Housing remains the most expensive monthly outlay for most Americans. There are signs of things getting better, but the fact remains that for those living within the first or second ring of suburbs surrounding a given city, space is at a premium. For this holiday season, give the gift of not taking up any more of that precious, precious space.

Don’t give them instant pots or juicers for their already full kitchen counter. Don’t give them clothes to go in their overflowing closets. Don’t give them knick knacks, tschotckes, or decorative thingamajigs that will rapidly migrate from shelves to bins to (shudder) storage units. Don’t get them stuff.

I’m not going to say get them “an experience” because we’ve all become a little weary of that cliche. What I suggest is getting them a luxury that might fall at the margins of their budget. Get them a massage. A facial. A stretching session (that’s a real thing). If they line wine or whiskey, get them a bottle they’ve never tried. The stuff they already like is easy, but my expectation is that is probably already in their budget. Gift them the risk of trying something they might not like.

Books are acceptable because there is an entire ecosystem that exists that take books from one home to the next once it has been read. Get them a subscription to Amazon Music or a download code for a new game on their PlayStation. Get them tickets to a concert or play. Get them a two hour cleaning service.

Babysit their kids for a Saturday. Tell them their hair looks nice and really sell it that you mean it. Leave them alone for a couple days so they can recooperate from a long week. Just no more stuff please.

This is the 4th year in a row that the crew has put together some recommendations on products or books that we actually use, for your consideration in holiday gift buying. I’m going to put things into categories of Stuff for Adults, Kid’s Toys, Books for Adults, and Kid’s Books

Stuff for Adults (Men can be hard to shop for, so this might save Christmas!)

Scott says these scissors are amazing: “Fiskars 9 Inch Serrated Titanium Nitride Shop Shears”, available from Amazon here. Unlike some thick, heavy, or stubby heavy-duty shears, these have the feel of regular scissors, with fairly long, narrow blades. The handles are fairly substantial, and very comfortably contoured to the hand/thumb. The real magic is in the blades. They are sharp, with a very hard titanium nitride coating. Also, they have fine serrations in the cutting edge, that tend to grip the material in place as you are cutting.

Zachary recommends 5 things that he really uses at home

Food makes great presents for adults. Just give me Doritos, thanks.

Kid’s Toys

A wonderful game that you might not already have is Protect the Penguin. It’s high-energy but much less work than something like Twister. I actually enjoy playing it, too.

I’ll re-up from last year that Spot It is incredible and fits in your coat pocket. Fun for all ages. Several versions of the game. Not everyone has to know how to read or add to play so good for events with lots of ages represented. LEGO sets are always fun. If you keep the difficulty level age-appropriate than your kid should be able to play independently for an hour. I’ll put up one link but of course there are many thousands to choose from that can be tailored to any interest. My son likes Minecraft-themed sets.

Books for Adults

If you want to see all the books we have read and reviewed, just click on the Books category or go to

Not all of those posts are going to give you quick gift ideas, so if I had to pick out one from the last year it would be:

Secondhand: Travels in the New Global Garage Sale is a great book in my summer stack on fast fashion. I have always been interested in the combination problem-blessing of too much stuff. Adam Minter explains perfectly what many of us have been curious about.

You might have a relative who is very environmentally conscious or works hard to reuse and recycle. They might think it’s interesting to learn about the secondhand markets in America and beyond.

Kid’s Books

I’m reading The Hobbit aloud to my son right now and I highly recommend the experience. It’s going to take us months to get through it by reading a few pages at a time around bedtime.

Camp Out!: A Graphix Chapters Book (Bug Scouts #2) Funny graphic novel series about a group of friends in a scout troop. Probably especially fun for a kid who is in some kind of scouts program. Calvin and Hobbes is another comic series that my kid genuinely looks forward to reading.

Joke books can lead to great conversations. If the kid wants to know why something is funny, you can end up talking for a long time about the complex world.

See what we recommended in previous years. We have always had a mix of kid and adult items.

Do you know someone who likes practical gifts? Then these timely recommendations are for you given that Christmas is on the horizon. If none of the below recommendation strike your fancy, then there’s also the list that I made last year. The nice thing about practical gifts is that they tend to remain good gifts from year after year. This year’s list mostly concerns home-goods.

I didn’t build my house. And whoever installed the light fixtures had the poor foresight of choosing ones with candelabra bulbs (smaller bulbs with smaller plugs). They are much less bright. I like a nice bright room because it makes everything feel cleaner, neater, and there’s always enough light. I can always provide accent lighting with lamps, but the overhead light needs to – well – enlighten the room. I found these 800 lumen candelabra bulbs and they are pricey, but they are better than the daily resentment of a disappointing overhead light.

If you liked last year’s custom length Velcro recommendation, then you’ll also like this year’s worm-gear clamps. Have you ever needed a heavy-duty fix that’s also fast and easy? It’s the same clamp that’s used in to affix dryer exhaust ducts. It’s great for any project that needs a quick and secure solution. It’s super easy if you have a drill, and relatively easy if you just have a screwdriver. I used mine for some mechanical elements of my golf card.

This week I was in Bretton Woods, New Hampshire. The Mount Washington Resort there is lovely on its own terms as a grand old hotel surrounded by mountains, but it is better known (at least among economists) as the site of the 1944 conference that gave us the International Monetary Fund, the World Bank, and the postwar international monetary system.

This got me thinking about what other destinations should top the list of sites for economics tourism. Adam Smith’s house in Scotland has to be on there. In the US I’ve been trying to visit all 12 Federal Reserve banks; they tend to have nice architecture as well as a Money Museum. You can stay at Milton and Rose Friedman’s cabin in Vermont, Capitaf. I’d like to go to Singapore for many reasons, but one is that they seem to listen to economists more than any other country; I’m not sure what places to visit within Singapore that best reflect that, though.

The places I’ve listed so far are somewhat inward looking to the economics profession; you could get a much bigger list by looking outward to the economy itself, doing “economic tourism” rather than “economics tourism”. Visit a port, a mine, or a factory (like Adam Smith visiting a pin factory and getting ideas for the Wealth of Nations); visit a stock exchange or a bazaar. Visit whatever country currently has the fastest economic growth, or the worst inflation.

Those are my ideas, but I’d love to hear yours: what are the best places for econ tourism?

It’s the time of the year when we share ideas for things to buy, possibly as Christmas or other holiday gifts. But I’m going to share with you not a specific thing to buy, but instead a method for buying things. And probably not the kind of thing you might think of sticking in a wrapped present: food.

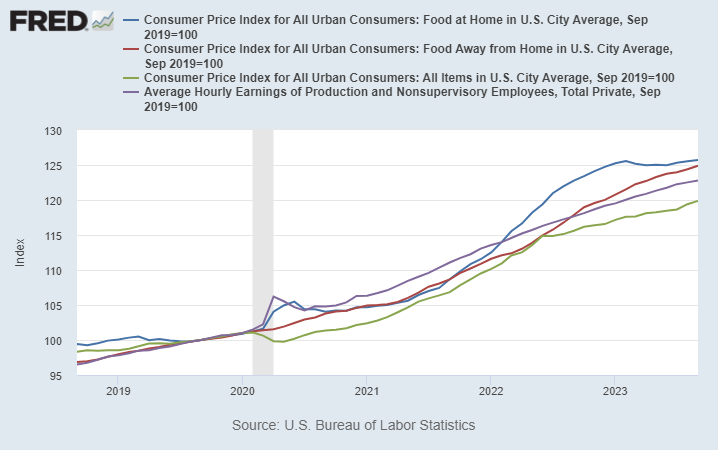

We’ve all heard about and felt inflation lately. But food prices have been especially noticeable to consumer, and not just because it’s a product you frequently buy and probably know the price of many food items. Food prices, both at home and restaurants, have increased much more than the average price levels.

On average, prices are up about 20 percent in the US over the past 4 years. But food prices are up about 25 percent, on average.

Wages (the purple line) actually have increase faster than the general price level over the past 4 years — that may shock you given what we constantly hear in the traditional and social media about “price increases outpacing wage gains” — but it is true when we are talking about food. Your dollar doesn’t go quite as far as it used to for food.

In some sense these costs are hard to avoid: food is a necessity. But there are ways to reduce your costs, and you probably know the general tips. Eat less at restaurants. Buy generic. Buy in bulk. Etc. These are good tips, but they all involve some sacrifice or annoyance. Is there anything else a consumer can do?

Yes. Here’s a few tips that can save you money, without the sacrifice. There is some thought involved, and perhaps a slight annoyance, but I’ve found that once you get in these habits, the mental and time cost is pretty low.

1. RESTAURANT APPS

You should always be ordering your food through restaurant apps when possible, especially for fast food. I try to track limited good deals on Twitter, but most restaurants offer on-going good deals. For example, McDonalds usually has a 20% off coupon, just for using the app. Taco Bell has a $6 box you can build, which would cost around $10 to order as a combo or à la carte at the restaurant. That’s a 40% discount for using the app.

Using apps also means you are using the restaurant’s rewards programs. Valuations vary, but McDonald’s rewards are roughly worth 10% cash back.

2. CHASE THE SALES AT GROCERY STORES

Clipping coupons is the classic way of saving money at the grocery store (we even have reality shows about it), but in the modern world grocery stores have expanded the ways to effectively save the same amount of money. The clearest example is, once again, the rise of apps. Stores will often have “digital only” coupons that you need to access through their app (which is also tied to your rewards account, just like restaurants).

While I’m a strong advocate of coupon clipping (and the virtual equivalent), it can be time consuming. Another strategy that can save you is thinking ahead about seasonal and other cyclical prices. For example, my kids like M&M’s. We usually buy a bulk 62-ounce container at Sam’s Club (already a savings), but today I took the additional saving step of buying the Halloween-themed bulk container. It was 36 percent less than the identical Christmas-themed M&M’s container right next to it. And I was replacing the Easter-themed bulk container that we purchased back in April, and they just finished.

Of course, I had to be planning ahead and know that November 1st was a great day to buy M&M’s. That takes some mental effort, sure. And you might think these kinds of deals are fairly limited in nature. But holidays aren’t the only kind of seasonal deals. For example, even though most fruit is generally available year-round now, there are still predictable price cycles of when things are “in season” and when they have to be imported from expensive locations. Even if you are only able to find these cyclical deals for 10 percent of your purchases, saving 30-50% on cyclical goods will shave another 3-5% off your grocery bill — bringing it closer in line to the average increase in prices (and wages).

3. CASH BACK CREDIT CARDS

I could write an entire post about credit card rewards. But let me focus here on credit cards that are especially good for buying food. At a minimum you should be getting 2 percent back on all of your purchases, as there are several no-annual-fee cards that give you 2 percent: the Citi Double Cash and Wells Fargo Active Cash are good examples.

But on food purchases, you should be able to beat 2 percent. For example, the Citi Custom Cash card gives you 5 percent back on your top spending category each month, up to $500 of spending. This can be on either groceries or restaurants. And since a family in the median quintile spends $250 at restaurants and $460 on groceries per month, you should be getting 5 percent back on basically all of your purchases in one of these two categories. (Personally I stick to restaurants for this card, because I buy most of my groceries at Walmart and Sams Club, which don’t count towards the grocery cash back.) Or if you want a simple card that gives you 3 percent back on both groceries and restaurants, check out the Capital One SavorOne card (again, no annual fee).

There are also several cards that have rotating 5 percent cash back categories each quarter, and they often include either restaurants or groceries. How do I keep track of which card to use for what kind of purchase? Simple: put a strip of masking tape on the card with a label. This will get some chuckles from your friends or the server at the restaurant, but that’s just an opportunity to tell them how to save money too!

Is There Really a Free Lunch?

Some of my economist friends are probably skeptical at this point. Aren’t I say there is a free lunch here? Isn’t the extra hassle of the steps I suggested going to outweigh any discount you get?

The answer is No. And while economists are quick to bring up the concept of opportunity cost, I find that most people tend to overestimate their opportunity cost. But even if you don’t overestimate your opportunity cost, you can bring in another useful economic concept: price discrimination.

Restaurants are very much in the business of price discrimination, and always have been. Tuesday Night specials, happy hours, etc. Every consumer has a different willingness to pay, and since it’s hard to resell a restaurant meal, restaurants can potentially use this technique to their advantage (and yours, if you are willing to look for discrimination). Grocery stores don’t have as much of an opportunity to discriminate, but they still find ways.

Don’t be afraid of price discrimination: use it to your advantage!

My rave product for this year is “Fiskars 9 Inch Serrated Titanium Nitride Shop Shears”, available from Amazon here. I randomly bought these scissors a few years ago for a relative, and then realized how useful they were. So, I got a pair for our household, and it became our go-to scissors. When we lost that pair a few months ago, we felt the loss keenly enough to go and buy a replacement.

What is so great about them? Unlike some thick, heavy, or stubby heavy-duty shears, these have the feel of regular scissors, with fairly long, narrow blades. The handles are fairly substantial, and very comfortably contoured to the hand/thumb. The real magic is in the blades. They are sharp, with a very hard titanium nitride coating. Also, they have fine serrations in the cutting edge, that tend to grip the material in place as you are cutting. They will set you back about $24. Made in China, of course.

Two images from the Amazon site are:

With 935 ratings, the average rating on Amazon is a stratospheric 4.9/5. Reviewers find themselves reaching for superlatives:

We have an embroidery shop and find regular scissors dull quickly. These do not. They cut through everything!

The best heavy duty scissors. Period… These pups will handle any cutting job even remotely appropriate for this tool.

My wife has multiple pair of shears that she uses on her sewing table. She would not miss one pair if I were to borrow them for the shop, right? Well, that did not work. I’m in purgatory for that, for sure. So… I bought these. These shears are MY shears. I get to use them for all of those things in the shop that need to be cut. No, I don’t cut asphalt roofing shingles and corrugated steel roofing with them, but I cut rough and heavy and coarse and dirty stuff that needs cut with the accuracy of using shears. Stuff where a razor knife is not quite adequate. You know the stuff I mean. Ladies, do the old man a favor… and do yourself a really good deed… and buy a pair of these for him. He’ll hopefully not be using yours any more.

The best pair of shears I’ve ever used… I swear, you could split the atom with these things. Matter simply parts at their touch. I’ve been using them daily for all my shearing needs for the last six months, and they’re as sharp and perfect as the day I received them.

Well, you get the picture. We use them for food cutting in the kitchen, cutting cloth, cardboard, thin sheet metal, wire, etc. They can also handle ordinary cutting of paper, although they do leave fine teeth marks.

Honorable Mention: Leatherman Micra Tool

Another cutting implement I find very useful is the Leatherman Micra Tool. At about 2 inches long all folded up, it is small enough to easily fit in a pocket or purse, though just a bit heavy to hang on a keychain. It has small but very capable scissors (can cut fingernails well) ; a very sharp little knife ; a diamond-grit file for nails, etc.; some light-duty screwdrivers; tweezers (not the best); and an old-fashioned bottle-cap opener. Also, it has ruler markings, which I have used on occasion. So many items now come packaged in very tough, clear plastic covering that you can’t peel or rip with your fingers. It is great to be able to whip out this Micra and quickly slice through that plastic. The quality of the workmanship is so good that anyone who appreciates tools will feel good about it.

This is an easy win as a present. If someone has no use for it, they can easily regift it. Once upon a time when I was a project leader, I bought one for everyone as a celebration for reaching milestone. I got them from Leatherman, engraved with the project name. They were a hit.

The only downside is the price. I am used to getting these for like $25 or so. But when I just looked on Amazon, I see the new price has jumped to $57 (though you can get them cheaper at the Leatherman.com site). That seems kind of steep. These are made in the U.S.A. You can purchase Chinese knock-offs for much less, though the quality may vary.

There is, however, a lively market for used Micra tools. Below are two images for one for sale on eBay, for $13.00 plus $4.75 shipping. If you are getting one for yourself or say a son/father/brother or buddy, getting a high quality tool with a few scratches and no packaging may be fine. Other recipients may not appreciate a used item.

I had the opportunity to present a new paper about theft to the faculty and students at two law schools last week. The questions and comments were interesting throughout, but I noticed a pattern in several of the questions from students: were we attributing too much rationality and sophistication to criminals?

Citing Becker (1968) as a useful exercise in applying economic parsimony to understanding how punishment and enforcement deter crime is one thing, but I think it’s simplicity sometimes undercuts a really important intuition that I hold to strongly: crime is boring. More specifically, a lot of crime (not all, of course) is a product of a banal calculus that arrives at the conclusion that my expected life (probabilistically) is better if I take this illegal action. These crimes seem irrational is because of two behavioral errors, not on the part of criminal, but on the part of the observer.

The first mistake is failing to realize you are observing the conclusion ex post, after the outcome has been revealed, and your ability to observe it is almost exclusively because the action failed i.e. they got caught. You know they got arrested for shoplifting an item that won’t significantly change the quality of their life. This feels like a mistake, but what you can’t observe is how many times they or someone else has taken the same action without negative consequences. If 1 in 10,000 thefts worth $500 are caught, then that’s probably an optimal choice for a lot of people.

The second mistake is implicitly assuming the same level of constraints that apply to your life apply to the criminal actor. We all know the question asking whether it is a sin to steal bread to feed a starving family, but that same logic applies in broader and less severe circumstances when considering the ex ante rationality of a choice. The cost-benefit analysis facing a potential thief is far different if they already carry the stigma of a criminal record. If their labor market opportunities are limited. If rent they have insufficient funds to cover is due is three days.

I find it interesting that people who disavow the salience of IQ and the people that place IQ at the center of their core model of humanity both seem to consistently underappreciate the sophistication of most human problem solvers. I’m not saying we all get the math right. Quite to the contrary, not only do we make constant errors in judgement, but the duress of operating under difficult constraints likely makes optimal decision-making all the more difficult. But those errors are relatively modest relative to the humans who are, at a baseline, tremendously sophisticated. They want and need resources and they can conceive of myriad manners in which to acquire them. Applying a lesser sophistication to people who steal from a CVS and sell to a middle-man who turns it over at a street corner or on Amazon puts any policy design at a disadvantage from the start.

If you want to divert people out of illegal markets and into legal labor, you’re better served treating them as people who made the optimal decision. Your ambition should not be to change their decision-making, but to change what the optimal decision is.

I suppose books were, for a time, the cheapest way to convey bits of information, before anyone had heard of “bits”. I asked ChatGPT to do my boring work and rehearse the history of the term “bits” so I could get my facts straight for this post.

Based on my other research, I was not confident that this paper called “The Binary System” exists. I could find no evidence of it from 5 minutes of googling. When I asked ChatGPT about it, ChatGPT apologized and said it probably isn’t real.

That kind of error would have been less likely with paper books that had human editors and authors. We hardly thought about this benefit of the old system, until it was gone. Because books had some cost to write and print, it made economic sense to employ an editor to ensure quality. For a while, no one would have thought of spewing out this ocean of associated terms that we get from ChatGPT, because it was too expensive. So, the first underappreciated benefit of printed books was that they were relatively more accurate.

This is the first “generative book” that I had ever accessed. I did the worst thing, right away. I asked the Chatbot to give away the ending, and it did.

I wish I could have bought the paper book and read until the end, using the suspense as a device to get me to learn new details about famous economists. Books and movies used to be able to use suspense to keep the audience engaged. Before generative books, that just seemed like the only way.

I didn’t think of books as special until I used a phone to (try to) learn. Now I put more value on the hours I spent reading paper books when I was younger. Authors were manipulating me through that rigid medium. I was forced to wade through pages and pages to get to the point. But what value is the “point” without the context? Getting to the point through arguments and examples, instead of just seeing a tweet, made us smarter. The second benefit of books was that we were forced to work harder.

Generative books are a further step toward poastmodernism.

A middle ground I can imagine is asking the chatbot to play coach instead of search engine. What if the Chatbot could write you a shorter version of the book that cuts out the parts you would have skimmed in a paper book? Still, just knowing that you were skimming certain parts actually created context. I took that for granted, until now.

Something has happened in the world outside of our screens that feels both “full circle” and “anti-Network State”. The BBC announced that an American tech billionaire bought the English pub where J.R.R. Tolkien and C.S. Lewis famously met to talk with a group of friends.

We could just see pictures of that place on the internet. You can see my 2014 pilgrimage to it pictured below. But people want to go in person, if they can afford it. That used to just be the only way to do things. Now that we can see what it is like to live through digital media, we are discovering the value that existed all along in 3-D doings.

Speaking of Tolkien, I’m reading The Hobbit aloud to my son right now and I highly recommend the experience. I’m glad that he is capable of enjoying it, since the pacing is so different from the media and games on screens. To get an elementary-aged boy reading from paper, I also recommend Calvin and Hobbes.

We like to put up recommendations for holiday gifting at this time of year. That paperback of Calvin and Hobbes would make a great gift for a kid (or adult!).

Zachary told us that he has printed out our own blogs for the week to read at home on paper. That’s “full circle.” Maybe print has something for us, even if it is more expensive than scrolling screens.

Buying new hardcover books at a bookshop regularly can be prohibitively expensive. But if you look at used books, you can easily walk out of a rummage sale with 10 quality books for $10.

Also, sometimes ordering older print paperback books or DVDs on Amazon is extremely cheap. Here are some of the cheap Amazon media purchases I made in 2023. I might have found them even cheaper at a local garage sale, but getting it delivered to my house saves a lot of time. I recommend all of these items over scrolling mobile screens.

Some people might prefer Kindle to paperback because it allows them to maintain a larger “library”. If you have very limited space to store books, then I can understand that advantage. However, I know that I learn better from paper. Printed media might still be worth paying for.

Afterword: I printed out two chapters of Tyler’s new book and it’s excellent.

It’s mostly very smart and serious, but this paragraph made me laugh out loud.

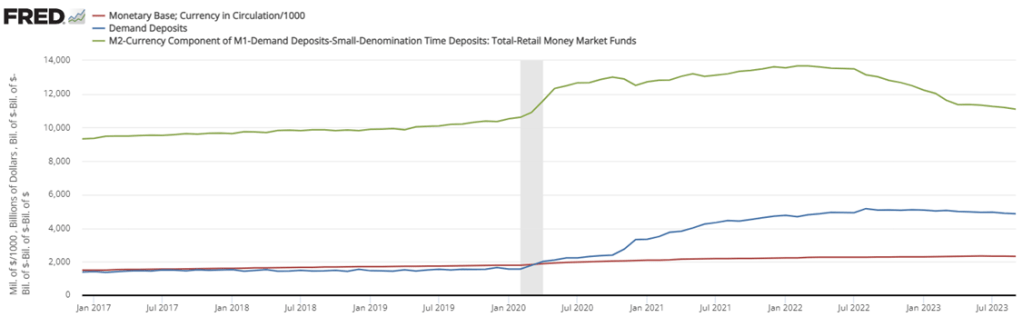

Money and interest rates have been in the news because the Fed wants to slow the rate of inflation, maintain financial stability, and avoid a recession. Let’s break it down. First, some broad context. The M1 and M2 were all chugging along prior to 2020. M2 was growing along with NGDP and, after raising interest rates, the Fed had begun lowering them again. Then Covid, the stimuli, and the redefinition of M1 happened. Now, we’re trying to get back to something that looks like normal. See the graphs below.

But these aggregates gloss over some relevant compositional changes. Let’s go one-by-one.

The monetary base includes both bank reserves and currency in circulation. We could break it down further, but I’ll save that for another time. What we see is that while currency in circulation did grow faster post-covid, it was nothing compared to the growing reserve balances. From January to May of 2020, currency grew by 7.5% while reserves almost doubled. That means a few things. 1) People weren’t running on banks. Covid was not a financial crises in the sense that people were withdrawing huge sums of cash. 2) Banks were well capitalized, safe, and stable. Further, uncertainty aside, banks were ready to lend. And they did. Not long after the recession, everyone and their brother was re-financing or taking on new debt. More recently, we can see that currency has stabilized and, again, most of the action has been in reserve balances. As of September 2023, reserve balances are down 23% from the high in September 2021.

The thing about the monetary base, however, is that reserves don’t translate into more spending unless the reserves are loaned out. The money supply that people can most easily spend, M1, is composed of currency held outside of banks, deposit balances, and “other liquid deposits” (green line below).* See the graph below. Again, most of the action wasn’t in the physical printing of hard, physical cash. People’s checking account balances ballooned thanks to less spending on in-person services and thanks to the stimulus checks and other relief programs. Deposit balances more than doubled from January to December of 2020. Ultimately, deposit balances were 3.3 *times* higher by August of 2022. Since then, the balances have been on a slow, steady decline of about 5.8% over the course of the year. But even then, it’s those “other” deposits, previously categorized as M2, where most of the action is. The value of those balances have fallen by a whopping 2.5 *trillion* and 19% dollars in the past 18 months. People are drawing down their savings.

Finally, we get to M2, the less liquid measure of the money supply. Besides the M1 components, it also includes small time deposits, such as CD’s, and money market funds (not including those held in IRA and Keogh accounts). Money market funds and small time deposits have *increased* in value since the post stimulus tightening as people chase the allure of higher interest rates on offer. Measured by volume, the declines in the broad money supply have darn near all come from declines in M1 (again, the jump is redefinition). And of that, it’s almost entirely coming out of “other” liquid deposits, as illustrated above. That’s savings balances. It’s true that there is some other-other balances, but it’s mostly savings accounts.

Zooming in on just those “other” balances (below left), people still have higher balances than they did prior to the pandemic. But by now, they’re below the pre-pandemic trend. Savings accounts are depleted. However, since many people don’t use savings account anymore due to the decade plus of low interest rates, it’s appropriate to consider both “other” accounts and demand deposits (below right). By that measure, we still have plenty of post-Covid liquidity at our disposal.

*Other liquid deposits consist of negotiable order of withdrawal (NOW) and automatic transfer service (ATS) balances at depository institutions, share draft accounts at credit unions, demand deposits at thrift institutions, and savings deposits, including money market deposit accounts.

PS. So where is all this above-trend NGDP coming from, if not the money supply? Hmmmm.

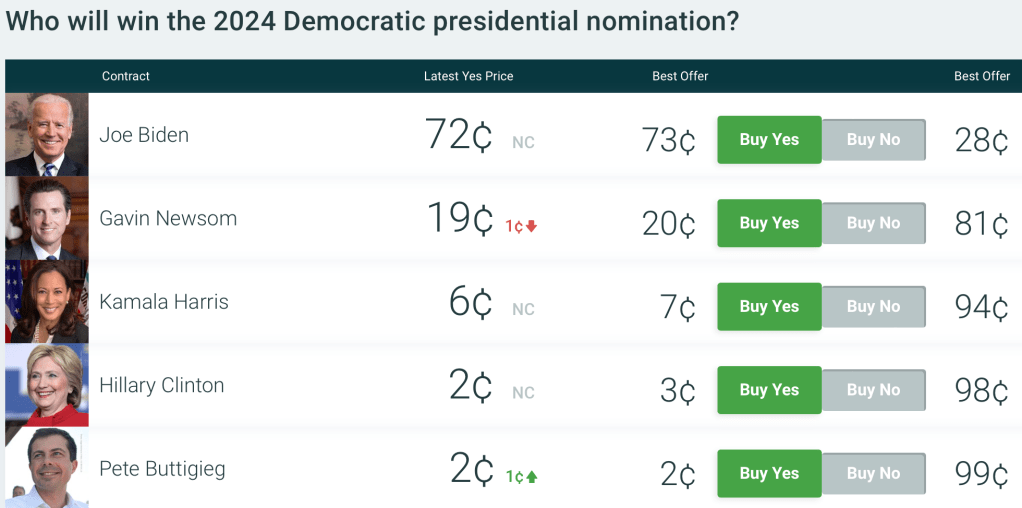

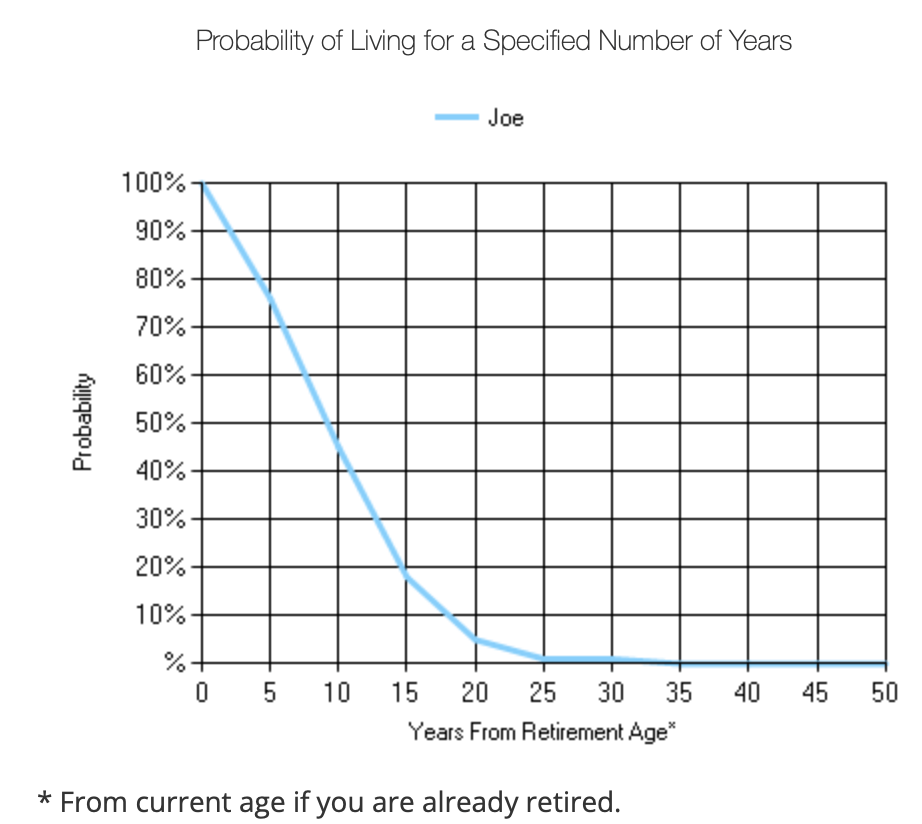

President Biden winning the Democratic nomination is currently priced at 72 cents on PredictIt, implying a roughly 72% chance of winning the nomination. Not the general 2024 election- where he is priced at a mere 43 cents- but the Democratic nomination.

To me it seems crazily underpriced to put the odds of an incumbent president being renominated by his own party at only 72%. Yes, his approval ratings are underwater, and yes he’s old, but the base rates here very much work the other way. No incumbent president has lost a vote to be renominated since Chester Arthur in 1884. It think its extremely unlikely Biden would run for nomination and lose; it makes more sense that he would choose not to run, like LBJ in 1968, but I see no indications of that.

I think Biden will only fail to be renominated if he dies or experiences a major decline in his health by the convention next August. This is certainly possible for an 80 year old but the odds of it are well below the 28% implied by PredictIt. A recent WSJ article lays out the details:

a nonsmoking male with Biden’s birthday, in good health, would be expected to live nine more years after next year’s Election Day, while for one with Trump’s birthday, it would be 11 years.

WSJ focuses on his chance of finishing a second term and doesn’t give an estimate for just making it to renomination, but my own look at actuarial tables shows that the average 80 year old has only a 6.5% probability of dying within a year. The chance of dying or getting a disabling health condition in a year is of course higher than that, but the convention is actually less than a year away in August, and the primaries will be done by June. Plus the WSJ article gives several reasons to think Biden is in better health than the average 80 year old:

First, the median includes people who drink alcohol. Regular drinking of two or more drinks, three or more times a week, shortens life expectancy by about seven years. Both Trump and Biden are teetotalers, in addition to being nonsmokers.

“Those are two of the biggest killers right there,” said Bradley Willcox, a professor and research director at the Department of Geriatric Medicine at the University of Hawaii. “When you eliminate excessive alcohol intake and smoking, one thing you’re left with is genetics.”

Here, Trump and Biden picked their parents well. Trump’s mother lived to 88 and his father to 93, though late in life he developed Alzheimer’s disease. Biden’s mother died at 92—living long enough to see her son become the sixth-oldest vice president. Joe Biden Sr. died at 86. That is even more impressive than it sounds: When those four individuals were born, life expectancy was around 50.

Biden and Trump are each highly educated at a time when the life-expectancy gap between the educated and uneducated has been growing. They are wealthy, also a strong predictor of longer life. They receive excellent healthcare.

Add it all up and I think Biden has over a 90% chance of being renominated, so being able to bet on him at 72 cents seems like a great deal (even if it means tying up money that could now earn 5% interest elsewhere). PredictIt has betting limits and high withdrawal fees, but other prediction markets are in the same ballpark; Polymarket currently has Biden at 75c.

For similar reasons Trump is may also be underpriced to win the nomination, currently at 68 cents on PredictIt. He’s not an incumbent the same way, but he’s enough of one that I don’t think any of his electoral opponents can beat him for the nomination; he’d have to beat himself by dying or withdrawing (very unlikely), or be beaten by the legal system (he’ll continue to have trouble but I don’t think it will be enough to get him disqualified or in prison by the June convention).

It’s boring and its not my preference, but I think we are headed for a rematch of 2020. On the bright side, 80 isn’t what it used to be: