO. Because these funds are weighted by stock capitalization, they inexorably increase their weighting of the more successful companies and dial down the unsuccessful companies. This dumb, automatic selection process is so effective that it is very difficult for any active stock-picking fund manager to beat the S&P 500 for any length of time.

What the article suggests in this regard is to focus on businesses that have “durable competitive advantages (network effects, powerful brands, intangible property, economies of scale, oligopoly participation, and so forth),” or to try to pick up decent/mediocre companies at a low price.

The big tech companies which are mainly listed on the NASDAQ exchange have these durable advantages, and indeed the QQQ fund which is comprised of the hundred largest stocks on the NASDAQ has far outpaced the broader-based S&P 500 fund over the last 10 or 20 years.

Real Estate

All of us suburbanites know that owning your own home has been one of the best investments you can make, over the past few decades. The article points out, however, that real estate in general has not been such a great performer. If your property is not located close to a thriving metropolitan area, where people want to live, it can be a dog. The article cites abandoned properties all around Detroit (“large once-expensive homes that are now rotting on parcels of land that nobody wants”), and notes, “In Japan, there are millions of abandoned countryside homes that are nearly free. Many of them are in beautiful and safe rural areas, and yet there is insufficient demand for them.”

And so, “Most real estate falls somewhere between those extremes. It performs decently, especially when considering that it can replace the owner’s rental income or be rented out for cashflows, but after maintenance and taxes are considered, its unlevered total return from price appreciation and cashflow generation net of maintenance leaves something to be desired relative to gold.”

Gold As a Reference

The article uses gold as, well, the gold standard of investing returns. The supply of gold creeps up roughly 1.5% per year, so after say 95 years there is four times as much physical gold as before. We find that an ounce of gold will buy more food or more manufactured goods than it did a century ago, but that is because our efficiency of producing such things has increased faster than the gold supply. On the other hand, “All government bonds have underperformed gold over the long run, and most unlevered real estate has underperformed gold as well.” Stocks in the broad U.S. market (most foreign stock markets did more poorly) greatly outperformed gold, but that is only accomplished by the top 4% of stocks. The other 96% of stocks as group did not generate any excess returns.

Owner-Operators versus Passive Investors

I am looking at these issues from the point of view of a passive investor – I have some extra cash that I want to plow into some investment, and have it return my original capital plus another say 10%/year, without me having to do extra work. It turns out that many companies, especially smaller ones, provide useful products to customers and they make enough profit to pay off the owner/operators and the employees, but not enough to reward outside passive investors, too. These companies serve an important role in society, but are not viable investment vehicles:

Being an owner-operator of a business, or a worker at a business, makes a lot of sense. However, the vast majority of businesses are not strong enough to provide good returns for outside passive investors after all expenses (including salaries) are considered.

Good returns for outside passive investors are reserved for only the best types of companies; companies that are so dominant and high-margin that even after paying all of their executives and workers, they have plenty of excess profits for outside passive investors. Although stocks from any sector can have these characteristics, Bessembinder’s research found that major outperformers were disproportionally concentrated in the technology, telecommunications, energy, and healthcare/pharmaceutical sectors. They are on the right side of an emerging tech trend, they have network effects, they have economies of scale, they have protected intangible property such as patents, or they are part of an oligopoly, and so forth.

Similarly, real estate (especially unlevered), works most easily when it is occupied or used by the owner. After all, you must live somewhere. Now, you can make money buying and renting/flipping properties, but that typically demands work on your part. You add value by fixing the tenant’s toilet or arranging for a plumber, or by scoping the market and identifying a promising property to buy, and by working to upgrade its kitchen. All this effort is not the same as just throwing money at some building as a passive investor, and walking away for five years.

Upping Returns via Leverage

This is a packed sentence: “Historically, a key way to turn mediocre investments into good investments has been to apply leverage. That’s not a recommendation; that’s a historical analysis, and it comes with survivorship bias.”

For example, banks have historically borrowed money (e.g. from their depositors) at lowish, short-term rates, and combined a lot of those funds with the bank corporate equity, to purchase and hold longer-term bonds that pay slightly higher rates. Banks are often levered (assets vs. equity) 10:1. This technique allows them to earn much higher returns on their equity than if they used their equity alone to buy bonds.

It is easy to leverage real estate. If you put 20% down and borrow the rest, bam, you are levered 5:1. Now if the value of your house goes up 6%/year while you are only paying 3% on your mortgage, the return on the actual cash (the 20% down) you put in becomes quite juicy: “After maintenance and recurring taxes, the majority of unlevered real estate, even when rented out for cashflows, doesn’t outperform gold. But unlike gold, 5-to-1 leverage makes real estate actually pretty good in many contexts, and historically allows it to outperform gold.”

Large corporations can leverage up by issuing relatively low-interest bonds: “They can borrow large amounts of money for decades at low interest rates, and use that capital to organically expand their business, buy smaller companies, or buy back their own shares. Either way, they are borrowing abundant fiat currency at low rates and using that capital to build or buy business equity, and they are arbitraging that spread for shareholders.”

Savvy firms like Warren Buffett’s Berkshire Hathaway take it a step further, by having controlling interests in insurance companies, and investing the low-cost “float” funds, as we described here. From the article:

Berkshire has also made a habit out of buying small and medium sized private businesses in full. Many of these smaller companies would have higher borrowing costs if they were independent. But Berkshire can buy a lot of them, and then issue corporate debt at the parent company level at much lower interest rates than any of them could issue on their own. So he can buy a lot of unlevered cashflow-producing small or medium-sized businesses, and turn them into a portfolio of businesses that are levered with Berkshire’s very low cost of capital.

Now other companies like Ares Management and Apollo are jumping onto this arbitrage bandwagon, buying up insurance companies to get access to their captive cash, to be used for investing.

Here is another rough example of the power of leverage. The unleveraged fund BKLN holds bank loans, and so does the closed end fund VVR. But VVR borrows money to add to the shareholders’ equity. There is more complication (discount to net asset value) with VVR which we will not go into, but the following 5-year chart of total returns (share price plus reinvested dividends) shows nearly triple the return for VVR, albeit with higher volatility:

The Changing Global Economic Landscape

The article closes with some summary observations and recommendations. The past 30-40 years have been marked by ever-decreasing interest rates, and by cooperation among nations and generally increasing globalization. It seems that these trends have broken and so what worked for the last four decades (buy stocks, shun gold) may not be as good going forward:

For equity and real estate investors, the key takeaways from this piece are 1) do not extrapolate the prior decades for a given investment and instead assess it with this context in mind, 2) try to emphasize the sectors [such as Big Tech] that Bessembinder identified as ones that disproportionally generate excess returns, and 3) look for companies that have locked in or are otherwise still able to play this arbitrage game going forward in a more difficult environment for it.

Additionally, hard monies [i.e. gold, silver] become a serious alternative once again in this context, and are worth serious consideration for a portfolio slice, because the hurdle rate for stocks to outperform them is high when there are not a lot of tailwinds at the backs of stocks.

I was writing up something for my graduating seniors about how to keep learning economics after school, and realized I might as well share it with everyone. This may not be the best way to do things, it is simply what I do, and I think it works reasonably well.

Blogs by Economists: There are many good ones, but besides ours Marginal Revolution is the only one where I aim to read every post

Podcasts on the Economy: NPR’s The Indicator (short, makes abstract concepts concrete), Bloomberg’s Odd Lots (deeper dives on subjects that move financial markets)

Podcasts by Economists: Conversations with Tyler and Econtalk (note that both often cover topics well outside of economics). Macro Musings goes the other way and stays super focused on monetary policy.

Twitter/X: This is a double-edged sword, or perhaps even a ring of power that grants the wearer great abilities even as it corrupts them. The fastest way to get informed or misinformed and angry, depending on who you follow and how you process information. Following the people I do gives you a fighting chance, but even this no guarantee; even assuming you totally trust my judgement, sometimes I follow people because they are a great source on one issue, even though I think they are wrong on lots of other things. Still, by revealed preference, I spend more time reading here than other single source.

Finance/Investing: Making this its own category because it isn’t exactly economics. Matt Levine has a column that somehow makes finance consistently interesting and often funny; unlike the rest of Bloomberg, you can subscribe for free. He also now has a podcast. If you’d like to run money yourself some day, try Meb Faber’s podcast. If you’d like things that touch on finance and economics but with more of a grounding in real-world business, try the Invest Like the Best podcast or The Diff newsletter.

Economics Papers: You can get a weekly e-mail of the new papers in each field you like from NBER. But most econ papers these days are tough to read even for someone with an undergrad econ degree (often even for PhDs). The big exception is the Journal of Economic Perspectives, which puts in a big effort to make its papers actually readable.

Books: This would have to be its own post, as there are too many specific ones to recommend, and I don’t know that I have any general principle of how to choose.

This is a lot and it would be crazy to just read all the same things I do, but I hope you will look into the things you haven’t heard of, and perhaps find one or two you think are worth sticking with. Also happy to hear your suggestions of what I’m missing.