Partly this has been a regulatory issue. Raising equity adds all sorts of legal burdens. Traditionally businesses could only accept equity investments from accredited investors and a small number of friends and family unless they did a full IPO and became public (hard enough that there are less that 5000 public companies in the US out of millions of businesses). This changed with the JOBS Act of 2012, which allowed small businesses to raise money from large numbers of non-accredited investors without having to register with the SEC.

Following the JOBS Act, equity crowdfunding sites like WeFunder emerged to match new businesses with potential investors. But equity crowdfunding has taken off relatively slowly:

Its seen more success recently with some additional regulatory relief and the overall market boom of 2020-2021. But at ~$400 million/yr, its still well under 1% of all venture investment (~$300 billon/yr), which is itself tiny relative to the public stock market ($40 trillion market cap).

Why has equity crowdfunding been slow to take off? Partly its new and most people still don’t know about it. Partly early-stage companies aren’t a good way for most people to invest a significant fraction of their money; you probably want to be at least close to accredited investor levels (~$300k/yr income or $1 million liquid wealth) for it to make sense, and those at the accredited investor level already have other options. WeFunder is up front about the risks:

The other issue here is with asymmetric information and adverse selection. Its hard to find out much information about early-stage companies to know if they are a good investment; part of the point of the JOBS Act is that the companies don’t need to tell you much. The companies themselves have a better idea of how well they are doing, and the best ones might not bother with equity crowdfunding; they could probably raise more money with less hassle by going to venture funds or accredited angel investors.

I’ve long thought this adverse selection would be the killer issue, but my impression (not particularly well-informed and definitely not investment advice) is that there are now quality companies raising money this way, or at least companies that could easily raise money elsewhere. WeFunder has a whole page of Y-Combinator-backed companies raising money there. This week Substack, an established company that has already raised lots of venture funding, offered crowd equity and reached the $5 million limit of how much they could legally accept in a single day.

Overall I think this model is working well enough that I’m no longer in a hurry to become an accredited investor. Accredited investors have many more options for companies they can invest in and aren’t subject to the $2,200/yr limit on how much they can invest in early-stage companies. But even if I completed the backdoor process of getting accredited without being rich, I wouldn’t want to put more than $2,200/yr into early-stage companies until I was a millionaire, at which point I’d be accredited the usual way. And while most companies aren’t raising crowd equity, enough are that there seem to me to be no shortage of choices.

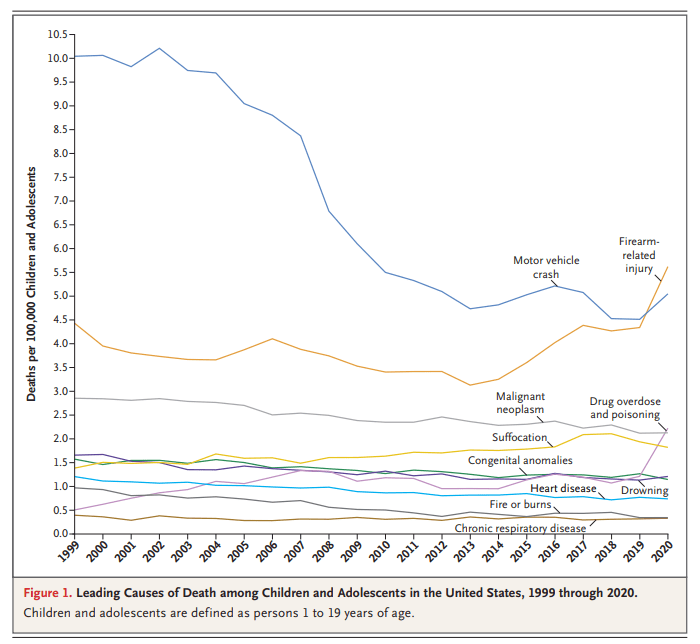

You might have seen this chart recently. It comes from a letter published in the New England Journal of Medicine in April 2022. The data comes directly from the CDC. It shows the leading causes of death for children in the US. You will notice that firearm-related deaths have been rising for much of the past decade, and in 2020 eclipsed car accidents as the leading cause.

Many are sharing this chart in response to the recent elementary school shooting in Nashville. It’s natural to want to study these problems more in the wake of tragedies. After the Uvalde shooting last year, I tried to read as much as I could about the history of homicide and gun violence in the US, and to look at the research on what might work to reduce gun violence, which is summarized in a post I wrote last June.

That being said, I don’t think the chart above accurately characterizes the problem of elementary school shootings. It might accurately describe some broader problem, but it’s misleading with respect to the shooting we all just witnessed. The most important reason is that the definition of “children” here extends to 18- and 19-year-olds. Much of the gun-related homicides for “children” shown here are gang-related violence, not random school shootings at elementary schools. It’s not that we shouldn’t care about these deaths too — we very much should care — but the causes and solutions are entirely different from elementary school mass shootings.

It has been a tumultuous several weeks in the world of finance. Just when “soft landing” (i.e., the notion that Fed rate hikes would tame inflation without causing a nasty recession) was the meme, a string of banks went belly-up. We summarized the history and status of this dismal parade of corpses a week ago.

On Friday, Germany’s Deutsche Bank (DB) was added to the list of endangered financial species. Its share price plunged as the cost of insuring its credit swaps soared, a sign of lack of confidence in DB among other financial parties. As best I can discern, however, DB is a relatively poorly-managed bank, but not one teetering on insolvency like Credit Suisse or the smaller American banks that have collapsed.

Silicon Valley Bank Getting Sold Off, Finally

On this side of the pond, the big news is that Silicon Valley Bank (SVB), whose spectacular implosion was really what brought “crisis” to banking, will be taken over by another regional bank, First Citizens Bank of North Carolina. The first attempt to auction off SVB was a fizzle, so the feds tried again. They really, really wanted to get this kind of full takeover deal done (rather than breaking up SVB and selling off bits piecemeal), so First Citizens was able to drive a juicy bargain. First Citizens was a fairly modest-sized bank, about half the size of SVB at the end of last year. First Citizens will get SVB assets of $110 billion, deposits of $56 billion and loans of $72 billion, and will start operating the SVB branch offices again. They will pay only $55 billion for the nominal $72 billion in loans that SVB had made, a 29% mark-down. The cost to the FDIC for this deal is about $20 billion. (I don’t know how First Citizens is paying for this acquisition). First Citizens stock skyrocketed on this news, so the market sees this as a sweet deal for First Citizens.

Going forward, the FIDC has pledged to share any losses (or gains) on those loans in the future, which offers further protection to First Citizens. FDIC gets shares of First Citizens valued up to $500 million. First Citizens decided not to take an additional $90 billion in securities that the FDIC will now have to sell on its own. These are likely the long-term bonds which sunk SVB when their value cratered with rising interest rates this past year. I’m not sure how much further losses the FDIC will bear on these bonds.

Anyway, so far, so good, kind of; it is sobering to note that this $20 billion cost to the FDIC just chewed up 1/6 of its total $128 billion kitty for backstopping all qualifying deposits at all banks in America. So we can’t readily afford too many more meltdowns of this magnitude.

Bank Deposits Continue to Flee, But Slower

A worrisome trend in the past month or so has been for depositors to pull their funds from bank checking/savings accounts, and stash their money instead in higher yielding money market funds or CDs or Treasury bills. Banks have borrowed records amounts from the Fed in recent weeks, in order to have lots of cash on hand if they have to pay off departing clients. And within the banking system, about half a trillion dollars has been moved from smaller regional banks to large banks.

I can’t find the reference now, but in the past two days I read an article stating that rate of deposit withdrawals is slowing down, and will likely not of itself destabilize the system. I’m going with that narrative, for now.

An indirect fallout from all this bank turmoil is the reduced inclination of banks to extend loans to businesses. This will make for a slowdown in economic activity, which should cool off inflation – -which is exactly what Jay Powell was hoping would be the outcome of the Fed rate hikes.

The marketfor the assassination of John Wick has absolutely failed, at least through three films. Lots of people want him dead. They keep sending people to kill him. Those people keep getting killed. Why?

John Wick 4 is in theatres now, I enjoyed it thoroughly, this discussion will have no spoilers. The question I want to ask is: how is this character still alive to inhabit a fourth film? Is he immortal? Some sort of demon or demi-god? No.

John Wick survived three films because the market for assassination is run by a oligopsonistic cartel (“The High Table”) with extreme price-setting power. And that cartel is simply not willing to pay the necessary price. John Wick lives because the High Table is a bunch of penny-pinching cheapskates.

Point of fact: trying to kill John Wick is dangerous. Everyone who tries to dies. Through the first three films he has killed 114 people. If you want someone to take on a dangerous job, you have to pay them accordingly. In economics we refer to this as compensating wage differentials. Killing John Wick is more than just dangerous, however. It’s also a tournament. It’s an open contract and only one person, the successful assassin, receives payment. So you, the would-be assassin who is considering entering this market, has to consider both the probability of success and the probability of your own death. The two are, of course, also inextricably related. So how much do you value your own life?

The value of statistical life in 2016 was somewhere around $9.6 million dollars. Updating that into 2023 dollars based on nothing but inflation pushes us to about $12 million. If we are to assume that the 115th person actually is successful in their task (which is a pretty heroic assumption considering the low probability that John Wick dies in the first 5 minutes of a nearly 3 hour 4th film), the you should expect that a less than 1% chance of success and that in your failure you will also lose your life. The appropriate compensating wage differentials should in turn be in the neighborhood of $1.38 billion.

That’s just the additional compensation on top of the standard wages that clear the market for individuals with the kind of skill set and, ahem, demeanor necessary to enter the high end assassin labor market. The market clearing price in question is likely closer to $1.5 billion. By the end of John Wick 3, the bounty on his head reaches a paltry $14 million, which is tells you all you need to know about the High Table. They just don’t get the economics of the situation they are in. You can’t treat killing John Wick like a standard labor market transaction for the same reason you can’t pay uniform wages for cleaning windows. Sometimes you need the first floor cleaned. Sometimes the 80th floor. Sometimes the inside of the windows. Sometimes the outside.

John Wick 4 is in theaters because The High Table ignored the first rule of economics. You get what you pay for.

It’s unusual for the expert opinions on an issue to range all the way from zero to 100%.

Economists using an instrumental variable approach found that digital piracy did not hurt record sales in the 2000’s. Hammond (2014) found, incredibly, that file-sharing increased record sales. The picture above is of an article critiquing the Oberholzer-Gee and Strumpf (2007) conclusion that was published by a top journal.

Liebowitz reports that music industry professionals believed that digital piracy was the primary or complete cause of the decline of record sales. One would think that industry insiders have accurate data on the problem and a decent mental model relating the variables together.

The estimated effect of music file-sharing ranged from helping music sales to completely eliminating them. Where else can we find so much disagreement on the answer to a narrow empirical question?

Between 1850 and 1910, most US censuses asked whether an individual was deaf. There were four alternative descriptions among the combinations of deafness and dumbness. Seems straightforward enough. The problem is that these aren’t discrete categories, they’re continuous. That is, one’s ability to hear can be zero, very good, bad, or just middling. What constitutes the threshold for deafness? In practice, it was the discretion of the enumerator. Understandably, there was a lot of variation in judgement from one enumerator to another. A lot of older people were categorized as deaf, even if they had some hearing loss.

I recently bought a used desktop computer for what seemed like next to nothing. $240 for a machine more powerful than my much-more-expensive 2019 MacBook Pro, most notably due to its 32GB of RAM. Desktops have always been cheaper than equivalently powerful laptops, Windows computers cheaper than Macs, and used computers cheaper than new, so this isn’t totally shocking. But the extent of the difference still surprised me. For instance, buying a new desktop from Dell with similar specs to the used one I just got would cost $1399.

So why is the used discount so big right now? My guess is that its one more knock-on effect of work-from-home. Remote work has been the most persistent change from Covid, and there’s been a huge decline in the demand for office space, with occupancy rates still half of pre-Covid levels.

This means that offices are on sale relative to their pre-Covid prices. Office REITs are down 37% over the past year even after the Covid-induced drop of the previous two years. So it makes sense that all sorts of office equipment is on sale too. Offices tend to be full of employer-owned desktop computers, but when employees work from home they typically use their own machine or a company laptop. That means less demand for office desktops going forward, and a big overhang of existing office desktops that are being under-used. Employers realizing this may just sell them off cheap. Several things about the refurbished desktop I bought, such as its Windows Pro software, indicate that it used to be in an office.

Recently I was watching a lecture by historian Marcus Witcher which addressed the treatment of African Americans in the Jim Crow era. Witcher mentioned the “pig laws,” which were severe legal punishments given to Blacks in the South for what used to be petty crimes. Such as stealing a pig. He mentioned that the fines could be anywhere from $100 to $500, and then he asked me directly: how much is $100 adjusted for inflation today?

My initial, immediate answer was about $3,000. That turns out to be almost exactly correct for around 1880. But the more I thought about it, the more I realized that this wasn’t a satisfactory answer. We were trying to put $100 from a distant past year in context to understand how much of a burden this was for African Americans at the time. Does knowing that adjusted for inflation it’s about $3,000 give us much context?

So much has been happening in the banking world it is a little hard to keep track of it. See recent articles here by fellow bloggers Mike Makowsky, Jeremy Horpedahl, and Joy Buchanan. Here is a quick guide to all the drama.

Credit Suisse Takeover by UBS

Perhaps the biggest, newest news is a shotgun wedding between the two biggest Swiss banks announced over the weekend. Credit Suisse is a huge, globally significant bank that has suffered from just awful management over the last decade. Its missteps are a tale in itself. Its collapse would be an enormous hit to the Swiss financial mystique, and would tend to destabilize the larger western financial system. So the Swiss government strong-armed a takeover of Credit Suisse by the other Swiss bank behemoth, UBS, in an all-stock transaction. The government is providing some funding, and some guarantees against losses and liability. An unusual aspect of this deal is that Credit Suisse shareholders will get some value for their stock, but a whole class of Credit Suisse bonds Is being written down to zero. Usually bond holders have strong priority over stockholders, so this may make it more difficult for banks to sell unsecured bonds hereafter.

Silicon Valley Bank Collapse: Depositors Protected

The Silicon Valley Bank (SVB) collapse is old news by now. The mismanagement there is another cautionary tale: despite having a flighty tech/venture capital deposit base, management greedily reached for an extra 0.5% or so yield by putting assets into longer-term bonds that were vulnerable to a rise in interest rates instead of into stable short-term securities.

A key step back from the brink here was the feds coming to the rescue of depositors, brushing aside the existing $250,000 limit on FDIC guarantees. That was an important step, otherwise large depositors would stampede out of all the regional banks and take their funds to the few large banks that are in the too-big-to-fail category. It is true that this new level of guarantee encourages more moral hazard, since depositors can now be more careless, but the alternative to guaranteeing these deposits (i.e. the collapse of regional banks) was just too awful. Bank shareholders and most bondholders were wiped out. Presumably that will send a message to the investing community of the importance of risk management at banks.

The actual disposition of the business parts of SVB are still being worked out. The feds originally tapped the big, well capitalized banks to see if one of them would take over SVB as a going concern. That would have been a nice, clean, thorough resolution. But the big banks all declined. I suspect the actual responses in private were unprintable. Here’s why: in the 2008 banking crisis, the Obama-Biden administration went to the big banks and encouraged them to take over failing institutions like Countrywide Mortgage, who among other things had made arguably predatory loans to subprime borrowers who had poor prospects to keep up with the mortgage payments. The Obama administration’s Department of Justice promptly turned around and very aggressively prosecuted these big banks for the sins of the prior institutions. J. P. Morgan ended up paying something like 13 billion and Bank of America paid 17 billion. So when today’s Biden administration reached out to these big banks this month to see about taking over SVB, they got no takers.

Now the assets of SVB (renamed Silicon Valley Bridge Bank) are getting auctioned off, perhaps piecemeal, but how exactly that happens does not seem so critical.

Signature Bank: Shut Down, But Sold Off Intact

Crypto-friendly Signature Bank was shuttered by New York State officials on Sunday, March 12, making this the third largest (SVB was the second largest) bank failure in U.S. history. Forbes gives the whole story. At the end of last year, Signature had over $110 billion in assets and $88 billion in deposits. Spooked by Signature’s similarities to failed banks SVB and Silvergate, customers rushed to withdraw deposits, which the bank could not honor without selling securities at huge losses. As with SVB, the feds had the FDIC insure all deposits of all sizes at Signature.

Unlike SVB, Signature has received a bid for the whole business, from New York Community Bancorp’s subsidiary Flagstar Bank. Flagstar will take over most deposits and loans and other assets, and operate Signature Bank’s 40 branches.

First Republic: Teetering on The Brink, Propped Up by Banking Consortium

First Republic is in a somewhat different class than these other troubled institutions. Its overall practices seem reasonable, in terms of equity and assets. However, it caters to a wealthy clientele in the Bay Area, with a lot of accounts over the $250,000 threshold. In the absence of a rapid and decisive move by Congress to extend FDIC protection to all deposits at all banks, somehow (I haven’t tracked what started the stampede) depositors got to withdrawing huge amounts (like $70 billion) last week. This was a classic “run on the bank.” That would stress any bank, despite decent risk management. Once confidence is lost, it’s game over, since there are always alternative places to park one’s money. Ratings agencies downgraded First Republic to junk status, and the stock has cratered.

It is in the interest of the broader banking industry to forestall yet another collapse. If folks start to generally mistrust banks and withdraw deposits en masse, our whole financial system will be in deep trouble. In the case of First Republic, the private sector is trying to prop up it up, without a government takeover. So far this has mainly taken the form of depositing some $30 billion into First Republic, as deposits (not loans or equity), by a consortium of eleven large U.S. banks led by J. P. Morgan. This is was a quick and fairly unheroic intervention, since in the event of liquidation, depositors (including this consortium) have the highest claim on assets. This intervention will probably prove insufficient. Two potential outcomes would be a big issuance of stock to raise capital (which would dilute existing shareholders), or some large bank buying First Republic. The stock rose today on reports that Morgan’s Jamie Dimon was talking with other big banks about taking an equity stake in First Republic, possibly by converting some of the $30 billion deposit into equity.

Old News: Silvergate Bank Liquidation

Overshadowed by recent, bigger collapses, the orderly shutdown of the crypto-focused Silvergate Bank is old news. It was two weeks ago (March 8) that Silvergate announced it would shut down and self-liquidate. The meltdown of the crypto financing world led to excessive loss of deposits at Silvergate. Unlike SVB and Signature, it held a lot of its assets in more liquid, short-term securities, so its losses have not been as devastating – – all depositors will be made whole, though shareholders are toast (stock is down from $150 a year ago to $1.68 at Monday’s close).

Warren Buffett To the Rescue?

Banks generally operate on the model of borrow short/lend long: they “borrow” from depositors and buy longer-term securities. Normally, short-term rates are lower than long-term rates, so banks can pay out much lower interest on their deposits than they receive on their bond/loan investments. With the Fed’s rapid increases in short-term rates this past year, however, the rate curve is heavily inverted, which is disastrous for borrow short/lend long. Fortunately for banks, many depositors are too lazy to do what I have done, which is to move most of my immediate-need money out of bank accounts (paying maybe 1%) and into T-bills and money market funds paying 4-5%.

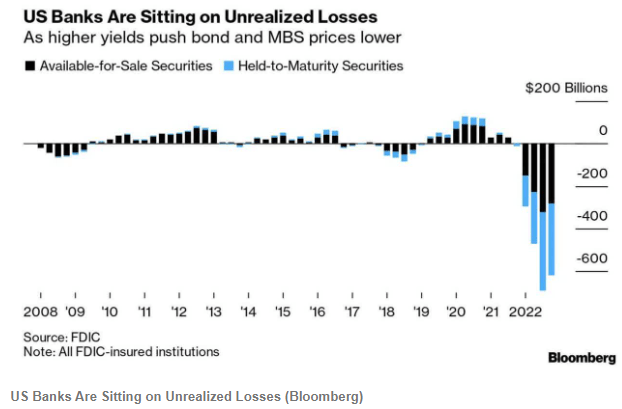

All this churn goes to highlight an inherent fragility of banks: there is typically a maturity mismatch between a bank’s deposits/liabilities (which are short-term and can be withdrawn at any time) and its assets (longer-term bonds it purchases, and loans that it makes which can be difficult to quickly liquidate). Runs on banks, where if you were late to panic you lost all your deposited money, used to be a real feature of life, as dramatized in classic films Mary Poppins and It’s a Wonderful Life. Eliminating this danger was a key reason for setting up the Federal Reserve system, and in general that has worked pretty well in the past hundred years. Banks in general (see chart above) are now carrying enormous amounts of unrealized losses on their portfolios of bonds and mortgage-backed securities (MBS) due to the increase in market rates. In addition to the existing “discount window” at which banks can borrow, the Fed has set up a new lending facility to help tide banks over if they (as in the case of SVB and Signature) get stressed by having to sell marked-down securities to cover withdrawal of deposits. Also, new measures reminiscent of 2008 were announced to extend dollar liquidity to central banks of other nations.

But when Gotham really has a problem, the Commissioner calls in the Caped Crusader. Warren Buffett has been in touch with administration officials about the banking situation. We wrote two weeks ago about Warren Buffett’s gigantic cash hoard from the float of his Berkshire Hathaway insurance businesses which allows him to quickly make deals that most other institutions cannot. Buffett rode to the rescue of large banks like Bank of America and Goldman Sachs in the 2008-2009 financial crisis. A lot of corporate jets have been noted flying into Omaha from airports near the headquarters of various regional banks. Buffett’s typical playbook in these cases is to have the troubled institution issue a special class of high yielding (with today’s regional banks, think: 9%) preferred stock that he buys, perhaps with privileges to convert into the common stock. That stock would count as much needed equity in the banks’ books.

There’s no getting around the fact, however, that I remain pretty rationally ignorant of what’s happening in my neighborhood. This stands despite my being both a local homeowner and an economist who is intellectually invested in the idea that obstacles to housing construction are a major cause of a wide variety of social ills. The reason for my ignorance remains the same as most peoples: I’m busy.

Many cities have blogs and subreddits that one can follow to keep abreast of local policy. What I really need, though, is a paid liason who’s entire job is to absorb and distill all of these political currents into a single information digest consumable as a quarterly email. Decent chance there are at least 100 homeowners in my area who would pay for such a service. Should you offer such a service?

No, you should not. Why? Because you’d be rendered obsolete within a two years because I’m pretty sure I’m going to be able have a large language model produce exactly that email for me, probably for free.

Everyone keeps looking for “the big use case” for AI and LLMs. Allow me to suggest instead that the big use case is in fact thousands of micro use cases, those tasks for whom we could all use a 3-5 hours per year personal assistant, but such a relationship simply isn’t a net gain given the fixed costs of a retaining an assistant. Some of the big use cases for early AI’s will, in this sense, be similar to Uber or Airbnb: they reduce the fixed costs and transaction costs of personal services.

For me, one of those first personal services provided by Chat GPT or it’s closest rival may simply be telling me who to vote for:

“I am a X year old homeowner in zip code XXXXX. I am single/married with X children of ages [X….X]. I earned X dollars last year. What should I vote for and against in the upcoming election on November 11th?”