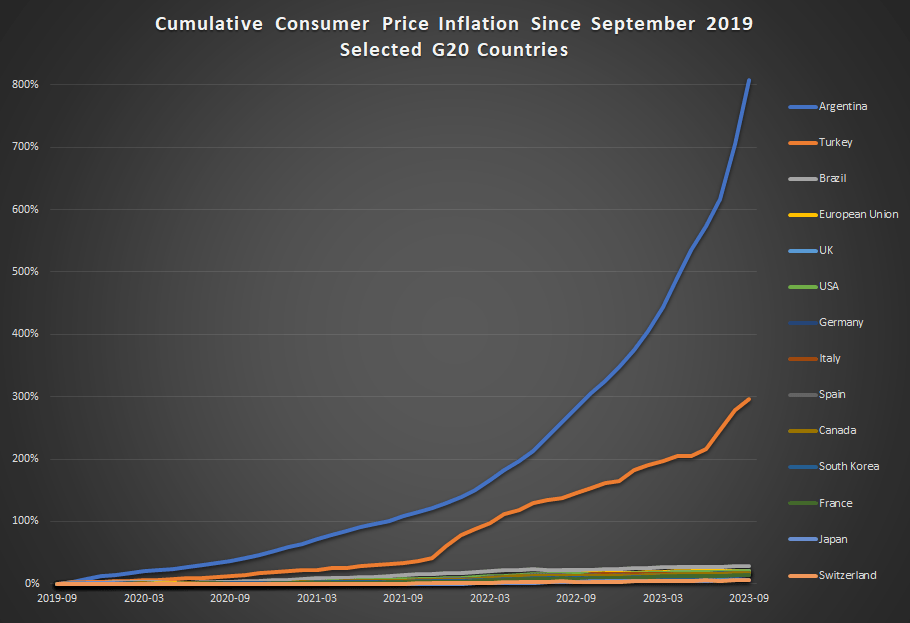

Inflation has been constantly in the news over the past 2 years, but it has especially been in the news lately with regards to one country: Argentina. That country has been experiencing triple-digit annual inflation lately, and it has become one of the key issues in the current presidential race.

How bad is inflation in Argentina? Here’s a comparison to some other G20 countries from September 2019 through September 2023 (data from the OECD).

Cumulative consumer price inflation in Argentina over the past 4 years is over 800 percent. That means goods which cost 100 pesos in September 2019 now costs 900 pesos, on average. Well, they did in September. It’s almost November now, so if the recent inflation rates persisted, those goods are around 1,000 pesos now.

Turkey also stands out as a country with very rapid inflation the past 4 years — without Argentina on the chart, Turkey would clearly stand out from the rest. But other than Turkey, all the other countries are bunched at the bottom. Has there not been much difference among them? Not quite.

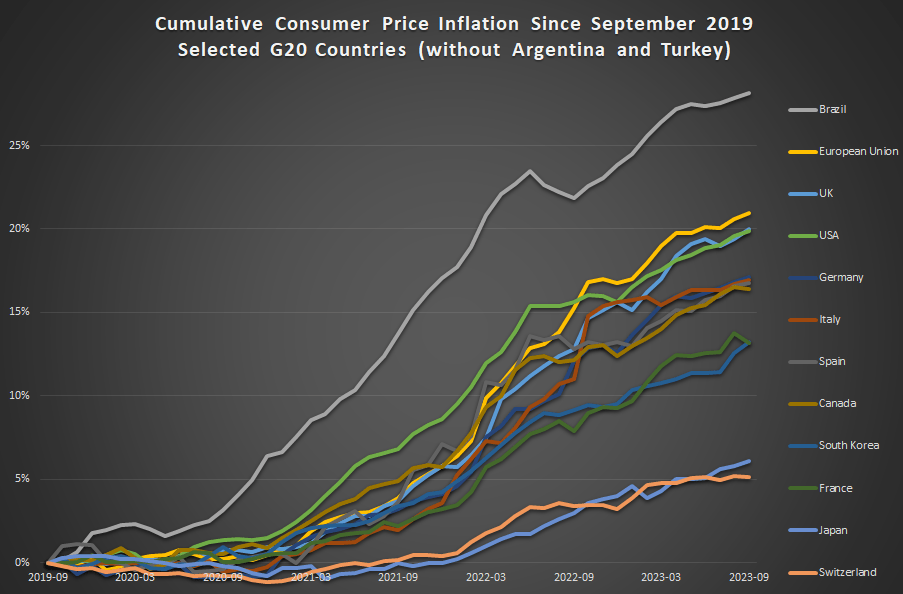

This next chart removes Argentina and Turkey:

In this second chart we see two standouts on the opposite end of the spectrum: Japan and Switzerland have had extremely low inflation, just 6 and 5 percent cumulatively since late 2019 (and this is not unusual for these two countries in recent history).

For us here in the USA, things don’t look so good. Only Brazil and the EU are higher (and the EU is mostly due to energy price inflation in Eastern Europe), so other than that we are basically tied with the UK for the worst inflation performance among very high income countries during the pandemic. That’s bad news! But perhaps one silver lining is that average wages in the US have outpaced inflation slightly: 23 percent vs 20 percent growth over this time period. That’s not much to celebrate — except relative to most of the rest of the world.

Wall Street analysts love to get out ahead and tout The Next Big Thing. Earlier this year it was Generative AI that was going to Change Everything. I am old enough to remember a surge of enthusiasm when fractal number sets were going to Change Everything (“How did we manage to get along without fractals?” was a question that was really asked), so I tend to underreact to these breathless hot takes.

Well, The Next Big Thing as of last week seemed to be the new generation of weight loss drugs. With names like Ozemic and Wegovy and Mounjaro (who thinks up these names, anyway?), these are mainly GLP-1 blockers which up till now have been mainly used in treating Type 2 diabetes.

These drugs mimic the action of a hormone called glucagon-like peptide 1. When blood sugar levels start to rise after someone eats, these drugs stimulate the body to produce more insulin. The extra insulin helps lower blood sugar levels.

Lower blood sugar levels are helpful for controlling type 2 diabetes. But it’s not clear how the GLP-1 drugs lead to weight loss. Doctors do know that GLP-1s appear to help curb hunger. These drugs also slow the movement of food from the stomach into the small intestine. As a result, you may feel full faster and longer, so you eat less.

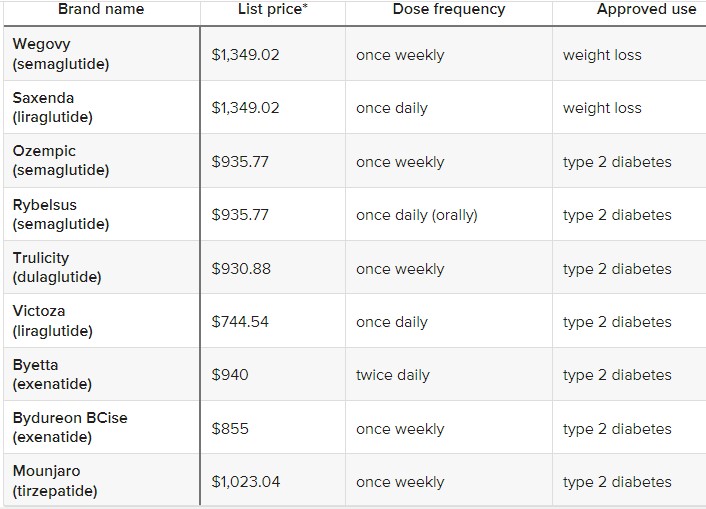

I’ll append a table at the end with a bunch of these drug names, for reference. At this point, most of them are only FDA approved for diabetes treatment, but are being prescribed off-label for weight control. It is no secret that obesity is rampant in America, and is spreading in other regions. The knock-on health problems of obesity are also well-known. So, these treatments might be very helpful, if they pan out.

What does Wall Street think of all this? Well, there is first the potential profit to accrue to the makers of these wonder drugs. You typically take them via daily or weekly skin injections, similar to insulin shots. A month’s worth of these meds may cost a cool $1000. Cha-ching right there, for makers like Novo Nordisk and Eli Lilly.

But wait, there’s more – Jonathan Block at Seeking Alpha calls out a number of possible financial angles for these drugs:

While at first glance the impact of these medications — known as GLP-1 agonists — might just impact food and beverages, the reality is that they could influence many other consumer industries.

Apparel retailers, casino/gaming names, and even airlines are just some of the industries that could see an impact from the growing popularity of weight loss drugs.

The thinking is that folks who lose 15 pounds will go out and buy a whole new wardrobe, which is good for clothing makers and retailers. On the other hand, gambling is highly correlated with obesity, so maybe casino business will fall off. There are claims that kidney health is so improved with these drugs that purveyors of dialysis equipment may be under threat.

Fuel represents some 25% of airlines’ expenses, so somebody with a sharp pencil at Jefferies sat down and calculated that for one airline (United) the cost savings would be $80 million per year if the average passenger shed 10 pounds. And who know, if people get really thinner, maybe the airlines can pack in an extra row of seats…

Analysts estimate that nearly 7% of the U.S. population could be on weight loss drugs by 2035, which could lead to a 30% cut in daily calorie intake due to the consumption changes for the targeted group. There is also some conjecture that the increased attention to dieting and weight loss in general could have a downstream impact on the consumption of snacks and sweets.

Real World Efficacy of Weight Loss Drugs May Fall Short of Clinical Trials

Throwing buckets of cold water on these scenarios of slenderized Americans is a study by RBC Capital Markets suggesting that the actual impact of these meds may be much less than indicated by clinical trials:

“Unlike clinical studies, insights from real-world use of these drugs imply weight loss can be limited or short-lived as a result, making it difficult for some users to justify the treatment’s lofty price tag,” RBC analyst Nik Modi said. “Recent insurance claims data on 4k+ patients who started taking GLP-1s in 2021 indicate only 32% remained on therapy and just 27% adhered to treatment after 1 year, citing an increase in healthcare costs.” He mentioned one study on 3.3k subjects that found after a year on the drugs, patients saw an average of just 4.4% weight loss. That is significantly less than declines cited by Novo Nordisk (NVO) and Eli Lilly (LLY) in their studies.

Also, he said IQVIA data found that the growth in GLP-1s is due mostly to new prescriptions, not refills, “making us question its sustainability.” Given this information, “we believe GLP-1s have genuine hurdles to prolonged use that have the potential to limit their long-term societal/economic impact.” To back up his argument, Modi provided several real-life examples of drugs or products where hype that it would shake up a consumer segment ended up falling flat.

The clinical trials for the GLP-1 blockers were paid for by the manufacturers, so they tend to be skewed to the positive. It is not clear whether these flattish real-world results are due to the drugs themselves not being so effective, or to other factors. These factors include side effects, unpleasantness of self-injection, and the huge out-of-pocket cost (~ $12,000/year). Weight loss drugs are often not covered by insurance, since obesity is considered a behavioral outcome, not a disease.

My guess is the final outcome will fall somewhere between mass weight loss and nothing. We hope that progress continues to be made in this area, since so many other health conditions are worsened by being overweight. For instance, fellow blogger Joy Buchanan recently linked to an article by Matt Iglesia in which he described significant and long-lasting weight loss from bariatric surgery.

And as promised, that list of diabetes/weight-loss meds:

The Republicans can’t seem to elect a speaker of the house. This seems like a classic collective action problem, where the prisoner’s dilemma is a holding everyone back as they all try to individually free ride, hold out, defect, etc. But I think there is something deeper happening here that is actually quite simple.

Republicans are struggling to take a collective action because too many of them have no interest in producing any public good at all. As Mitt Romney observed, Jim Jordan has never authored legislation nor even sponsored a bill that passed. Humans have spent thousands of years devising clever mechanisms for solving collective action problems in pursuit of public goods, but the crux has always been a public good that could be pointed towards as a point of coordination and motivation for pushing through uncertainty and personal risk. If you are congressperson who has no interest in changing or defending the body of law, then the goal of electing a speaker within your party has no interest to you. In fact, failure to elect a speaker is actually preferred if that failure is generating attention that builds awareness of you and your personal brand.

Democrats should heed the warning of what they are observing as well. A small minority of pure attention seekers can shut down an entire party at the choke points both purposefully and accidentally placed within our constitutional republic. Collective action is everywhere and always fragile, not least of all when some participants have no interest in the public goods that might be produced.

Roger Forsgren is a retired Chief Knowledge Officer of NASA. He was a director of Academy of Program, Project and Engineering Leadership at NASA. Roger is also an undergraduate with a liberal arts degree, a mechanical engineering degree… the author of … “When Graduation is Over, Learning Begins – Lessons for STEM Students and Professionals”.

In this episode, Swami & Roger discuss the importance of having a liberal arts background for an engineer, foundational skills needed for successful engineers, how communication skills, decision-making skills, and working with people are as important as number crunching, and where empathy can help achieve efficiency in an imperfect world filled with vulnerable people.

Forsgren does not see education as primarily a signaling exercise. Engineers need to know math and they learn much of it in school. Forsgren thinks of communication as a skill that can be learned, although I don’t think he would say that a traditional classroom is the only place to do that learning. Extra curricular activities probably play a role in developing social skills, and traditional school can be a good place to get that practice.

Forsgren: “I’d be wasting my time if I tried to train NASA engineers in calculus… they know it already… In the past it’s always been called soft skills [and that turns people off]… what we do is we change that to ‘professional skills’ and this is something I think is ideal for an engineer because an engineer has a choice in their career… [you can just do the analytics and math] but if you want to move ahead in your career, if you want to become a manager… you really have to develop the post-professional skills of leadership and communication…”

He has a section on former president Herbert Hoover. Forsgren said Herbert Hoover was the Elon Musk of his day. Hoover was extremely successful as an engineer, and even in some government positions relating to war and logistics. Then Hoover was a bad American president because of his poor communication skills. “He couldn’t lie… he had a hard time talking to people…”

Forsgren has a lot of patience and compassion for people who don’t have naturally good social skills. If you don’t think you are great with people, then I recommend this short blog on Lucidity (HT: Tyler) by Leber. Leber’s portrait of a husband and wife misunderstanding each other could apply to people on either side of the Israel-Palestinian conflict right now.

This makes me think of Putin’s failed assault on Kyiv. Putin has succeeded in getting many thousands of people killed, but his initial goal of the invasion was not achieved. Putin was 70 years old when he thought he could take Kyiv in 2022. He had photos in mind, but probably with the old kind of newspaper reporting and Soviet-style control over media. Now every villager holds up an iPhone and livestreams marauding soldiers. However, if you go to the Wikipedia timeline of events, you can see how important “traditional” journalism still is. Sources include the New York Times and Al Jazeera (based in Doha, Qatar). Paying for journalism affects the world. Saying what journalists “should” be doing without paying for any newspaper subscriptions has less of an effect I would think.

Alfred Hitchcock’s ‘Psycho’ famously omits graphic violence. You never see the bad guy stab anyone – though it’s heavily implied. Some say that this accounts for the impact of the film. The most thrilling parts are left to the viewer’s imagination. And a person’s imagination can be pretty terrifying. The delight of the unseen was especially appropriate at a time of 13 inch televisions and black-and-white movies. If the graphics on the screen couldn’t carry the movie, then the graphics in a person’s mind would do the trick.

Fast forward to ‘Burn Notice’. I don’t watch this show, but my in-laws do. They have a huge TV with a super high resolution. The TV has a diagonal span that almost surpasses my height. I’m short, but not that short. This is a big TV. I’ve only seen Burn Notice at their house. It strikes me as poorly acted, poorly written, and self-serious to the point of absurdity. I keep expecting that self-referential nod to the open secret that the show is ridiculous, but it never comes. It’s a bad show. From all that I can see in high definition, there’s nothing worth seeing.

What is so good that I watch? Although I’m seven years late, I’ve recently been watching Marvel’s Luke Cage. Being a superhero show, some of the standards are lowered. The script is weak at times, the acting is OK, and the plot has some credibility holes. But the point of the show is to explore a world in which superheroes exist, and one of them happens to live in Harlem. Luke Cage is part of the earlier Marvel cadre of post-acquisition-by-Disney shows that also includes Iron Fist, Daredevil, & Jessica Jones. These shows are less tongue-in-cheek and comedic than the later shows like Loki, Wandavision, or Moon Knight. I enjoy watching Luke Cage on a small 40 inch television, and occasionally on my phone.

Then I stayed at an Airbnb last weekend that had a HUGE TV. This thing easily had a diagonal measure that surpassed my height. After getting the kids down and answering emails, I sat down to enjoy my current go-to show before hitting the hay. And dang it if I wasn’t distracted the entire time. On this massive screen I could see every pore on everyone’s face and every blank stare parading as acting. I could see each and every glare of poor lighting and every character’s ill-timed reply and change of expression. Most of the show is one big charade.

Much to my dismay, I had discovered that I was watching ‘bad tv’. Let me be clear. I’m not supposed to watch bad tv. That’s the realm of those other people. But me? I have enlightened preferences and a refined pallet. I’m not a person who watches bad tv. But that grandiose self-conception has been dashed by this serendipitous visit to a nice Airbnb.

I’ve had some time to dwell on my new revelation and this is what I’ve settled on. First, I’m going to keep watching Luke Cage on my small TV and I’m going to enjoy it. There is little that I can do now about the nagging knowledge that, given a higher resolution, it’s not a good show. You can’t unknow things. Second, maybe Burn Notice isn’t a bad show. Maybe it’s just a bad show when I can see too much detail, such as on my in-law’s TV. Maybe I would enjoy it on a TV with lower resolution. Regardless, I’m not going to watch it.

Third, now I have a new margin of preference over shows and movies. Now I consider whether a show or movie would be helped or hurt by more visual detail. Quick-paced, big-budget action shows like Jack Ryan are probably better in greater detail. Game of Thrones is probably better as a 4k experience. But shows in which the comedy or the drama unfolds by virtue of the circumstances, rather than the visual spectacle, are probably best watched at a lower resolution. When the audience experience hinges on implications and connections that occur in the viewer’s mind, that’s probably a better show at a lower resolution. Luke Cage is a ‘good’ show in low-res. In high-res, I’m afraid that see too much.

When Hitchcock omitted visual detail, he leaned on the mind’s eye to fill in the gaps. He was guiding the brain toward conjuring the unnerving scenes that he could not as easily mimic on screen. Advances in home entertainment have moved the goalpost. A more detailed viewing experience changes the type of shows that we are willing to watch because we have a new criteria for fitness. The supply side response on the part of studios is that shows lacking visual stimulation will need to lean more on the mind’s eye and our interpretations of social interactions in order to for audiences to experience the best version of the show. Because the best version won’t be in front of us. We know too much.

The latest Global Valuation update this week shows that Poland (along with Colombia) has some of the world’s cheapest stocks. Their overall Price to Earnings ratio is 8, compared to 28 for the US:

Does this mean Polish stocks are a good deal, or that investors are rationally discounting them as being risky or slow-growing? After all, they had a low P/E ratio last time I wrote about them too.

Stocks can rise either based on higher investor expectations (higher P/Es) or improved fundamentals (earnings rise, investors see this and bid up the price, but only enough to keep the P/E ratio roughly constant). Over the past year Polish stocks have done the latter; I bought EPOL (the only ETF I know of that focuses Poland) a year ago because its P/E was about 6. Since then its up 70% and the P/E is still… about 6.

Why haven’t investors been excited enough about this earnings growth to bid up the valuation? I think the biggest concern has been political risk, given that the ruling Law and Justice party has been alienating the EU and arguably undermining the rule of law and finding pretexts to arrest businessmen critical of the government.

The recent Polish election promises to change all this. A coalition of ‘centrist’ opposition parties won enough votes to oust the current government, and Washington, the EU, and business seem relieved:

As Europe’s sixth-largest economy, a revitalised pro-EU attitude in Poland would be particularly welcome.

“It will be a positive development for sure because it will unlock the (EU) money that has been withheld and reduce a lot of the tension that has been created with Brussels,” said Daniel Moreno, head of emerging markets debt at investment firm Mirabaud.

Some 110 billion euros ($116 billion) earmarked for Poland from the EU’s long-term budget and the post-pandemic Recovery and Resilience Facility (RRF) remain frozen due to PiS’ record of undercutting liberal democratic rules.

The case for optimism is an influx of EU funds, less risk for business, and an appetite for higher valuations among Western investors who no longer dislike the government.

Being an economist I also have to give you the “other hand”, the case for pessimism: the new government hasn’t actually formed yet, meaning the current one still has the chance for shenanigans; population growth has been strong recently with the influx of Ukrainian refugees, but it is likely to go negative again soon; and EPOL is almost half financial services, which have relatively low P/E even in the US right now.

Nothing is guaranteed but this is my favorite bet right now. I find it amusing that this “risky” emerging market has had a great year while “safe” US Treasury bonds are having a record drawdown (easy to be amused when I don’t own any long bonds and they have done surprisingly little damage in terms of blowing up financial institutions so far). I emphasize the investing angle here but hopefully this signals a bright future for the Polish people.

Disclaimers: Not investment advice, I’m talking my book (long EPOL), I’ve never been to Polandand I’m judging their politics based on Western media reports

On X.com Matt Yglesias posted a chart that sparked some conversation about child safety:

One thing about the much-lamented rise of more intensively supervised childhood activities is that kids have in fact become a lot less likely to die. pic.twitter.com/MTjR7spLM8

Of course, it was probably more his comment about the “rise of more intensively supervised childhood activities” that generated the feedback and pushback. And I assume his comment was partially tongue-in-cheek, as often happens on Twitter, and designed to generate that very discussion. Still, it is worth thinking about. Exactly why did that decline happen?

I’ve posted on this topic before. In my March 2023 post, I looked at very broad categories of child death. While all death categories have declined, about half of the decrease (depending on the age group, but half is about right) is from a decline in deaths from diseases, as opposed to external causes. And fewer disease death can largely be attributed to improvements in healthcare, broadly defined. Good news!

Of course, that means that about half of the decline is from things other than diseases. What caused those declines? Let’s look into the data. Specifically, let’s look into the data on deaths from car accidents.

What is the VIX and why should you care? The CBOE Volatility Index (VIX) is a measure of the expected near-term price swings in the S&P 500 stock index (SPX). The VIX value is derived from the prices that market participants are willing to pay for options that expire roughly 30 days in the future. Typically, movements upward in VIX correspond to movements downward in broad market averages, since price volatility is usually associated with some “problem” cropping up. During market turbulence, the VIX can shoot up very high, very fast, with a percentage of change far higher than for stock prices.

The VIX is know as the “fear gauge,” since it provides a standardized measure of market volatility expectations. It is thus a number that conveys significant information about the attitudes of market participants. Also, it provides opportunities for investors to make (or lose) a lot of money quickly. You cannot invest directly in the VIX (it is just a calculated number), but you can buy/sell VIX futures and options on those futures. Also, there are convenient funds that buy (e.g., VXX) or short (e.g., SVIX) the VIX futures. Because the VIX makes much bigger percentage moves than stock themselves, you can make a killing with a modest investment, providing you get the timing right.

For instance, over the past twelve months, the SPY S&P 500 fund has gone up by about 18%, so $10,000 would have gone to $11,800. That’s pretty nice. But in that same period, SVIX went up by 143%, which would take $10,000 to $24,300 (see below). (Nerdy notes: (a) SVIX shorts the VIX, so it generally goes up when VIX goes down, i.e., when stocks go up. (b) There is another factor with SVIX called the monthly roll, when tends to make it rise something like 2-4% a month on average. This monthly roll factor is layered on top of the rise and fall in SVIX value based on VIX level. So even if VIX is flat, SVIX may go up something like 30% in a year. )

SVIX and SPY share prices for the past year. Source: Seeking Alpha

Of course, the price swings on SVIX cut both ways. It is down hugely from its highs a month ago, as VIX has increased from roughly 14 to 20. You can go even more crazy by purchasing/shorting VIX-related funds like UVXY that are leveraged at more than 1.0X.

Even you were even more clever, you could have made even more, much more, by working VIX options. Also, if you just want to hedge your stock portfolio against sudden drops, it is often more economical to do that by buying (call) options on the VIX, than by buying (put) options on the stocks (e.g., SPX, SPY) themselves.

During long periods of market stability, the VIX tends to slowly drift downward, to an asymptote somewhere in the 12-13 range. For example, in the five-year plot below, VIX spend much of 2019 around 13, then shot up over 80 within a month when the scope of the COVID pandemic became apparent. It then drifted downwards (with many spikes along the way, especially during the big bear market of 2022), getting down to around 14 for much of June-September of this year.

VIX Level for past five years. Source: Seeking Alpha.

It is notable for VIX to be this low, considering a number of serious current market concerns (the relatively high valuation of the stock market, stubborn inflation, hawkish fed, gridlock in Washington, etc.). And now with serious conflict in the Middle East resulting from the massive attacks on Israeli civilians, the VIX has so far only risen to 20.

A number of market commentators have noted the seemingly anomalously low level of the VIX, and have proffered various explanations. They observe that macroeconomic outlook continues to look probably OK. They also point to some fundamental changes in the stock market operations. One factor is the rise of zero-day options, very short-term stock options that expire within one day. More of the speculative action has gone to those options, with proportionately less in the month-out options that drive the VIX.

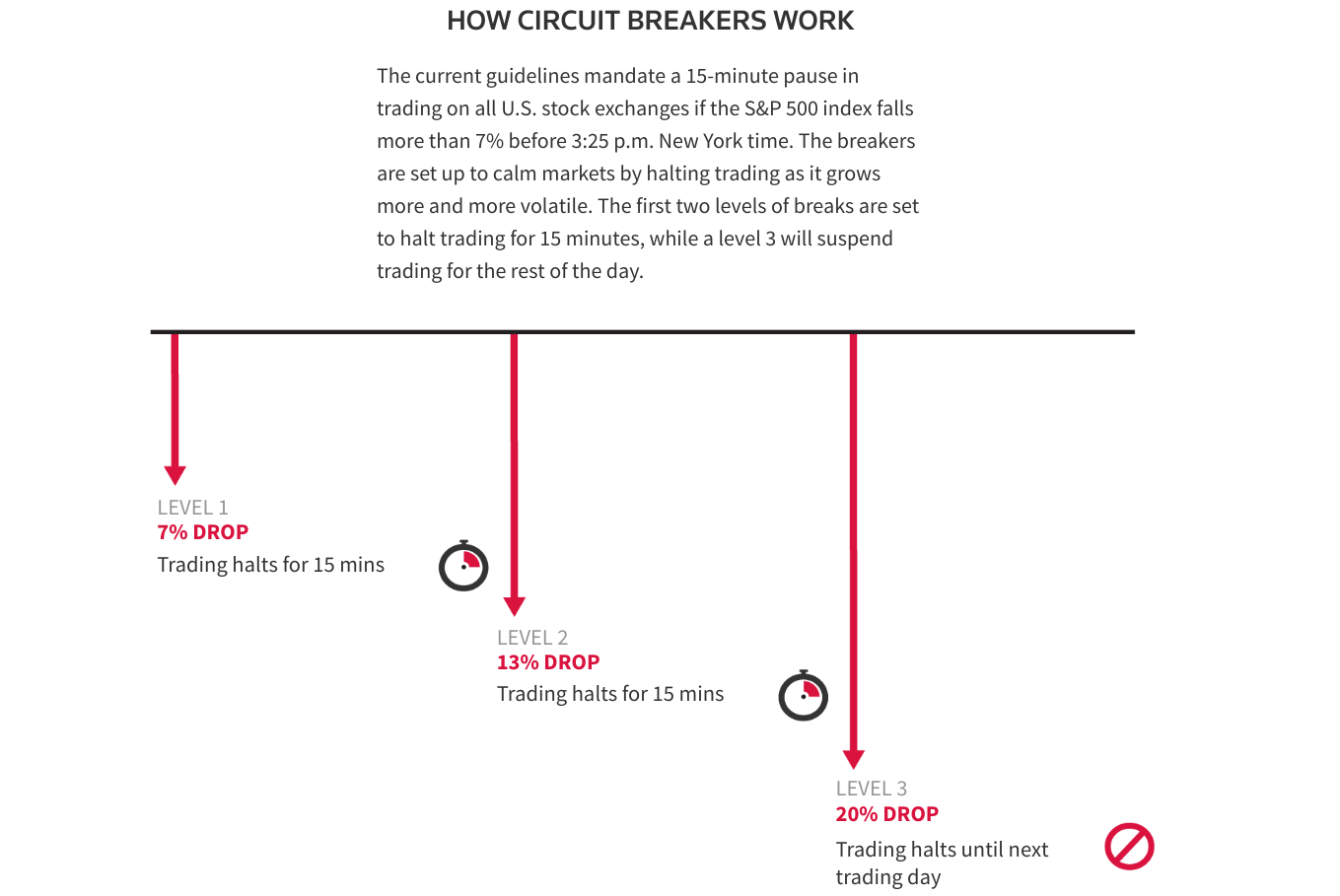

Also, the stock exchanges have implemented various “circuit-breakers,” which halt trading for specified time periods, if swings in stock prices get out of hand. This gives participants a chance to cool off and recalibrate, and not have to make frantic, quick (possibly losing) trades in order to protect themselves. Here is a diagram illustrating these circuit breakers, which are triggered by big moves in the broad S&P 500 stock average:

Source: Seeking Alpha, article by Christopher Robb

There are also Limit Up/Limit Down (LULD) rules in place that temporarily halt trading in an individual stock if its price swings exceed some designated band. is designed to stop excess volatility in a single stock. With these protective circuit-breakers in place, market participants seem less worried about huge price swings coming at them, and hence may feel less of a need to “buy insurance” by purchasing options. This suppression of stock option prices in turn leads to a lower calculated VIX.

As usual, this blog post is not meant to be advice to buy or sell any security. (And seriously, the “never bet more than you can afford to lose” rule applies doubly with the high-volatility products discussed here).

For those earnestly interested in addressing issues surrounding firearms in the United States (and not just aligning with a political coalition), this working paper from Moshary, Shapiro, and Drango (MSD from here on) is an absolute must read. The technical moves are an interesting overlap of industrial organization economics and marketing analytics, but the punchlines all hit on the same topic: how do current and possible future firearms owners respond to prices for different products? When MSD estimate the price elasticities for different firearms, they are in effect asking one of those deep questions in economics that is always lying below the surface: are these goods substitutes?

It’s uncanny how much of the disputes within economic policy and regulation come down to how one defines substitutes. Is Coca-Cola a monopoly? Well, that depends on whether or not you think Pepsi or water is a close enough substitute. Should vapes be banned? That depends on how much demand you think will shift over to traditional cigarrettes. No matter your thoughts on marijuana legalization, I promise you the marketing and lobbying wings of the largest alcohol distributors have invested a lot in determining if cannabis is a substitute for their products (spoiler: it is).

Should assault weapons be banned? I am on the record as saying they should be, but the results in MSD give me pause. The bulk of firearms deaths are from handguns, and the bulk of people in the market for an assault rifle point to a handgun as their next-best alternative if an assault rifle is not an option. Would an assault rifle ban have the unintended consequence of pulling more handguns into the market and, in turn, create more firearms deaths?

This is not an easy question to answer because we haven’t actually taken the time to define the good. And by define the good, I mean define the bundle of attributes actually being purchased. The most obvious attribute of a firearm is the ability to point it at a living creature and take away its entire future. That it is such a chilling capacity that we sometimes fail to fill in the rest of the ledger. Firearms are a source of personal security, no small detail for isolated individuals. They are a means of pest control, an absolute necessity for anyone farming or raising smaller livestock. They are a way of signaling your group identity to others. Of affirming your idependence and strength. They are collectable, both as historical vintages and customizable baubles. They are highly effective at hunting game. They are fun to shoot at targets.

All of that means that when we consider banning, regulating, or taxing a specific class of firearm, we have to think really hard about the bundle of attributes being purchased and consumed, and what the next best alternative is for each customer shifted to a different product on the margin. The outcomes are perhaps more unpredictable than is often considered. Who is the marginal customer and what exactly is it that they want?

Consider a ban on assault rifles. Some will shift their demand to the black market. Despite the obvious danger in a group of individuals who illegally purchase high power firearms, we can actually ignore them at this stage because there’s no option where they don’t acquire assault weapons. What about the rest? Some are desperate to protect their homes. Hopefully they will be easier to persuade now that a shotgun is their best option (pro tip: it always was). Some want to maximize their capacity to do harm: absent maximal power, they may now opt for concealability and mobility i.e. a handgun. This seems like a particularly viable story in states that allow for the carrying of concealed weapons in public with or without a license.

Some, however, might view their $1200-$3000 might be better spent putting a snorkel on their jeep engine ($700), a bowie knife on their hip ($250), and bottle of Michters Single Barrel Whiskey on their shelf ($500*). Maybe they’ll blow it all at once on a lift kit for their truck. We can rest assured that the marketplace will offer no shortage of goods that offer little value save for people to impress their friends with what they just bought, which is a blessing. Substitution to tactical sunglasses and raunchy mudflaps is unequivicably preferable to more Glock 19s.

What about a ban on handguns? Here MSD identifiy an important asymmtry: customers in the market for a handgun don’t consider long guns, while would be purchasers of long guns frequently explicitly consider a handgun on their 2nd choice. From the point of view of minimizing firearms deaths, a ban on handguns may be optimal, but it is hard to predict what the substitutes will be. Based on their measured elasticities of demand for different types of guns, MSD estimate that a 10% tax on all firearms would have the same net effect on total firearms in the market. Perhaps most importantly, it is highly unlikely to backfire into a shift in market composition towards assault weapons, something that can’t be ruled out by a handgun ban. Combined with current political realities, a tax on firearm would appear more feasible than any broad class bans.

For a large, but not unanimous, share of social scientists studying firearms, the outcome desired is 1) a smaller fraction Americans with access to firearms, and 2) reduced capacity to commit large scale acts of violence with high powered firearms. Putting aside any disagreement on the desired outcomes, the policy steps forward still allow for meaningful uncertainty. Yes, I know that heavily restricting firearms in Australia has been wildly successful. It’s hard to argue with a total homicide rate roughly a tenth of the US rate. But we can only consider the policy options that are actually on the table and the voter status quo. Current options are likely limited to either a narrow ban on a subset firearms or a modest tax on them all. The status quo is one where a third of all Americans own a gun, 81% of whom feel safer because they have one.

Given these unavoidable constraints, good firearms policy (not optimal, merely good) requires knowing what it is that people are buying so we can tilt the playing field in the right way. We live in a world where politicians are sending AR-15 toting Christmas cards and pantomime tough guys are ordering their Subway Chicken Teriyakis while armed to the gills. There’s no policy prescription that’s going to magically create earnest politicians and emotionally secure men, but everyone responds to prices.

*I apologize to fans of Michters, I just don’t like their bourbon very much relative to the price. If you want to impress your friends, track down a bottle of William Larue Weller. It’s expensive, but it might be the best bourbon in the world, and that includes all of the Pappys.**

**Okay, its not as good as the Stitzel-Weller Pappy 20 I first tried in 2011. That’s still the greatest thing I’ve ever consumed. But that doesn’t exist anymore as far as I know or could hope to afford. My advice is to let it all go and just buy a bottle of Four Roses Single Barrel. Always less than $50, always fantastic.

{kind=link}