This post illustrates a couple of things that I learned this year with an application in finance. I learned about the simplex when I was researching amino acids. I learned some nitty-gritty about portfolio theory. These combined with my pre-existing knowledge about game theory and mixed strategy solutions.

Specifically, I learned a way of visualizing all possible portfolio returns. This post narrowly focuses on 3 so that I can draw a picture. But the idea generalizes to many assets.

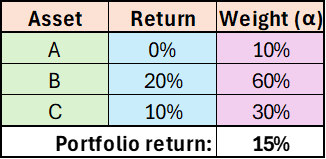

Say that I can choose to hold some combination of 3 assets (A, B, & C), each with unique returns of 0%, 20%, and 10%. Obviously, I can maximize my portfolio return by investing all of my value in asset B. But, of course, we rarely know our returns ex ante. So, we take a shot and create the portfolio reflected in the below table. Our ex post performance turns out to be a return of 15%.

That’s great! We feel good and successful. We clearly know what we’re doing and we’re ripe to take on the world of global finance. Hopefully, you suspect that something is amiss. It can’t be this straightforward. And it isn’t. At the very least, we need to know not just what our return was, but also what it could have been. Famously, a monkey throwing darts can choose stocks well. So, how did our portfolio perform relative to the luck of a random draw? Let’s ignore volatility or assume that it’s uncorrelated and equal among the assets.

Visualizing Success with Two Assets

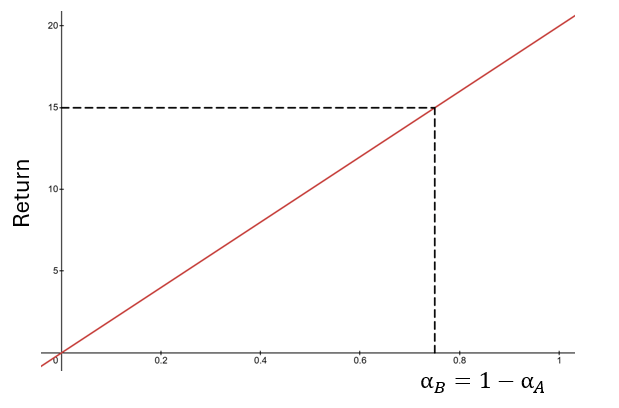

Say that we had only invested in assets A and B. We can visualize the weights and returns easily. The more weight we place on asset A, the closer our return would have been to zero. The more weight that we place on asset B, the closer our return would have been to 20%.

If we had invested 75% of our value in asset B and 25% in A, then we would have achieved the same return of 15%. In this two-asset case, it is clear to see that a return of 15% is better than the return earned by 75% of the possible portfolios. After all, possible weights are measures on the x-axis line, and the leftward 75% of that line would have earned lower returns. Another way of saying the same thing is: “Choosing randomly, there was only a 25% that we could have earned a return greater than 15%.”

Merry Christmas! I’m gifting you a couple ideas for money things to do in the remaining six days of 2025.

Ways to Help Yourself

Money in US Flexible Spending Accounts (FSAs) often disappears if not requested by New Year’s Day. Don’t forget to draw these down- especially it is a Dependent Care FSA, which can’t carry any money over to the new year. The money goes back to your employer if you don’t spend it, which means they don’t have an incentive to remind you themselves; so I’ll remind you to save you from having to go Krieger.

The next few days are also your last chance to do most tax-deductible spending in 2025, which could be business expenses, or contributing to tax-deductible accounts that don’t expire like a 401k or HSA (not FSA). See a more detailed list of tax ideas here. Depending on your situation (especially whether you itemize), this might also be a good time to make tax-deductible donations, which would:

Help Others

There are many good causes to donate to, but funding high-value low-cost health interventions in poor countries was probably the cheapest reliable way to save a life even before this year. When one of the largest funders of global health, USAID, was shut down this year, the marginal benefit of donations to global health likely went even higher. Givewell does the cost-effectiveness calculations to identify good options for specific charities in this area, like Helen Keller International. I like that I’ve been donating to these charities for years via Givewell’s donation portal and none of them have ever called me (since they don’t require a phone number) or mailed me anything.

This picture shows all the remains of the website of USAID, an agency that spent $32 billion in FY 2024

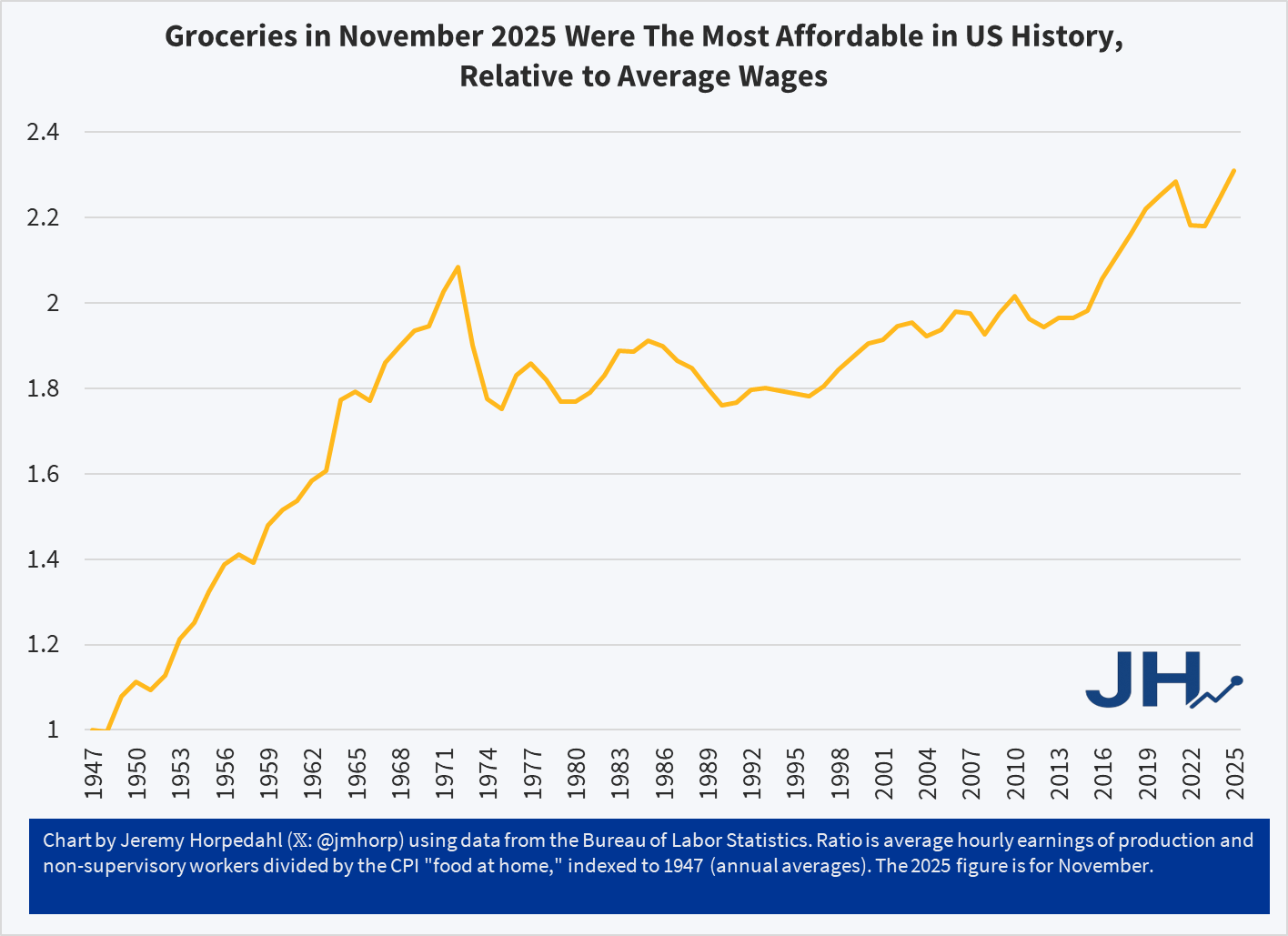

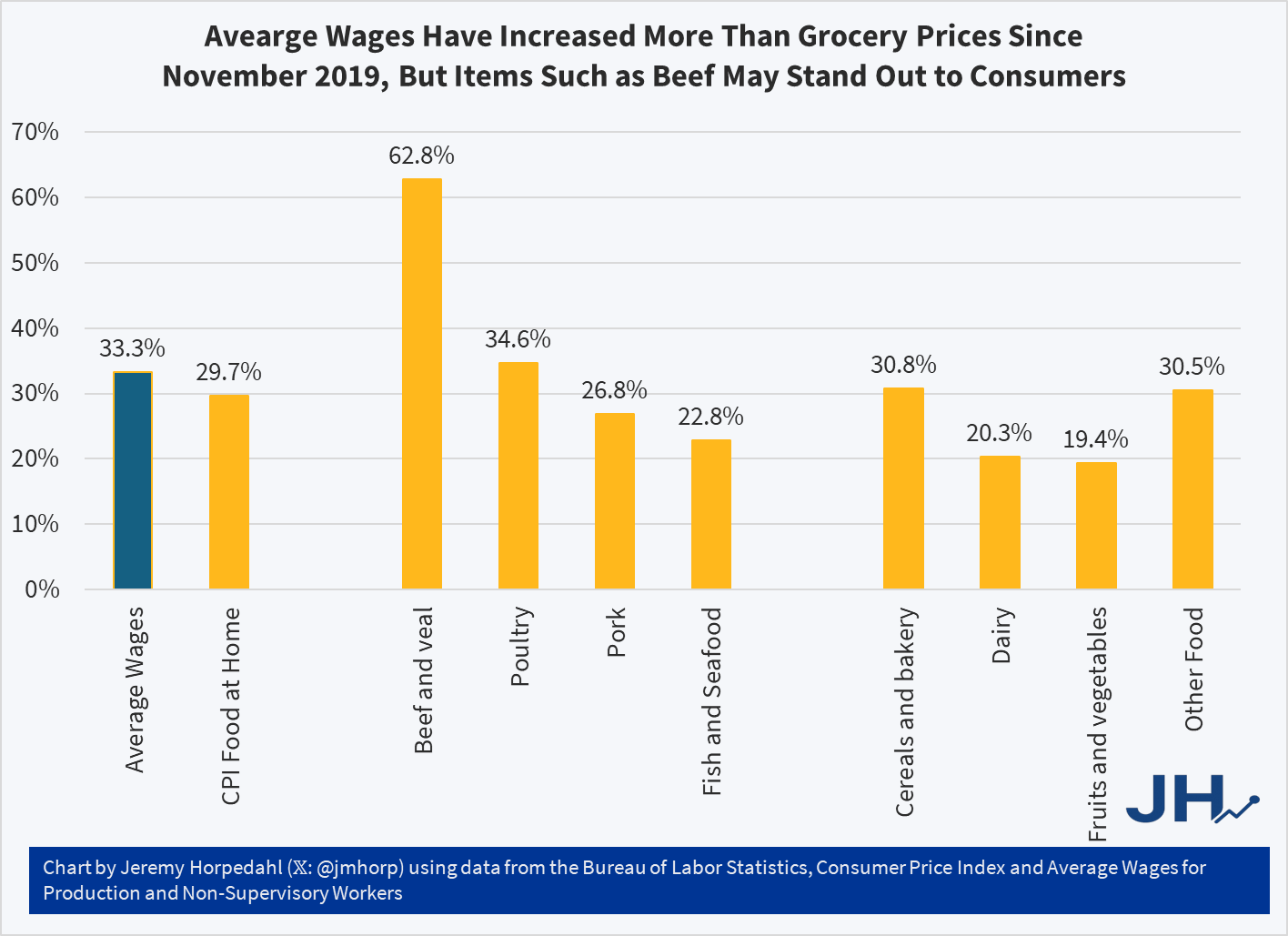

The chart shows a simple measure of relative grocery affordability. Starting with the levels of wages and grocery prices in 1947, if in any year wages increase more than prices, the line goes up (it can also go down, as it does in some years). Cumulatively, you can see that today groceries are over twice as affordable as in 1947.

You could reasonably complain that there hasn’t been much progress since the early 1970s. Fair enough. But there has been significant progress since the 1990s. Even if the progress is less than we would have liked, groceries are still, right now, the most affordable they have ever been in the US relative to average wages. And since US consumers spend by far the lowest share of their income on groceries in the world, we might be tempted to say that right now groceries in the US are the most affordable they have ever been in human history. Period.

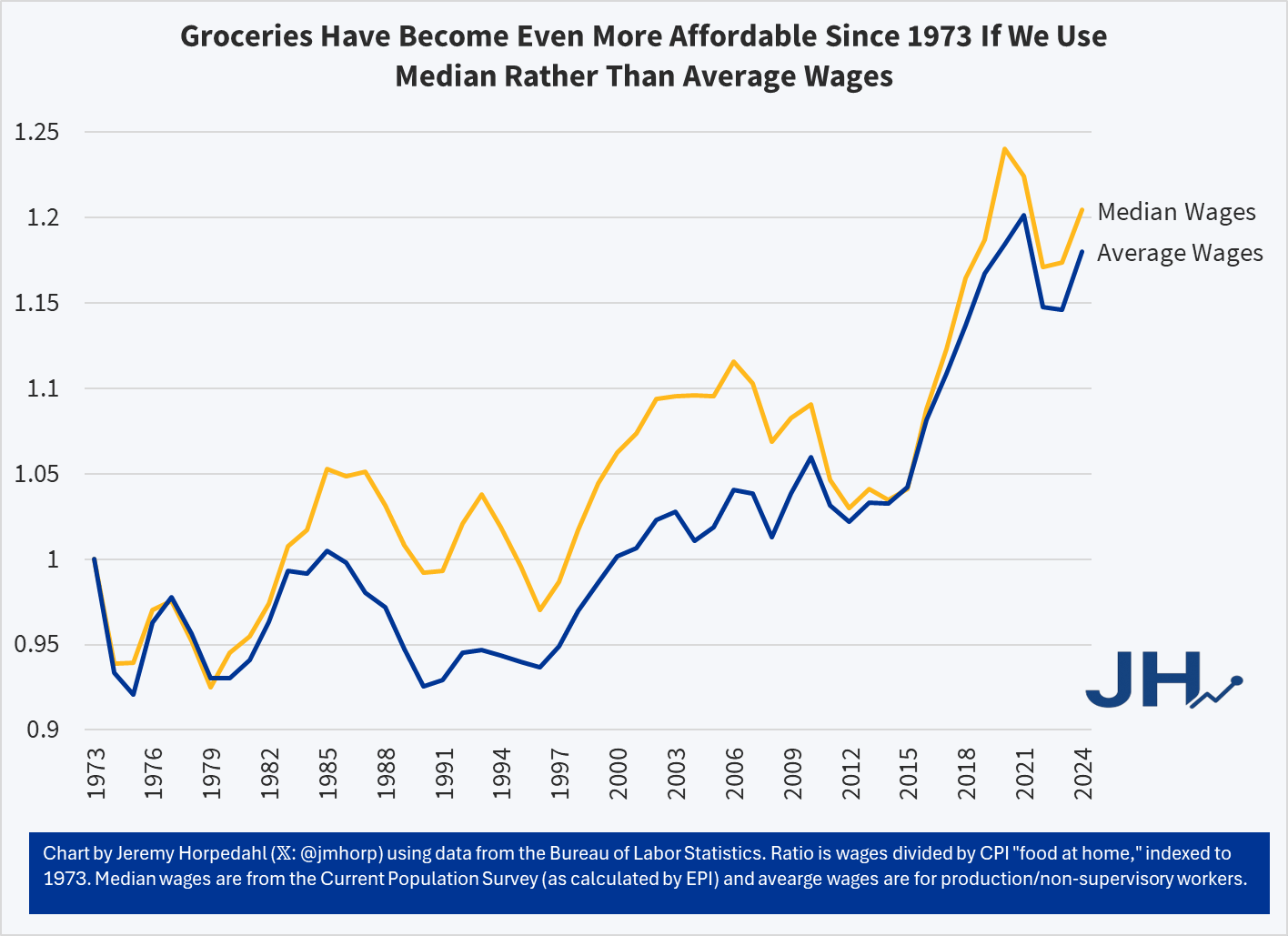

This is not just a trick of using average wages, which can be distorted by outliers. First, we are already using an average wage series that strips out the highest earners (supervisors, managers, etc.). But we can show this more clearly by using a median-wage series, such as the CPS series (calculated by EPI) starting in 1973. Notice this affordability trend gets slightly better if we use median wages from 1973-2024:

It’s true that using the median wage series, 2020 and 2021 look more affordable than 2024 — but that’s because the compositional effects of the job losses in the pandemic really throw off the median wage. But the growth rate since 1973 is slightly better for median rather than average wages — it’s not a trick! And when we have the median wage data for 2025, it will also likely be the most affordable measure on this chart.

So why are people so pessimistic if wages have been rising faster than grocery prices? One theory: availability bias. People focus on the prices where they notice goods becoming less affordable, but ignore the ones that are more affordable. Many consumers could probably tell you that a dozen eggs increased from $1.40 per dozen in November 2019 to $2.86 today, and at times was much higher, topping $6 briefly in early 2025. Likewise they could tell you that a pound of ground beef soared from $3.81 in late 2019 to $6.54 today. Both of these prices increases vastly exceed wage increases over the same timeframe (about 33 percent for wages), but most consumers probably couldn’t tell you that these were outliers and most major categories of food increased by less than average wages since late 2019:

While the “beef and veal” category has clearly outpaced wages — by almost twice as much! — nearly every other category of meat and as well as other food product prices increased less than wages. Poultry is the one exception, though here it is almost equal to wage increases. But if we are talking about pork or fish, or the non-meat categories, most food is more affordable than in late 2019 relative to wages. Consumers won’t as easily identify these more affordable categories, and they probably have no idea how much average wages increased.

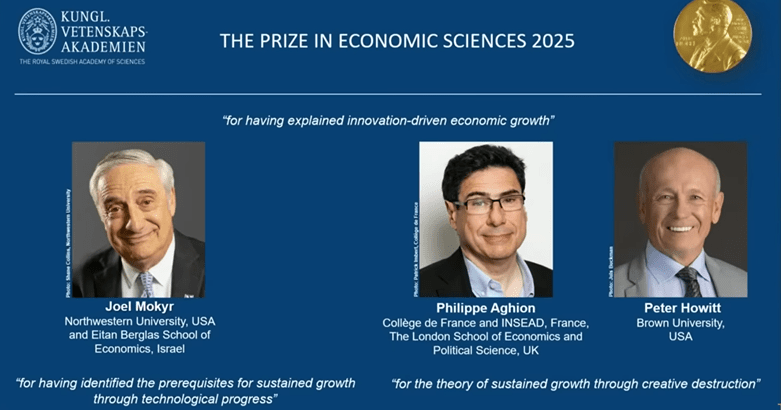

Fellow EWED blogger Jeremy Horpedahl generally gives good advice. Therefore, when the other week he provided a link and recommended that we watch Joel Mokyr’s 2025 Nobel lecture*, I did so.

There were three speakers on that linked YouTube, who were the economics laureates for this year. They received the prize for their work on innovation-driven economic growth. The whole video is nearly two hours long, which is longer than most folks want to listen to, unless they are on a long car trip. Joel’s talk was the first, and it was truly engaging.

For time-pressed readers here, I have snipped many of the speakers’ slides, and pasted them below, with minimal commentary.

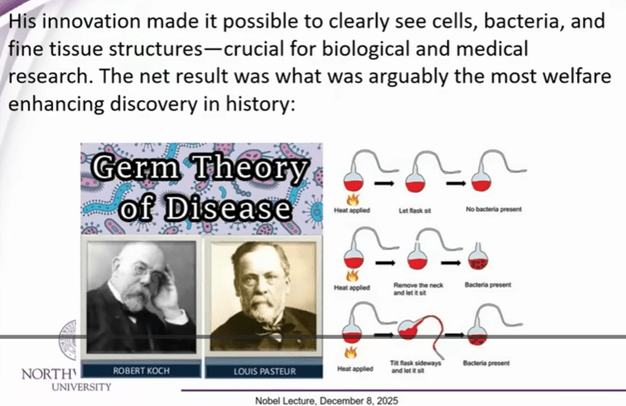

First, here are the great men themselves:

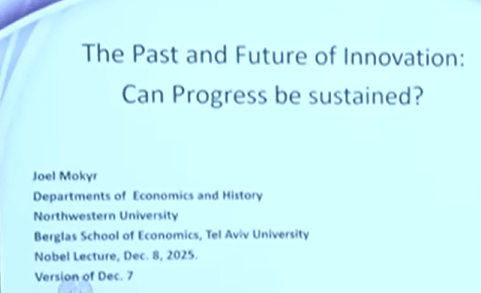

Talk # 1. Joel Mokyr: Can Progress in Innovation Be Sustained?

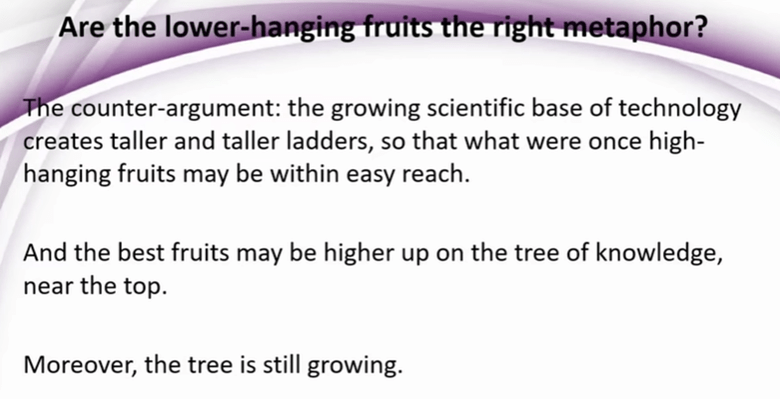

And indeed, one can find pieces of evidence that point in this direction, such as the slower pace of pharm discoveries.

But Joel is optimistic:

Joel provides various examples of advances in theoretical knowledge and in practical technology (especially in making instruments) feeding each other. E.g., nineteenth century advances in high resolution microscopy led to study of micro-organisms which led to germ theory of disease, which was one of the all-time key discoveries that helped mankind:

So, on the technical and intellectual side, Joel feels that the drivers are still in place for continued strong progress. What may block progress are unhelpful human attitudes and fragmentation, including outright wars.

Or, as Friedrich Schiller wrote, “Against stupidity, the gods themselves contend in vain”.

Talk # 2: Philippe Aghion, The Economics of Creative Destruction

He commented that on the personal level, what seems to be a failure in your life can prove to be “a revival, your savior” (English is not his first language; but the point is a good one).

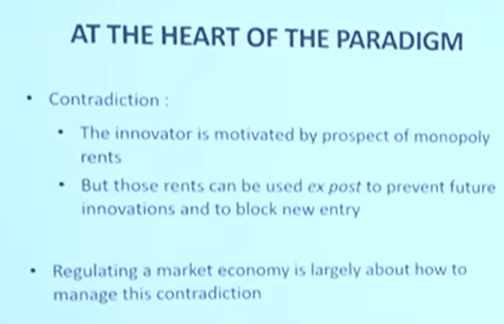

Much of his talk discussed some inherent contradictions in the innovation process, especially how once a new firm achieves dominance through innovation, it tends to block out newer entrants:

KEY SLIDE:

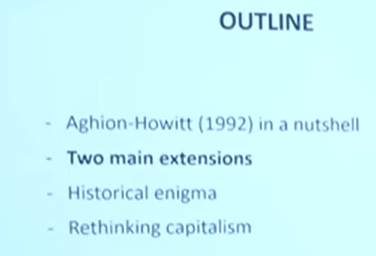

Outline of the rest of his talk:

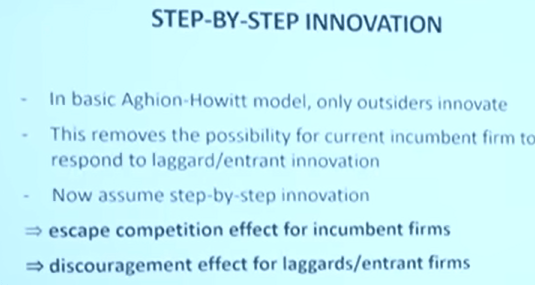

[ There were more charts on fine points of his competition/innovation model(s)]

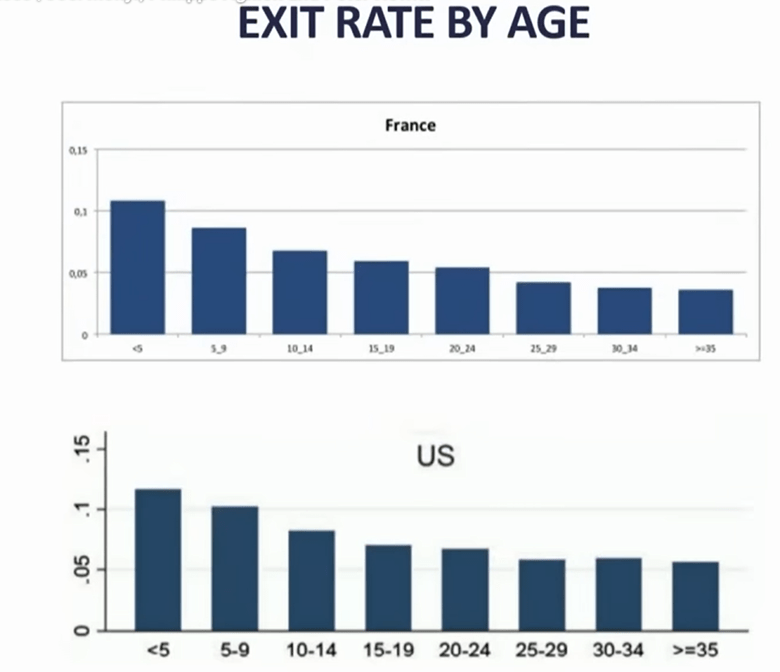

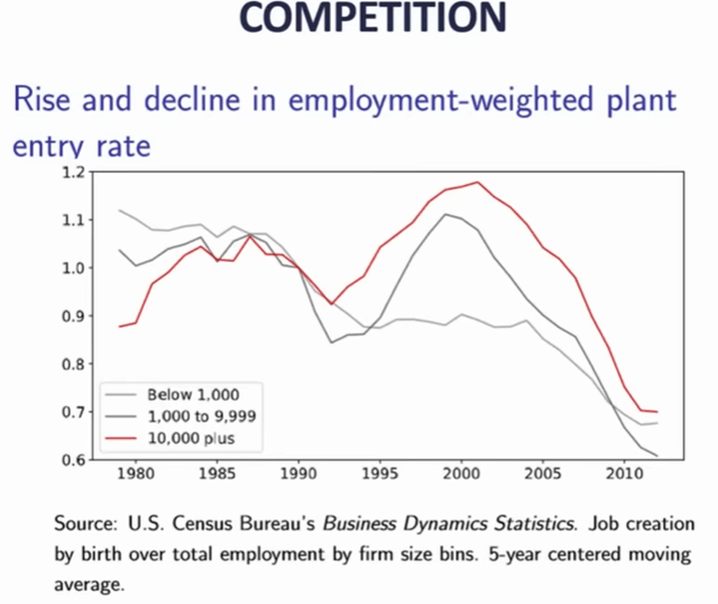

Slide on companies’ failure rate, grouped by age of the firm:

His comment..if you are a young , small firm, it only takes one act of (competitors’) creative destruction to oust you, whereas for older, larger, more diverse firms, it might take two or three creative destructions to wipe you out.

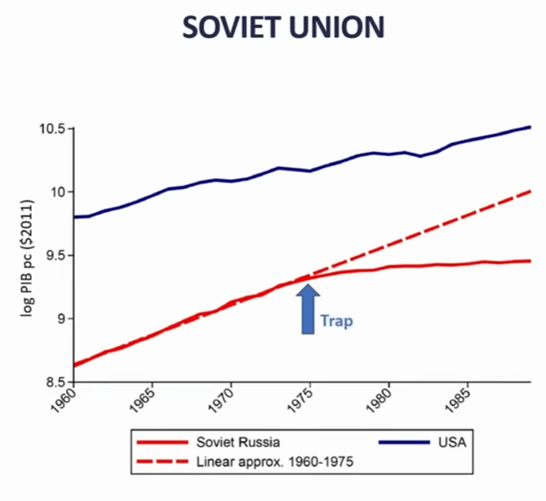

He then uses some of these concepts to address “Historical enigmas”

First, secular stagnation:

[My comment: Total factor productivity (TFP) growth rate in economics measures the portion of output growth not explained by increases in traditional inputs like labor and capital. It is often considered the primary contributor to GDP growth, reflecting gains from technological progress, efficiency improvements, and other factors that enhance production]

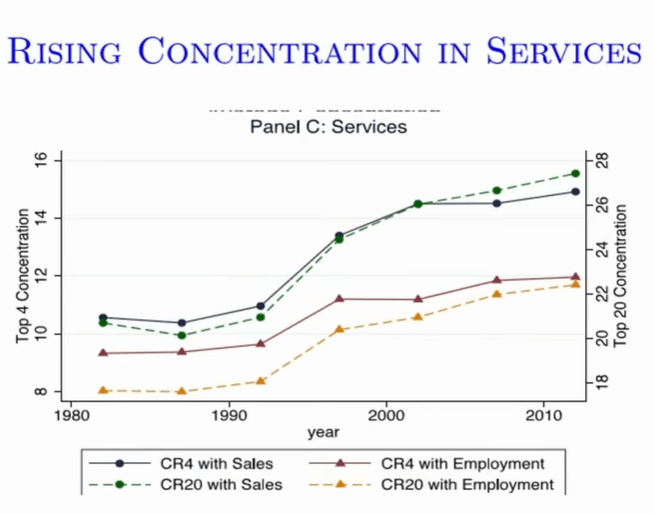

I think this chart was for the US. Productivity, which grew fast in the 1996-2005 timeframe, then slowed back down.

In the time of growth soaring, there was increased concentration in services. The boost in ~1993-2003 was a composition effect, as big techs like Microsoft, Amazon, bought out small firms, and grew the most. But then this discouraged new entries.

Gap is increasing between leaders and laggers, likely due to quasi-monopoly of big tech firms.

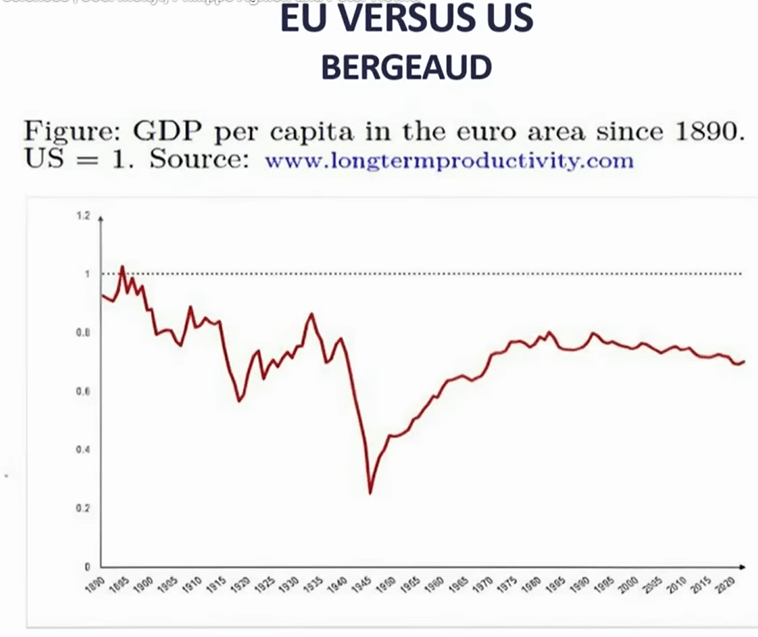

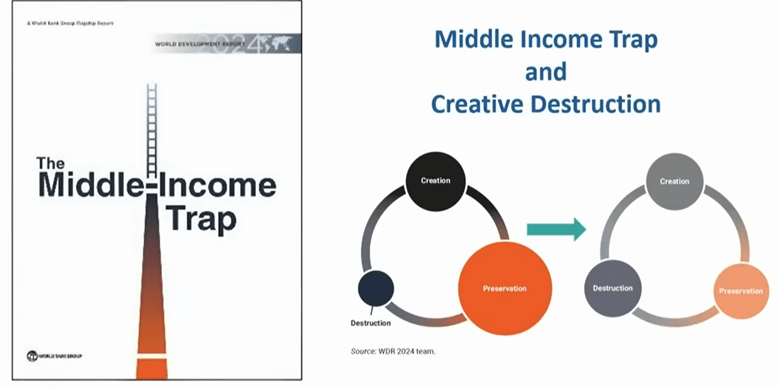

Another historical enigma – why do some countries stop growing? “Middle Income Trap”

s

Made a case for Korea, Japan growing fastest when they were catching up with Western technology, then slowed down.

China for past 30 years has been growing by catching up, absorbing outside technology. But the policies for pioneering new technologies are different than those for catching up.

Europe: During WWII lot of capital was destroyed, but they quickly started to catch up with US (Europe had good education, and Marshall plan rebuilt capital)…but then stagnated, because not as strong in innovation.

Europeans are doing mid-tech incremental innovation, whereas US is doing high tech breakthrough.

[my comment: I don’t know if innovation is the whole story, it is tough to compete with a large, unified nation sitting on so much premium farmland and oil fields]

Patents:

Red =US, blue=China, yellow=Japan, green=Europe. His point: Europe is lagging.

Europe needs true unified market, policies to foster innovation (and creative destruction, rather than preservation).

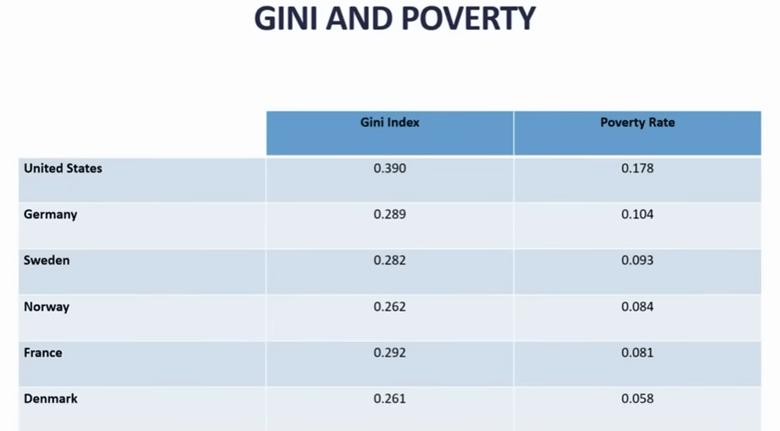

Finally: Rethinking Capitalism

GINI index is a measure of inequality.

Death of unskilled middle-aged men in U.S.…due in part to distress over of losing good jobs [I’m not sure that is the whole story]. Key point of two slides above is that US has more innovation, but some bad social outcomes.

So, you’d like to have best of both…flexibility (like US) AND inclusivity (like Europe).

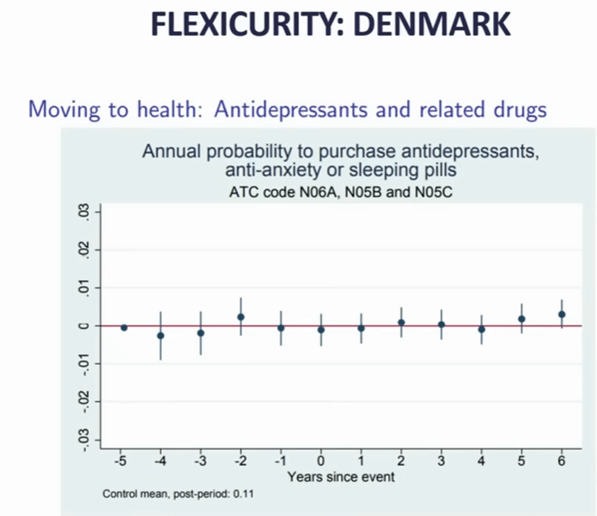

Example: with Danish welfare policies, there is little stress if you lose your job (slide above).

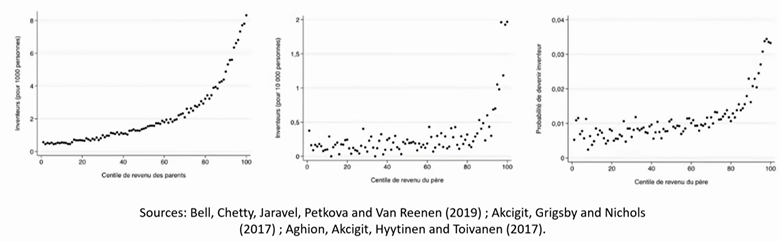

Found that innovation (in Europe? Finland?) correlated with parents’ income and education level:

…but that is considered suboptimal, since you want every young person, no matter parents’ status, to have the chance to contribute to innovation. Pointed to reforms of education in Finland, that gave universal access to good education..claimed positive effects on innovation.

Final subtopic: competition. Again, the mega tech firms discourage competition. It used to be that small firms were the main engine of job growth, now not so much:

Makes the case that entrant competition enhances social mobility.

The third speaker, Peter Howitt showed only a very few slides, all of which were pretty unengaging, such as:

So, I don’t have much to show from him. He has been a close collaborator of Philippe Aghion, and he seemed to be saying similar things. I can report that he is basically optimistic about the future.

* The economics prize is not a classic “Nobel prize” like the ones established by the Swedish dynamite inventor himself, but was established in 1968 by the Swedish national bank “In Memory of Alfred Nobel.”

Here is an AI summary of the 2025 economics prize:

The 2025 Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel was awarded to Joel Mokyr, Philippe Aghion, and Peter Howitt for their groundbreaking work on innovation-driven economic growth. Mokyr received half of the prize for identifying the prerequisites for sustained growth through technological progress, emphasizing the importance of “useful knowledge,” mechanical competence, and institutions conducive to innovation. The other half was jointly awarded to Aghion and Howitt for developing a mathematical model of sustained growth through “creative destruction,” a concept that explains how new technologies and products replace older ones, driving economic advancement. Their research highlights that economic growth is not guaranteed and requires supportive policies, open markets, and mechanisms to manage the disruptive effects of innovation, such as job displacement and firm failures. The award comes at a critical time, as concerns grow over threats to scientific research funding and the potential for de-globalization to hinder innovation.

Our episode began with some clips from TikTok of young people expressing anger over feeling trapped in “the subscription economy.” Watch our show at the link above to see.

The subscription economy is a business model shift where consumers pay recurring fees for ongoing access to products/services (like Netflix, SaaS) instead of one-time purchases, focusing on “access over ownership” for predictable revenue. Gen Z feels upset that they are getting charged for subscriptions, some of which they simply forgot to cancel. They have nostalgia for the days of toting a zipper case of CDs onto the yellow school bus in 2004.

My commentary starts around minute 5:30 in the show. The first thing I point out is that, by and large, we have more entertainment available to us at a lower price than people did in that bygone era of mostly cable TV and physical discs. (This is a bit like the point I made on The Stream in March 2025 about how fast fashion represents more stuff for consumers at lower prices, which is good.)

In the episode, we discussed how people can still buy CDs today. Sanya Dosani made the point that, “there’s a place for buying and a place for renting.” Everyone should be aware of how cheap DVDs, books, and CDs are at rummage sales in the United States in 2025. You can get a music album for 50 cents. Some youths have (re)discovered that DVD players are cheaper than a year of streaming subscription costs.

Around minute 17, I got to bring up my research about intellectual property, digital goods, and morality.

We find that people do not feel bad about taking the digital goods, or “pirating.” We even find that, in a controlled experiment with no previous context for what we might call intellectual property protection, the creators of these digital goods do not call such taking stealing either. It seems to be understood that folks will take and share if they can.

The proposed reason for artificially restricting the taking and resale of intellectual property is that creators need a way to profit from providing a public good. (Intellectual property rights in the U.S. Constitution are covered by Article I, Section 8.)

I said in the interview, “If you were able to just give a song to all of your friends, you probably would, and then that artist might not be able to make songs the next year.”

Thus, I suggested, “The subscription economy is a reaction to the fact that most people don’t view it as wrong to take things they can take and not necessarily pay for them. Companies had to find a new way to be able to make money and stay in business.”

I’ll clarify that I have not done quantitative research to prove that subscription models emerged causally because of pirating. I’m speculating. Another side to this is that people simply want to stream and companies are providing exactly what people want (despite the complaints circulating on TikTok). People reminisce about the “golden days” of early Netflix, but most people forget that the company was losing money at that time. Media production and distribution companies have to make money to stay in business.

At the end, the host asked me, “… what does it mean for who we are as humans, more of an existential question, where we are going with this age?”

That’s a deeper question than you might expect for a conversation about CD-ROMs. However, people do care about having some tangible form of art about them. Think of the ancients buried alongside beads and dolls. Netflix will never be the only thing that people want. As for Gen Z being upset about convenient Spotify, “what does it mean for who we are” has got to be part of it.

As an aside, furthermore, I’ll say here on the blog that Gen Z is by some measures the most entertained generation in history. For spiritual, not financial, reasons, I encourage them to cancel their subscriptions, take out their AirPods, and feel the silence and dread for a week.

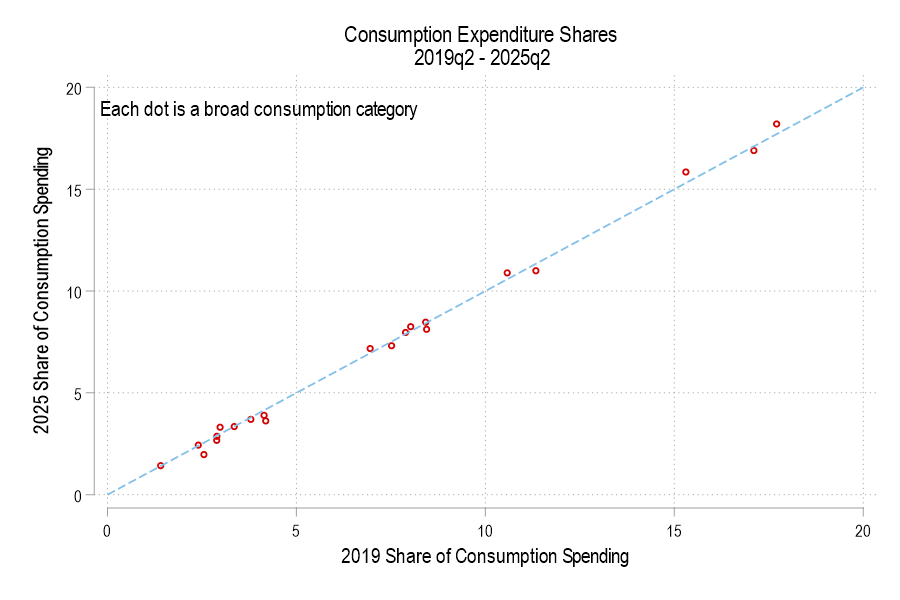

In aggregate, consumer spending on different broad categories of goods is relatively stable. The year 2019 feels like forever ago – and it was more than half a decade ago. But since then we’ve been hit by a pandemic and an AI shock and a trade war, and tariffs, and… plenty. We live in different times. Except, broadly, consumers are spending their money much as they did six years ago. Let’s compare some data from the 2nd quarter of 2019 and 2025.

First the Spending

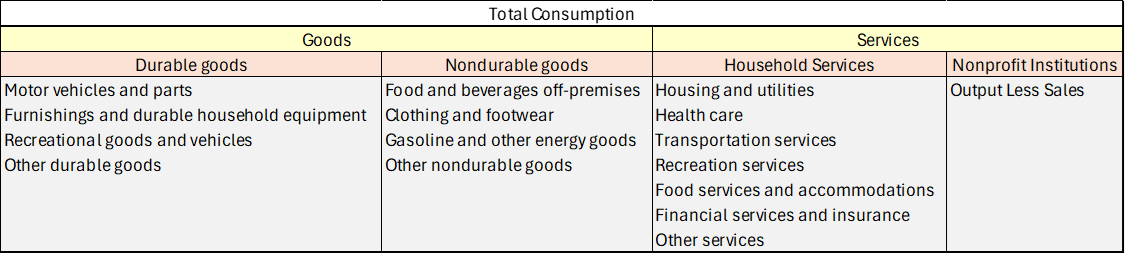

Consumption spending is categorized in the below table.

If total consumption spending (not inflation-adjusted) is 100%, then how has the allocation of spending changed? Below is a graph comparing each consumption component’s 2019 share versus 2025. The dotted line denotes an identical share. I haven’t labeled the categories because, suffice it to say, that spending shares are little different. None is more than one percentage point different.

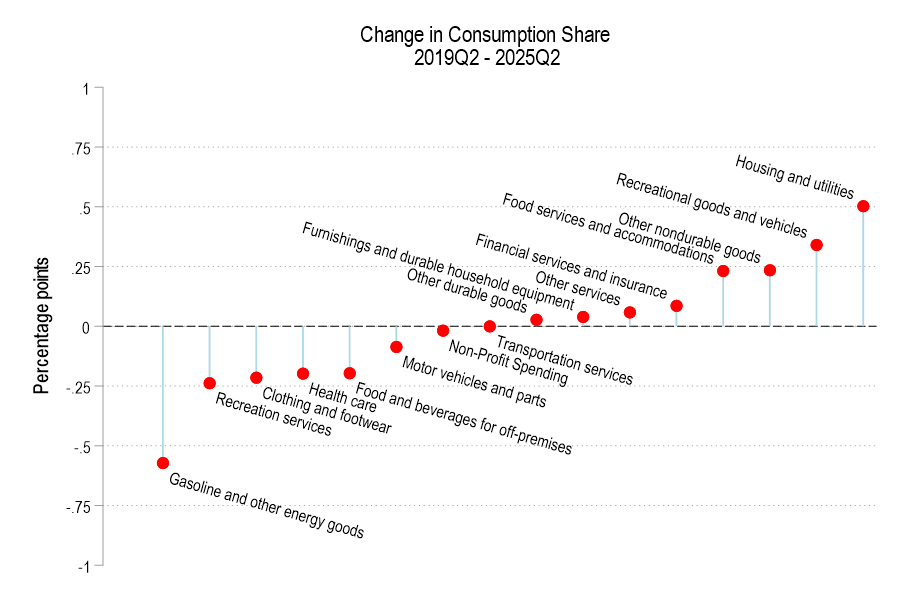

The below figure displays the spending share difference. We’re spending less of our consumption on gasoline and the like, recreational services, and clothing. Surprisingly, we’re also spending less on healthcare and food for off-premises consumption (non-restaurants). However, we’re spending a greater share on housing, recreational goods, food services for on-premises consumption (restaurants).

The Little Book of Common Sense Investing: “John Bogle, the founder of Vanguard, wrote a short book in 2006 that explains his investment philosophy. I can sum it up at much less than book length: the best investment advice for almost everyone is to buy and hold a diversified, low-fee fund that tracks an index like the S&P 500.”

The Little Book that Beats the Market: “Greenblatt offers his own twist on value investing that emphasizes just two value metrics- earnings yield (basically P/E) and return on capital (return on assets). The idea is to blend them, finding the cheapest of the high-quality companies…. Greenblatt’s Little Book is a quick and easy way to learn a bit about value investing, but I think Bogle’s Little Book has the better advice.”

When Genius Failed: “Myron Scholes was on top of the world in 1997, having won the Nobel Prize in economics that year for his work in financial economics, work that he had applied in the real world in a wildly successful hedge fund, Long Term Capital Management. But just one year later, LTCM was saved from collapse only by a last-minute bailout that wiped out his equity (along with that of the other partners of the fund) and cast doubt on the value of his academic work…. The story is well-told, and the lessons are timeless”

The Art of Spending Money: “Its main point is that people tend to be happier spending money on things they value for their own sake- rather than things they buy to impress others, or piling up money as a yardstick to measure themselves against others (this is repeated with many variations). Overall it is well-written at the level of sentences and paragraphs with well-chosen stories and quotes, but I’m not sure what it all adds up to.”

Non-fiction I didn’t previously mention here:

The Napoleonic Wars: A Global History, Alexander Mikaberidze: Aims to educate us about the surprisingly major effects of the Napoleonic Wars outside of Europe. Succeeds wildly; I also learned a lot about the main European theatre. Hadn’t realized how poor British Russian relations were in this era, since they defeat Napoleon together in the end. But they were heading for war early on until a czar was assassinated, then actually went to war in the middle over Sweden and trade. Outside Europe, Britain briefly took Buenos Aires and Montevideo, and accidentally (?) captured Iceland, along with all the French and Dutch overseas colonies.

Talent: How to Identify Energizers, Creatives, and Winners Around the World, Tyler Cowen and Dan Gross: A business book that works best for someone who hires a lot. How to attract and retain diverse candidates, including but not limited to the most-discussed types of diversity. Tyler says that when he lived in Germany people often thought he was Turkish, and one told him to ‘get out of here, you Turk’.

Almost Human: The Astonishing Tale of Homo Naledi and the Discovery That Changed Our Human Story, Lee Berger and John Hawks: The story of how the authors excavated a cave in South Africa that held many remains from a previously unknown type of early human. Good storytelling, good explanations of what we know about early humans from other discoveries, and surprisingly frank discussions of the academic politics behind getting paleontology research funded.

The Ends of the World, Peter Brannen: The book explains Earth’s 5 previous mass extinctions and the geology / science behind how we found out what we know about them. Written explicitly about what all this means for current global warming; see my full review on that here.

Annals of the Former World, John McPhee: New Yorker writer follows geologists from New York to San Fransisco to learn about the land in between. Published as a series of 4 books (Basin and Range, In Suspect Terrain, Rising from the Plains, Assembling California), each one focusing on a different geologist and region. McPhee is known as an excellent stylist but the books are also quite substantive, I feel like I learned a lot.

Fiction

The Works of Dashiell Hammet: My friend Dashiell mentioned that this is who he was named after, and that Red Harvest was a good book of his to start with. He was right, and it lead me to read many others: The Thin Man (you may have heard of Hammet because of the movies adapted from this and The Maltese Falcon), Best Cases of the Continental Op, Honest Gain: Dicey Cases of the Continental Op. Almost every story has a twist more interesting than “the murderer isn’t who you suspected”.

Tress of the Emerald Sea, Brandon Sanderson. Sanderson is one of the most prolific authors of our time, so where do you start with him? He suggests “Mistborn or Tress of the Emerald Sea, depending if they want something more heisty and actiony or something more whimsical.”

The Frugal Wizard’s Handbook for Surviving Medieval England, Brandon Sanderson: Sanderson doing his best impression of Terry Pratchett rewriting Mark Twain’s Connecticut Yankee in King Arthur’s Court, with shades of Scott Meyer’s Off to Be the Wizard.

Janissaries, Jerry Pournelle: What if instead of going to a more primitive world alone, you got sent there with an army?

The Narrow Road Between Desires, Patrick Rothfuss: Enough of an expansion of The Lightning Tree to be worth reading, but at this point anything Rothfuss does other than finally finish Doors of Stone can’t help but be disappointing.

Beguilement, Lois McMaster Bujold: Her Sci Fi works are great so I looked forward to her take on the Fantasy genre, but this turns out to be her take on the Romance genre.

Meta

This year I realized that Hoopla has a lot of books that Libby doesn’t, it is worth checking both apps for a book if you have access to libraries that offer both

BLS is slowly (actually, it probably feels very quick for those working on it!) catching up on data releases that were delayed during the federal government shutdown. This week, we saw the release of the November jobs report, which also includes data from October, even though there was no separate release for October. Well, kinda.

For the household survey (which is used to calculate the unemployment rate, among many other measures of the labor market), there is no October report. Because there is no data to be collected. Look at Table A in the employment situation report, and you will see no data in the column for October 2025. Look at the FRED page for the unemployment rate, and you will notice a gap in October. As I wrote a few weeks ago, this is not the end of the world, but it is rather sad for a gap to show up in a series that consistently ran for 933 months back to 1948.

So what is in the jobs report? Lots of new information. A few related areas that have gotten a lot of attention this week are the changes in federal government employment vs. private sector employment, and the changes in native-born vs. foreign-born employment.

In some quarters there is a sense that quantitative easing (QE), the massive purchase of Treasury and other bonds by the Fed, is something embarrassing or disreputable – – an admission of failure, or an enabling of profligate financial behaviors. For months, pundits have been smacking their lips in anticipation of QE-like Fed actions, so they could say, “I told you so”. In particular, folks have predicted that the Fed would try to disguise the QE-ness of their action by giving some other, more innocuous name.

Here is how liquidity analyst Michael Howell humorously put it on Dec 7:

All leave has been cancelled in the Fed’s Acronym Department. They are hurriedly working over-time, desperately trying to think up an anodyne name to dub (inevitable) future liquidity interventions in time for the upcoming FOMC meeting. They plainly cannot use the politically-charged ‘QE’. We favor the term ‘Not-QE, QE’, but odds are it will be dubbed something like ‘Bank Reverse Management Operations’ (BRMO) or ‘Treasury Market Liquidity Operations’ (TMLO). The Fed could take a leaf from China’s playbook, since her Central Bank the PBoC, now uses a long list of monetary acronyms, such as MTL, RRRs, RRPs and now ORRPs, probably to hide what policy makers are really doing.

And indeed, the Fed announced on Dec 10 that it would purchase $40 billion in T-bills in the very near term, with more purchases to follow.

But is this really (the unseemly) QE of years past? Cooler heads argue that no, it is not. Traditional QE has focused on longer-term securities (e.g. T-bonds or mortgage securities with maturities perhaps 5-10 years), in an effort to lower longer-term rates. Classically, QE was undertaken when the broader economy was in crisis, and short-term rates had already been lowered to near zero, so they could not be lowered much further.

But the current purchases are all very short-term (3 months or less). So, this is a swap of cash for almost-cash. Thus, I am on the side of those saying this is not quite QE. Almost, but not quite.

The reason given for undertaking these purchases is pretty straightforward, though it would take more time to explicate it that I want to take right now. I hope to return to this topic of system liquidity in a future post.Briefly, the whole financial system runs on constant refinancing/rolling over of debt. A key mechanism for this is the “repo” market for collateralized lending, and a key parameter for the health of that market is the level of “reserves” in the banking system. Those reserves, for various reasons, have been getting so low that the system is getting in danger of seizing up, like a machine with insufficient lubrication. These recent Fed purchases directly ease that situation. This management of short-term liquidity does differ from classic purchases of long-term securities.

The reason I am not comfortable saying robustly, “No, this is not all QE” is that the government has taken to funding its ginormous ongoing peacetime deficit with mainly short-term debt. It is that ginormous short-term debt issuance which has contributed to the liquidity squeeze. And so, these ultra-short term T-bill purchases are to some extent monetizing the deficit. Deficit monetization in theory differs from QE, at least in stated goals, but in practice the boundaries are blurry.

First, yes, the commenter is correct, this is grim:

This is fucking grim. Somebody invented a white guy, an "IT professional" named Edward Crabtree, who stopped the Bondi shooting and spread it all over the internet, which was picked up by AI agents and slop aggregation sites.The real hero is a fruit stand owner named Ahmed el Ahmed.

The tragedy of needlessly lost lives is, of course, bad enough to despair, but it’s made that much worse that false information created to ostensibly (and obviously) prevent a Muslim man from being credited with the kind of heroism normally reserved for films* is so casually distributed through major social media channels. Putting despair aside (easier said than done), I’m not interested in only shaming twitter et al for promulgating false narratives that always seem to conveniently fit into Grok’s preferred narratives of white/western supremacy. I’m more interested in thinking about how our processing of information will evolve.

There is always selective pressure in labor and life for those who better adapt to a changing technological and information landscape, and there’s no shortage of change happening right now. Some of it falls into classic “resist the propaganda” tropes. Don’t believe what you see on TV has evolved to don’t believe what you learn from the internet→ social media→AI→??? Once again, easier said than done, and I think it is more nuanced than that. It’s not just about information insulation and nihilism, it’s about cultivating the ability to better intuit when you are being misled.

Is there a subreddit? Of course there is a subreddit:

The comments are interesting because they are collectively sussing out specific, tangible clues that this is or isn’t AI. The convenient lack of license plates is both evidence of an error (if the state requires front license plates) and one of selective deception (the left car has their plate cropped out rather than blurred out). There is also the uncanny over-simplicity of the setting. No other people, debris, trash cans, mailboxes, etc. The absolute perfection of the cars outside of the region immediately surrounding the point of collision.

We have intuitive tools at our disposal, likely borne out of the same cogntive sources of the “uncanny valley” that haunts certain animation. We may have evolved to avoid predators that used mimicry to approach and infiltrate. These skills are ancient and innate, though. They are not inherently honed to combat AI-generated and distributed deception. We will have to evolve. And, as alluded to earlier, this is going to show up in far more than our politics.

There’s lots of hype around training students to work with AI. That’s all well and good, but I’m not sure how different those tools are than the ones that we honed to search with Google, to write and debug our own code, or to simply write effectively. What about the skills to evaluate and credit inputs? To discern the product of narrow expertise from distilled generalizations i.e. to discern new workflow and products from recycled “AI slop”. How much of a manager’s job is to simple assess whether the task was completed sufficiently or half-assed 70% of the way there? A lot of it? Most of it? The thing about half-assing it is that you are only incentivized to do it when avoiding 50% of the toil is worth the risk of getting caught. What happens when you can avoid 95% of the toil? Basic economics says you’re going to half-ass it a lot more unless the probability of getting caught or the punishment increases. What that means is that if management doesn’t get better at identifying 5%-assed AI slop from employees they’re going to have to start firing employees when they do get caught. In a world with high separation costs, that’s not an attractive option. Which means tilting the balance of decision-making back towards “actually doing the work” will fall to improved managerial oversight and monitoring. There’s no shortage of handwringing over escalating C-suite salaries. It will be interesting to how people respond to wage scales rebalancing towards middle management.

The most cliched thing to ask for in a job applicant has long been “attention to detail” or that they be “detail oriented”. I’m not sure if that is now obsolete or more important than ever. It’s not just about attention, per se. It’s evaluation, perhaps even cynicism. And it’s not because AI is evil or corrupt or even wrong. It’s just overconfident, and that overconfidence is catnip for anyone who wants to believe their work for the day is done at 9:05am. If you want to be in charge, you’re going to have to get really good at sussing out the little signs that what you’re looking at wasn’t produced for your task, but the average of all similar tasks. Can you look quickly and closely? You’re the boss, you’re busy, but so you better be good at it. The AI is in the details.

*And seriously, Ahmed al Ahmed is a hero. A movie hero. A crawling through the air ducts to fight the bad guys hero. Unarmed, he tackled a man actively firing a rifle at innocents and in the process saved a number of lives we will never know. He was shot twice. He’s real. I am in awe.